TwoCitiesCapital

-

Posts

4,637 -

Joined

-

Last visited

-

Days Won

6

Content Type

Profiles

Forums

Events

Posts posted by TwoCitiesCapital

-

-

1 hour ago, james22 said:

Once investment advisors are cleared to recommend making bitcoin an allocation, there won't be a race to secure their clients that allocation?

I think plenty of them will be cautious to buy if it has just gone up 50-100%. Also, plenty of firms/advisors are still not 'for' it despite the approval of BTC. It's a pipe dream to expect the company I work for to allocate to it any time soon.

And as far as those with advisors, people don't tend to be as greedy when allocating others' money then when trying to resist the pull of greed on their own so will be more cautious as the price rises I suspect.

-

18 minutes ago, james22 said:

Thought there'd be more reaction to this?

RIAs manage $8T.

75% of them plan to allocate an average of 2.5% to the bitcoin ETFs.

That's $150B demand.

And doesn't include the wirehouses, regional broker-dealers, or institutions (Blackrock alone manages $9T).

I think its going to take years. How do you get $200+ billion into a market cap that is only $1 trillion? You either drive the price to the move massively by hitting every bid and then risk having no liquidity if you need to sell OR you slowly accumulate while waiting for that $1 trillion market cap to grow to $5-10 trillion.

I think most of these allocations occur AFTER the next exponential step-wise move in BTC. Unfortunate for those guys - great for me to continue to accumulate.

-

2 hours ago, Gmthebeau said:

Stocks. I still think there is say a 25% chance the FED will be forced to raise rates even higher.

I'm open to the Fed hiking again. I think it would be a mistake. I don't think the data will support it especially now that we're seeing outright deflation in many goods/real assets. But I can believe that their motivations may be something other than "stable employment and inflation".

Powell has basically said, in other words, that their intention is to drive the economy into a recession. Whether he does that by raising rates, or leaving them too high for too long, I can't say. But I've been pretty confident for awhile that 4% was too high and have been buying duration every time its available above 4%.

37 minutes ago, Gmthebeau said:I like floating rate a lot better in the bond area. You can get 8% and FED stuck having to stay higher for longer despite Powell wanting to cut. The folks on the committee with some common sense won't let him.

I'm in a lot of things in fixed income at the moment. Started off in cash and iBonds when rates were basically zero in late 2021. Then started accumulating short-term spread products and agency mortgage expopsure as rates rose and certain spreads blew out in 2022. Then started adding intermediate government duration and core bond type products. Then I started adding TLT calls when rates were on their way up to 5%. In recent months I was adding fixed income CEFs at sufficient discounts to NAV to make me want the low-quality credit. 10+% cash yields.

At this point, I don't really care what rates do. Lower rates benefits my duration exposures and can give me ~10+% while likely giving me attractive opportunities in stocks. Flat rates let me collect a yield that probably YTMs that are 6-7% in aggregate. Higher rates hurts my duration, but likely help my spread products - so maybe ~5+% while setting me up for even juicier returns next year.

I'm ok with any of those scenarios.

-

1 hour ago, mattee2264 said:

Markets aren't stupid. They are seeing evidence of a soft landing and expect that will deliver interest rate cuts and an eventual return to growth (it is better to have a landing so long as it is soft than keep having the landing postponed with the associated lingering uncertainty)

Markets are plenty stupid from time to time. Pricing the 2021 stock market at 30x+ earnings while knowing inflation was accelerating was idiotic. Seemed like everyone was saying equities were an inflation hedge. Meanwhile, myself and a few others were suggesting real returns on equities were going to be poor, that margins were likely to contract (and profits fall), and that picking your spots in bonds and gold would likely outperform.

And what did we see? Contracting margins and falling profits. S&P 500 profits are STILL below what they were in 2021 in real terms. Even after the double-digit rally in Q4 last year, nominal returns are mediocre and real returns are roughly -2%/yr over that time.

