TwoCitiesCapital

-

Posts

6,302 -

Joined

-

Last visited

-

Days Won

10

Content Type

Profiles

Forums

Events

Everything posted by TwoCitiesCapital

-

It doesn't bother me. They can elect to pay in cash or shares. Them electing to pay most in cash sits well with me. While I'd prefer they not use any shares, using shares that were purchased at an average price of $14 and then being redeemed at higher values could be argued to be better than paying in cash - particularly if you're looking to preserve some liquidity for upcoming deals. The fee was a much larger issue after they IPO'd. They were still unproven, it was trading at a significant premium to its NAV, and the fees are high. Now, we have a demonstrated track record, and asset trading at what we estimate to be a significant discount. The fees are high - but they are known - and haven't yet prevented the results from being decent. Only Mr. Market keeps giving us the opportunity to buy a proven team for the price of a mediocre one.

-

Anyone able to do the math on what a Japanese investor hedging USD/yen can expect to make ona 10-year treasury? I have a bunch the move in Japanese rates has made US bonds quite a bit less attractive to the #1 owner of treasuries, but I don't have ability to check currency forward prices.

-

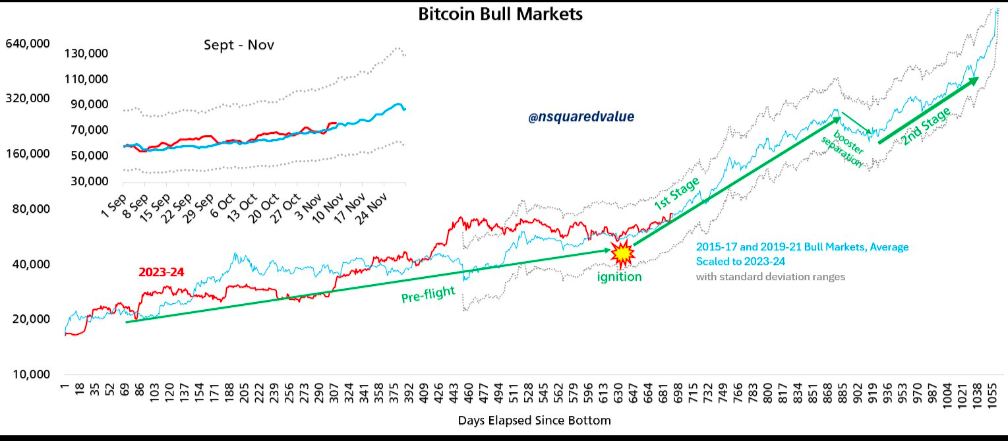

+1 If this is the supposed IPO-like activity for BTC, then you'd think large holders who've been in for decades will reach a price where they are no longer comfortable selling and the supply dries up. There hasn't been a large rush from retail this cycle and so we shouldn't be seeing large panic exits either. It's not uncommon to get 50% corrections in the later portion of the BTC cycle. We didn't get an euphoric 100% months though so I don't expect any 50+% corrections - but perhaps ~30%ish is to be expected. Or maybe we get the 50% anyways... +1 The primary part that is "abnormal" is that it is occurring during a period where BTC is typically seasonally strong and at the end of the post-halving year which has historically been where the bulk of returns have been made....and we're negative YTD. I always knew the 4-year cycle narrative wouldn't hold, but there is statistically significant data for October and Q4 specifically that makes it strange to be occurring now - especially when it was preceded by a euphoric rally.

-

I'm not sure it would be known - someone will hack the keys to the coins and have the permission to send them like the owner who previously owned the keys and lost them would have. Or maybe you get white-hat hackers who help people quantumly recover lost coins. Either way, just assume 21 million outstanding and you have no problems.

-

I disagree. I think it was clear to most who expected a mass adoption that these were natural developments. There's also quite a bit of analysis out there re: on chain movement of old coins and it's not a ton and doesn't seem to explain the general sentiment and bucking of the seasonal/post-halving trend. I don't have the ability to review/parse the data myself, so hard to say which is true. But Willy Woo has commentary on this saying much of the old coin movement has been wallet to wallet (possible house-keeping, i.e. moving to more secure wallets less susceptible to quantum hacking) and not to exchanges where volumes of BTC inventory are still falling. Probably the same thing as holders who bought in 2016. And 2019. And 2021. And etc. The reason it has gone from 0 to $100k is because over time more and more people have found conviction in it and ridden out the bear markets. I'm class of 2019 myself.

