TwoCitiesCapital

-

Posts

4,667 -

Joined

-

Last visited

-

Days Won

6

Content Type

Profiles

Forums

Events

Posts posted by TwoCitiesCapital

-

-

4 hours ago, rkbabang said:

And the drop in USD by far greater than 75%, more like 98%, is a permanent one that it will never recover from. In fact it is still dropping further year by year and no one expects it to ever stop dropping.I think the point people miss is the "long term" of "long term store of value".

USD is a decent "store" of value for a ~12 month period. But long term? It's been miserable despite being one of the best fiat currencies in existence. Same with bonds that pay USD.

But Bitcoin? Has served it's purpose for anyone that has a 3+ time horizon which still isn't "long term" IMO - but rather intermediate. Long term holders? Well, it's worked out better than any store of value should, but that's because they're early adopters in what will be the largest payment network in the world.

-

9 minutes ago, rkbabang said:

I read somewhere that there are now more females graduating from college than males. I wonder if this will be more common in the future. If the wife makes more being a medical specialist or something then the husband will stay home with the kids.

Or... it'll be entry and mid-level college educated jobs displaced by AI, inordinately impacting Gen Z women, while physical labor/construction/building is unbothered and remains dominated by men.

Hard to tell how that one plays out.

-

1 hour ago, rkbabang said:

There is likely a lot of that, especially in marriages where there is only 1 income. But most families have 2 incomes. Two people with 2 incomes pooling their resources is likely much better than 1 person with 1 income trying to go it alone.

It's going to be true of 2 income families as well. The majority of women value this in a man and WANT a man that earns more than them (not all - but more than half for sure). Men on the other hand? Don't seem to care near as much about the stability/earnings capacity of their wife.

The men who get married are far more likely to have above median incomes than below median. The same may NOT be true for women where I actually think it's possible women with above median incomes are LESS likely to be married.

Therefore two income families will typically be a man, and a women, both earning money. The men will have fat tails on the right side of the probability distribution. Hers will be more of a random distribution, but likely slightly skewed to the low end of the income distribution.

-

Snow balls get bigger as they roll downhill...

-

3 hours ago, ValueArb said:

A long term store of value in something that has no intrinsic value, no cash flow, no dividends and every few years drops 75% in price?

And "instant-payments"? Why do I need that when I have Zelle, Venmo, Cash App, etc? Last I checked, Lightning network was doing roughly a billion in annual volume in USD, while Zelle alone did nearly a trillion in USD in the last 12 months. If the Lightning network was so useful, why isn't it being used?

And is there any evidence that BTC is used for even 1% of world wide cross border remittances? Again, if its so useful why isn't it being used?

I use Venmo to send money to my account - takes 3 business days to get there.

I just got an insurance check for 65k for fire damage on my condo. Cashed the check? Bank has a hold on the funds for 10 days to make sure it doesn't bounce.

Bitcoin? I can have confidence is sent/received in less than 10 minutes for lower fees than a wire transfer.

That's the benefit.

How people don't see these problems in the current financial plumbing or fail to see Bitcoin can be superior to them is beyond me.

And that store of value you complain has fallen by 75% before? The USD has also fallen by 75%. As has gold on prior occasions. Bitcoin, despite its drops, has outperformed every single asset class (and damn near every individual investment) over the past 3, 5, and 10 year horizons - so yes - I consider that a solid long term store of value.

-

3 hours ago, rkbabang said:

It is a lot harder to actually help the needy than most people think.

And a lot fewer 'needy' than most suppose.

A I've grown older, I've grown more suspicious of charity for these reasons.

Being 'poor' today still looks great compared to being poor in the early 1900s in the US.

-

Maybe I'm doing the conversion wrong from INR to USD, but would seem at today's market IPO price that Fairfax was NOT, in fact, inflating the value of Digit by $1.1B on their stake....

-

5 hours ago, xboojum said:

Welp! (To be fair, that was three whole months ago.)

Was coming here to say just this

-

1 hour ago, ValueArb said:

...yet hasn't found any significant economic application despite being in a world awash with the internet and modern technology.

