BG2008

-

Posts

3,039 -

Joined

-

Last visited

-

Days Won

1

Content Type

Profiles

Forums

Events

Everything posted by BG2008

-

Dude, you need to allocate to some private self storage and pay someone 2 and 20 to lock up that capital LOL

-

What Is the Best Investment That You've Ever Made?

BG2008 replied to Blake Hampton's topic in General Discussion

Okay, I hope this would be interesting. It was buying the Peter Lynch Book One Up on Wall Street I don't consider myself that bright. I'm a hard asset guy. People who met me in person know that I'm kind of a burly guy who's better at REITs and physical stuff. The book was $7 or $10 But Peter Lynch talked about how rock pits are good businesses, it just kind of stood out. It was a very simple concept. Cost $10 a ton, cost $10 to truck it 30 miles etc. In 2015, Patriot spins off the RE business which became FRP Holdings. I bought the stock at $30. Made it a 26% position and a huge position in my PA and told my family to buy it. Blackstone buys the warehouse for $359mm. The EV that I paid was $340mm but they still owned the MF and the rock pits and other cats and dogs. We made a double. I also raised outside capital because of this idea. Fast forward to 2020, Covid hits and FRP Holdings was trading at $40 but The Maren leased 45% of their units during Q2 of 2020. Holy Shit! They leased 45% when people were not allowed to view it? WTF? Made it an 18% position and raised some more capital. In total, realized gains for my family and investors are likely closer to $2mm. Unrealized gains from the second investment in 2020 is around $4mm. These are gains from my own accounts and capital that I manage for others. The gains alone are double digit % of my current asset that I manage. All of this from a book that Peter Lynch wrote about containing some little nuggets about rock pits. Investing is funny like that. You get an insight that is timeless, i.e. rock pits are good business. You get to know the assets, the management, the capital allocation, and the business. You can recycle the idea and come back. -

A little bit of a market rally and now we're talking about watering flowers and cutting weeds I thought we are value investors! Just kidding, yes, this strategy has a lot of merit. But then some of my left for dead positions are the biggest winners

-

I guess I'm really gonna miss those 0.9% and 1.9% car loan rates.

-

What is the car lease interest these days?

-

I have a 2020 Acura MDX with tech package where the lease is set to expire this Saturday. Got a quote from Acura for $29,963. In the past, I would just send it in and get a new lease. Given the car market these days, I am thinking of getting financing and buying the car outright as we've driven it ourselves mostly and have done all the oil change. Has anyone done this recently? To get financing, should I contact the Acura dealership? Or should I do it directly via Acura financial and get a loan from a local credit union/bank? Thoughts?

-

I'm not going to convince anyone on this name which is why I stopped talking about it. All that Sunbelt hoorahh, now it is facing a bunch of new supply. This is how one creates value in NYC residential. Who the F gives a damn about the opinion of @Gregmal some Jersey Trash or @thepupil some know it all from the Mid Atlantic who bench mark the company against other mega REITs. If you own half of a company, you try hard to make sure you don't do something to lose it all. You keep owning more RE over time. Which they have done without diluting themselves aside from the initial IPO. The funny thing is that everyone bitches about NYC landlords. But most multigeneration NYC landlords are wealthier than you, me, and Gregmal combined. So just keep owning more dirt in NYC and things tend to work out. People bitch and moan about NYC this and that. I'm a lifer. Leave it or take it. Now on the decent management skill. They just built a new MF to a 7% cap according to them. Will cash out $30mm from new loan if it hits the stabilized yield. They make sure all debts are non-course with no cross collateralization. Any of you asshats try to run this business and you'll probably get your ass handed to you. Alignment or mis alignment, I don't know, you get a 7% yield while they lease up buildings. It's not where I want the stock to trade. But here we are. It is what it is. If you want, you can create your own share buyback. Again, no one will believe me. So who cares. Someone of you need to try to pull off the financing they did in May 2020 with NYCB and in Feb of this year with 1010 Pacific. Those are master strokes. Probably never gets a bid, yada yada. But you get your 7% yield.

