TwoCitiesCapital

-

Posts

4,637 -

Joined

-

Last visited

-

Days Won

6

Content Type

Profiles

Forums

Events

Posts posted by TwoCitiesCapital

-

-

-

2 hours ago, JRM said:

From a factor standpoint Bitcoin still trades like a high beta tech stock. I think it is still to be determined if it de-couples with gold over time.

The interesting sector is the gold miners (and silver miners). Gold is at all time highs, oil is around $80, and the mining stocks are severely depressed. Maybe they finally work this time?

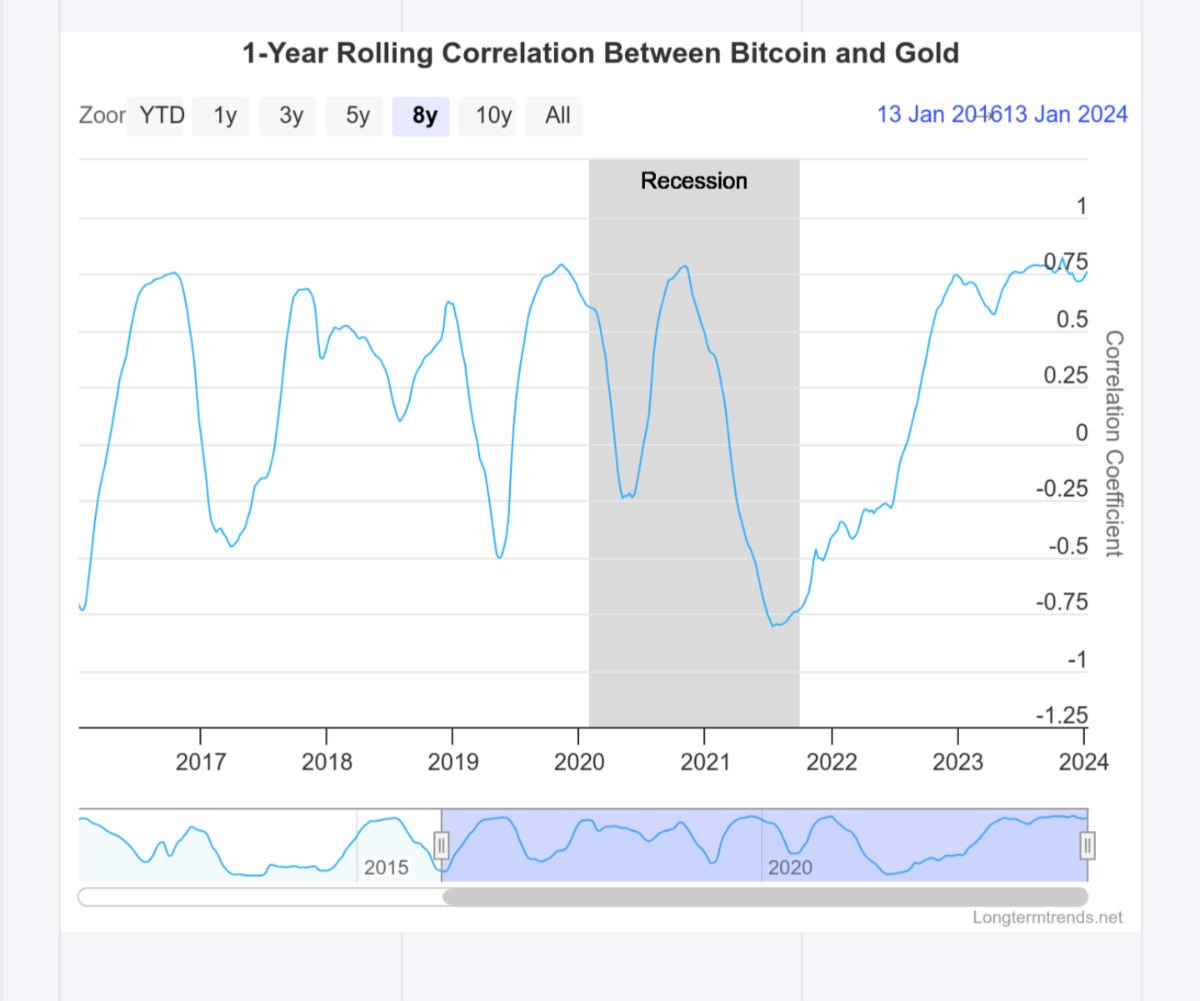

It's correlation to gold is pretty high at the moment.

-

15 hours ago, Sweet said:

Will it return to par though. Eg.https://finance.yahoo.com/quote/SHY/

5 year view. That should be mean reverting but it’s not.

Generally speaking it should behave bo different than the underlying bonds.

In this case, my suspicion is that as 1-2 year bonds rolled down to 0-1 year type bonds, they were probably sold and 3-4 year bonds purchased - all the whole rates kept rising and 3-4 year bonds kept falling in price. This appears to have stabilized over the past year which is what we'd expect with few hikes and the amortization towards par.

We'll likely see the opposite occur in a falling rate cycle. Bonds near par regularly sold to buy more 3-4 years which keep gaining on each subsequent rate cut.

So your ups and downs are amplified by the ETF trying to stay true to its 1-3 year target you basically press-the-bet on 1-3 year bonds instead of allowing them all to to zero.

Perhaps a better proxy for the underlying bonds would be to own a money market AND the 1-3 year fund so you have the spectrum of 0-3 years covered.

-

4 hours ago, scorpioncapital said:

is anyone worried money market etfs might have liquidity issues in a panic?

What we saw for client accounts in 2020 was that we continued to get daily/intra-day liquidity for bond ETFs and Mutual Funds in 2020, but it could take days to get liquidity for individual bonds when it came to individual Muni and/or corporate issues unless if we wanted to take massive haircuts.

