MMM20

-

Posts

1,877 -

Joined

-

Last visited

-

Days Won

10

Content Type

Profiles

Forums

Events

Everything posted by MMM20

-

I'm trying to understand. Is the implication that the recent rally might be mostly due to some technical supply/demand imbalance around the TRS / ex-dividend date? Could someone please explain for the slowest among us? Maybe I'm wrong but it seems like the stock almost always seems to rally in January, at least for the last 5-6 years... so is this all just amplifying typical "seasonality" in what is a relatively less liquid stock?

-

Agreed…

-

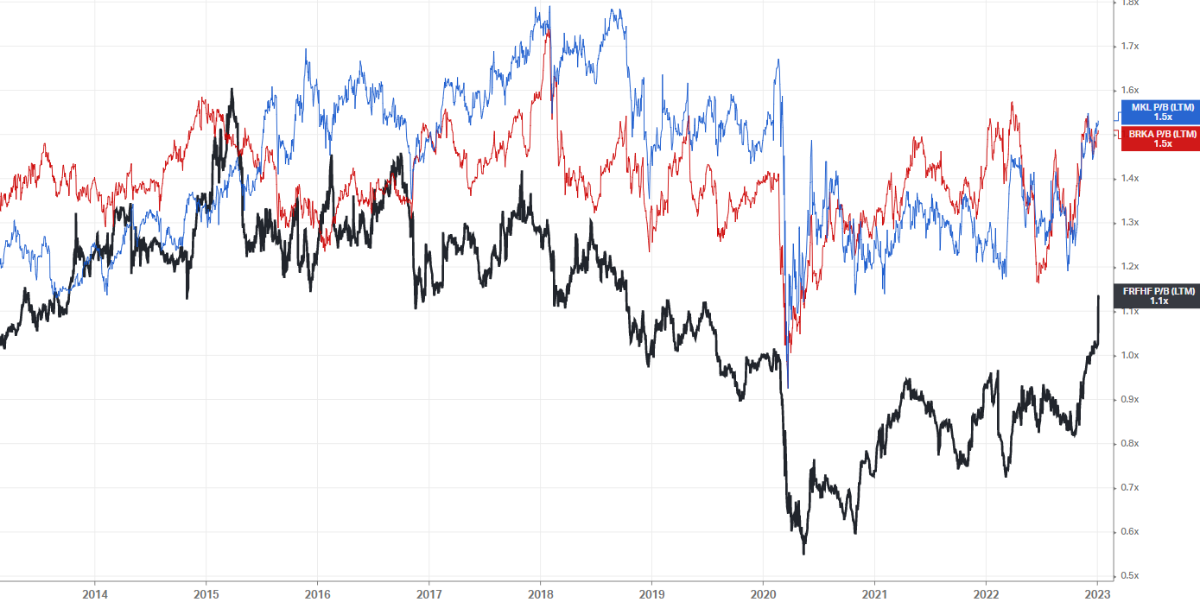

Price/Book vs. BRK / MKL... don't mind me...

-

@steph Blackberry is a tiny sliver of enterprise value at this point so wouldn't it be surprising if that makes much of a dent in fundamentals and/or sentiment with all the other positives nowadays?

-

Not to derail the convo here - i get your point but don’t think it’s quite the right comparison. We aren’t talking peak cyclical earnings in the same sense as a commodity producer, right? This won’t be like a US shale biz that makes 50% margins at $100 oil and then hands the keys to the bank at $40 oil. We are talking about insurance prices up 20%+ for consecutive years before leveling off at some point, right? Would you expect their underwriting to flip to extremely unprofitable in a soft market? Seems like the real earnings power should still be there. The investment portfolio is looking like a cash machine esp if they end up moving fixed income out in duration ahead of a flattish to down rate environment over the next few years. I guess my point is the huge growth of float and the investment portfolio has created what looks like a big permanent boost in per share earnings power, so I think a higher multiple makes sense (even if insurance price increases over the next 5 years probably won’t look like the past couple) b/c Fairfax has many high incremental return uses for $100/share in sustainable annual earnings - they're not committed to investing back into the insurance business at lower incremental returns. I mean, how much could they buy back if they prioritized it for the next few years and the stock theoretically stayed at 6x earnings along the way? Like half the company at a 20%+ cost of (return on) equity? IMHO the low multiple is more about Fairfax still being in the penalty box for past indiscretions and the correction / redemption arc naturally happening in slow motion over years as these things go. Maybe I’m wrong. Fairfax has luckily been a big position and winner for me for the past couple years, offsetting more than a few clunkers…but I’ve been recently inclined to add to it if anything.

