glider3834

-

Posts

1,017 -

Joined

-

Last visited

-

Days Won

4

Content Type

Profiles

Forums

Events

Everything posted by glider3834

-

-

we have no idea who the parties are to this trade but is it hypothetically possible Fairfax could reduce part of their TRS position & in turn purchase the underlying shares directly from counter-party - could they do this under a block trade exemption to NCIB with security regulator clearance? I am just thinking if the 2% repurchase tax kicks in on 1 Jan then this would be an opportune time to do it.

-

This is what i found Under subsection 88(1.1) of the Income Tax Act, non-capital losses of a subsidiary corporation may be carried forward and deducted in computing the parent corporation's taxable income, but only in a taxation year of the parent that following the winding-up of the subsidiary. Subsection 88(1) of the Income Tax Act applies where a “taxable Canadian corporation” has been wound-up into a parent taxable Canadian corporation that owns at least 90% of the shares of each class, immediately before the winding-up https://taxpage.com/articles-and-tips/winding-up-a-corporation-per-subsections-881-882-842-of-income-tax-act/

-

yes but look its been a terrible investment for Fairfax so its really its just extracting something of value - turning a lemon into lemonade in a sense - they will need to call time on the turnaround at some point if there is no traction there & I hope thats sooner rather than later

-

viking I am no tax expert but Farmers Edge had circa C$500M in non-capital tax losses at end of 2022 & that number would be higher now & if FFH can acquire all the shares (they currently have 61%) for around C$4M by my rough math, then if turnaround fails & they then choose to wind up this sub, then Fairfax the parent corp I think could use those tax losses applying whatever appropriate tax rate. Farmers Edge hasn't recognised any tax asset due to its ongoing cash burn. I think as well as a private co. they would have lower running costs than a public co. Its end of tax year as well so given minority investors are likely sitting on tax losses there is probably intuitive sense to the timing. They have a new CEO who is trying stuff but its not showing up in any revenue numbers , its possible Fairfax will want to give him more time but the recent financing of C$6.37M feels like it has almost been calculated to the dollar- thats my impression anyway.

-

I think there may also be a contingency, tax planning objective here, in the event the turnaround is not successful

-

I would expect them to pay the fines & move along, but these delays to IPO are frustrating, but on the flipside IPO conditions now in India look better than late 2022 https://www.business-standard.com/finance/personal-finance/india-emerges-as-global-leader-in-the-number-of-ipos-in-2023-123110600198_1.html and it does allow Digit to include their latest financials for Jun-23 quarter in their IPO application showing Digit's improving profitability

-

https://www.prnewswire.com/news-releases/blackberry-announces-partial-extension-of-convertible-debentures-301986571.html I guess will allow Fairfax to free up around $200M to invest in higher return debt instruments

-

this article is relevant to discussion on valuation https://www.insidepandc.com/article/2cdgrj2sqw8zb25mjo2yo/specialty-lines/ipc

-

I wrote a bit a long winded reply but main point I would say is that we have to give Fairfax credit for their fixed income mgmt - luck plays a role but you have to put yourself in a position to take advantage - they saw more value in the optionality of holding cash over stretching for the limited yield on offer.

-

one potential driver of future earnings will be future additional impact on EPS if/when they acquire additional shares from minority interests in Odyssey, Brit, Allied - as premium growth slows & they can build excess capital in subs, they should be in better position to generate cash to pay divs to holdco &/or buy out minority interests IMHO

-

thanks viking its interesting how price can drive narrative

-

this is an interesting article on Pacwest deal for KW & FFH which shows it was a strategic acquisition & looks like portfolio is performing as expected https://commercialobserver.com/2023/11/kennedy-wilson-expanding-debt-platform-reach-pacwest-loan-acquisition/ 'The loan portfolio Kennedy Wilson assumed has remained healthy despite the many market headwinds that unfolded over the past 18 months due largely to rising interest rates. Whitesell said there are zero losses in the portfolio as a result of low leverage and a strong asset management team that actively works with borrowers to rebalance loans as needed. The portfolio is facing some looming maturities, with about half of the loans positioned for an immediate paydown and the rest expected to receive extensions, according to Whitesell.'