Funds/ETFs will only have liquidity issues if the underlying bonds have them first. Outside of treasuries which remained very liquid, it actually seems safer to own the fund/ETF vs the individual bonds given how that has worked historically.

-

10 hours ago, Sweet said:

I don't like the treasury ETFs for the following reason - please correct me if I am wrong.

If interest rates rise, the ETF will drop and if you want to exit the position you have to sell the ETF and take the loss.

However when you buy an actual treasury you, and the interest rates rise, you can just wait for redemption at par to exit (if it is a short term bond).

So if it is within your means to purchase a treasury why would you buy the ETF?

Why can't you just wait a similar amount of time for the treasury ETF to amortize back to "par" i.e. rise in value?

Owning a vehicle that owns bonds isn't any different than owning them yourself in regards to how it behaves for rising/falling rates.

The primary differences come from fees and management decisions around what to buy/sell with inflows/outflows and the overall portfolio characteristics (average maturity/duration, coupon, etc).

If you don't trust a professional manager to make those decisions on your behalf, then you shouldn't own a fund in the first place. Basically, it has nothing to do with how the vehicle behaves in response to interest rates.

-

3 hours ago, blakehampton said:

I’m deciding on whether to stick with my Fidelity money market or switch over into BIL. I’m curious on what you guys do with your cash.

If it's cash as to not bear risk because it may be needed, money market and high yield savings account.

If it's cash that's waiting for a better opportunity to deploy, my preferred vehicle is JSCP at the moment.

-

23 minutes ago, ValueArb said:

Gemini settled with NY. It appears to me they only got a slap on the wrist ($37M), the regulator is using the $1.1B number to make it seem like a big win, but that's just returning customer funds they were going to return any ways. And no indication that Gemini will have trouble coming up with the funds, though the wording of what is being returned is "will result in all Earn users receiving all of their digital assets back in kind" which I am too lazy to go to regulators press release to parse out what that means.