-

Amazing that FFH's NTM p/e is right around ~10 years lows given the performance of the past couple years. Maybe it's just confirmation bias as this imperfect metric squares with my view that the stock has gotten much cheaper relative to the growth in sustainable earnings power even as the stock price has nearly ~2.5x'd from pandemic lows. What a ballast for portfolios since the pandemic. It looks like they're set up better than ever to go from strength to strength... here's to a fairer low-teens multiple / $1,000+ stock in '23. Knock hard on wood.

-

Trading at about half that multiple on an economic basis. The accounting doesnt educate but rather obfuscates when it comes to FFH. This has been the opportunity for at least a couple years now. Stock is trading cheaper to intrinsic value now than at $360 2 years ago.

-

What’s the deal with the BB bond position? Is that actually new or just the convert showing up? Thx.

-

I keep saying the same about Fairfax.

-

Prem is looking better and better with his long time skepticism of Chinese capital markets. India is looking a prime beneficiary. Maybe Fairfax can take advantage with the Digit IPO.

-

Much more than that, it's about re/descheduling at the federal level and the likely downstream effects. This is about as much as Biden could do. I have seen credible typically skeptical DC sources saying this is the biggest news for cannabis since the Cole memo. Who will now stand in the way of a CA/NJ interstate cannabis trade agreement, which has long been in the works? Or other states that opt into the same? Will the MSOs be the ones to fight against freedom in cannabis markets? More likely they'll become Glass House customers. IMHO, GLASF should be up 3-5x on this news.

-

Props. I did something similar for just a couple weeks into the dutch auction last year and didnt sleep much. Similar age to you at the time too. Lots to learn from the OGs. Coming at this one humbly but seems the situation is similar now. Do you disagree?

-

How big could you make something like that as a % of net worth, or however you think about it?

-

More interesting to make 3-5x (IMHO) on a massive low impairment risk position anyway.

-

+1 4-5x forward normalized operating income starting point for valuation + ongoing hard market as competitors retrench from bond portfolio losses + extending massive cash/bond portfolio duration + monetizing "hidden" assets like recent pet insurance sale + anything good on the public stock portfolio, which is small vs the total pie and overanalyzed + any bonus from Digit IPO etc + massive negative cost float-based leverage + demonstrated willingness to buy back big slugs of stock below intrinsic value + potential for +50% (or *any*) multiple expansion after a long enough stretch of good execution = lollapalooza returns for FFH shareholders over the next few years missing anything? considering going uncomfortably big again

-

Not super in the weeds on FFH at the moment - sold most to (try to) upgrade portfolio - but I still own a core position and hope this is an indication that Fairfax is setting up to sell its more cyclical holdings to buy back stock and/or upgrade the equity portfolio, now that valuation dispersions (eg between “junk” and “compounders”) have narrowed somewhat Prem loves to talk about lessons learned from Buffett over the decades. Have they finally learned their lesson to pay a fair price for truly great businesses? With the hard market maybe even accelerating (!), still a short duration fixed income portfolio, etc etc, step back - they’re really in a massive position of strength. This is their opportunity make real moves for shareholders. Goldilocks scenario in many ways! Dont fool yourselves - ATCO is a great savvy operator but in an ultimately extremely cyclical crappy business with low returns on capital and filled with sketchy and irrational actors like state owned employment center shipyards. It was insanely cheap, now it’s not. So let some strategic capitalize the locked in earnings and pay you a big multiple. Punch out. Incredible how fast we went from “Prem owns trash that’ll never go up” to debating whether he’s stealing the trash from shareholders Upgrade the portfolio. ACTUALLY do a Singleton and buy back massive chunks of the company over the next couple years. Walk the talk. That’s how FFH might compound BVPS at double digits AND trade at a deserved premium to BV again. ^Just the strong opinion weakly held of one relative newcomer