-

Most disappointing bull market, but still within the established 2-year trend. Hard to know if this 'Uptober' disappointment along many subscribers to the 4-year cycle throwing in the towel now that we're at the end of ~4 years will lead to the next bear market without a blow-off top or if that capitulation is what is setting up the blow-off top. I guess nothing to do but wait and see...

-

Perhaps it's just volatility. For instance, did anyone expect Eurobank to double this year after a long stretch of already good returns? Did anyone expect CLF to drop by 50+% after buying Stelco? A good chunk of the variability is just natural variability in interest rates, equity values, and catastrophes (or lack thereof). When I think about earnings, I'm often "averaging" out or "smoothing" over a longer time frame and could be dramatically off on any one quarter.

-

Not if price remains static. The price is what moves to balance the sellers/buyers. So it isn't incorrect to characterize more sellers than buyers if the price is dropping - it's dropping to incentivize a buyer to step in for an active seller so it is balanced.

-

So when BTC becomes digital gold used to spend/collateralize the digital economy, it's market capitalization will only be $3 trillion vs gold approaching $30 trillion?

-

+1 I asked it which of my three goalies I should start for fantasy hockey - it's reasoning was because Sorokin wasn't even scheduled to leave up. And yet, when I went to go check myself, Sorokin was confirmed as the starting goalie. Grok later confirmed with additional prodding/prompting, but was clearly wrong the first time on something easily verifiable. Data centers will need to be insured. System-wide FSD will need to be insured. Catastrophic failure of the system resulting in 100s of accidents at once will need to be insured. Etc etc etc. I don't see the premiums falling as much as changing hands.

-

Buying back insurance subs and buying out minority partners in their equity investments are akin to share buybacks. Buying back Brit and increasing ownership in Gulf Insurance Group are both akin to buybacks - each share fo Fairfax now gets more of the profits from those subsidiaries. Same with transactions like potentially taking KW private and increasing stakes in each of their private equity investments. They decrease minority interests and increase the pass through of profits per share all things equal. Fairfax has been engaging in both and you have to credit them for both when discussing buybacks.

-

Can you imagine where BTC would be if all the BTC Treasury companies hadn't sopped up the capital? Every share issuance wasn't 100% interested - and then you have to minus liquidity for dividends/interest, investment banking fees, etc. Every dollar in MSTR and others yielded significantly less than $1 moving into BTC. Had all of that capital simply flowed to BTC at NAV, bought it and held, this probably wouldn't be the weakest bull market/weakest post-halving year in history. But retail had to talk themselves into how paying 4x for the open market price of an asset made sense and now we suffer the consequences of that capital being eviscerated as the Treasury companies themselves have cratered.

-

I think Fair and Friendly is misleading and can be interpreted in many ways. For instance, Watsa could say it was "Fair and Friendly" to announce the acquisition at a large premium to the prevailing price instead spending weeks/months of privately buying whatever they could in options/open markets before forcing a take-under for the remainder with a surprise announcement for the rest. Or KW could have tipped Ackman off to buy a ton of stock with the agreement to vote in favor of the agreement to ensure it went through to further screw minority shareholders. We've seen instances of both from others, and this is certainly more "fair and friendly" to existing shareholder base than those options. Ultimately, you should expect that when minority interests conflicts with Fairfax's interests, Fairfax will win out. That doesn't mean it isn't "fair or friendly" - just that we all have different interpretations of where the lines Fair and Friendly are drawn and Watsa doesn't owe you your interpretation. so maybe best to ignore "fair and friendly" and just simply think of it as they have more integrity than most but will still act in their own interest.

-

I hope they offer more than a 30% premium for that one

-

You can assume it's a risk, but probably a remote one. Fairfax believed it was worthwhile to collect public capital for investment in India. Fairfax probably also saw value in the revenue stream. I don't see why any of that has changed - particularly with the sizes of deals they're discussing now with things like IDBI bank. Probably best and easiest to have some combination of temporary private and permanent public partnership and Fairfax India gives them that public part. People had all sorts of excuses for why it deserved a premium at IPO. Now there are all sorts of excuses for the discount and why it should be private. Ultimately, I think it's just sentiment and that it'll eventually have a premium again - maybe after the BIAL Ipo

-

Overall probably turns into a good deal sourcing for fixed income and saves them on fees. I like it. Not to mention it'll bump up their equity holdings in KW to YTD highs marking BV up YTD.

-

+1 I repurchased the small portion of the position I sold earlier this year today at $1,565 to get in before earnings which I expect will still be strong. Saved $50-150/SH on the lots sold. Not a home run by any means, but always nice when a roundtrip works out. Always nice to know Fairfax is likely still in the market with this NCIB sopping up the liquidity from weak hands during these types of markets. Hopefully price recovers some before YE when Fairfax will have a few truckloads of cash to be delivering to TRS counterparties otherwise. ~$330-$350 million at todays count.

