MMM20

-

Posts

3,339 -

Joined

-

Last visited

-

Days Won

14

Content Type

Profiles

Forums

Events

Everything posted by MMM20

-

Yeah my bad, I shouldn't have called you out for that... edited.

-

I gotta take a victory lap here. Almost ~5x on my biggest position since Jan '21 which has made up for a lot of dumb mistakes. It's now trading around what I'd previously considered a fair P/B if we're talking about a ~15% normalized ROE through cycles, but that's an extremely simplistic heuristic that misses the key changes under the hood over the past few years. Nowadays I still think it's too cheap by half, but I might cut it in half anyway. And now that I've posted this, I'm sure the next 50% drawdown is right around the corner.

-

“I don’t remember a month or a quarter gone by where Greg didn’t have a question or a clarity or a thought,” said NetJets CEO Adam Johnson. “And I have to remind myself that he’s doing that 60 times [across all of Berkshire’s subsidiaries].” https://omaha.com/news/local/business/article_5a02fb17-e783-4060-8e8e-d270cd70e019.html

-

This is the path to rerating nirvana.

-

Right, so I'm starting from the assumption that he won't touch certain things while WEB is still around. Maybe I'm wrong about that.

-

Has anyone taken a stab at quantifying the potential boost to earnings from Abel taking over and getting more hands on?

-

BRK is trading around intrinsic value and 2 standard deviations above two decade average P/E and P/B. I'm increasingly wondering if BRK is the proverbial 14-year-old thoroughbred still trading like she's in her prime. I'm tempted to sell to a token position, fully aware that would've been a horrible mistake for BRK's entire history.

-

Totally agree. If you're effectively outsourcing some / all of your portfolio, I think it's become underrated to invert - to seek out another investor who shares your north star / framework (let's say a long-term value-oriented approach) but whose expression is very different, who owns things you wouldn't own yourself. Maybe it's hard for many b/c you gotta put your ego aside to some degree. That's what diversification means to me at least!

-

Haven’t they empowered junior members of the team to make small investments like that? I assume it’s that and don’t read much into it but maybe I’m wrong.

-

You dispute that some investors don’t own Fairfax because it’s outside their circle of competence?