Cross-border remittances? Long-term store of value? Instant-payments via the lightning network?

What other significant economic applications are you looking for that would it give it credibility and legitimacy that the above don't?

-

23 minutes ago, sholland said:

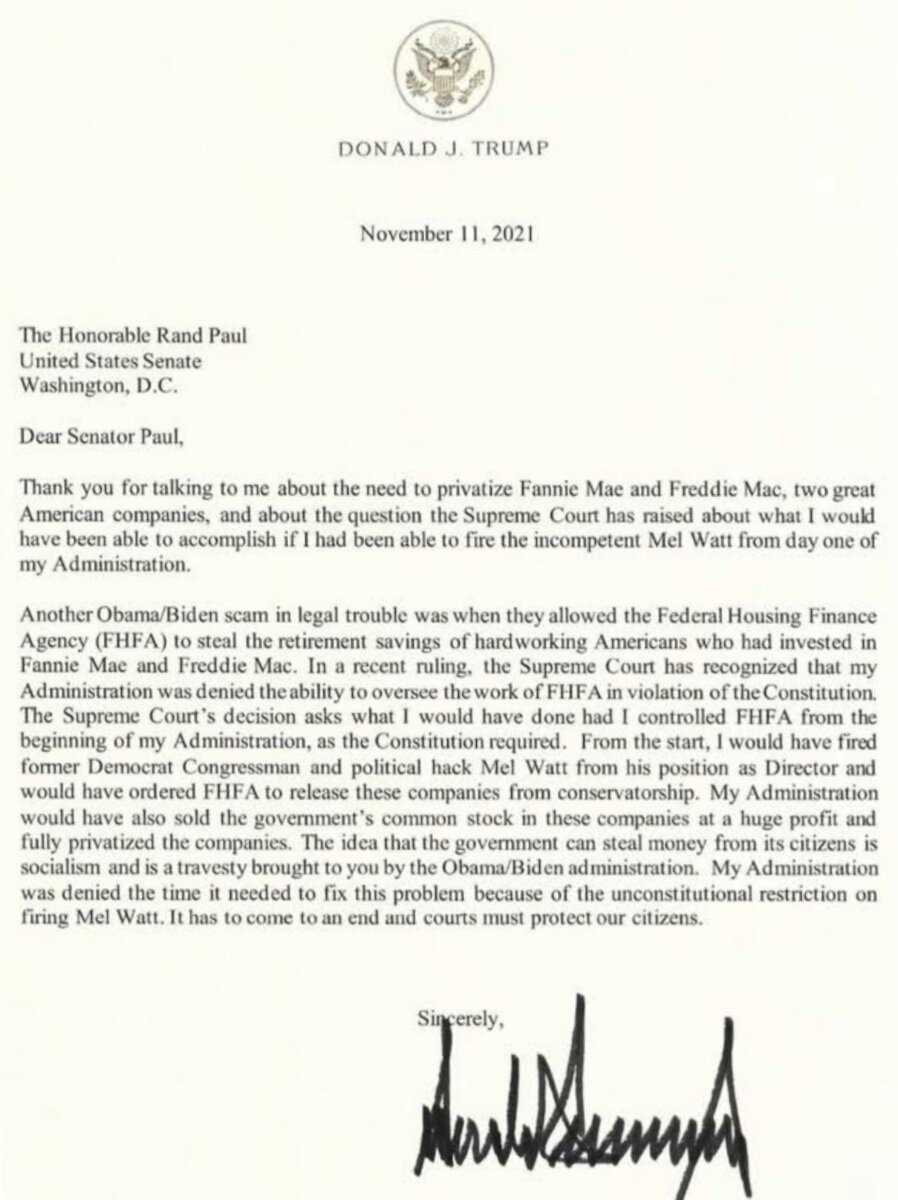

It’s a Trump trade. Share prices going up lately because Trump’s poll numbers have gone up. Trump floated the idea of John Paulson being the treasury secretary. Paulson was a backer of the Moelis Plan to recap and release.

