glider3834

-

Posts

1,017 -

Joined

-

Last visited

-

Days Won

4

Content Type

Profiles

Forums

Events

Everything posted by glider3834

-

when FFH IPO'd FIH it gave them access permanent 3P equity capital to fund deals and ability leverage their expertise/networks in India to generate AM fees. The ideal scenario for any asset manager is to generate good returns for investors, grow the capital pool and potential fee stream over time. If FFH were to fully privatise FIH by themselves, they would lose that 3P capital and AM fees and then there is the cost to fund/leverage considerations. So the question then is - is the value extraction opportunity so significant that it would justify a take private assuming they pay a 'fair & friendly' acquisition price etc? You could hypothetically have an Atlas/Poseidon type scenario where you get one or more investors (eg pension funds, sovereign wealth funds) who form a consortium with FFH to take FIH private - in which case maybe FFH (via HWIC) could possibly remain the asset manager and retains 3P equity capital with potentially deep pocketed investors - plus there are time/cost savings of not being a listed entity.

-

BIAL hold the leasehold until 2068 - about 5 years prior to expiry they have around 2 yrs to negotiate a mutual agreement with GoI to extend concession beyond that time https://www.civilaviation.gov.in/sites/default/files/2023-02/moca_000743.pdf

-

I think Fairfax will invest in a moaty business at the right valuation and they have tended to find more opportunities outside US like BIAL or NSE of India(recently sold) If you put businesses in the poor , good and great (ie castle wall like moats - think Facebook or Costco) categories. I think the seachange with Fairfax is they are now being more disciplined at avoiding the 'poor' business type situations (eg Farmers Edge) & preferring the 'good' category - track record of profitability, competitive strengths and quality mgmt. Investing is ultimately an exchange of cash flows (what you pay now vs what you receive back over time translated into todays dollars) and buying a good business at a fair valuation with potential for earnings &/or multiple expansion may be a better bet than paying 40-50x for a wide moat business where there is significant risk of multiple contraction, even if that business achieves the expected earnings growth rate.

-

One of Fairfax's most interesting positions, integrated energy utility and green metallurgy business Metlen (MYTIL.AT) (formerly Mytilineos) results out https://www.ekathimerini.com/economy/1244896/metlen-registers-record-profits-in-january-june/ Edison have an analyst report on Metlen & below is a quote from this report with their take on valuation. https://www.edisongroup.com/research/a-new-name-for-its-next-phase/33738/ 'Valuation: Undervalued for a €1bn+ EBITDA business Metlen currently trades at P/E multiples of 7.7x in FY24e and 7.2x in FY25e. It trades at EV/EBITDA ratios of 6.0x in FY24e and 5.6x in FY25e (our estimates are broadly in line with consensus), a significant discount to peers. As a comparison, its peer group trades at a range of multiples, from 5.2x for metals to 9.7x for RES, with an FY24 Metlen EBITDA-weighted average of 7.7x, a 38% premium to Metlen’s market multiple. In our view, Metlen’s multiple looks low for a business that has high-quality, low-cost assets in power generation and aluminium production, and very low for a company with a high-growth renewable energy business that accounts for almost one-third of its earnings. We value Metlen at €49/share (up from €45 in our last update). Our DCF valuation has risen to €47/share after incorporating recent results and some minor adjustments to earnings based on commodity, energy and electricity price assumptions, which are broadly in line with forward curves, and we now blend this with a peer multiple valuation of €51/share to reflect the potential of peer re-rating with an additional listing.'

-

-

viking I am not on the ground as you are in Canada, but I saw this article with quarterly survey by Stifel suggesting that while discretionary spending intentions are still weak there are perhaps signs consumer confidence is starting to improve. https://retail-insider.com/retail-insider/2024/07/canadian-consumer-spending-intentions-show-surprising-rebound-stifel-survey-reveals/?utm_source=rss&utm_medium=rss&utm_campaign=canadian-consumer-spending-intentions-show-surprising-rebound-stifel-survey-reveals Few quotes that look relevant to Sleep Country & mattress demand “Surprisingly, spending intentions are up sequentially in most of the categories we track and near a one-year-high. Categories such as mattresses, powersports, dollar stores, the pet industry, apparel and toys are all at or near a one-year-high,” said the report. “While our survey suggests improvement in Canadian consumer confidence, spending intentions are still in a pattern of contraction with 52 per cent of respondents being likely or very likely to reduce their discretionary spending over the next 12 months. Despite that, these results piqued our curiosity and suggest investors should start to think about how to position their portfolio under a scenario where Canadian consumer confidence returns to an expansionary mode. Our survey results are positive for Sleep Country, Dollarama, Aritzia, Gildan, Pet Valu, KITS, BRP, and Spin Master. “In our view, the results paint an accurate picture of the state of the Canadian consumer and historically the results have been generally a good indication of upcoming financial performance of our companies under coverage.” 'Signs of demand recovery within the mattress industry continues. The demand environment for mattresses in Canada has been challenging for the past two-plus years. However, our survey results suggest that the outlook is improving with spending intentions up for two consecutive quarters, and with July 2024 showing the strongest spending intentions since March 2022. Hence, we could see a scenario for a rapid pickup in demand as the economic environment improves;'