The only real surprise here has been the markets willingness to bid stock prices up again, despite an environment that is clearly cautionary and even that couldn't deliver good results to the average stock.

1 hour ago, mattee2264 said:The first leg of the bear market was multiples reacting to higher inflation and rate cuts and at the time things looked pretty grim with double digit inflation and uncertainty as to how high interest rates would go and for how long. That leg seems to be over now (barring an unexpected second wave of inflation) and therefore markets are pricing in lower interest rates with a major benefit to P/E multiples. And note that if earnings are $1 then even PE multiples going from 15 to 20 is enough to increase stock prices by over 30%. So it is a pretty powerful impact even if outside of AI there still isn't much evidence of improving earnings.

On rates: The problem that markets get wrong about rates is that if you're lowering your discount rate, then you should be lowering the average growth rate you expect as well. The effects largely cancel one another out.

This was borne out in the 2010s when U.S., Europe, and Japan all had 0% rates. Broad revenue growth was abysmal. GDP was significantly below average. Real earnings to workers and etc suffered.

The primary saviors of the S&P 500 came in the form of refinancing high cost debt and levering up which expanded margins, using cheap debt to buyback shares, and the eventual concentration of the index in a few hyper growth names that were ablet o buck the trend. But 2 of those 3 trends are basically guaranteed to reverse and act as headwinds in a decade of non-zero rates.

1 hour ago, mattee2264 said:The second leg of the bear market was supposed to be earnings falling as a result of higher interest rates and falling consumption in response to cost of living crisis etc. Not a huge amount of evidence of this. Earnings have been pretty resilient and held up better than most would have expected. And while Big Tech earnings growth has been a lot weaker over the past few years and increasingly relied on cost-cutting/restructuring with the AI hype investors are looking forwards to a return to fast earnings growth.

Earnings have NOT been resilient and have NOT been better than originally expected. The only expectations beat were the expectations that were previously cut dramatically. The expectations were earnings would be inflation resistant. We are still below 2021 earnings in real terms by a fair bit.

Not a huge amount of evidence? It's only in services consumers are "splurging". Retail sales plummeted in 2022 in real terms in 2022. 2023 basically got us back to even in real terms. The best characterization of that is stagnation. And that stagnation was existing before we entered a consumer credit cycle.

Now? Credit card defaults are accelerating. Major economies ARE going into recession. Commercial real estate is beginning to weigh on regional banks and we know major banks have been cutting back on lending. I have to believe that sets us up for a worse 2024 than 2023 i.e worse than stagnation.

1 hour ago, mattee2264 said:The few bears left standing continue to argue that every landing looks soft until it turns into a hard landing and cite various factors that are delaying the recession (US fiscal deficit spending, pandemic era excess savings, benefits to corporations from locking in cheap long term debt during ZIRP, loosening of financial conditions due to much higher stock prices etc).

But even if there does end up being a mild cyclical recession the negative impact on earnings will be offset by lower inflation and interest rates and as we saw during COVID the market are comfortable buying the dip and looking through mild recessions.

I don't know what is delaying the recession. The timing of these things is always difficult - especially when confounded by trillions in an unprecedented bout of stimulus. But forward data continues to disappoint and now coincident data is starting to.

The only three things that appear to be holding up are the 1) S&P 500, 2) the unemployment rate, and 3) GDP.

1) The S&P can make mistakes and turn fast. It has repeatedly done so in the past

2) On unemployment? The numbers have been trending in the wrong direction. And while headline numbers are fine relative to historic figures, the moves under the surface are concerning. More part time jobs and fewer full time jobs. Higher wages, but fewer hours, leading to less take-home pay. More government jobs, fewer private sector jobs. Etc. etc. etc. The weakness is there and growing and we know this is a lagging indicator

3) On GDP? It's painting an entirely different picture from GDI which aims to measure the same thing. And it can be revised lower as it has been in prior periods leading into recessions. My expectations are historical GDP figures will be revised lower and GDI figures will be revised higher and GDP will not appears as robust in hindsight

And lastly, we have official recessions in Germany and Japan. France is teetering on the edge. Most of the rest of Europe is slowing. As is Canada. As is China. The majority of the global economy is pointing to a slowing.