-

High Quality Multi-family REITs - EQR, CPT, ESS, AVB

BG2008 replied to thepupil's topic in General Discussion

What is the 1% rule? Can you expand? -

This puts a smile on my face. When I was younger and more immature. I would criticize a lot of active managers who did not have a 15% net CAGR over their careers. As I have gotten older and dissected more investment returns. Sequences of returns is absolutely a thing. Look at a lot of the heroes from 2020 that were up 100-200%. Look at a lot of fintwits who posted 30% CAGR since 2017-2018 during a period when if you went long "unprofitable growth equity" factors, you killed it. Imagine if you had money with someone volatile but also need to take out a certain $ every year. When you're down 50%, that 4% withdrawal is now 8%. All a sudden now, you're fighting a much harder war. Guys who was toiling and buying highly cashflow generative companies with low leverage got left behind and got called "washed out". My experience has been that if you've got wealth and you're older, you worry more about wealth preservation and beating inflation by 4-5% a year over the long run. How does this tie into bonds? It's the view that if you're wealthy already, you should have some bonds in your portfolio.

-

Farifax and their long bond trades? Anyone who bought long duration bonds in the early 80s

-

Who Do You Follow and What Are their Circle of Competence?

BG2008 replied to BG2008's topic in General Discussion

We want names!!! When are we going deer hunting or rucking on the beach here in NYC? -

Let's have a little fun I follow @Gregmal @thepupil @realassetsvalue for real estate related topics I follow @wabuffo for event driven and on $HQI, dude is smart I follow @Parsad James East for Fairfax related topics @Packer16 for Telco, distribution themes, interesting business models etc Just wondering who do you guys follow here on CoB, on Twitter etc and what would you say their circle of competence is?

-

I use a Aeron chair from an outlet store in Brooklyn. Bought it for about $700, the largest size. I was starting to get significant hip pain as I am a larger guy and weight a decent amount. The Aeron chair has been really helpful with getting rid of hip pain. Side note, I started squatting this past summer. It's done wonders for my posture, back, and hips in general. I only squat once a week, but tend to go heavier as it is a stress relief for me. I highly recommend it. Also just going out for walks is great as well.

-

Bought some options that are now way out of the money. Won't expire till Mid Jan. But would rather lapse them and take the tax loss for year end. Does anyone know what the mechanism for this is?

-

$ATUS has real value to me...as a tax loss harvesting candidate.

-

Down 99% for the year because I bought $ARKK calls People who are really down probably not sharing their pain Been hiring a couple interns/analysts for the business actually and having a good time mentoring and coaching them

-

https://twitter.com/Mr_Neutral_Man/status/1542575840483020800?s=20&t=hj6w8MPOylw1UtDflE6h9A

-

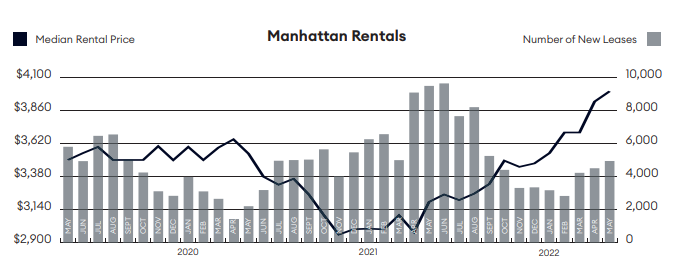

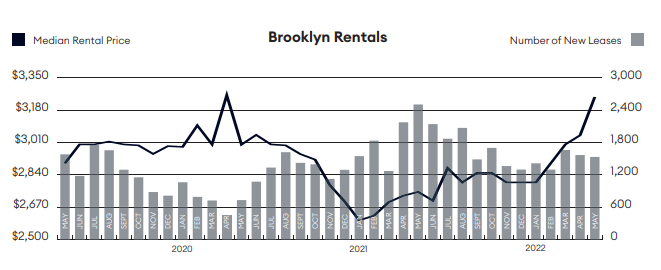

Manhattan and Brooklyn rent recovery - Nuts We're getting back to 2019 and go higher from there

-

TLT chart - Imagine buying US Treasuries and losing 16% in 3-4 months?

-

What happened to Glenn Tongue?

-

Yeah, but you need to log in and it's an extra step

-

Thanks for the feedback. I am not the people building the services. I just happened to find it and it will save me $1,000 a year or whatever it cost to use ValueLine. It loads quickly (faster than NY Public library) and is meant as a quick glance. When you wind up investing, you'll have to check the actual filings anyway. So good enough for me.

-

This is a really cool tool. It creates Value Line For Free https://roic.ai/company/BRK-A

-

Times in that AOL deal.

-

Will definitely shrink after Covid. That's why I think the $3 EPS goes to $2. Figure a 1.2 bn of revenue at 8% EBITDA margin instead of $1.6bn of revenue. Gets to you to roughly 10x P/FCF normalized in 22. Good management team gets you some optionality in growth and this company becoming AMN in the future.