-

still early days but we have had some updates now from Beazley & WR Berkley - also Evan Greenberg possibly might provide commentary on Chubb's call tomorrow https://www.reinsurancene.ws/crowdstrike-outage-unlikely-to-materially-impact-re-insurer-results-fitch/ 'So far, prominent cyber underwriter Beazley has said that it will not change its current undiscounted combined ratio guidance of low-80s for its full year 2024 results in light of the event, while W.R. Berkley said it does not see the incident as a material loss to the company. No doubt other insurers and reinsurers will also comment on the IT outage in the coming days and weeks as second quarter results are announced, which should provide a clearer picture of where the ultimate insurance industry loss might fall.'

-

yes looks like that CAD 1.7B TEV figure includes lease liabilities

-

https://cyprus-mail.com/2024/07/12/hellenic-bank-board-rejects-eurobanks-acquisition-offer-as-unfair/

-

https://www.sedi.ca/sedi/SVTItdSelectIssuer?locale=en_CA

-

I think this article helps answer this question of the impact more broadly (my underline below) 'In brief, the data show that thus far, economic ties have not been impacted significantly, likely due to two factors: consistency in the supply and demand on both sides, and a lack of signalling by either government that they intend to take steps to hamper business ties.' https://www.asiapacific.ca/publication/despite-diplomatic-strains-canada-and-india-conduct-business

-

if Fairfax holdco is issuing mostly 30 yr notes plus some 10 yr notes to repay Allied's US$500M debt due 2025 then it could potentially be capital contribution or inter-company loan, if cap contribution then my question is will Fairfax receive increased equity ownership in Allied?

-

Grivalia Hospitality news article - looks like One & Only Aesthesis off to a solid start this summer https://www.ekathimerini.com/economy/1240403/grivalia-hospitality-continues-to-expand-offerings/

-

Fairfax's dividend from Eurobank should be close to EUR 116M based on 34% reported stake https://www.bloomberg.com/news/articles/2024-06-06/greek-banks-get-ecb-approval-for-first-payouts-since-2008-crisis?utm_source=google&utm_medium=bd&cmpId=google

-

no worries @Viking- definitely lot of moving parts with this deal

-

not sure but should be in public offer document - I did find this also 'the acceptance period starts (between 30 and 55 days, although it can be extended to 75 days) and “within 3 months of the end of the time allowed for acceptance of the bid”, the offeror has the right to “squeeze-out” (section 36(2) of the Takeover Bids Law).' https://www.globallegalinsights.com/practice-areas/mergers-and-acquisitions-laws-and-regulations/cyprus/

-

I believe they can't do a minority 'squeeze out' as they would need to reach a 90% shareholding first & issue is as you point out Demetra is sitting on over 20% They originally offered EUR 2.35 to Poppy S.a.r.l & others and that was raised to EUR 2.56 in line with mandatory bid - hopefully they can reach agreement but if not, this article tables some different scenarios if Demetra/Dimitra & ETYK don't participate in public offer https://www.philenews.com/oikonomia/kypros/article/1476226/theli-100-tis-ellinikis-trapezas-i-eurobank/ (might need google translate) one takeaway from article - Eurobank I believe would need around 75% of votes to approve merger of Hellenic with Eurobank Cyprus - so 75% would be key initial target with their public offer.