Doesn't seem like the NY regulator views this as some massive fraud on behalf of Gemini either if they were willing to settle a multibillion "fraud" for just $37 million.

I mean, Wells Fargo has probably paid that amount in settlements every month for the last several years

-

1 hour ago, Castanza said:

I don't think he ever disclosed it, but he did say it was "life changing money" for his family. Some sleuths out there found that he bought a 7.8m house in Mass and has 6 luxury/sports cars (Aston, Porsche etc.) registered in his name.

Yea - I know he was still holding $10+ million when he went quiet and has suggested he wasn't selling

But I also believe he has disclosed that he'd taken $5-10 million off the top at different times as he rolled some of the contracts so he probably did well even if he never sold another contract and rode them down to being worthless

-

10 hours ago, james22 said:

It's beginning.

I was beginning to wonder if yesterday was the start of the FOMO.

Strange it may be happening before the supply shock, but perhaps 4th time is a charm for markets to actually be forward looking.

-

31 minutes ago, ValueArb said:

No, because they created and sold a fraudulent product on their platform, they are guilty of fraud.

I don't think this word means what you think it means.

31 minutes ago, ValueArb said:So you are asking me to spoon feed you all the legal claims and evidence that has been provided against Gemini? It doesn't seem you really care that much if you aren't reading it on your own.

Im not going to pretend to be an expert on everything that is happening (BlockFi, Celsius, FTX, Genesis, etc). It's a lot. There's a ton of cases, filings, bankruptcies etc.

But I am following it more than a casual armchair observer because I had money at stake in multiple of the platforms and am involved in the Celsius bankruptcy.

I'm open to being wrong, but ultimately from what I've seen it wasn't Gemini that did anything other than perhaps vetting Genesis to be the one who provided the services.

BlockFi and Celsius both used used some Genesis' product on the back-end as well. It's my under Genesis originated 70+% of the crypto loan volume before it's collapsed. Everyone used it.

It's Genesis seems to be largely at fault. Celsius has some questionable activities like the CEOs friends and family yanking tens of millions of deposits while he was separately tweeting about how safe/sound everything was. Additionally, they lied about concentration and collateralization of the loans.

BlockFi and Gemini? From what I've seen, they largely just got caught up as collateral damage and ice yet to see anything show untoward behavior. And Gemini survived that where few others did.

31 minutes ago, ValueArb said:Paying interest on loaned assets makes Earn tick a few more boxes on the SEC definition of a security than a generic crypto coin.

Perhaps. But it's the same agency that thinks a token that provides no ownership interest, no interest, no anything constitutes a security as well.

Some things in crypto are fundamentally the same - like banks and a need for regulation and transparency. Other things, like tokenization and DAOs aren't entirely different and need rules to be throught through.

-

1 hour ago, ValueArb said:

Why have a conversation if you don't read anything I wrote?

So because they advertised a product on their platform, they're guilty of fraud?

Interest WAS being paid. Returns were being made. But it was riskier than advertised and the risks blew it up. Can you prove that Gemini knew it was riskier?

Genesis certainly knew. They were the ones making the loans. They absolutely lied, concentrated the loans, and encouraging risky behavior from the borrowers.

But prove to me Gemini committed fraud by offering the product. What internal documents? I'm not following the trial in detail, but what I've seen so far is Gemini pulled billions in client funds from the program which is, in part, what toppled the house of cards. Not that they continued to add to it.

And as far as the SEC? They also said that Bitcoin spot ETFs couldn't proceed while approving futures ETFs and had to be taken to court, wasted years, and millions of investor dollars through inflated fees and negative roll yield because of it. The SEC has an axe to grind against crypto for whatever reason and their lawsuits against ripple and Grayscale prove it. Not sure that it was fraud just because the SEC called this a "security".

-

Just wanted to point out that there is no option for 50-100k.

You have 10-50k and then 100k.