If Trump really wanted to help them, couldn't he have forfeited the Treasuries' defense in court and admitted that the institutions were stolen from shareholders, and pillaged, at the direction of the Treasury and the prior administration?

He didn't.

-

1 hour ago, thepupil said:

I agree with this, but would point out that the value of that bond is much higher than $250K. Because I'm a complete nerd about this, I have a spreadsheet that automatically imports the yield curve and discounts each future mortgage P&I payment at the relevant zero coupon rate.

My mortgage has 316 months left on it, has a 2.875% rate, and is worth about

83% of par using the treasury curve

75% at tsy curve + 100

68% at +200

63% at +300

50% at +600

38% at +1000.

The weighted average life of the principal payments on my mortgage is 177 months, so while it was a 30 year mortgage in its now a 26.33 mortgage and the principal payments are on average just 15 years away so rates have not made 30 year mortgages worth 50 cents on the dollar. More like 80%.

So the way i see it is that a risk averse person with my mortgage should just buy bonds (I buy about $5K / month in my 401k) as a way to slowly defease the low cost mortgage. An enterprising investor should buy riskier assets do do so.

There's a tax angle as well. Assuming full taxability of the treasury interest, at the maximum federal rate, the return on treasuries is actually treasuries MINUS 1.5%. At that discount rate, my mortgage is worth a full 97% on the dollar (assuming no mortgage interest deduction). It's here where the argument for simplicity and just paying off the mortgage is strongest. If the choice is between treasuries in a taxable account and paying off mortgage where taking the standard deduction and there's zero tolerance for market risk,and no value placed on liquidity flexibility, then just pay off the mortgage.

I value flexibility, liquidity, think i'll make more than treasuries (but am buying those in a tax advantaged account) and don't envision paying off the mortgage until i move or 2050

+1

Sounds like your specific example is very similar to mine. Agree that mortgages have not fallen 50%. The monthly principal payments make them less duration sensitive than a similar maturity bond - they just happened to be MORE duration sensitive than the 10-year everyone benchmarked them to as prepayments go down and mortgage spreads widened.

I am reducing other debts, even where it doesn't maximize the full financial value I could receive from the leverage, but the mortgage is a harder equation for me for me to decide on.

-

19 minutes ago, Sunrider said:

Indeed - what a slow burn. Just wondered whether there's anything new in terms of admin action or courts which I missed? I seem to recall that there was a plan to release once they build enough capital - was that ever formalised? How far away would the companies be from that?

C.

They're still not able to really build capital. Every $ of retained earnings is offset by a liability of $ owed to the Treasury via liquidation preference. They get the benefit of having access to that liquidity, but any return it generates is still owned by the Treasury and not shareholders.

The only real benefit of "reforms" made by the Trump admin is it put an extra layer of trouble for the Treasury in accessing those funds that they technically own - basically made a current asset a deferred asset.

Shareholders do not benefit from this arrangement though - it seems more designed to punish the next administration then improve anything for the stockholders. People have argued it was set up to incentivize additional negotiations between the two parties to come to an agreement in the middle, but here we are 4-years later with 0 progress made there. It was a hard argument to make as a positive twist then and significantly harder argument to make today with the benefits of hindsight.

-

15 minutes ago, Gregmal said:

In this scenario, couldn’t you arb it? Like rent your primary with the super low mortgage, net money on the rent, and then instead of buying fixed income pay cash or heavy cash allocation towards a second place?

I've rented the guest room on and off over the last 6-years. But my location doesn't really have the demand for me to be able to cover the note/HOA in consistent rent unless if I'm looking for high turnover tenants like travel nurses - which is work and risk unto itself.

Love the condo - but do long for the flexibility.

-

1 hour ago, LC said:

Assume you have the cash to pay off the note, why not instead buy a 30 year treasury, use the coupons to pay the mortgage? Plus you still have some spread for taxes or profit?

It doesn't work like that. Because your monthly mortgage payment amortized differently and requires principal AND interest.

