TwoCitiesCapital

-

Posts

4,995 -

Joined

-

Last visited

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by TwoCitiesCapital

-

I started DCA'ing in 2019. I'm up near 20x on certain lots acquired in 2020. 7-10x on most lots purchased in 2019/2020. And even up 1.5-2x on the most of the lots purchased in 2021. Have I outperformed NVDA? Hard to say - I haven't calculated my exact performance, but not outperforming a single stock for me isn't a sign of failure. Its a recognition that I would have been unlikely to pick NVDA in 2019 as a conviction pick and commit to holding it for years like I did for BTC. What I did instead was allocated to BTC with the thought it would likely outperform the average stock. It has done so in spades. As well as outperforming all of my individual stock picks - even fantastic ones like Eurobank, Fairfax, and Rolls Royce - all of which were acquired at great prices from the 2020 drawdown. You didn't need to buy BTC back in 2012 to do well. You just need to DCA with a 3-5 year time horizon. Will BTC achieve the same level of returns it had in 2013 and 2016? I doubt it. But that doesn't mean it still won't be the best place for incremental capital for most of us.

-

Butthurt much? I mean, I agree to an extent. Me buying Bitcoin and holding it is nowhere near the achievement of Carnegie, JP Morgan, Rockerfeller, etc. But just like one could simply get rich but buying Amazon stock and "white knuckling it" from 2002 onward, I don't see why BTC is any different. We saw the opportunity. We capitalized on it. We yelled its sermons of hard money and fiscal responsibility from the mountaintops. And we waited years to be proven right while few listened. I don't see any issues with being rewarded for that foresight, patience, ridicule, and risk undertaken.

-

I'm not finished - but the book has definitely improved my impression of Musk. I was unaware of how involved he actually was with the start of Tesla prior to taking control. Same with OpenAI. His contributions are even more impressive and his work-ethic is maniacal. That being said, it also doesn't paint him the best light when it comes to home life and how he treats others when he's in one of his moods and what he expects from others who work for him who aren't necessarily devoting their entire lives to launching an electric vehicle. It's also obvious to me now why Tesla had all of the quality control issues it has when he was "deleting" even minor details like going from 6 bolts down to 3 to secure things. There's absolutely good to his approach of "delete, delete, delete" and hope for the best. And while that is excellent for cost control and efficiency, the cavalier attitude in which it is approached echoes his attitude towards things auto-pilot deaths which are problematic when we can point to competitors like Google who have none. Overall - it's a good read. And leaves you with a mixed impression of Musk.

-

I believe the commitment was every new, non-insurance indian investment would be done via FIH to prevent a conflict of interest in determining which shareholders get access to which deals. If FIH and FFH are both contributing proportionately due to a deal being too big for FIH, I wouldn't be upset because it doesn't upset the apple cart of favoring one group over another. If it's structured where FFH gets the bill and FIH a token amount, I think you'll see problems.

-

They can take it in cash and buy the shares at the same discount and end up with the roughly the same number of shares. The difference being float/tradable shares decreases (as opposed to increases) which may help close the NAV gap in the future AND is does NOT adversely impact FIH shareholders (including the existing balance of FIH shares Fairfax holds) via unnecessary dilution.

-

This is why, historically, equal weighting has tended to outperform over long-periods of time. Hasn't been true of the last 10-15 years, but is likely to revert and come true for the decade ending 2030 IMO.

-

IF the ETF approved, will you make Bitcoin a NEW position?