-

21 minutes ago, gfp said:

Were there any surprises in the Q4 earnings? Seems like we knew all of that ahead of time: TRS profit, Micron profit, October bond moves, interest rates move for the quarter, lack of big Cats, etc

Fairfax has demonstrated time and time again that its share price is NOT part of an efficient market.

As mentioned in my post, there used to be stellar earnings reports that the stock wouldn't react to and then 2-days later the stock would pop 4-6% for seemingly no reason. I actually started a strategy of adding to my positions after great earnings and then selling into those pops that worked reasonably well for 12-18 months.

So while there is nothing that surprised us, given things like the headlines characterizing these earnings as a "miss" or as lower than last-years (without adjusting for the $1.2B gain from a subsidiary sale), or the share price tanking after the MW report, it's clear that the market doesn't follow this anywhere near as closely as we do as is regularly missing the story here. Which is why I'm surprised the earnings report didn't spell it out for those folks with $1.7B in Q4.

14 minutes ago, StubbleJumper said:There are probably some people who took the opportunity to add last week and are lightening up before the long weekend. I increased my position by 30% about five minutes after I read that amateurish report. I went from being unwisely concentrated in FFH to being bat-shit-crazy concentrated in FFH. I really should have been trimming the position in 2024, but have instead increased it significantly. At some point, reason will have to prevail and I'll put in a sell order for the shares that I bought last week.

High conviction is high conviction, but stupid is stupid.

SJ

That could be. That was exactly my plan into a 5-10% earnings pop ABOVE the pre-MW report prices.

Broke my own rule on position concentration to allow adds in the wake of the MW report. Gains since then have been satisfactory, but was definitely expecting more "oomph" from it. Now I have to decide how long I'm going to allow myself to break my rule for.

10 minutes ago, MMM20 said:I've felt this way every quarter for the past few years. And yet.

Give it a couple months. Or at least a couple days!

Yea - we'll see. Hoping it's the return of the 2-3 day lag in share response to earnings.

-

Going to be honest - the share price reaction to an a amazing earnings report is a bit disappointing

Makes me wonder if 1) the market had it "right" and the earnings rally was what we saw in January or 2) if we're back to the days of the getting the earnings look for free and the stock responds 2-3 days later

Either way - I am somewhat shocked we didn't get a pop of 5-10% from market participants who haven't been following this as closely as we have.

-

1 hour ago, mattee2264 said:

Still it is a little bizarre to see UK, Germany and Japan surprising markets with negative GDP growth and seeing their stock markets shoot higher. Either market is prophetic and looking through to a robust recovery in 2024. Or more likely the market figures bad news = quicker rate cuts and the rate cuts will produce the desired economic improvements.

This is concerning me as well. Was already on edge with the U.S. markets ignoring leading indicators, tax receipts, PMIs, composition of jobs, etc.

But now we actually have corroboration from other countries that this slowdown is global and still nothing. Lines go up.

Seems like this is going to be one of those things that appeared obvious in hindsight, but that markets were able to ignore in the moment. In the meantime, content to be heavy in bonds.

-

1 hour ago, Gmthebeau said:

and here we go again. Everyone who bought the 4% being blown up.

If long-term, rates go from 4% to 5.5%, which do you think will likely lose more? Stocks or bonds?

-

1 hour ago, valuesource said:

Newswire services have a way of really cutting to the bone...

Jeezus....

You just can't win, can you. No mention of last year's profits being goosed by $1.2B from the per insurance sale....

1 hour ago, StubbleJumper said:The most obvious point is that there's basically one bil of unrealised gains on fixed income, and it is unlikely that those bonds will be sold any time soon. We will see a nice pile of interest and divvies over the coming years, which is outstanding. But the $997m of unrealised gains on the bonds is low quality of earnings.