-

Eurobank S.A. has now secured 55.3% (~228M shares) of Hellenic and submitted mandatory takeover bid for remaining shares 44.7% (~184M) at €2.56 per share https://cyprus-mail.com/2024/06/04/eurobank-now-holds-55-3-per-cent-stake-in-hellenic-bank/ https://www.eurobank.gr/en/group/grafeio-tupou/etairiki-anakoinosi-04-06-24

-

I think BW sets out in his tweet that they will be each fishing in different ponds but yes both in India. https://x.com/benwatsa/status/1797745797280170441

-

no - most recent KBRA report below - but I do notice their secured vessel financing program has BBB rating 'On August 23, 2023, KBRA affirmed the BB+ issuer rating of Atlas Corp. (Atlas), a global asset management company based in Vancouver, BC with focuses on assets in the maritime sector, energy sector and other infrastructure verticals. KBRA also affirmed Atlas' wholly-owned subsidiary Seaspan Corporation’s (Seaspan) BB+ issuer rating, the BB+ rating on Seaspan’s $750 million senior unsecured notes due August 2029, as well as the BBB ratings of Seaspan’s $1.1 billion Term Loan due March 2028, $410 million Term Loan due March 2029, and $400 million Revolving Credit Facility due March 2028 comprising the secured Vessel Portfolio Financing Program. The ratings Outlook is Stable.' https://www.kbra.com/publications/rrpFtbKq/kbra-releases-surveillance-report-for-atlas-corporation-and-seaspan-corporation

-

cheers @nwoodman here is their their weighted avg interest rate at Mar-24 'The weighted average interest rate for March 31, 2024 was 6.83% compared to 6.19% at March 31, 2023.' noticed they declared a 52M div on common shares in Q1, a 38.1M div paid Mar & 13.9M div paid in Apr - not sure if 13.9M was a special div ie a once-off or whether they have lifted their dividend rate from 37M per qtr in 2023 to 52M per qtr - we will have to wait & see over next few qtrs

-

https://www.tradewindsnews.com/containers/seaspan-to-splash-1-6bn-on-container-ship-newbuilding-comeback-sources-say/2-1-1651499