-

^this

-

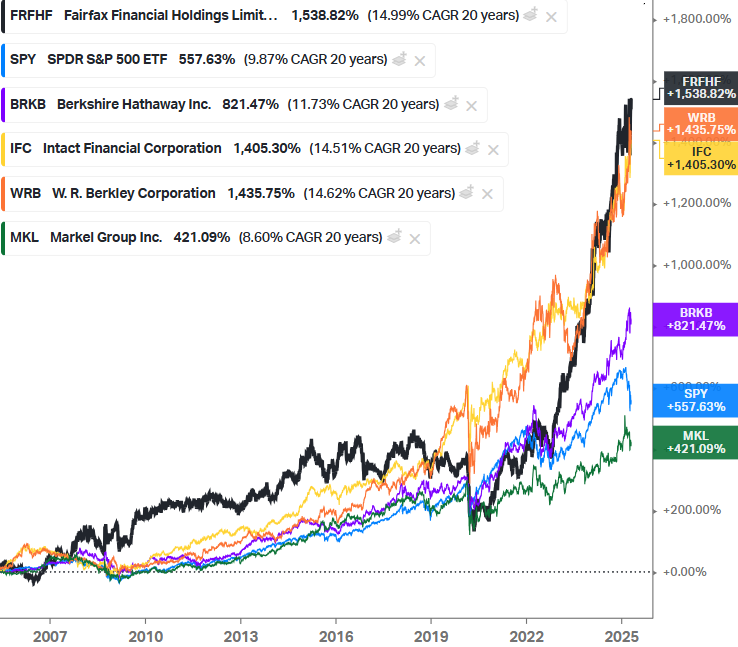

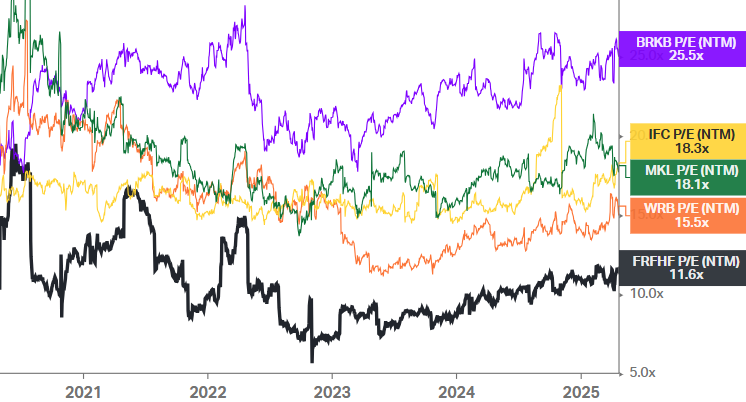

Top performer for the past 20 years. And still the statistically cheapest of the bunch.

-

That’s obviously a quintuple lindy upward-facing dog constellation situation formation. Extremely bullish.

-

I'm sure 9/10 investors wouldn't guess Fairfax is top 10. Still misunderstood, underrated and undervalued.

-

Any chance you can share the first page?

-

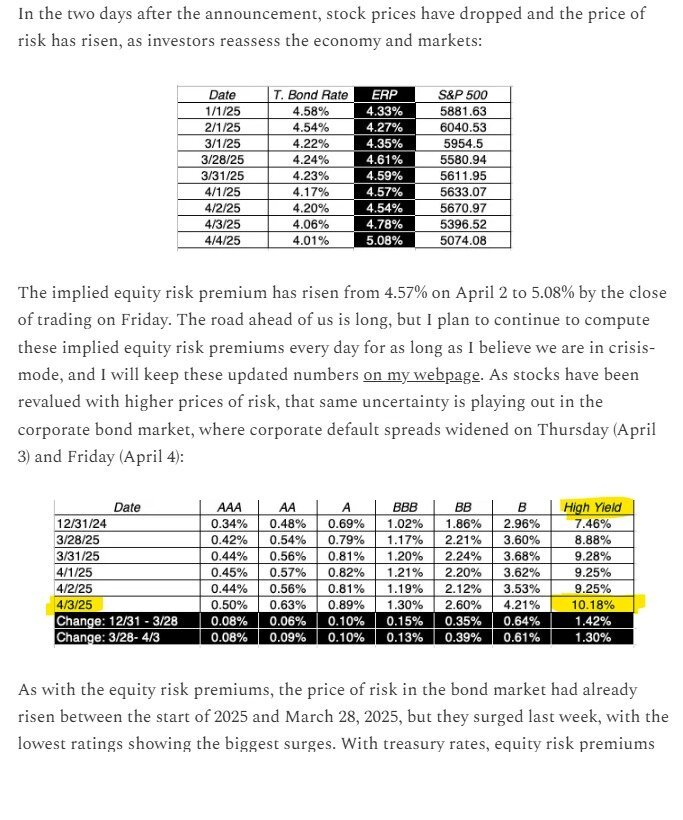

Maybe this is not the right place for this, but high yield has widened out ~272bps since year-end to ~10%+ spreads (with ~3-4 year weighted average duration) per Damodaran. I think that's starting to look attractive and I'm tempted to dip a toe in. That's got me wondering if Fairfax is getting more active on the credit side or staying patient for a fat pitch in high quality credit. I'm guessing the latter but curious about the board's take on it. https://aswathdamodaran.substack.com/p/anatomy-of-a-crisis-tariffs-markets

-

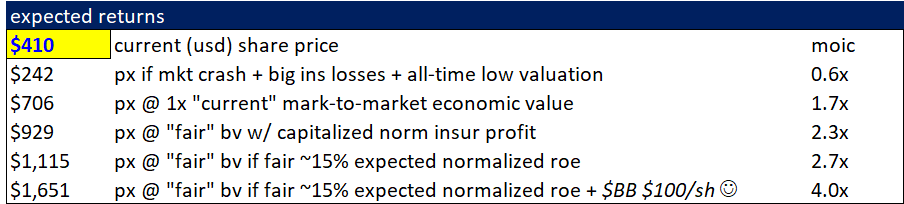

I'm thinking more about the big picture for FFH these days at what I believe is another new all-time high (at least in USD... and what a ballast). How are folks here thinking about valuation on normalized earnings? Let's assume normalized combined through cycles is closer to 100% than 94%, let's say ~99%. Is that still a reasonable assumption for a high-quality insurance operation through long-term cycles? I guess that assumes nothing has fundamentally/structurally changed about the business, eg fewer new entrants responding to strong prices b/c of higher regulatory burdens or something along those lines. Plugging in reasonable expectations for equity and bond returns from these starting points for valuations, that would put Fairfax at ~14-15x normalized lookthrough P/E, which pencils to ~10-12% per share long term compounding from this point. Agree/disagree?