Someone who owns, say $60k of shares, has nowhere to vote.

-

17 hours ago, ValueArb said:

Maybe it’s their BTC stake that has you so wound up here, but Gemini committed fraud, WeWork didn’t. Avoiding bankruptcy over money you frauded from customers isn’t a badge of honor.

What fraud did Gemini commit?

If you were accusing Genesis if something, I might could agree with you. All I think Gemini is guilty of is perhaps poor due diligence in selecting a partner for the product.

Maybe it's their BTC stake that has YOU so wound up?

-

27 minutes ago, ValueArb said:

Lets not make false equivalencies, its a poor analysis tool. Adam Neuman got paid off because Softbank and other investors wanted to continue the business without him, as far as I know non alleged any fraud on his part, being a bad CEO and spending like a drunken sailor aren't crimes.

Trump has been convicted of fraud, but not in combination with the bankruptcies of his subsidaries. He's mainly rich because of his inheritance. Bank CEOs always are well paid, and should be given their stewardship of billions in shareholder investments and client funds. In 2008 the administration should have clawed back more compensation in exchange for bailouts, but didn't. That's on the administration.

Gemini promoted a financially unsound Earn program (and illegal according to the SEC) to clients, promising imaginary returns that weren't supported by the collateral. Their own internal documents showed they knew this, and that they kept promoting it even when they knew Genesis was at risk of failure. The issue isn't that their main investment filed bankruptcy, its that they lied to clients about the safety of their investments, including using misleading language to lead clients to believe their deposits were FDIC insured. All of these allegations, if proven, are fraud.

What I'm hearing is you're making excuses for Adam Neuman, Trump, and Bank CEOS being rich after failure, but the Winklevoss can't be afforded the same excuses when a firm they partnered with failed?

Did I get that right?

Point is, this is what bankruptcy does. It takes the onus off the executives and decision makers and onto those capitalizing the firms debt/equity. It's ALWAYS the capital providers who lose in bankruptcy. Employees still get paid. Lawyers get paid. Trade claims get paid. Equity and debt? Well that's for the courts to work out.

This is how EVERY bankruptcy works. Not just the Winklevoss' - which is itself a misnomer because their firm is still operating and avoided bankruptcy.

Outside of Gemini, the Winklevoss brothers are probably some of the largest holders of Bitcoin as it's estimated they still hold over 70,000 BTC that were purchased largely from their Facebook settlement proceeds. There was never any questions they'd still be filthy rich even if Gemini went bust.

-

5 minutes ago, ValueArb said:

The Winklevoss twins are still filthy rich apparently, giving $4.9M to a superpac. I was worried they'd gone broke because of Gemini Earn but apparently only their investors and clients did.

Gemini is still a functioning brokerage, no?

Thought they just halted withdrawals from their Earn program because Genesis couldn't make good on it?

Could be wrong. So many bankruptcies in this space, but also this is how bankruptcy typically works.

Adam Neuman is still filthy rich despite WeFail. Trump is still stupid rich despite having multiple bankruptcies. Bank CEOs circa 2008 largely remained super wealthy after the bank failures and consolidations. This was the intent of bankruptcy process - protect those taking the risks so they keep taking risks to push business forward.

-

7 hours ago, Luca said:

If a collectible falls so hard in value and gains so hard in value within such a short time frame, it is simply not a good collectible. I'd rather buy a collectible that has very high desire from very wealthy clientele and holds/rises in value over time.

Can you name a collectible that has outperformed BTC since 2009? What about since 2019? Just curious why all of these desirable/rare collectibles are a better buy than the thing that continuously trounced them in its adoption/growth/price trend?

7 hours ago, Luca said:i dont see how you are better off buying a "bitcoin" then buying real assets that will be productive 20 years down the road.

Good thing they're not mutually exclusive. I own both. But if I had to pick one, I'd pick BTC for any incremental add outside of my residence.

