MMM20

-

Posts

1,870 -

Joined

-

Last visited

-

Days Won

10

Content Type

Profiles

Forums

Events

Everything posted by MMM20

-

I understand the logic but I’m 1) really not a fan of management selling shares to the company and 2) still hugely overweight FFH - and so I’m taking this as a cue to sell a chunk of my own shares too over the next couple months.

-

Let's say Country X's currency trades 1 for 1 with Country Y's. If Country X's inflation over the next 20 years is ~5-6%, then in the end that 1 unit = 3. If Country Y's inflation is 0, then 20 years later that 1 unit still = 1. So all else equal, the fair exchange rate would change from 1:1 to 3:1 over that time period. I guess I would expect evidence to be mixed b/c in the real world, nothing is held constant. But maybe it's more useful as a starting point than ignoring the issue or a finger in the wind or w/e.

-

Do we have a ticker!?

-

I'm confused by the question b/c, at least as far as I understand it, it's just arithmetic - obviously absent some regime change or long-term distortion in supply/demand factors. And Japan is typically the exception that proves all sorts of rules so I'm not sure I'd look there for evidence of anything other than the power of a cohesive society (and the psychological impact of a stock market derating from like 100x to 5x p/e over a few decades).

-

Over long periods of time like that, the fx movements track inflation differentials. If the US actually ends up in a higher inflation regime and India an economic boom with moderate inflation, maybe the INR vs USD will look very different over the next 10-15 years. Maybe we end up both with the higher growth and a currency benefit - or at least not such a big headwind. Seems like a reasonable possibility at least, right? Anyway, can’t wait to see what Digit and BIAL look like in 2030-35…

-

My takeaway was there was little remarkable about the quarter and that's a good thing.

-

Great work @SafetyinNumbers and thanks for sharing @gfp. We like the stock

-

Any chance you can post a PDF?

-

that pretty much covers it...