TwoCitiesCapital replied to james22's topic in General Discussion

3) more people finding value and using it... as has been the case for the last ~15 years There are pros and cons to self custody. If you had a lot of money in a wallet and didn't take steps to safeguard this potential, it's on you and is a con. Long term store of value Online digital payments with immediate settlement Censorship resistance Cheaper payment processing than credit cards (when using L2 networks like CC networks are) Ability to remit payments across borders w/ no unnecessary fees/taxes/intermediaries I'm sure there are more. They are NOT free as all prices rise to reflect the cost to the business and They are NOT quick for the receiver. Cash is by far the loser here as you pay the higher prices and get no reward for it. Everything the consumer sees is a papering over of the problems that the processors/businesses see on the back-end of the financial plumbing. Some things I don't like as a consumer? 1) I don't like waiting 5-days at Schwab for the money to settle when I'm trying to do a IRA contribution/backdoor conversion. 2) I don't like waiting 3-5 business days when moving cash between one financial institution and another. 3) I don't like waiting 2 days for trades in my brokerage account to settle before the money can be withdrawn or redeployed into other securities with faster settlement. 4) I don't like paying wire fees to ensure large payments need to get where they're going more quickly than the standard 3-5 days when I had to close on my mortgage. BTC transactions settle in 10 minutes for lower fees than a wire transfer and BTC/blockchain solve the above issues. And these are just the issues I see as a consumer. It doesn't consider the immense pain/resources/delays that actually occur within the financial plumbing that we expend untold resources/time navigating it. No, it doesn't. It takes 10 minutes for the payment to be finalized (as opposed to days/weeks with a credit card). Lightning Network does it in seconds. Bitcoin doesn't SOLVE every problem. But it's superior to cash/credit cards in the ways that matter (long term wealth preservation) with other solutions to make it more competitive in areas of less importance (buying a latte). -

It was 20% of my net worth at the beginning of the year. Definitely higher now and predominantly in BTC with a little ETH. Wish I had been as hands-off. I lost 10-15k learning DeFi and altcoins in early 2021 by buying near the top and riding it down and then lost another 0.4 BTC in the Celsius bankruptcy. Would be doing quite a bit better had I just stuck with Bitcoin and kept it in my wallet.

-

Im sure it depends on which currency you're looking at, but Bitcoin is hitting ATHs in several currencies including the USD. We just hit $69k+ a day or two ago surpassing the prior ATH by a few hundred $. In many non-USD currencies, the highs are more notable and 2021 levels surpassed much earlier. And while I understand the point that gold is up over the last 3-years while BTC is flat, would also note that 1- and 5- and 10- yr returns all favor BTC and that it's notable that we hit a new ATH before the supply shock of the halving which has never happened before - so I'm optimistic we're gonna turn the 3- time frame as well.

-

IF the ETF approved, will you make Bitcoin a NEW position?

TwoCitiesCapital replied to james22's topic in General Discussion

Perhaps Egypt will be the next country where a BTC parallel currency makes the most sense.

-

-Poll- How much Fairfax does the board own?

TwoCitiesCapital replied to Luke's topic in Fairfax Financial

It's a ~9.25% portfolio position for me which is basically right at my self-imposed limit of 10%. I also have ~3% in Fairfax India and some overlap with their individual investments like the ~2% allocation I have to Eurobank which is why I haven't added more to Fairfax despite technically having some room to do so. As part of my net worth, Fairfax/Fairfax India are just shy of 10% collectively. -

https://www.zeebiz.com/markets/ipo/news-sebi-clears-fairfax-backed-digits-ipo-after-delay-letter-shows-278705