No lower quality than the $1.2B in losses taken last year for interest rate moves. Most of these gains won't be given back because it's not reflective of premiums to par as much as it the reversal of prior discounts to par from interest rates running higher in 2022 as well as the amortization of those discounts as portions of bonds come nearer to maturity.

-

53 minutes ago, Redskin212 said:

I have been a FFH shareholder for over 20 years, regularly attending annual meeting and listening to most quarterly conference call. It is hard to explain, but I can hardly wait for the annual results release tomorrow and conference call Friday morning. To me this silly MW report has just hyped it up more for me.

Thanks to all, especially Viking, for all the recent posts - the wealth of learning is amazing!

I'm giddy myself

Is gonna be high quality earnings (not accounting/paper gains) and a killer report

-

49 minutes ago, Viking said:

@dartmonkey I think management has commented on the TRS in the past. I think they have said they hold it as an investment. Not complicated.

How do you evaluate an investment? By calculating intrinsic value. My guess is Fairfax can do this… for itself.

I don’t understand all the hand-wringing / urgency to ‘do something’ with the TRS position. Especially given the likelihood of mid to high teens ROE the next couple of years.

The hand wringing is largely just due to the liquidity drag it can potentially create. Just like I was paranoid about their duration until they got around to locking it in. There has been a history of mistakes made that we don't want repeated.

Fairfax damn near run afoul of covenants and cash @ holdings company before. Having to come up with cash to front the movement on 7% of it's shares every quarter is not chump change. Particularly as the share price has moved from $500s to $1000s.

This isn't like their other equity investments because those wouldn't necessarily require additional cash infusions to continue holding through a downturn. And as the financing hurdle rises, and as the stock price rises, the potential cash cost of holding a position through a downturn is rising significantly

For now, I'm comfortable with it. But I would prefer them to let it go too early than to be forced to let it go too late.

"Buy fear, sell dear". Selling dear by definition means it hurts to sell and you don't want to do it.

-

3 hours ago, SafetyinNumbers said:

A combination of the USD wrecking ball that outperforms all currencies for technical reasons over the long term and oil prices being down, especially in real terms from $110 in 2011.This.

All currencies have sucked relative to the USD over the last 10-15 years.

I've been surprised by the staggering amount in some countries that aren't really "hyper inflationary" and the currency drag is the predominant reason my EM value plays at 3-5x earnings didn't trounce the S&P.

The below aren't peak to trough - they're just rough approximations of the exchange rates that existed in 2011 compared to where they're at today.

Mexican Peso is down like ~40%.

Brazilian Real is down ~70%.

Korean Won is down ~20%.

Euro is down ~25%.

Australian dollar is down ~40%.

Yen is down ~50%.

-

50 minutes ago, Santayana said:

Wow, it really would be something if the report was on the behalf of Brett Horn. Claim Fairfax book is 20% overstated, hope for a drawdown of at least that much, and then Brett can point to his price target and say "See, I knew it was overvalued".

Jokes on us. Brett Horn hired MW just to have a second voice agree with him

-

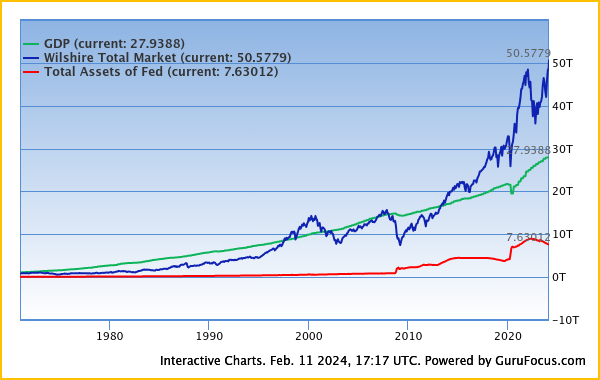

2 hours ago, blakehampton said:

The Buffett indicator looks pretty scary relative to the past. The ratio of total market cap / GDP is currently 181%, what do you guys think about it?