-

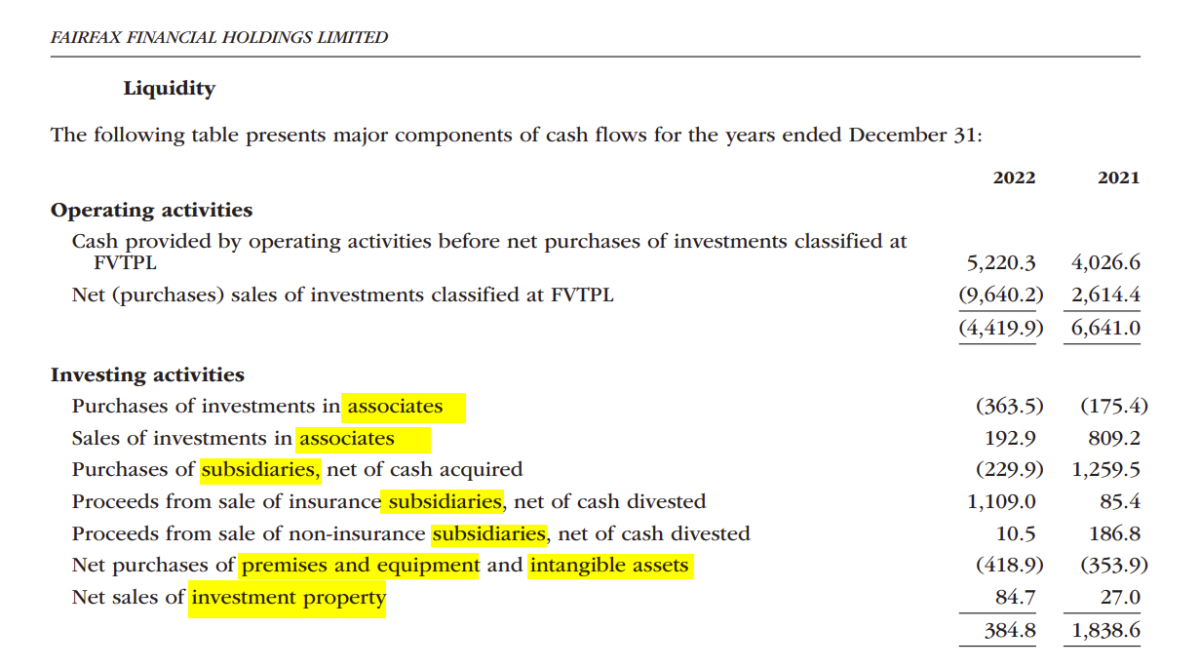

I am not an expert but I think under IFRS 9 if Fairfax's business model is managing certain financial assets for changes in fair value (see below) it would classify them at FVTPL assets - purchases & sales of these FVTPL investments appear under operating activities. These FVTPL designated investments are different to investments in associates, subsidiaries, real-estate, P&E or intangibles (see below) where purchases or sales of these assets appear under investment activities.

-

I think Fairfax can only take perf fee in shares up to 49% ownership 'In no instance will Subordinate Voting Shares be issued to satisfy the Performance Fee if, after such issuance, Fairfax and its affiliates would own more than 49% of the outstanding equity capital of the Company on the date of issuance.'

-

Yes would be good to know - I suspect they want to finish their actuarial review of y/e reserves before they publish an official number, having said that they probably update this number during the year, as they need to determine what dividends they can pay to the holdco from the insurance subs.

-

I am not sure if I have said this before so apologies if I am repeating myself, but I met Brian Bradstreet at the FFH dinner in the year after Fairfax had the big CDS win, he really came across as very down to earth - maybe not what you would expect from someone who had helped Fairfax make $2B or so on their CDS bet. I asked how he knew about the issues at AIG & he said it was there if you read the footnotes. My takeaway from this brief conversation was here is a guy with who doesn't have a big ego & who really does the work & that honestly impressed me.

-

looks to be Grivalia's largest luxury hotel investment With an investment approaching 300 million euros, Grivalia Hospitality inaugurated yesterday, with the participation of the Prime Minister , Kyriakos Mitsotakis , the head of Fairfax, Prem Watsa, and prominent names from the business and artistic worlds, the first luxury tourist complex One&Only in Greece and one of the three planned by the Kerzner International group in our country. https://www.powergame.gr/akinita/533059/to-proto-oneonly-anoigei-tis-pyles-tou-stis-11-noemvriou/#google_vignette

-

SJ yeh agreed - I dug into this a bit because I hadn't been able to understand the shareholding structure for Ki

