beerbaron

-

Posts

1,516 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by beerbaron

-

I have asked the question many times with very few answers... scability does not seem to be a concern for Bitcoin bulls. Maybe that is because trasaction volumes are of no concern because bitcoin if aimed as a store of value, not a transactional vehicle. Not sure but there is no free lunch, if a transaction today costs 20$ in energy someone has to pay for it and that that is the minimal cost not including capex. Similar to stock dilution, bitcoin dilution has a cost. People might not be seeing it because demand exceeds supply but it still is a cost. BeerBaron

-

About 13%, sligthly below my benchmark of 50% SP500 / 50% TSX. Due to Canadian FX gaining grounds on the USD, some years it's a tailwind some it's a headwind... makes no difference in the long run tough. Performance was achieved with about 20% cash. All in all, not a bad year considering the limited time I have to do research. BeerBaron

-

So quick calculation: 591 000 000 Gallons of oil at $2.50/Ga = 1.5 Billions in energy Cost per year Lowball estimate for bitcoin mining: 1 000 000 kWh @ $0.10/h * 24 *365 = $876 000 000 Highball estimate for bitcoin mining 4 000 000 kWh @ $0.10/h * 24 *365 = $3 504 000 000 So here is the billion dollar questions: If today's power consumption for bitcoin mining is the same as a big chunck of the overall gold produced. What is going to be bitcoin mining power consumption next year or 10 years from now? It seems to me that it is just not a scalable solution, energy efficiency gains on the IC side cannot offset an exponential growth, at least not at this stage and not with silicon. If I were in the bitcoin business I would do everything in my power to address this issue... Is there solutions that would not compromise the security aspect or fragment the network? I don't know... but I'd like to hear about it because that is a pressing matter. Can the technological side support the demand? Saying that comparing BC to 1995 internet is not the same at all. In 1995 there were OC-192 communications lines available, a solid history of the silicon process increasing 50% per year, a solid understandind of where the theorical limits were to speed and size (can't go smaller than an atom). Hence, a lot of room to grow the technical side to support the demand. All in all, the internet had technological tailwinds while crypto currencies have technological headwinds. Maybe I'm wrong but I son't see how it would make sense to spend 100B in energy cost in 5 years for now to save on a fraction of that in transactions. IMO SD has a pragmatic view of the whole picture, I would listen to him for anybody thinking to invest. BeerBaron

-

Blockchain is nothing more than a distributed database it has huge potential but lots of hype is around that word now. As a rule of thumb if in a text you can replace blockchain with DB it's likely not a groundbreaking application. Also, blockchain is a lot less efficient than a db in terms of speed and size so you have to bear that in mind. Dont' get me wrong it will change part of the worlds "transactions" but as any new groundbreaking tech, lots of hype, just gotta separate the diamonds from the coal. BeerBaron

-

:( Sight, I added BBD in my watch list 2 weeks ago and wanted to pick my friends brain that follows aeronotics tonight. I was kinda surprise the BBD stock did not meaningfully moved (added volatity but no real change) when the department of commerce imposed those fines... it seemed it was already priced in or people were expecting an agreement. BeerBaron

-

The way you have to see it is not on the cost saving side. Most of the time those softwares allow for much more streamlined operations and it reduces the employee's workload. But what ends up happening is that the new IT platforms can generate so much reports that all of a sudden employees managing POs, supply, etc... end up reading reaports and acting on it. Sometimes the implementation completely fails and it's a big waste of money and efforts. Even worse, sometimes management refuses to revert back to avoid losing face or because it's just impossible. However, a proper IT platform also allows for a much more scallable business, usually companies that failed to properly invest into their IT start losing ground as they add more SKUs, place bigger orders, add suppliers, etc... A quick rule of thumb can be seen as every time you double the employee size you quadruple the information flow. Having a software to support all those complex tasks allows to add people to support the business without being affected by this exponential loss of efficiency (or less of). On a final note, IT investments should be seen as cost of doing business. You always have to invest in it, when it's not new software implementation it is support and upgrades. Most companies rely heavily one knowledge workers, hence knowledge has to be stored, process and acted upton. Regards BeerBaron

-

Wish I could get my hands on this software. BeerBaron

-

Anybody has a good suggestion for a low management fee + synthetic ETF for emerging market? Something like IEMG but synthetic, I'm from Canada and I hate to see witholding taxes eating my dividends. Thanks BeerBaron

-

By laddered do you mean just buying a bit of all the ones posted, or is that a different product? Yeah, I mean something like 800k in 60 days duration, 800K in 120 days duration, etc.. as your 1st bond expire you roll it over to 2 years.

-

Why not laddered short term canadian bonds spread between now and 2 years? BeerBaron

-

So two questions have been troubling my mind over crypto currencies and I'm lik e non fanatic opinions on each of those. The ledger or full blockchain size. I don`t see how it would be feasible to have an exponentially growing ledger at the rate that would make bitcoin widely adopted. I can foresee the size growing at a rate much faster than any hd of SSD capacity. Las time I checked HDD were doubling every 3 years but I'm fairly certain that a a full transaction ledger would grow much faster than that. It has two problems against it, 1st as the growing user base grows it also grows the amount of transactions. So in a sense we might not be working on a much more aggresive power than HHD drive capacity. ID be happy to see anybody prove me wrong on this one but I do think there is one fundamental law, the size of the ledger cango to infinity, the size of a hard drive cannot. The power efficiency I really don't see how on a massive scale where every civilized human being would use a bit currency what kind of power would be necessary to maintain the hash at an acceptable rate. Already we are seeing stress in the video cards supply I don't see how a planet wide adoption would be even possible under a decentralized approach... did anybody did the calculations of how much eneergy would be needed to compute the blockchain in let's say 15 year from now? I would bet that those calculations would show a ridiculous amount of energy, and if the calculations would be applied to 50 years it would be a multiple of all of today's power plant. I did not dig very deep but my gut tells me that we are looking at a exponential power that is greater than our capacity to out innovate. Blockchain has a place in our future but probable not as widely adopted as we think. What do you guys think care to help me gather the data and see if the numbers makes sence in a long term approach? BeerBaron