Buffett has said in the past that this is “probably the best single measure of where valuations stand at any given moment.” In an interview, I heard Alice Schroeder say that he would like to buy when total market capitalization is at 70-80% of GDP.

This indicator is less relevant with multi-national companies that exist today. At one time, it made sense that the capitalization of companies in the US would be tied to the incomes/economy of the U.S. and could not meaningfully grow beyond that. This was the case for much of Buffett's early career.

But now? Companies do a ton of business overseas and are no longer linked to just American incomes (what GDP is measuring) allowing for higher multiples to U.S. incomes to persist. I doubt we see 70-80% again outside of some economic depression.

-

46 minutes ago, blakehampton said:

So I have seen "the stock market is not the economy" a couple of times and I have to say I don't understand. Wouldn't the stock market essentially be a delayed representation of the economy?

Yes and no. As mentioned by others, the index essentially represents the best of the best (not always, but a close approximation) and thus isn't representative of the "average". Also, a chunk of revenues/profits are derived overseas which may be less sensitive to the ebbs/flows of U.S. specific economy..

Historically, they are related but not perfectly correlated. If only because weakness in the overall economy tend to lead to weaker consumers which will hit even the best of companies, a slowdown in the US can cause slowdowns elsewhere globally given how much we import, and because as people are laid off there are fewer $ flowing to excess savings/investments to bid up shares.

But they rarely coincide perfectly - stocks often lead, and sometimes lag, the developments in the economy.