-

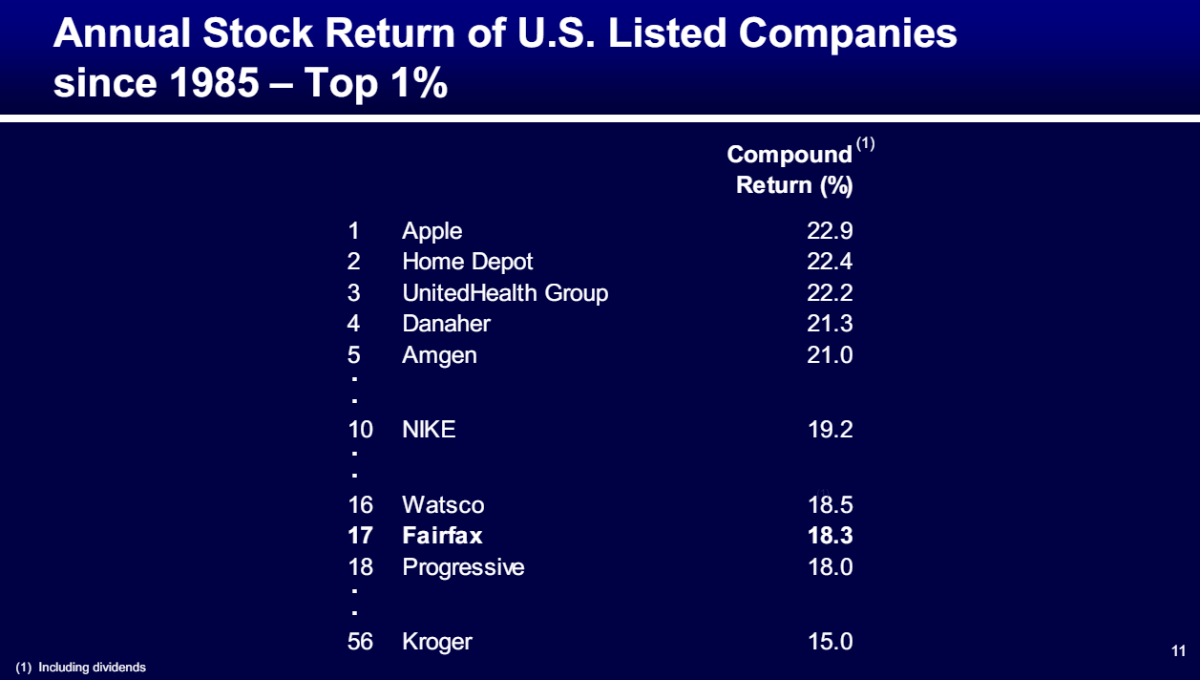

I hear you. Either way it makes no sense that FFH still trades where it does, even if some people hate the portfolio and think it's a weird agglomeration of bad businesses and venture type bets.

-

I wasn’t referring to you - I know you can change your mind. Other people I talk to IRL continue to push back similarly, though, harping on Blackberry and other cherry-picked bad outcomes, despite what is now a satisfactory result over any long term period. They tend to be more GARP/ quality growth investors who don’t really like or get old school value and seem to expect a reversion to ZIRP and 2010s environment in which they built their careers. I guess we’ll see about that. My own view is that this is a quality growth stock but driven by an old school value investor, so for many it just does not compute. Still, if FFH had outperformed consistently in the broadly defined equity portfolio over the past ~15 years, there would be no debating that this is a quality compounder and it would trade at ~3x book today. And do you include pet insurance? Do you include digit? Do you include the other insurance acquisitions? Would those not be considered “equity investments” inside of any conglomerate? I think the whole bifurcation is the wrong way to look at it. So much comes down to how you frame the analysis. Anyway, they seem set up to outperform peers for years and still we’re still at 7x p/e and 1.1x book.

-

Some people believe that Fairfax has performed poorly on the investment side and won’t be convinced otherwise by any amount of data or examples.

-

The test of a first-rate intelligence is the ability to hold two opposed ideas in the mind at the same time and still retain the ability to function. 1) Fairfax management has executed and upgraded the quality of the business - yet the stock still trades around 1.1x book and 7x p/e and even after a monster run still seems like an absolute and relative bargain. 2) Interest rates normalizing off all-time lows was a huge tailwind and made them look even better - if that hadn't happened (yet), it might still trade at $500.

-

Not sure exactly, but FFH has now compounded at ~15% post-GFC when they supposedly lost their fastball. Hey, maybe the unprecedented interest rate environment had something to do with it after all.

-

Incredible. And nowadays no one can hand wave it away as driven by the early years.

-

What do we make of the argument that, like a bodybuilder on steroids who ends up popping a bicep tendon, such rapid growth might inherently introduce fragility into their operations? Is it too much too fast for a staid insurance biz? Is Fairfax more susceptible to a black swan event than they were five years ago?

-

Very good news IMHO. Wish BRK would do the same.

-

Makes sense purely on inflation differentials if you're a long-term investor thinking/reporting in USD.

-

https://east72.com.au/wp-content/uploads/2024/04/E72DT-Quarterly-Report-March-2024.pdf

-

?

-

https://www.valueinvestorsclub.com/idea/FAIRFAX_FINANCIAL_HOLDINGS/8951778558 Fairfax write-up on VIC from Feb 14th. Sorry if this has already been posted. "MW never discusses the earnings power of the business. Why? Because it makes a mockery out of the short thesis. In my opinion, the company, helped by higher interest rates and a hard insurance market, will be able to generate north of $200 per share in EPS per annum for at least the next three to five years. "Muddy Waters never states what the company is worth and why. It ignores all disconfirming evidence and ignores the elephant in the room – the earnings power of the business. When a company is trading at five times net income, MW must expect earnings to collapse, and if they don’t how will the short work?"

-

Zoom out… and BTW the stock was up this month.

-

Why does higher volume imply shorts adding?

-

@dartmonkey I believe it was addressed by those who rightly pointed out that leaving some money on the table in any particular transaction is not inconsistent with the fiduciary duty to shareholders.

-

It would be cool if a Canadian insurance company still trading at mid-high single digits P/E ends up being the best way to invest in the Indian growth story over the next decade (ironically maybe even better than Fairfax India)