-

-

The "plummeting" thing gets me. We get a 10% S&P 500 drawdown about once a year and a 20% drawdown once every few years. Fairfax trades where it did about a month and a half ago! I guess I'm just barely old enough to remember -50% in the GFC and maybe that's a blessing and a curse - sort of a light version of a Depression baby. I think Fairfax is worth ~US$2500-3000+ so I don't really understand trading around a drop from ~US$1500 to ~US$1350. Not much has changed. I was maxed out size-wise at ~US$1500 and I'm still maxed out now.

-

So now on pace for almost 10% total annual shareholder yield? Am I missing something?

-

Right, so maybe more like +7-15% to FFH BVPS unless I’m missing something about minority interest? Thanks!

-

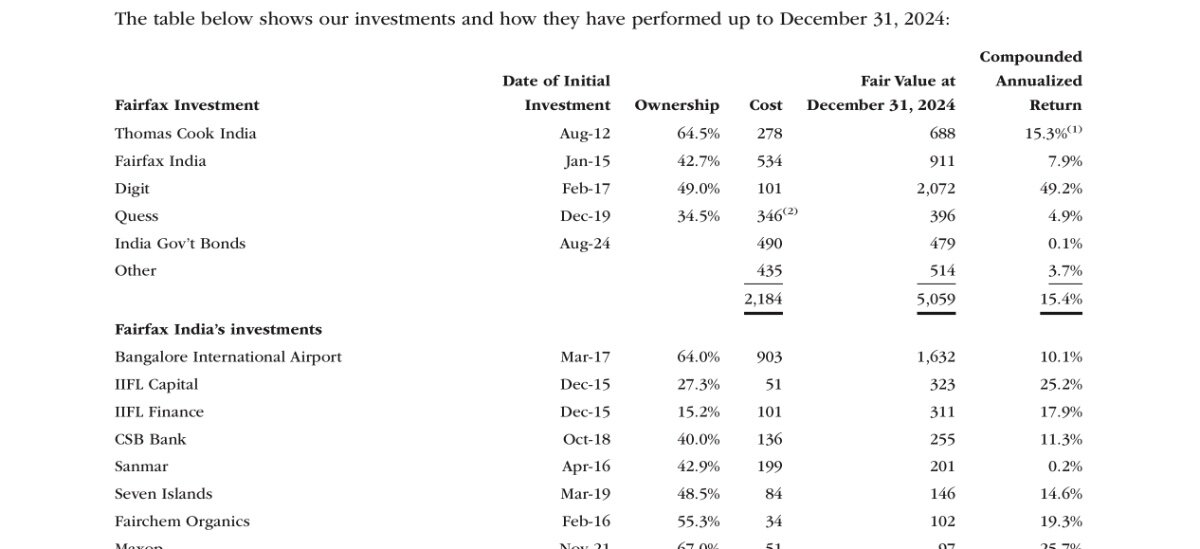

If the Bangalore airport fair value is really understated by ~2-3x, would FFH’s book value upon the airport IPO be up +10-20% from that alone? Is that roughly right?

-

The right answer is probably “noise” / unwinding of index add speculation, but I did see that Andy Barnard sold almost C$5mm of stock last week. Of course, that’s only ~5% for him and insiders sell for many reasons.

-

It’s clearly a well managed bank but the catch is it’s Egypt where inflation is ~25%. They say “unfortunately” the depreciation of the currency has taken returns from 21% in local FX to 1% in dollars, but that’s exactly what we should expect - we gotta adjust nominal returns expectations for the local FX depreciation given 20%+ inflation differentials. Not monopoly money but close! That doesn’t mean it can’t be a good investment.

-

It's a sizing question more than a binary one.