-

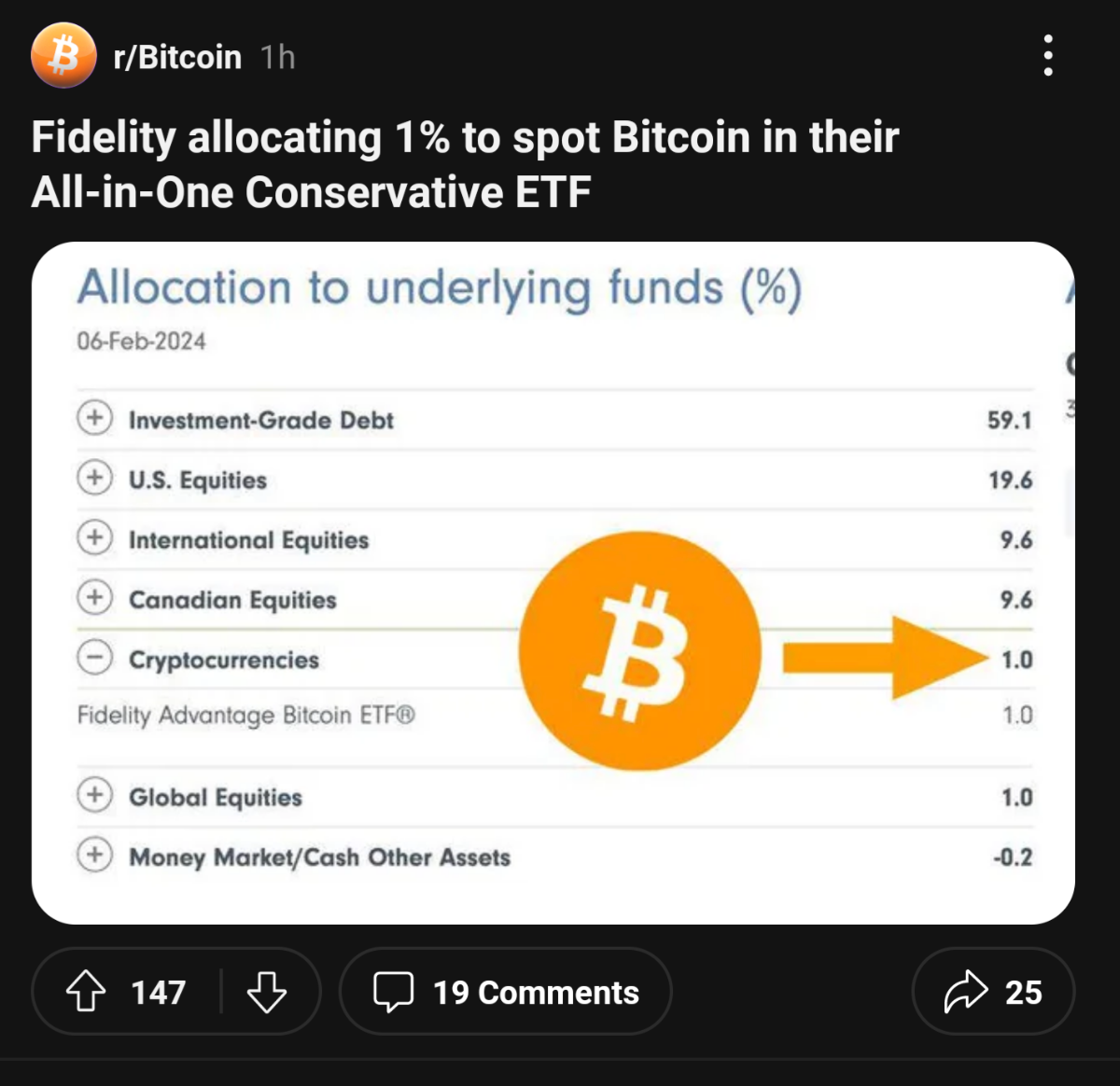

14 hours ago, james22 said:

Not quite here yet, actually.

1% of $168M, not $4T.

Fidelity Canada. And this allocation has been around for years and Canada has had a BTC spot ETF for three years now.

https://www.reddit.com/r/Bitcoin/comments/1ala1yi/fidelity_allocating_1_to_spot_bitcoin_in_their/

Still, so fidelity has been able to hold people's btc safely for 3 years without issues? promising

Good call - hadn't realized it was already in the Canadian models either so I suppose still good news to me, but certainly less impactful.

That being said, hard to say it won't be a road map for US models now that the ETF is approved.

-

What's interesting about all of this, to me, is the 10% move today had me buying shares and increasing my position by 10%.

But I wasn't increasing my position by 10% when we were at this price 4-6 weeks ago. Probably 1/2 anchoring bias and 1/2 knowing earnings announced next week are gonna be amazing

-

17 minutes ago, Hektor said:

IF the share price tanks, what is the impact on (of) TRS?

Cash would flow out of Fairfax to the counterparty. But this dip so far only takes us back to where we were in January, so nothing to be concerned with on Q1 at this point as it's just reversing cash that would have been due to Fairfax.

Plus, we've got blowout earnings coming in a week that may take us right back up.

TRS is only concerning when the economy actually tips IMO. Then you'll likely have falling asset values AND falling liquidity as it drains cash from Fairfax's coffers.

-

24 minutes ago, gfp said:

Well he would be smart to exit before the annual report comes out, that's for sure. I suspect his best exit opportunity in the shares was to exit on this morning's open but I assume he expressed this "short" in the credit default swap market so who knows how those spreads look (not me).

Fairfax has no options and trades in in Canada and OTC - this isn't a very good "short and distort" candidate to get others on the bandwagon.

Yea, I dunno about how he expressed the short, but I tend to agree with Greg's take here.

I'd prefer Fairfax without all of the inter-related transactions, paper gains, etc. because it definitely muddies the waters

That being said, the transactions that are the most questionable are tiny, the transactions he points at that are off-balance sheet debt have already been identified as such here and were obvious done to raise liquidity and stay compliant with bond covenants amongst other things, and ultimately I would argue it's probably a good thing Fairfax has these relationships and avenues for recognizing value when the market won't give it to him given the regulatory importance of book value and liquidity for underwriting.