-

Hi Parsad, how do you monetize this service? Beerbaron

-

Hi, our company is considering switching law firms in a cost reduction effort. The majority of the work we need from a law firm is related with IP. I was wondering if anybody else on the board has experience switching law firms? Any recommendations? How did you proceed with negotiating a better rate? For example, were you able to negotiate better hourly rates? Thanks BeerBaron

-

My take on this is I'll believe it when I see it. It's part of a large group of ideas that are technically feasible but also technically very difficult. I think Musk was smoking weed when he he stated the costs of such a system. No way it can be cheaper than other high speed alternatives. The kid in me says "WAY COOL", then engineer in me says "GOOD LUCK". BeerBaron

-

Yeah the clickbait is him referencing at the advertising techniques he talks about. BeerBaron

-

I have been thinking about it and Donald Trump "Alternate Fact" theory fit perfectly well with Daffy Duck's alternate reality... I cracked the code guys, the US elected a cartoon character. https://www.youtube.com/watch?v=tqcMxy7BbP4 Note I might be watching too much kid's shows lately. BeerBaron

-

Thank you Sanjeev, and a belated happy New Year!

beerbaron replied to John Hjorth's topic in General Discussion

+1 Hope you get success in all your current and future projects. BeerBaron -

Even better. Do start your own Reit. Market will price it 20x cash flow at minimum

-

Costco might be considered as generating float as the payment terms of distributors is 30 days after the goods are received in the stores. Goods are almost always sold in less than 30 days. Amazon, is also know for having negative working capital. Testing labs (ETL, UL) also have very good economics with 70% payment before the work is done and 30% once completed. Some would say that float is a wonderfull thing because it give free credit but I think it's the other way around. Free credit is only worth what the interest rate (1-2% these days for corporate bond yield). Nothing to go crazy about. Instead I believe that usually companies with float have a pricing power over their suppliers and customers that allows them to have favorable payment terms. Regards BeerBaron

-

Reduction in Equity Hedges to 50%

beerbaron replied to valueinvesting101's topic in Fairfax Financial

Welcome back Gio. -

What's happening with the China Currency

beerbaron replied to beerbaron's topic in General Discussion

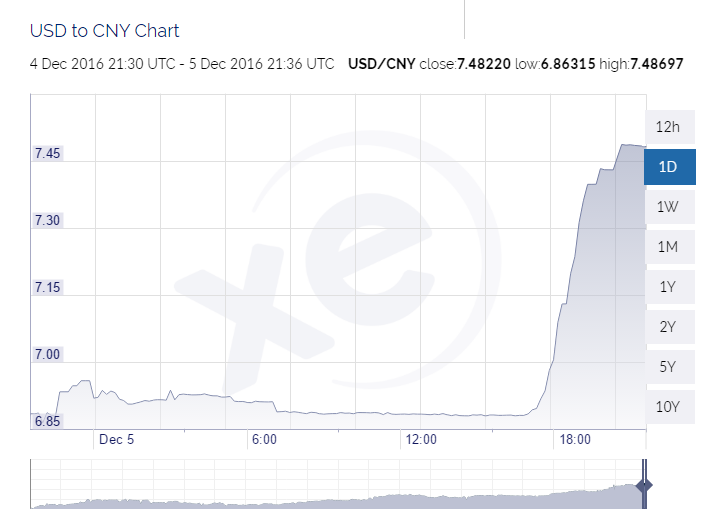

Thanks for the double checking. It goes to say that free data is not 100% right :) If I were the Chinese I would actually do something like that. Let the currency fall for an hour or two and bring it back to the initial level. Would be a nice little warning shot for president elect. BeerBaron -

Anybody knows what happened with Chinese's currency exchange? Is it a response to Trump saying he's raise duties? BeerBaron

-

Brookfield Asset Management / Infrastructure Privatization

beerbaron replied to EricSchleien's topic in General Discussion

Couple of question here. Why would Brookfield earn outsize returns if infrastructure is privatized& Don't you think that when the government puts a project for bid that other player's like retirement funds, private asset managers, engineering firms, will not bid till the return are merely meeting the return on capital? Why would Brookfield get better returns on infrastructure than others? Do you think their current portfolio is worth multiples of what it is currently valued at? Why would it be a multiple of what it is today? BeerBaron -

Buffett interview on CNN Money 11 Nov 2016

beerbaron replied to kiwing100's topic in Berkshire Hathaway

I have rarely seen Buffett seem so uncomfortable talking about the first two subjects. It clearly showed that he was weighting it's words big time to keep it's habit of praising individuals and blaming groups alive. I guess he was not happy about doing it tough, especially the part about WFC's reputation. BeerBaron -

Sometimes it amazes me how Trump can lack proper judgment for lack of better words. Of all the Hilary supporter he had to name the only one that 2 years ago was showing it's tax return on air to make a point...what were the odds of Buffett showing them again... like 100%! BeerBaron