7 hours ago, Luca said:Bitcoin needs government approval and implementation, any sane democracy understands that controlling the currency is a significant lever countries need to flourish, why would they surrender that control to bitcoin?

And yet, so many democracies relinquish control of their currencies to peg to the $....

or relinquish control of their resources to have access to the world bank/IMF funds....

or allow themselves to be puppeteered in global affairs to retain access to the USD banking system.

Yea, I wonder why any of them would look to BTC

7 hours ago, Luca said:

7 hours ago, Luca said:I really dont, cash is trash. Assets is what one wants to own, high quality and on a cheap price.

$50k BTC is as cheap today as 5k BTC was in 2017.

7 hours ago, Luca said:If you exclude speculators and traders, how many people do you know who use bitcoin in their daily life to buy groceries and other important things? I dont know anyone, i dont know anyone who knows anyone doing that either.

1) there are many.

2) there's a law of good money vs bad money that explains why it isn't more

7 hours ago, Luca said:7 hours ago, Luca said:Why would the german, france, UK, US, Chinese government want to lose control of their currencies? What will happen in a depression where stimulus is needed? What with a pandemic? Bitcoin is a bad currency that does not match the flexible needs of a countries economy.

Yes. One absolutely needs a currency that can be devalued so that a country can continue to make the mistake of too much leverage and debt over and over and over and over again.

You're absolutely right. There's no other solution.

7 hours ago, Luca said:Currencies were never meant to be an investment and to hold their value over 100 years. Assets on the other side do.

Then perhaps you should start seeing BTC as an asset. Because it's both.

-

1 hour ago, Luca said:

A collectible isnt going down -70% and then up 100%+ in a timeframe of half a year to a year. No Picasso ever.

Collectibles is a broad term that includes more than Picasso.

Wines. Whiskeys. Cars. Sports cards. Beanie babies. Absolutely have booms and busts associated with all of them. And many of those have busts, and booms, that absolutely mimic -70% and +100%.

Back in the early 90s, you could find used Porsches for cheap. The company's sales halved for new cars and used car prices were in the dump. Now? Cars from that era literally go for 100k + as collectors items. Significantly more than the cars sold new for back then. And cars are traditionally a depreciating asset? How's that for a bust/boom

1 hour ago, Luca said:1 hour ago, Luca said:It is absolutely no coincidence that bitcoin dropped so hard with tech stocks dropping and same is true with the upside. Ill guarantee you that the common variance with tech stocks is very significant and reasonable high. Arguably bitcoin wasnt as bubbleesque back then as it is now.