-

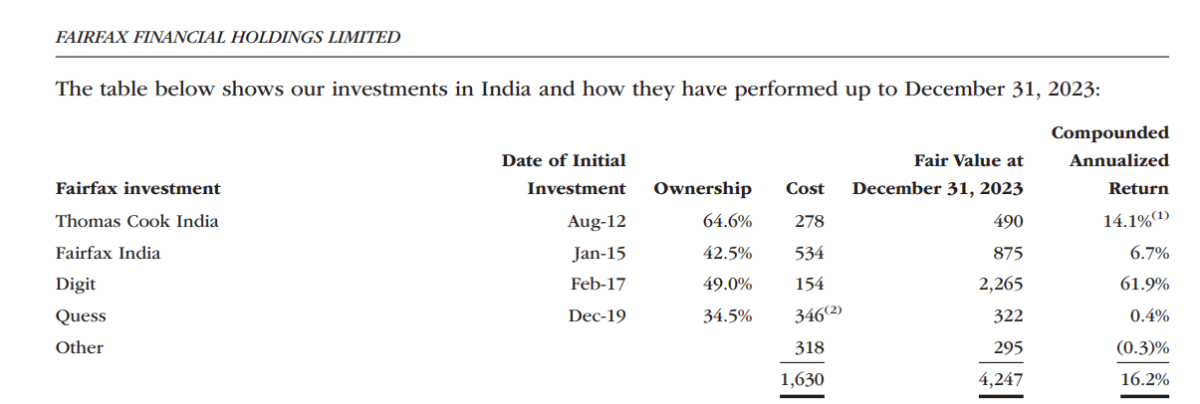

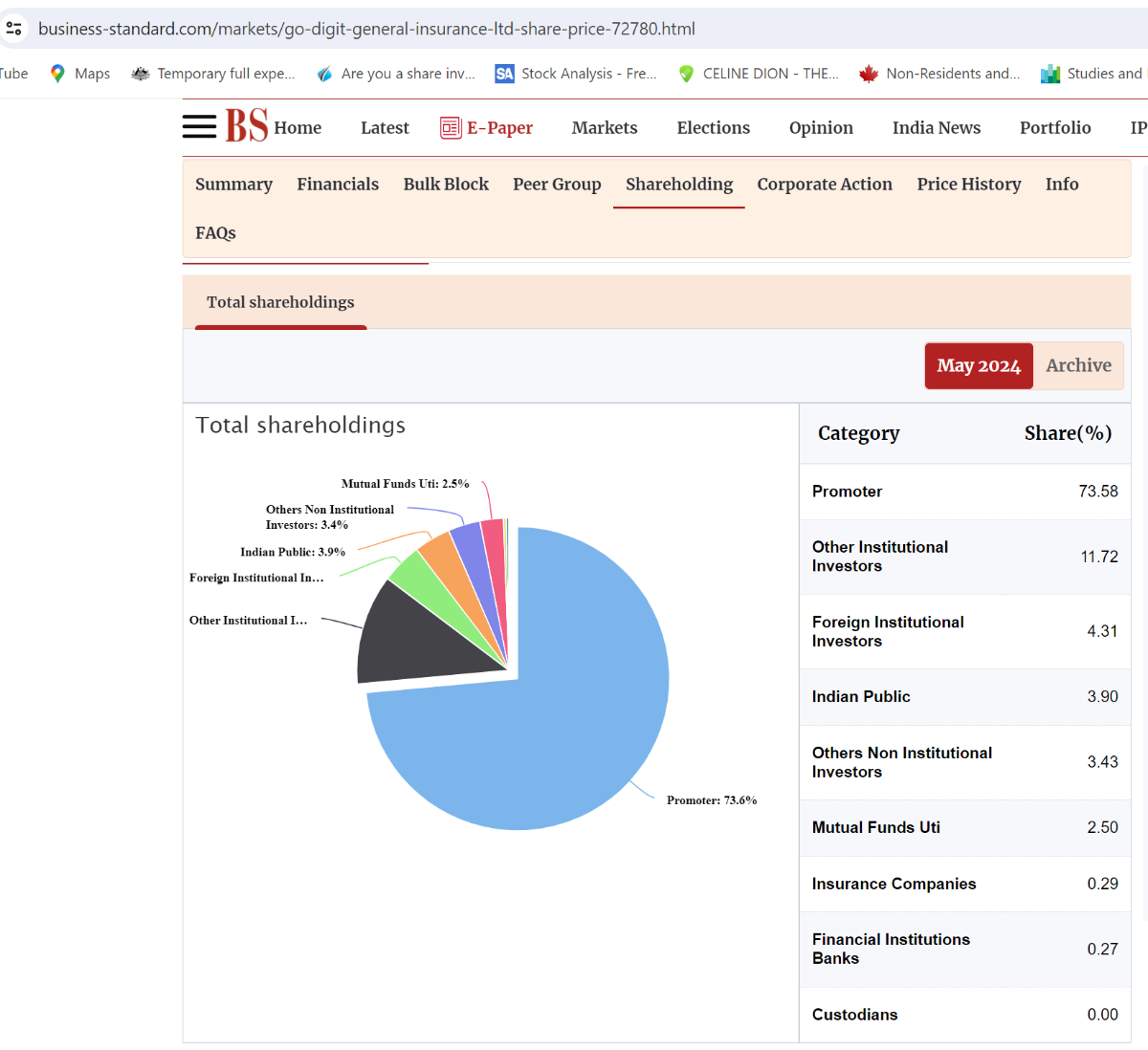

I have edited this post Here is my take below (opinion not advice) - feel free to correct me guys if we base it on current Digit market value I don't agree there is a big FV mark down here - FV looks to be around US$100M or just under 5% less than FV at 31 Dec'23 if we factor in value of GDISPL (Go Digit Life Insurance Pvt Ltd) stake in Digit Insurance plus proceeds GDISPL receives from IPO - also I am not factoring in how Go Digit Life 24.2% stake is being carried by FFH because I am not clear on this. i am unsure post Digit insurance IPO if Fairfax will use DCF/mkt price hybrid valuation method or use just mkt price for FV now we have gone to public listing on primary exchange. Also Fairfax is carrying Digit stake at $1.94B which is below aggregate fair value at 31 Dec23 because they are carrying equity portion at cost (CCPS at 1.79B and equity at 0.15B) GDISPL owns approx 73.6% of Digit Insurance post float or 674.8M shares in Digit Insurance (owned 729.5M share pre float, sold 54.7M shares in IPO) Digit Insurance - current mkt cap US$ 3.3B (current share price INR 300 or USD 3.60 (USD/INR 83.2) Digit Insurance shares outstanding post float 917M (876M pre float + 41M fresh issue) GDISPL current stake value US $2.42B in Digit Insurance Assuming there is conversion of CCPS (see below), FAL would own 82.07% of GDISPL - ie indirect ownership of 60.3% of Digit Insurance valued at US $1.99B) 'subject to the maximum permissible limit under applicable laws and the provisions of the JV Agreement, and would be cumulatively converted such that the CCPS holder holds equity shares of GDISPL representing up to a maximum of 82.07% of the share capital of GDISPL.' plus GDISPL sold 54.7M shares in Digit Insurance @272INR (USD 3.26) raising approx pre-tax US$178M less taxes Add these together & you get US$2.17B (less any taxes) for which is approx US$100M below FV of US $2.26B at 31 Dec-23 BTW I am unclear if Digit Life 24% stake is included or excluded in fair value for Digit?