-

Eeesh. Repurchase high and sell low....

-

Is Europe becoming uninvestable?

TwoCitiesCapital replied to lnofeisone's topic in General Discussion

+1 Just like Mississippi may have reasons to want to leave the US.... But it won't thrive if it does.... Reasons =\= better outcome -

Bitcoin dramatically underperforming prior bull market trends, but still within the two-year trend. We may still see $150-160k by year end despite an incredibly muted post-halving year/October.

-

Technically I judged it before needing the rear view mirror. I sold 100% of my shares in 2018 when it was clear that rates were coming down, Fairfax had missed the boat, and nothing in the foreseeable future could justify the $550/sh it was trading at because earnings weren't going to do it. I also made posts in 2021 about Fairfax being stupid cheap when rates had nowhere to go but up and that it was clear we were at trough earnings for all insurance/bonds/equities and that it was dumb cheap at $300-400/share. It's just strange everyone views their bond plays differently than their equity plays - they're all macro bets. Everyone here was banging the table for them to stop making macro bets in equities - and is glad they have seemingly done so... but somehow everyone is ok with them doing it in the bonds, wants more of it, and makes excuses for their past mistakes in doing it while calling it "maintaining optionality" Isn't weird nobody views the equity hedges as 'maintaining optionality' but going to 0 duration on 100% of your fixed income exposure is? Why isn't a duration of 3-4 years to match your liabilities 'maintaining optionality' without betting the whole portfolio on higher OR lower rates? I don't understand the lack of accountability or the difference in views or why it's so controversial to point it out.

-

Is it plausible? Perhaps. But you're own admission is that rates peaked and started to fall a full ~15 months before the COVID was anyone's concern. In 2019, forward indicators were negative, the yield curve was inverted, overnight funding markets were breaking, and the manufacturing sector had been contracting for months. Isn't it more plausible that contraction/slowdown was already, coming regardless of COVID, and that they was no economic growth miracle under Trump even if COVID has never happened? I think it's more likely that the only reason rates ever got to 4+% for them to have been majorly "right" was COVID. And even with that, here we are in Trump's second term, another round of tax cuts, M2 still massively expanded from COVID stimulus, and we have a 3-handle on the 10-year bonds again ... Rates peaked over a year ago, forward indicators have been negative for a long while, the yield curve is rapidly reinverting after spending a long time inverted, and rates are coming back down. It feels A LOT like 2019 all over again and it's feeling like Fairfax might be missing the opportunity to lock in rates all over again (though 2.5 years is WAY better than like 6-months or whatever duration was back in 2019). It's not like I'm shouting for them to go 2x levered on TLT. I'm simply pointing on t they missed major rates calls in the past, we're lucky with COVID to bail them out, and I kind of want them to stop making major rates called going forward with a neutral duration position of ~4 years.

-

So equity hedges and deflation swaps aren't macro calls that failed? But rather "keeping their options open for a wide range of unknowable possibilities"? Or is that only the case when it's fixed income and they lucked into being right?

-

The expected value framing makes no sense. They didn't exit duration in 2015 when rates were lower. They didn't add duration in 2018/2019 when rates were higher than where they exited. They exited their duration immediately following Trump's election. They said themselves that they expected economic growth to take off and rates to run much higher. They were wrong. They got rates modestly higher, never locked those in, a global pandemic and recession where long-end rates went to 0, missed out on additional income and massive capital gains potential for a handful of years, and were bailed out of all of it by a combination of an unforeseen hard market for insurance which ballooned the float that could then be invested at higher rates as rates rose their fastest pace in 50-years ....from supply chain disruptions/inflation expectations and not Trump's economic growth from policies passed 5-years priors. I'm not upset about it. The terrible call and investor fatigue after a string of terrible calls is what allowed me to renter the position in size at $250-450 2-years after selling my stake for $500-600. But I'm not rewriting the history because they got lucky - they were wrong from 2016 - 2020. They were right from 2021 - 2024. 2025 onward remains to be seen, but it's a coin toss and I don't like those odds. Would prefer to see neutral duration positioning with their alpha earned on credit opportunities. They seem to have a better track record with that.

-

You're falling victim to resulting. Nothing that they said they were preparing for in 2016 change of positioning happened. An entirely unrelated, and unforeseen, set of circumstances came to be 5-years after they made the bet to bail them out of it.