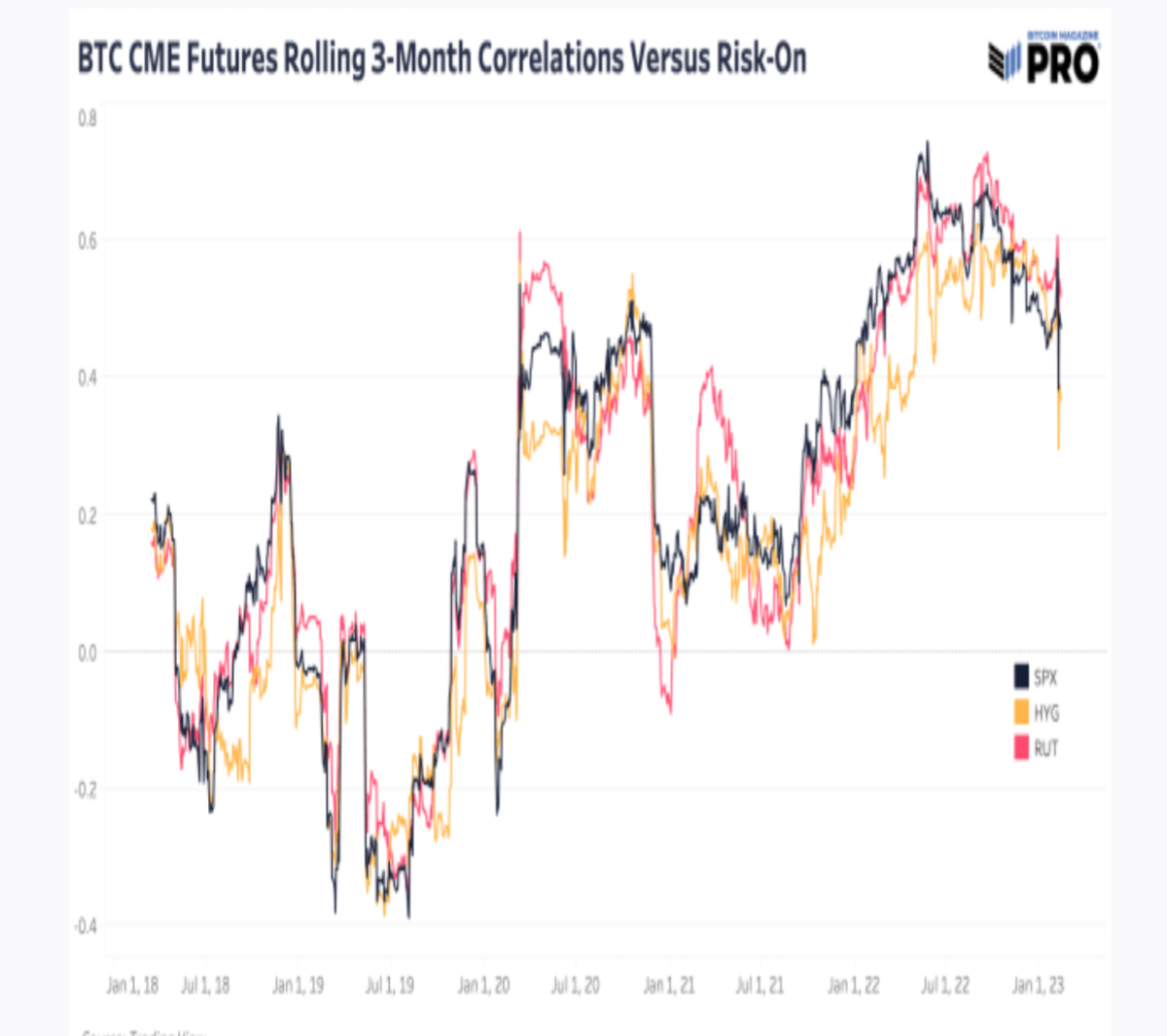

What makes you say no coincidence? Because the correlation has been negative, zero, and positive several times over the last 5-years. And is currently cratering...

Why should BTC behave differently going forward and simply be correlated with equities when historically the correlation is basically zero? What gives you confidence in this view?

1 hour ago, Luca said:And el salvador and central african republic are countries that the world looks to for imitation because their societies and economies are so successful?

Of course not. Countries looking for alternatives are ones that have previously failed. I don't why that isn't obvious to everyone out there. The countries who will switch first are countries who have everything to gain, little to lose, and likely have failing currencies.

But let me let you in on a little secret - every reserve currency before the USD has failed. So why is it you're so confident the US won't eventually get there? Especially after 5 decades of it losing value against real assets?

And why do you believe that the US getting there is the only thing that would justifies BTC having value?

1 hour ago, Luca said:"name a single bubble that survived for 15 years".

Thats the danger i pointed out right there. Just because it went this way has no support for the thesis. And the "market" doesn't know either as can be seen in the chart.

I mean, you seem to be willing to cast your faith in the USD/fiat currencies when history is literally littered with failures of the majority of them.

But you'll also assume it's BTC that is the one-off bubble as opposed to secular growth trend even when no other bubble has previously persisted this long through multiple busts?