It actually requires quite a bit more than the principal in treasuries to cover the monthly payment. Something to the tune of ~60% greater than the balance of my mortgage in treasuries where the 6-month coupon would cover 6 months of payments - Treasury balance can decrease with time/principal reduction.

And then the HOA fees? Total would be more than double the mortgage balance to be covered in FCF from treasuries.

-

5 hours ago, Castanza said:

The standard financial response

I don't disagree with the math. You can't put a price on the other things. No longer servicing a mortgage means my wife can raise our kids more (as she wishes) and work less. Less daycare costs etc. I work from home, get to take my son for walks or go tot he park on my break. etc. Something you can't get back in retirement. I be a lot of retirees would give that 400k liquid asset in a heart beat if hey could go back and have more time with their kids/family.

I don't disagree with the math. You can't put a price on the other things. No longer servicing a mortgage means my wife can raise our kids more (as she wishes) and work less. Less daycare costs etc. I work from home, get to take my son for walks or go tot he park on my break. etc. Something you can't get back in retirement. I be a lot of retirees would give that 400k liquid asset in a heart beat if hey could go back and have more time with their kids/family.

I by no means want a life that resembles a business where I'm always thinking about money or how to make an extra percentage point here or there. But I'm a simple man who lives a simple life. Yeah I enjoy investing and get the importance of sound financials. But the less I think about it the better!

I have zero desire to own a vacation home, go on 20k vacations, or own fancy sports cars. Not my cup of tea! Nothing wrong with that that choice if you do. And if you do, your approach makes sense. Different strokes for different folks!

+1

I'm torn on this. Because I have a mortgage @ 2.75% and know financially it's the very last thing I want to put marginal $ towards.

But I also hate my job and would love to quit and just take some time, and the mortgage is basically the only impediment to quitting and/or taking a lower paying, but more satisfying, job.

Freedom and flexibility is hard to put a price on. But it's worth something.

1 hour ago, blakehampton said:The thing that I don't understand is how an "urge" gets passed on. I can wrap my head around health and looks, but feelings toward certain actions seems odd to me. I'm not disagreeing, I'm just curious.

Same as anything is born with instinct - just like babies instinctively root and mouth for a nipple when they're hungry.

-

2 hours ago, gfp said:

Just to get this straight, if you are a MSTR and BTC maximalist / bull / whatever, you want the SEC to not approve the ETH ETF because everything except Bitcoin is a security and that means BTC is unique as digital property and "there is no second best." - right?

I tend to agree with rkbabang

Bitcoin is unique regardless of what the US govt approves or doesn't approve. Ether was bleeding vs BTC since long before the BTC ETF was approved...

Whether on Ether ETF gets approved or not matters little to the long term thesis of BTC - it only impacts short/intermediate flows and only marginally so (IMO).

In other news:

-

I'm going to go ahead and disagree with all the social media hate.

Let's not forget most boomers don't have enough to retire either and they lived in age before social media when pensions were a thing. Our government, made up of boomers, spends like drunken sailors regardless of which party is in charge.

It's just humans, in general, struggle with delayed gratification and savings. It's not a particular demographic or social media's fault. It's that people, in general, suck at this.

-

3 hours ago, Mephistopheles said:

Why would Trump help this time around when he didn’t last time? When his Treasury secretary explicitly stated it was his goal and did nothing. What will be different this time?

This is my concern.

It's easy to say "I couldn't do anything because I couldn't fire someone" but they also didn't really do much in favor of shareholders when they COULD do something after the firing.

I don't think Trump cares about anything other than what's good for him and what makes his opponents look bad. If he's previously disclosed an ownership stake, I'd agree. Until then, it's whatever is good for him @ the time is what we can expect he'll do so I expect the issue to continue being ignored.

The courts have failed us, thus far, and are our primary remedy

-

On 5/18/2024 at 6:23 AM, Gamecock-YT said:

Those of us that follow Altius have heard the CEO pounding the table for the past few years that this was eventually going to happen. I've positioned accordingly.

