TwoCitiesCapital

-

Posts

6,303 -

Joined

-

Last visited

-

Days Won

10

Content Type

Profiles

Forums

Events

Everything posted by TwoCitiesCapital

-

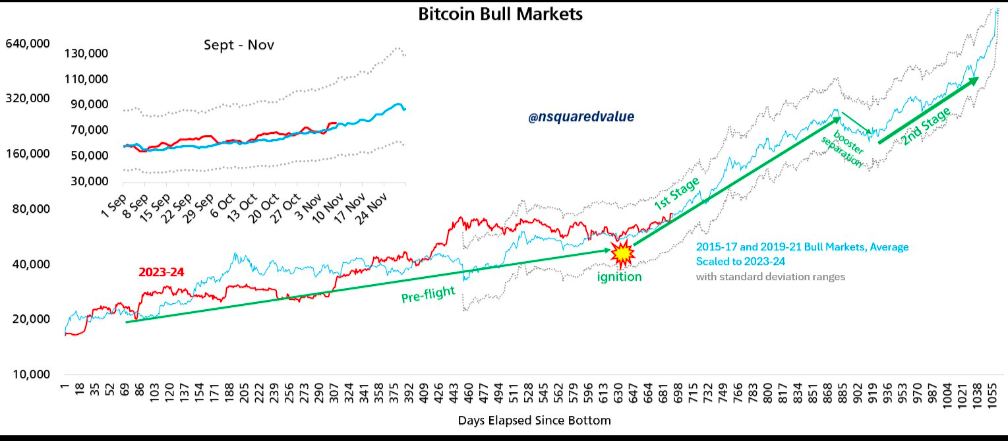

Re: the cyclicality and predictability of crypto Tim Peterson has been posting and updating this chart for a few months now So far has been amazingly accurate at predicting current price movements, and when they occur, by analyzing the average of prior cycles. Its hard for me to imagine what kind of capital requirement are needed to flow into the industry to get to $500-600k this cycle, but maybe it plays out the same way again. Watch out for that mid-cycle shake out though. That 50%-like drawdown is gonna be a doozy

-

Rolled out of positions in BITU in exchange for IBIT Leaps. Near similar 2x leverage but without the decay on down days eroding overall total return over the life of the option. Have a number of bull put spreads on BITO expiring between now and December. Will rolls those to IBIT options too. Love the idea of being able to sell covered calls against my core IBIT position to generate income as well, but will wait for the market to get real forthy before giving up the upside.

-

I don't think volatility justifies significant premiums to NAV and am highly skeptical of the "infinite money machine" people believe Saylor has found. That being said, it's not as dumb as paying million for monkey JPGs and we've seen that in the crypto space too, so anything can happen I suppose. I prefer the straight exposure without the basis/dividend risks and I expect most directional traders will as well. If you're just capturing volatility risk premia? Then there are dozens of options outside of IBIT that may be better at any given time

-

IBIT options are also more volatile than BTC itself. And have no basis risk. There are scenarios now where MSTR price could fall even while BTC rises or vice versa. IBIT options allow you to cleanly play the thesis or hedge without that risk

-

Will be huge IMO. Allows you leverage without having to pay 3x MSTRs NAV, the negative roll yield often accompanying futures contracts, or unexpected dividends that reduce the likelihood of the strike being hit. So better than all other alternatives and will absorb that capital.

-

As someone who played with ETH and DeFi on 2021, the potential seems to be there. But the fees killed it. You want to deposit your crypto at in a dApp and earn interest? You pay to permission the dApp to spend the crypto (each crypto), then you pay for the actual transaction, then you pay when you want to change the balance or claim the rewards or withdraw. Often times fees are $5-10/apiece pending how high demand is and how intensive the transactions are in computing power. The way they fixed this? Via multiple layer 2 solutions that didn't talk with one another and required another set of hefty fees (at the time) to get onto and off of along with 5-10 day type settlement periods. Pair this with rug pulls, unscrupulous actors, hacks of legitimate dApps, and legit dApps that just seized activities forcing you to transact, it was too much to navigate while prices were falling 90+%. I think things have improved slightly since then, but not enough to get me re interested. ETH ecosystem seems roughly the same as it did 3 years ago, but BTC has continued to power forward.