I tend to to take my chances that history will repeat/rhyme rather than bet that both the USD and BTC are outliers. Especially since the BTC being an outlier of a bubble argues against the USD being an outlier of a fiat currency. And if the USD was an outlier of a fiat currency, then there likely wouldn't be a growing number of people using BTC every year.

-

7 hours ago, Luca said:

Bitcoin is the currency that nobody uses and a collectible that doesn't behave like a collectible."

He also questioned its role as a hedge, stating, "It's gone up as stocks have gone up, it goes down when stocks go down. This is not the way a collectible is supposed to behave."

1) that's EXACTLY the way collectibles behave. They always boom with the economy risk/assets

2) Bitcoin was falling for most of 2014 while stocks were rising. Bitcoin exploded in late 2015 while stocks were falling.

Bitcoin was falling in 2018 while market was flat to rising. And in 2021, Bitcoin cratered 50+% between May/July 2021 while stocks were still rising. Bitcoin didn't bottom until early 2022 - months after most stocks had put in their bottoms in 2021.

Multiple environments where BTC behaved significantly differently than broad equity markets. It isn't a collectible. And it's correlation to equities ebbs and flows and varies based on the time horizon you're observing it over.

7 hours ago, Luca said:7 hours ago, Luca said:It is incredible unlikely governments will allow bitcoin as a larger scale currency, especially in the current disorderly political climate.

El Salvador and Central African Republic already have. Others are considering it.

7 hours ago, Luca said:5 hours ago, Luca said:Its a dangerous vicious circle, the higher the price of Bitcoin goes, the smarter the speculators feel and the more inflows happen. "brilliant investor bought bitcoin 5 years ago" yadda yadda.

Name a single bubble that survived for more than 15+ years with multiple "busts" that made higher highs and higher lows?

-

4 hours ago, Sweet said:

A couple of years ago I had all sorts of people telling me they owned crypto. Mail man, guy who did building work around the house, most shocking of all was a few girls in work. I asked each of them whether they owned stocks and none did, one even replied they were too risky. This a long way of saying that I don’t think Bitcoin is in the early adoption phase as all.1) most of the people I knew buying crypto in 2020/2021 weren't buying Bitcoin. They were shilling shit coins like Doge and Shiba Inu trying to find the next Bitcoin thinking they'd already missed the boat on that since it was already 30-40k. Now the vast majority of those coins are down 90+% whole BTC is in reach of it's ATH

2) while BTC isn't new, most people don't understand it, don't allocate to it, and don't recognize it's value. We still have to have conversations why it's not great for criminal activity and why it's unreasonable to assume 100% of the world's electricity will be used for mining in 5 years which are the same tired arguments that I was making in 2018 before being orange pilled myself.

We're still very early in the adoption trend even if the technology isn't quite new any longer.

-

23 minutes ago, Paarslaars said:

When I looked into Bitcoin and started reading the recommended material here, I took 10% position. Not planning on increasing this simply because of risk management but will hold when it grows.

Welcome to being orange pilled

-

7 minutes ago, blakehampton said:

Out of curiosity, what kind of bonds?

I like intermediate mortgages and treasuries for my core bond exposure. Can get 4-6% YTMs here without doing anything sexy or trying. Things like RGVGX, JCBUX, TLT, ZROZ, and etc. here. Primarily buying in accounts where my investment options are limited like 401ks, HSAs, etc. Best returns here will come from a rate cutting cycle.

In other accounts where I have a bit more freedom, I like short-duration spread sectors, CEFs @ discounts to NAV, agency mortgage REITs, and other higher octane/leveraged positions. This is for more "oomph" if the economy manages to avoid/delay a recession. 5-10% expected returns here aren't hard in a scenario where we avoid a hard landing OR keep hiking rates.