-

https://cyprus-mail.com/2024/05/24/hellenic-bank-posts-e93-3-million-profit-in-first-quarter-new-lending-hits-e208-million/

-

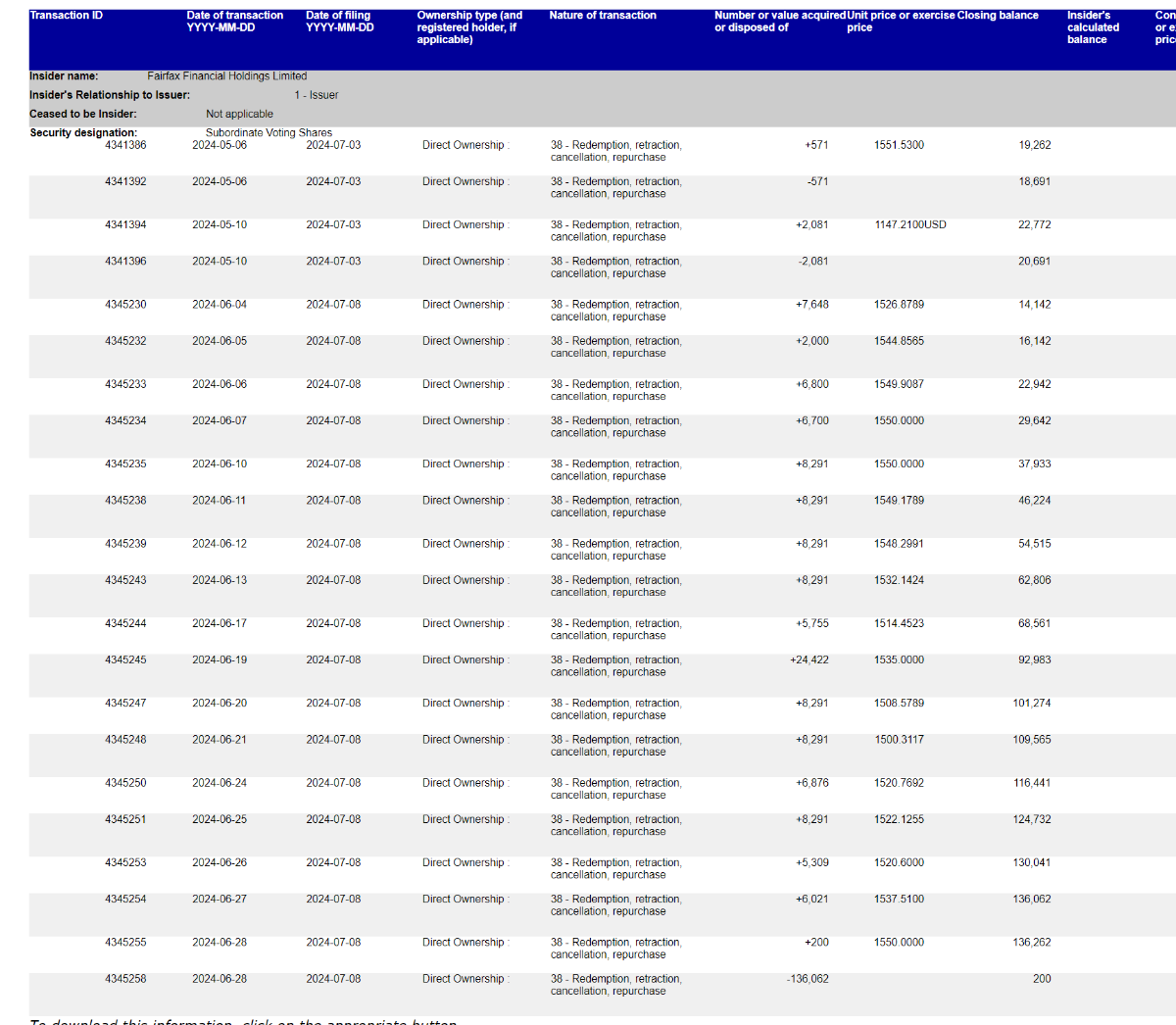

Fairfax buybacks ~ 130K shares during March & ~151K shares during April