-

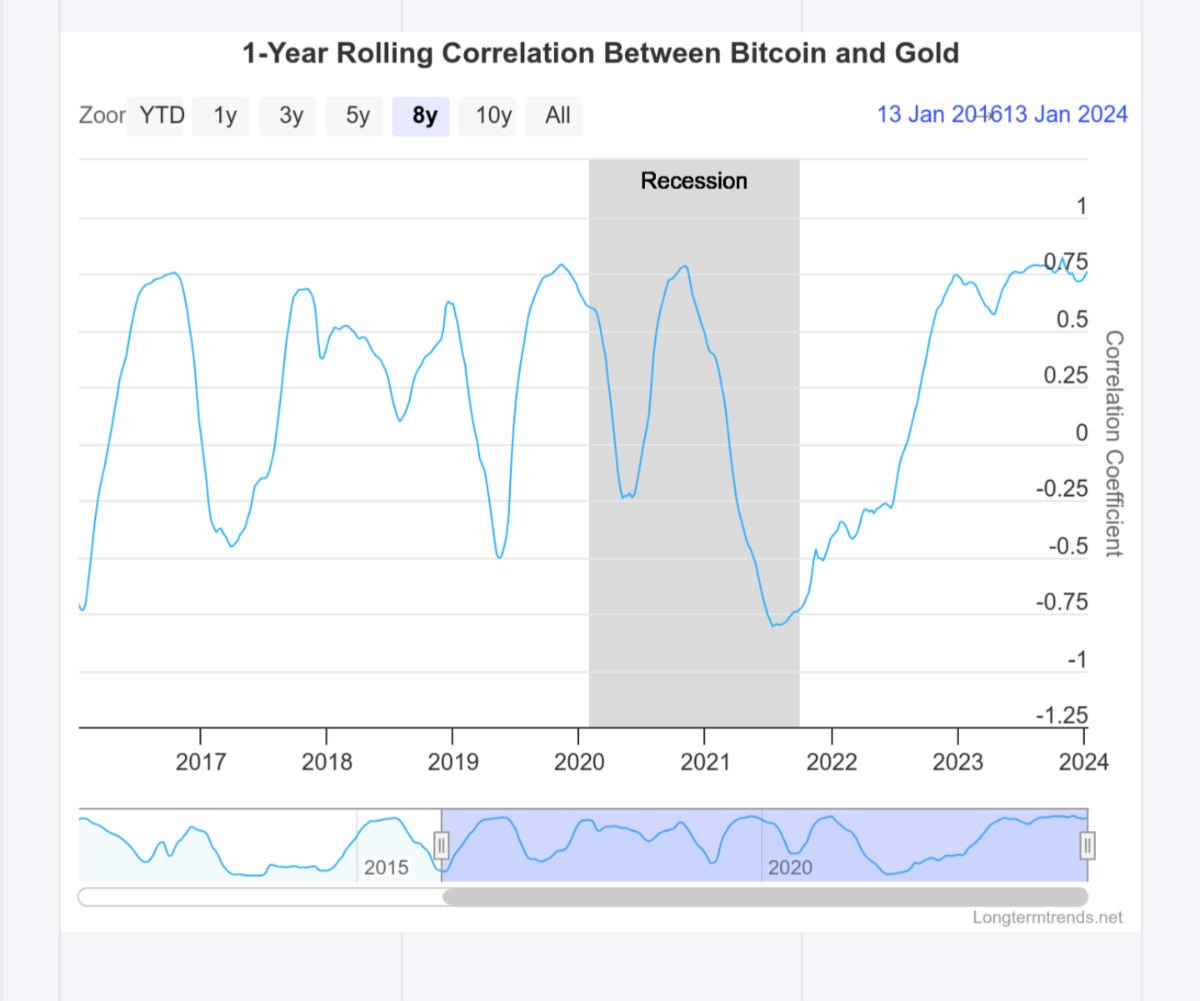

It's correlation to gold is pretty high at the moment.

-

Generally speaking it should behave bo different than the underlying bonds. In this case, my suspicion is that as 1-2 year bonds rolled down to 0-1 year type bonds, they were probably sold and 3-4 year bonds purchased - all the whole rates kept rising and 3-4 year bonds kept falling in price. This appears to have stabilized over the past year which is what we'd expect with few hikes and the amortization towards par. We'll likely see the opposite occur in a falling rate cycle. Bonds near par regularly sold to buy more 3-4 years which keep gaining on each subsequent rate cut. So your ups and downs are amplified by the ETF trying to stay true to its 1-3 year target you basically press-the-bet on 1-3 year bonds instead of allowing them all to to zero. Perhaps a better proxy for the underlying bonds would be to own a money market AND the 1-3 year fund so you have the spectrum of 0-3 years covered.

-

What we saw for client accounts in 2020 was that we continued to get daily/intra-day liquidity for bond ETFs and Mutual Funds in 2020, but it could take days to get liquidity for individual bonds when it came to individual Muni and/or corporate issues unless if we wanted to take massive haircuts. Funds/ETFs will only have liquidity issues if the underlying bonds have them first. Outside of treasuries which remained very liquid, it actually seems safer to own the fund/ETF vs the individual bonds given how that has worked historically.

-

Why can't you just wait a similar amount of time for the treasury ETF to amortize back to "par" i.e. rise in value? Owning a vehicle that owns bonds isn't any different than owning them yourself in regards to how it behaves for rising/falling rates. The primary differences come from fees and management decisions around what to buy/sell with inflows/outflows and the overall portfolio characteristics (average maturity/duration, coupon, etc). If you don't trust a professional manager to make those decisions on your behalf, then you shouldn't own a fund in the first place. Basically, it has nothing to do with how the vehicle behaves in response to interest rates.

-

If it's cash as to not bear risk because it may be needed, money market and high yield savings account. If it's cash that's waiting for a better opportunity to deploy, my preferred vehicle is JSCP at the moment.