JSCP --> 5.9% YTM @ 2.7 years of duration

JLS --> 10+% yield @ 10+% discount to NAV w/ sub-2 years duration

AGNC stock --> ~15% yield at the moment

TLT call spreads for leveraged duration exposure

Have also been looking at some other CEFs (like WIW and WIA for leveraged TIPS exposure), but am waiting to be opportunistic when discounts are widening.

Ultimately, my positioning is motivated by 3 things:

1) I work in finance and my compensation is impacted by equity returns - I like to have diversification to equities for this

2) I don't need anything higher than 6-7% returns to retire comfortably in 25-30 years. If I can get that in fixed income, why take the risk in equities?

3) I believe that history demonstrates fixed income will likely outperform equities in environments of volatile inflation and economic weakness. I expect both over the next few years

-

1 hour ago, Cigarbutt said:

The questions are not to annoy or to trap into some kind of useless discussion.

i don't know how to value cryptocurrencies and want to learn..

IMO it's still not clear, to most, what a cryptocurrency really is and my current understanding is that if the definition evolves towards what money really is, cryptocurrencies are likely to become underwritten by publicly shared institutions based on trust.

With the evolving money experiments since GFC and Covid, 'we' have seen various versions of the Cantillon effect (with money preferentially permeating to lower income quintiles since 2020 (!) at least for now which is kind of the opposite of what the referenced links describe) and 'this' is still work in progress*. It's hard to see how money management at large becomes so decentralized without a major regime change overall.

*progress in the sense of general improvement over time given science, reason and humanism.

How to value it becomes the case of valuing any commodity. Supply vs demand. How much it's worth is how much someone is willing to pay for it to have immediate delivery.

How much someone is willing to pay for it will depend on how much value it provides them. While I have no fancy/sophisticated model to map the supply vs demand date for current pricing minute-to-minute, there are some thoughtful models put together to try to assess the longer-term value which can then inform some smoothed price prediction removed from the minute-to-minute supply/demand imbalances.

The best work I've seen done on this is by N-Squared where he applies the Metcalfe theory to the Bitcoin network in terms of describing network value based on the number of users the network has. Beyond that, he makes informed assumptions about how quickly that network will grow to get a smoothed price projection into the future. Then its just a matter if discounting back to the present with your hurdle rate for what price you should be buying it at.

There's also the Stock-to-flow which is just focused on supply-side dynamics as has been a model for other commodities in the past. I like this one less for BTC because the price of Bitcoin would go to infinity once the supply dropped to 0 in 100+ years. With that, we know the model will break at some point. So far, it has been reasonably good at identifying inflections in the price and an upper bound as to which the price will likely trade and may continue to be useful in the intermediate term.

-

1 hour ago, Haryana said:

Volatility can be good for those who understand their hold and stay for the long term.

The danger is if they go out of business but then your cash holding bank can also fail.

"All I want to know is where I’m going to die, so I’ll never go there." - Charlie Munger

Absolutely. I agree.

Except cash isn't volatile. Treating Fairfax as a cash equivalent because of the fixed income it owns will likely be a mistake in volatile environments - environments where cash would be expected to "gain" in relative value where Fairfax might be "losing" relative value

-

15 hours ago, Haryana said:

I see it as a simple thesis that Fairfax is better than cash because that cash is in Treasuries with better than free leverage.

Just be careful applying this in practice.

Fairfax owned a ton of cash/short duration bonds in 2020. The stock still was down over 50+% from the peak despite that.

This was also demonstrated in 2008 where the stock of Fairfax was falling even while it's CDS were printing money.

In a panic, it'll trade like a stock regardless of how well it's underlying assets are doing.

-Poll- How much Fairfax does the board own?

in Fairfax Financial

Posted

It's a ~9.25% portfolio position for me which is basically right at my self-imposed limit of 10%. I also have ~3% in Fairfax India and some overlap with their individual investments like the ~2% allocation I have to Eurobank which is why I haven't added more to Fairfax despite technically having some room to do so.

As part of my net worth, Fairfax/Fairfax India are just shy of 10% collectively.