-

This isn't true - at least not in the traditional sense that would matter to common/preferred shareholders who would be expected to be entitled to that 'net worth'. They're accruing 'capital' - but every $1 of retained earnings is offset by a $1 increase in the Treasury's liquidation preference. The retained earnings are NOT owned by the companies nor the shareholders - it is owned by the Treasury

-

Or gold. Fixed income's problem is when interest rates fail to exceed inflation. Gold primarily does well when interest rates fail to exceed inflation. It's a natural hedge and a natural substitute to nominal bonds without the duration impact of TIPS offsetting the inflation adjustment. It has complimentary risk factors to fixed income while also regularly serving as a "risk off" investment so I typically consider my gold allocations as part of my fixed income portfolio and used it as a substitute for long-bonds back in 2021/2022. I personally have a position limit of 10% of my net worth (not necessarily my portfolio) on any 1 stock. And the stocks that I tend to take it there themselves are more conglomerates like Fairfax or Exor - so perhaps I could afford to loosen that some and bump it to ~15% for diversified companies. I've just had many large positions go against me while my small ones tended to do best so I was trying to correct for the error of overconfidence and equal weighting which would have seen me do significantly better earlier on in my investment career. The way I've always characterized it is that concentration is for wealth building...if you're right...and diversification is for regret minimization if you realize you could be wrong. I try to straddle a middle road. I concentrate 5-10% in each of a handful of names and diversify the rest.

-

I own a hair. Just a small amount left for my forays into DeFi. Would be the wrong point to sell it IMO. Long term I have few thoughts on ETH, but historically we're approaching what would be the time when ETH starts outperforming BTC.

-

It's not a Trump rally. It's the traditional post-halving rally that has happened every 4 years regardless of who was elected. It just happens to coincide with the election cycle this time around. Historically Bitcoin has gone vertical ~6 months post halving. Halving was in April. October was 6-months after that. If it plays out like prior cycles - it'll rally for 10-12 months and a face melting vertical climb with some major 30-50% pull backs along the way. Eventually this cycle will break - enough people will front run it to void the prior trading history. But every cycle people say that is going to happen then it plays out the same so waiting for it to break rather predicting when it will.

-

Fortunately for me, I bought a slug @ $12k and DCA'd all the way down to $4k and bought all the way back up to $40k over that period. Back then $500-600 still bought an appreciable amount of BTC . Unfortunately, there were set backs like losing 0.5 BTC in the Celsius bankruptcy and diverting my attention away from BTC accumulation to DeFi and altcoins, but Bitcoin covers a multitude of portfolio sins. At this point, $500-600 is dropping pennies in, but pennies I expect to compound at 40+% per year.

-

Yes. How you size it is up to your risk tolerance. What you sell to fund it is up to you as well. I hold both BTC and Fairfax. BTC is weighted far higher and Fairfax is by far my largest equity position. I recommend starting with a reasonable slug, committing to a DCA schedule either biweekly or monthly, and then have the patience to wait 3-5 years for a whole cycle to play out. The downdrafts are stomach turning, but acceptable with how quickly this compounds. I put $500-600 in every 2 weeks and have for most of the last 4-years. I put another 10-15k in during October to be opportunistic with the rally I expected shortly thereafter. I buy both BTC directly (via Coinbase and stored on a hard wallet) as well as BTC in my IRAs via the ETFs. I don't try to time the tops and bottoms, but I do have targets for when I reduce/eliminate my DCA and targets I'd be willing to let go of a minority of the position in my IRAs go for. We didn't hit those targets last cycle - we may not hit them this cycle - and that's ok with me. Because we'll hit them next cycle and I'll have more BTC.

-

We may not be quite at 100k yet, but its damn close enough to take the victory lap with 7 weeks left in the year. To be clear, this prediction was made when BTC was @ 61k. It wasn't an guarantee, but was very probable given the valuation of the network, where the price was trading relative to network value at that time, and how BTC has behaved post supply halving in the past cycles. This is the informational edge @james22 is referring to - it's still easy.

-

It reminds me of BTC in 2013, 2017, and 2021.

-

The value is in the scarcity of their cars. If people bid up the shares, issue shares to meet the demand. Buy them back opportunistically. Is a better solution than selling the shares, paying taxes, and losing control of irreplaceable asset.

-

Bitcoin is the representation of the network and required to interact with it. Figure out the value of the network - that's your market cap. Bitcoin is just an arbitrary division of that network into 21 million parts similar to how the # of shares outstanding for a corporation is largely arbitrary and what matters is not the share price of each share but the value as a whole. Value of the network divided by coins outstanding. An agreement that the US government regularly defaults on by actively diminishing the value of the currency that is their liability. How much is a contract worth if one side is constantly breaching the terms of it? Don't all assets have deviations from "fair value"? Or at the very least different estimates among participants of what "fair value" is? I'm not entirely sure I'm understanding what is questionable here? He acknowledges it was manipulated in its infancy back in 2011 -2013. And that's not universally agreed upon. But yes - any micro cap stock can be manipulated. BTC was no different in its infancy. Limited liquidity. Limited regulatory over sight. Limited market participants. That's not the case today. +1

-

So we're saying Paulson has a better moral compass than Trump? Because that's basically all this hints at.

