gfp

-

Posts

8,122 -

Joined

-

Last visited

-

Days Won

20

Content Type

Profiles

Forums

Events

Everything posted by gfp

-

It's better than that - it's essentially a blended 10% yield to maturity on something like $3B in total capital. Plus the incremental investment in KW that should do well in addition.

-

Raising bank capital requirements at the onset of an already-underway credit crunch. What could go wrong?

-

Here is the Fairfax press release on the deal. Love it. https://s1.q4cdn.com/579586326/files/doc_news/2023/PRFFH-June-5-2023-KW-June-2023-Transactions.pdf " Taking into account the discount at which Fairfax acquired the principal balances of the Loans, Fairfax expects the average annual return on the capital deployed by Fairfax in connection with the Loans to exceed 10%. All of the Loans are secured by real property located in the United States with an average loan-to-value ratio of approximately 51% and are supported by completion guarantees issued by the project equity sponsors. More than 70% of the Loans relate to multifamily or student housing development projects with the balance being a mix of industrial, hotel and life science office property development projects." and " In addition to the Transaction, Fairfax also agreed to make a $200 million preferred equity investment in Kennedy Wilson. Under the terms of the agreement relating to the investment, Fairfax will acquire perpetual preferred stock that carries a 6.0% annual dividend rate and is callable by Kennedy Wilson at any time. Additionally, Fairfax acquired 7-year warrants for approximately 12.3 million common shares with an initial strike price of $16.21 per share, based on Kennedy Wilson’s closing price on June 2, 2023."

-

And froze out so many existing homes from coming on the market.

-

https://fred.stlouisfed.org/series/T5YIE You are looking in the rear view mirror. Also, the Federal Reserve is next to powerless when it comes to inflation - in either direction. If anything, they are increasing inflation with their current policy rate.

-

There hasn't really been a "huge rally in equities this year." There has been a very narrow rally in a few very large companies. RSP and IWM are basically flat. Look at 5 year TIPS breakevens. 2%. Exactly what the Fed is targeting. The Fed didn't slay inflation. If anything they made it worse. But it went down on it's own anyway and they can claim it was them and move on with the high-fives.

-

The high interest rates increase the deficit spending stimulus to the economy, skewing that stimulus heavily towards those who have lots of money already. The problem with the Warren Mosler type of lens on deficit spending and the economy / inflation is that it misses a much larger portion of the monetary system that isn't even measured by the US Government. The monetary system outside of the US dwarfs the measured stuff like M2. If the US monetary system was just what the Federal Government had "control" of, we would be roaring higher. Instead we are just putting along because all of this stimulus is being offset by tightening money, flight to safety, hoarding and risk-off behavior globally. The market is telling you inflation is dead for now and deflationary risks are rising. We'll see how far it goes but the risks are higher that things get much worse because there isn't anything the Fed can do. The Federal Reserve is basically powerless and more of a "placebo effect" or hoping that a projection of confidence sends the correct messaging that might effect behavior in the economy and get what they want. The level of the deficit, higher or lower, is much more effective as a policy tool but it won't be used that way except in the depths of a crisis. The amount of money out there doesn't matter nearly as much as the amount of money that is freely circulating / recirculating. When market participants start with the "risk-off" stuff, the recirculation of money in the economy slows down and that effect dwarfs the small effects of slight changes in the level of deficit spending.

-

That Morningstar analyst report reads like it was written years ago. On another note, does anybody here know if the profits on the total return swaps on FFH's own shares are tax-free to the company? I know that usually transactions in an issuers own stock are not taxed (for example if Biglari Holdings were to ever record a profit on their holdings of own shares the "profit" would be tax-free) - but I do not know if that extends to derivatives on an issuer's own stock.

-

Not sure if you are totally getting this chart, but this is maturities of debt owed by the regional banks, not the loans on their books. CMA would be the one on the chart with the most debt coming due this year, not the one with the shortest maturity loan book.

-

Yeah I was going to mention that there was a seller in addition to that buyer as well. I do think it is likely that the block trades get taken by FIH itself. I guess we'll find out later when they file on SEDI. There are probably investors looking to reduce their exposure to emerging markets and their currencies in this environment. The Indian currency looks to want to go on another leg lower against the US dollar. The central bank is intervening almost every day to supply dollars and prop up the INR. But it is still weak, bumping along the line in the sand at 82.75. It may be more of a general shortage of dollars in Asia than India-specific weakness. We'll see.