Just glad I got to pick up more shares before what is likely to be an absolute smasher of Q4 earnings. Looking at $1+ billion just in fixed income gains/coupons - not even touching equities or insurance which we know also did strongly.

-

Thank you, Muddy Waters!

-

4 hours ago, TwoCitiesCapital said:

Just got my Celsius distribution today. Had a hair over 0.5 BTC there and ~4k of stable coins.

My distribution today was for 1.6 ETH. 85% loss in nominal terms compared to what the crypto would be worth today had I just held the BTC and stable coin in my wallet

No idea what the value of the private mining co is ,or when I'll get my shares and it'll IPO, but that is supposed to be the bulk of the recovery.

clawvacks from on going litigation could add a few more %, but it's looking ugly so far in comparison to my cousin was made whole in BlockFis bankruptcy

Just updating here:

Received a second separate distribution of 0.1055 BTC.

Not sure how they decided the make up of BTC and ETH for the recovery, but I wasn't expecting two separate payments.

Better than what was implied by my original post but still a far cry from the crypto lost

-

In other news, it has begun....

No shock that Fidelity is first to incorporate it for model-type portfolios

-

Just got my Celsius distribution today. Had a hair over 0.5 BTC there and ~4k of stable coins.

My distribution today was for 1.6 ETH. 85% loss in nominal terms compared to what the crypto would be worth today had I just held the BTC and stable coin in my wallet

No idea what the value of the private mining co is ,or when I'll get my shares and it'll IPO, but that is supposed to be the bulk of the recovery.

clawvacks from on going litigation could add a few more %, but it's looking ugly so far in comparison to my cousin was made whole in BlockFis bankruptcy

-

7 minutes ago, blakehampton said:

I don't know who would buy 10 years at a 4% yield. It seems to be an exceptionally bad deal when you can easily get 5-5.5% on your money short-term. I do know that the Fed owns a shit ton of 10-years and it seems like they are manipulating the market downward, I don't think anybody knows how that situation will end. On your point of DEO and MSGE, I don't disagree that there are deals in larger capitalization stocks, it just seems to me that they are very rare. How do you know that earnings will be this high going forward and that there will continue to be double-digit growth? I'm quite skeptical.

Is what you're seeing rational? This is of course very general, but do you think that people will do well getting in at these prices?

Why own the 10-year? Because a money market won't go up 10-15% if the Fed cuts to 2%. It's total actually falls as every day a portion of the money market resets to lower yields.

Govt duration is a primary hedge in most risk-off environments. 2022 was an exception given that it was an inflation scare and yields started at 0% at the start of it.

Cryptocurrencies

in General Discussion

Posted · Edited by TwoCitiesCapital

I agree. I think it'll just take more time.

The company I worked for was asked a question about BTC during an educational conference with our advisors 2 years or so ago. They laughed it off And basically said our clients were better off not owning it after the rapid drawdown we'd just seen. There was no intellectual honesty about it being the best performing asset over 3- and 5- year periods even after that drawdown.

Now that's it's gone up 2-3x from those amounts, there's still no one really talking about, or recommending it.

I'm sure over time more and more clients/FAs will push for us to allow it and have guidance on it - especially with the ETFs now available. But it's going to take time. We're not chomping at the bit to add it just because it's up 300% from the lowd and I imagine other firms are similar which is why you're seeing them block clients from owning it at this time.

I think we get one more cycle starting this halving. BTC may go up to 200-300k as the FOMO will be more widespread, but still not driven by the institutional adoption. Then we'll come back down to 50-100k in one last shakeout and from there the adoption curve will really take off as 2-3 years will have passed.

Market cap will be sufficiently high to start accepting widespread inflows from retail and corporates. That'll drive the market high enough to allow for the entrants of countries/sovereign wealth/central banks.

.