-

Doesn't seem like the NY regulator views this as some massive fraud on behalf of Gemini either if they were willing to settle a multibillion "fraud" for just $37 million. I mean, Wells Fargo has probably paid that amount in settlements every month for the last several years

-

Yea - I know he was still holding $10+ million when he went quiet and has suggested he wasn't selling But I also believe he has disclosed that he'd taken $5-10 million off the top at different times as he rolled some of the contracts so he probably did well even if he never sold another contract and rode them down to being worthless

-

I was beginning to wonder if yesterday was the start of the FOMO. Strange it may be happening before the supply shock, but perhaps 4th time is a charm for markets to actually be forward looking.

-

I don't think this word means what you think it means. Im not going to pretend to be an expert on everything that is happening (BlockFi, Celsius, FTX, Genesis, etc). It's a lot. There's a ton of cases, filings, bankruptcies etc. But I am following it more than a casual armchair observer because I had money at stake in multiple of the platforms and am involved in the Celsius bankruptcy. I'm open to being wrong, but ultimately from what I've seen it wasn't Gemini that did anything other than perhaps vetting Genesis to be the one who provided the services. BlockFi and Celsius both used used some Genesis' product on the back-end as well. It's my under Genesis originated 70+% of the crypto loan volume before it's collapsed. Everyone used it. It's Genesis seems to be largely at fault. Celsius has some questionable activities like the CEOs friends and family yanking tens of millions of deposits while he was separately tweeting about how safe/sound everything was. Additionally, they lied about concentration and collateralization of the loans. BlockFi and Gemini? From what I've seen, they largely just got caught up as collateral damage and ice yet to see anything show untoward behavior. And Gemini survived that where few others did. Perhaps. But it's the same agency that thinks a token that provides no ownership interest, no interest, no anything constitutes a security as well. Some things in crypto are fundamentally the same - like banks and a need for regulation and transparency. Other things, like tokenization and DAOs aren't entirely different and need rules to be throught through.

-

So because they advertised a product on their platform, they're guilty of fraud? Interest WAS being paid. Returns were being made. But it was riskier than advertised and the risks blew it up. Can you prove that Gemini knew it was riskier? Genesis certainly knew. They were the ones making the loans. They absolutely lied, concentrated the loans, and encouraging risky behavior from the borrowers. But prove to me Gemini committed fraud by offering the product. What internal documents? I'm not following the trial in detail, but what I've seen so far is Gemini pulled billions in client funds from the program which is, in part, what toppled the house of cards. Not that they continued to add to it. And as far as the SEC? They also said that Bitcoin spot ETFs couldn't proceed while approving futures ETFs and had to be taken to court, wasted years, and millions of investor dollars through inflated fees and negative roll yield because of it. The SEC has an axe to grind against crypto for whatever reason and their lawsuits against ripple and Grayscale prove it. Not sure that it was fraud just because the SEC called this a "security".

-

-Poll- How much Fairfax does the board own?

TwoCitiesCapital replied to Luke's topic in Fairfax Financial

Just wanted to point out that there is no option for 50-100k. You have 10-50k and then 100k. Someone who owns, say $60k of shares, has nowhere to vote. -

What fraud did Gemini commit? If you were accusing Genesis if something, I might could agree with you. All I think Gemini is guilty of is perhaps poor due diligence in selecting a partner for the product. Maybe it's their BTC stake that has YOU so wound up?

-

What I'm hearing is you're making excuses for Adam Neuman, Trump, and Bank CEOS being rich after failure, but the Winklevoss can't be afforded the same excuses when a firm they partnered with failed? Did I get that right? Point is, this is what bankruptcy does. It takes the onus off the executives and decision makers and onto those capitalizing the firms debt/equity. It's ALWAYS the capital providers who lose in bankruptcy. Employees still get paid. Lawyers get paid. Trade claims get paid. Equity and debt? Well that's for the courts to work out. This is how EVERY bankruptcy works. Not just the Winklevoss' - which is itself a misnomer because their firm is still operating and avoided bankruptcy. Outside of Gemini, the Winklevoss brothers are probably some of the largest holders of Bitcoin as it's estimated they still hold over 70,000 BTC that were purchased largely from their Facebook settlement proceeds. There was never any questions they'd still be filthy rich even if Gemini went bust.