-

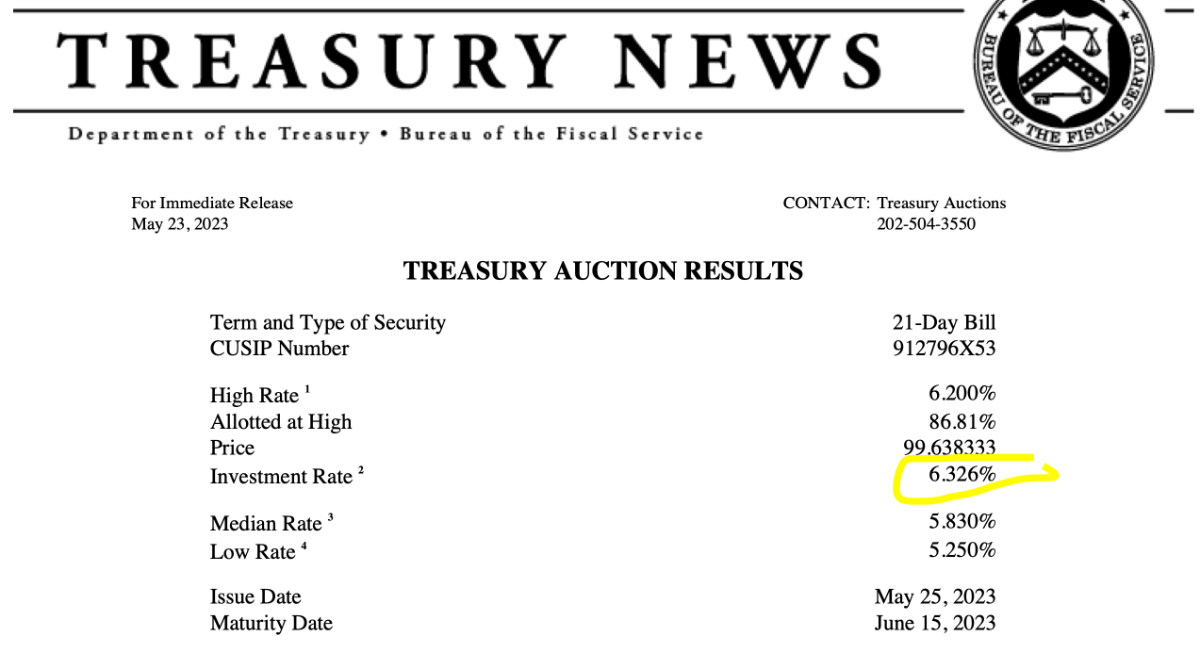

That is the coupon-equivalent yield on a $35 Billion bill auction for 21-day bills.

-

Meanwhile, Berkshire just keeps bidding on these distorted T-bill auctions!

-

Unfortunately it seems like the debt ceiling will probably not come to a head this week, as the Treasury is signaling for $64 Billion of net new issuance on 6/1 so we will probably have to sit through another month of this "negotiation."

-

Yeah I don't usually pay much attention to global macro either, but I don't hold any cash and I am super bearish and fully invested at the same time. This exact moment is a new high in every account I manage, yet I am adding to shorts in RSP and actually buying TLT. But I'm not going to sell the 5 stocks I own in size just because I am super bearish.

-

I'm not of the belief that what the Fed does matters much but I do find it surprising that markets are pricing in an additional 25 basis point hike in Fed Funds in the next meeting or two. Even copper has come down a lot - and there are legitimate supply shortages there. Commodities are telling you demand is weak. Shipping prices are telling you demand is weak. Oil prices will probably hold up because of the cartel but even oil prices are pretty weak considering the fundamentals. Demand is weak everywhere. China reopening was a dud. I would anticipate the market pops higher on the debt ceiling resolution and then immediately gets sold.

-

Why is that unusual? The main thing that would make the TYX yield go down would be economic weakness and the main thing that would cause the yield to go up would be economic strength. Just think about it as reflation/bullish vs deflation/bearish.

-

KW / PACW transaction. Fairfax likely benefits https://www.cnbc.com/2023/05/22/pacwest-bancorp-to-sell-real-estate-loans-to-kennedy-wilson-subsidiary.html https://www.sec.gov/ix?doc=/Archives/edgar/data/0001102112/000110465923062856/tm2316420d1_8k.htm

-

Yes that has been my experience with Fidelity as well. I'm sure Ken Griffin gets his cut but we don't see "commissions." I also don't always get a fill on marketable orders.

-

Prem's first name is Vivian

-

attached FFH Q1 23 CC.pdf

-

They finally cleaned up the separate holdings at Gen Re New England Asset Management. They all show up on Berkshire's 13F now. No new AAPL shares have been acquired since the Allegheny purchase.

-

Well I'm not sure it is accurate to say "Atlas was sold 100%." (if anything it was an "add" since they exercised warrants for $78.7 million in cash during the quarter)

-

That's right. They also bought 58,185 shares at 10.85 on June 19th 2022, 1,532,864 shares on May 26th at $10.61. They let Fairfax India have first dibs on repurchasing shares because they can do it under an automatic plan (x% of average daily volume plus "take blocks"). As an insider with nonpublic information, Fairfax is not able to buy FIH shares any time it wishes. Plus there is a low public float as it is (OMERS owns a block - something like 20m shares). Lots of purchases by Ben Watsa, Brian Bradstreet and other reporting insiders. The biggest buyer is FIH itself under an automatic plan - including a $10.7 million block trade last week. And every time Fairfax buys FIH or FIH buys shares in itself they are giving up fees they would otherwise be earning on those shares.

-

Yeah. They consolidate it so there is a lot of minority interest. Think of it this way, the market value of all of Fairfax India currently is $1.76 Billion, and Fairfax India's market price is way below book value.

-

I don't understand what you are saying here. You think Fairfax India represents 15% of the NAV of Fairfax Financial or Fairfax Financial's total investment portfolio? *edit to point out that Fairfax's ownership in Fairfax India shares is something like $625 million inside a $57 Billion investment portfolio (1%) or a $16 Billion market cap company (3.9%).