-

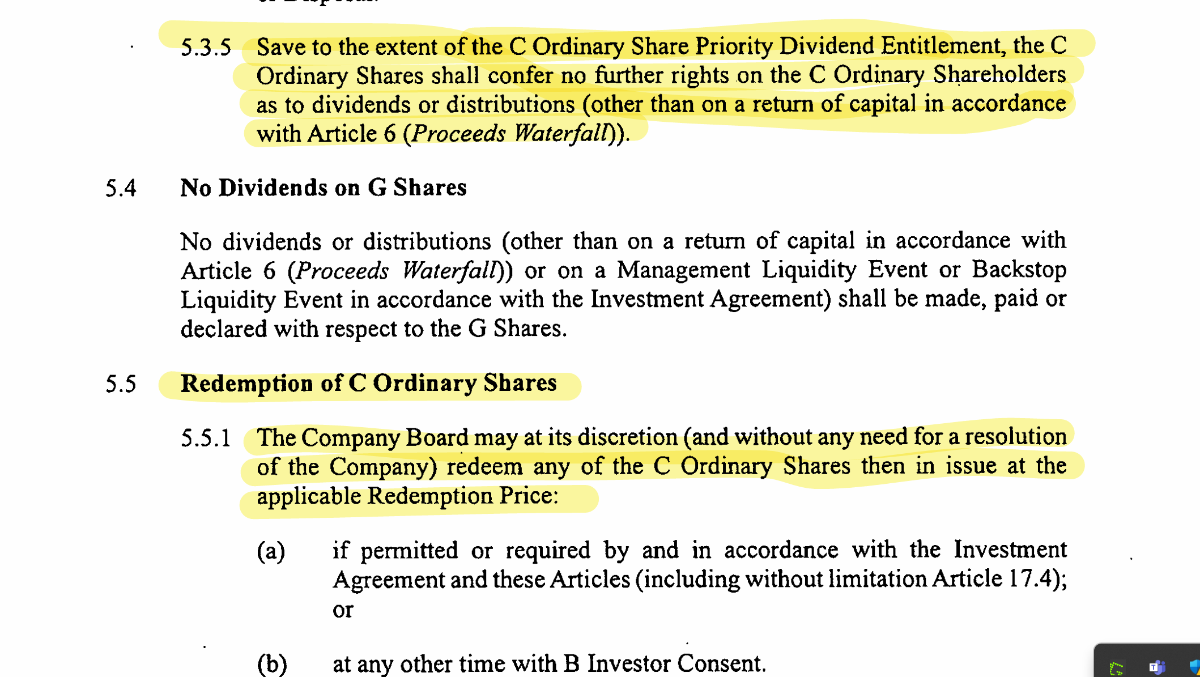

sure breakdown is Brit has 100M Ord A shares (1 vote each), Blackstone have 150M Ord B shares (0.64 vote each) and 250M Ord C Priority Div shares (non voting); and key execs have 80K Ord G shares (non voting)

-

Just looking at Articles of Association public filing from Ki Financial https://find-and-update.company-information.service.gov.uk/company/08821629/filing-history?page=1 With Ki, Brit has approx 20% economic ownership & 51% voting power. But interesting is that it looks like Blackstone's C shares (approx 50% of outstanding shares) carry a fixed 8% priority dividend entitlement, but are also redeemable by Ki (see below). Assuming Ki was able to redeem and cancel these C shares from Blackstone , it would increase Brit's ownership from 20% to 40% approx. Terms of Investment Agreement 19 September 2020 between Blackstone, Brit etc don't appear to be available, so we don't have all the information here. Recently Ki has been getting more traction in the follow market, so its worth considering what Ki could be worth and what Fairfax's ownership stake could be. https://www.reinsurancene.ws/ki-teams-with-travelers-aspen-to-expand-digital-follow-capacity/ https://www.insuranceinsider.com/article/2cc4cx6ph8z1opv140x6o/london-market-section/opinion-ki-who-owns-the-follow-market

-

-

https://www.insider.gr/epiheiriseis/294623/jp-morgan-katalytis-gia-ti-eurobank-i-exagora-tis-ellinikis-trapezas-blepei JP Morgan expects significant upside for Eurobank's shares , recognizing that the acquisition of an additional 7.2% (29,710,012 shares) in Hellenic Bank , thus reaching 55.3% and pending the approval of the regulatory authorities that will now make it a subsidiary of the group, will act as a positive "catalyst" for the systemic bank. In this light, the American house significantly increases the target price for the Eurobank share to 2.60 euros from 2.25 euros previously , with an "overweight" recommendation

-

check out https://www.bnnbloomberg.ca/greece-s-eurobank-plans-to-expand-overseas-wealth-management-1.1942573

-

they paid 380M dividends from insur/reinsu subs to Holdco in 2022 (excl C&F pet sale div) but only $79M in 1H23 so far (excl Brit div from Ambridge sale). So just to match 2022, they would need to pay another $300M divs to Holdco in 2H23. Looking at 1H23 operating income of insur/reinsur subs of $1.75B (vs $1.2B in 1H22) or increase of 46% YoY, & if things continue int he same trend over the 2H23, I think insurance subs might build decent amount of div capacity on top of $2.7B (rounded) level at 31 Dec2022. In 2022, the subs built up around $700M in div capacity (ie from $2B to $2.7B), after paying $380M in divs to the Holdco (with group interest and dividend income $960M in 2022) So if operating earnings of these insurance subs in 2023 are now trending over 40% above 2022 (with group interest & dividends expected at over $1.5B in 2023) , then couldn't we see an even bigger build in div capacity in insur/reinsur subs in 2023 assuming same divs paid to Holdco as in 2022? We are still not through end of hurricane season (he says with fingers crossed ) ,& there are always other risks that could create volatility in insur sub operating results, so nothing is guaranteed of course with the above, but really I am just trying to extrapolate what trends I can see in operating result of the insurance subs YTD SJ I do agree with you it would be better to see more cash in the Holdco over time