+1

Have been rebuilding my stake in Altius that was sold in 2021.

Have been rolling short puts on FCX monthly for a bit.

The call in copper was obvious with the political will to electrify everything.

-

On 5/3/2024 at 12:39 PM, beerbaron said:

Unethical. Nothing to discuss here. Not putting the time you charge is similar to stealing. Just because its harder to get caught does not make it more ethical.

I dont think anybody on this forum would be thrilled if a contractor came to your home for a days work on hourly contract, left half way through at lunch and billled the full day.

Beerbaron

Was anyone calling it unethical when employees were expected to be in the office for "face time" even when they completed their work?

As far as the contractor example goes - as long as they finish the job that I asked them to do, within the budget and timeline we agreed, I honestly don't care if they're leaving each day at lunch.

-

15 minutes ago, AG said:

No need for the autofx which is actually more expensive. You make the trade first and then close the negative currency balance. If there is a small residual Interactive Brokers automatically converts that to your base currency the day after I think

Mayhaps that is how they treat taxable accounts, but this is NOT allowed in my IRAs there. It always refused to take the trade unless if there is sufficient settled currency in the account to cover it.

regardless - the new functionality should fix whatever the issue is I covered for both taxable and qualified accounts if you so choose to use it.

-

I saw somewhere recently that Grayscale had received its first inflows since conversion to an ETF.

Which begs the question - who is buying the ETF with significantly higher fees than ALL other available options?

I understand capital gains trapping some current investors - I don't understand new inflows. Anyone have the angle here?

-

11 hours ago, schin said:

@bizaro86 @TwoCitiesCapital @johnpane - Thanks for the reply.

I have one German bank position (Commerzbank) that I believe will be a takeover target in the future. Do you know how stock mergers work out in ADRs? Do I get converted to cash nonetheless or will I get new ADRs if there is a stock transaction.

For example, if it get bought out by Deutsche Bank, which is NYSE traded, versus Unicredit (Italian and ADR, itself). How do mergers work out either way? I'm worried about the tax treatment.... if they pay me out, there's going to a huge cap gain... versus rollover into a stock position... of course, that's a rose-colored glasses problem.

Probably depends on the merger. If paid in cash, you'll receive cash. If acquired by a US listed company, my guess is you'll receive US listed stock. If acquired by a foreign listed company, my guess the ADR sponsor receives the shares, sells them, and distributes the cash to you.

But I cant say for sure it will likely vary pending the scenario.

-

On 5/4/2024 at 1:17 AM, schin said:

I have InteractiveBrokers, so both transactions should be easy (ADR or purchase in foreign market). That said, is there any reason to buy ADRs instead of going directly to the foreign market?

Many noted they bought Nintendo directly in Japan instead of the ADRs. I know ADRs have extra, hidden (custodian) fees...

Is there any reason to buy the ADRs?

The primary reason would be just the simplicity and access. Most domestic brokers don't trade in foreign markets OR they charge exorbitant fees to do so.

The only downside of buying local markets on IB was that you had to convert enough currency to make the trade and it was hard to get the right amount without uneconomic residuals sitting in the foreign currency. That being said, I believe they just announced auto-conversion of currency balances which SHOULD mean that this is taken care of and you can buy foreign stocks with USD balances and IB auto-converts the appropriate amount for settlement/commission on your behalf. I only own local holdings @ IB. I use ADRs in my accounts at Schwab.

The other piece is liquidity - there may be a handful of notable instances where foreign companies listed on major exchanges via ADR might actually have more liquidity in the US than their home country, but I don't know how often this might actually matter for us smaller individual investors.

Fairfax India new issue

in Fairfax Financial

Posted · Edited by TwoCitiesCapital

I, for one, am ok with the persistent discount.

The historic execution is there on the BV side. The present execution is there on the buybacks and future opportunities side. I have no doubt that the longer term execution will be there as a result.

The discount won't persist forever if BV performance continues, but am glad for the opportunity to increase my ownership via occasional incremental buys and let FIH increase my ownership for me with time as long as it does persist.