-

I suppose that it depends on how one defines "intrinsic value". There is little value in BTC itself - the value is in the network (using Metcalf Law framework). I don't think this is irreconcilable with other theories/values nor is it much different than saying "gold has little intrinsic value - most of its market cap is monetary premium" I believe BTCs characteristics lend itself to obtaining a monetary premium - but that only occurs if the network grows through collective agreement. There are varying estimates of how much has been lost. As of right now, most estimates suggest 3-4 million to be irretrievably lost. If you want to be conservative, use the 21 million hard cap in your valuations. If you want to be more accurate, but have less margin of safety, use 17-18 million.

-

+1 It was reading about the history of money, how societies exploited less-hard currencies, and how the world eventually agreed on silver/gold independently through multiple failed alternatives is ultimately what led me to evolve my views of BTC as just a payment network to understanding its use as a store of value/currency. The history didn't even have a pro-Bitcoin bend. It simply demonstrated that universality of harder currencies absolutely dominating lesser ones regardless of politics/policies/etc and that those who adopted the harder currencies, or 'shorted' the exploitable currencies, massively benefited from the expanding monetary premium. Once you understand that, and understand that Bitcoin's characteristics are the hardest currency characteristics we've known, the conclusion is natural.

-

Timothy Peterson of Cane Island Digital has pioneered the use of Metcalf's Law for Bitcoin. https://papers.ssrn.com/sol3/cf_dev/AbsByAuth.cfm?per_id=2848613 This is my preferred valuation tool based on network use and adoption. Plan B is credited for popularizing stock-to-flow for Bitcoin, but its a theory that was applied to many commodities beforehand. You can find his material on YouTube/Twitter, but probably can just google stock-to-flow. This is a supply-side model only and will eventually break as BTC's stock-to-flow approaches infinity (when the halving cycle ends and the network operates only transaction fees) - but is probably still useful for now while the stock-to-flow is comparable to gold/silver/real estate/etc. Giovanni Santosasi popularized the use of power-law for Bitcoin. This is very similar to the stock-to-flow model for the first 10-years or so of BTCs history, but is diverging to the more conservative side of valuation. This, again, is probably due to stock-to-flow trending towards infinity and becoming less useful over time. Other than hearing interviews on podcasts, I haven't personally googled/read Giovannai's stuff to link you. But you can google him.

-

My hope would be similar to my hope for Exor and their Ferrari position. I don't necessarily want Exor to sell Ferrari when Ferrari's valuation is stupidly high. I want Exor to exert its majority control to compel Ferrari to issue shares/capital at those levels. It's not as clean as a share sale and probably doesn't lock in as much of the upside, but it avoids taxes, maintains a control position (assuming you don't get diluted too much), and puts in a higher-floor for the Ferrari shares while giving them balance sheet flexibility. I would hope the same for Fairfax/Digit until the market is more mature.

-

There are cohesive answers earlier in the thread where this has been discussed. Stock-to-flow, Power Law, and Metcalf's Law are three such theories. One is a mathematical relationship observed in often in nature, one is a supply side function, and the other is a demand side function. Neither will give you the exact right answer or the whole picture. But all suggested BTC was cheap this year and is going dramatically higher in the next year due to the continuation of the trend, the continued decline in the stock-to-flow, and the projected demand growth on the network.

-

And the Republicans did it to Iraq and others before them. Our foreign policy has been atrocious regardless of party. Trump might be a slight improvement here, but I remain to be convinced. Yes. There are attacks from the left. But the right is no better and arguably more dangerous IMO. The media is far from perfect. But as of right now it is only Fox that has paid the largest settlement in history to avoid going to trial for knowingly lying for clicks and eyeballs. Additionally, Elon has taken over Twitter and is doing the exact things he complained about the prior board doing, but to elevate his voice, his conspiracy theories, and to quiet the dissenters against himself. All media is propaganda. But the way the left tends to propagandize is through silence on a topic. The Right does it by outright lying. I view both to be bad, but one is worse than the other. The left could use a dose of respect for self responsibility. So could the right - because they're all about it until they were hamstrung by the political climate, or unfair competition, or immigrants willing to work more cheaply, or the election being stolen, etc etc etc Same. I'm fairly center and primarily voted independent or right until Trump came into the picture. Now I support candidates on the left not because the policies are better but because they aren't absolute terrible people help bent on power by any means necessary like most MAGA Republican politicians seem to be.

-

That's pretty common with European companies

-

On this note: https://www.nytimes.com/2024/11/09/us/politics/donald-trump-ethics-transition.html