-

Could you explain this view a bit further for the generalists (outsider noobs) among us? Why do investment losses lead to an ongoing hard market? I understand that insurers *want* to raise prices to recoup investment losses - who wouldn’t? - but doesn’t their ability to do so depend purely on supply/demand dynamics on the underwriting side, independent of investment performance? Why wont new entrants with clean balance sheets come in lower than incumbents on pricing? Too theoretical? I think it’s an important question given that the gap to IV has closed a bit over 1.5 years and most other stuff has sold off… FFH is still cheap but maybe less of a relative bargain nowadays. But clearly this depends a lot on the duration of the hard market.

-

Agreed, when the yield curve is flat, why go out in duration unless you want the convexity b/c you’re betting on rates falling from here. You are getting way more risk and no extra reward on a YTM basis. I don’t see anything surprising in the release. I’m guessing market will disagree for one reason or another. Maybe the higher interest/dividend income gets capitalized and that gets the stock moving to $600 plus but who knows.

-

The fun part about investing is you can't really judge the decision from the outcome, especially between two arbitrary specific points in time. Maybe the process was sound and the odds were in their favor to hold at the time. This is not a Fairfax issue, this is an every-investment-always issue. Anyway, here's hoping they punch out and launch a $2B SIB @ $600 USD Share count remains on its way to 10M

-

I looked at JAB in the past. Some ethics questions came up. I like that Fairfax continues to add long term partnerships with great external capital allocators. I just wonder if JAB is the right pick. https://neckar.substack.com/p/jab-and-the-family-office-conundrum A brief history of JAB and the Reimann family The story begins in 1823 in Pforzheim, a town at the edge of Southern Germany’s Black Forest (about an hour from where I grew up.) Local businessman Johann Adam Benckinser (initials “JAB”) acquired a chemical lab from its bankrupt owners and hired a promising young chemist named Karl Ludwig Reimann from the Universität Heidelberg (where Reimann had been the first to extract nicotine from tobacco). Reimann married one of Benckinser’s daughters and took over the company after Benckinser’s death. The company expanded to a new plant in Ludwigshafen (today seat of Germany’s largest chemical company, BASF) and grew steadily. The family’s darkest chapter occurred when Albert Reimann Sr. and his son Albert Reimann Jr. became enthusiastic supporters of the Nazi regime. In 1937, Reimann Jr. wrote to Heinrich Himmler: “We are a purely Aryan family business that is over 100 years old. The owners are unconditional followers of the race theory.” The company as well as the family’s estate employed forced laborers who were subjected to abuse. After the war, the Reimann patriarchs denied their affiliation with the regime and the full story was not uncovered until a few years ago when JAB commissioned a historian (all of this was detailed in the New York Times). In a wild twist, the historian uncovered Reimann Jr.’s affair with a young employee, Emilie Landecker, whose father Alfred had been Jewish. Emilie’s mother was Catholic and, anticipating the danger, Alfred ensured that his children were baptized. While his children survived the war, he was deported and murdered in 1942. It seems the relationship between Reimann Jr. and Landecker continued after the war and resulted in three children. Reimann Jr., who had no children with his wife, eventually “adopted” those three children as well as six others. When he died, each inherited 11.1% of the Benckinser company (orange box on the below chart). Reimann Jr. also neglected to tell any of them that he owned the company. They believed he was merely an executive. His will also forbid them from selling to anyone outside the family. Thus they found themselves unprepared to lead the company which, despite a successful expansion into consumer products such as detergents, reportedly lacked scale and competitiveness. The heirs needed a leader and found one in a German Harvard MBA and former BCG consultant named Peter Harf. Harf radically restructured the company. He further expanded into consumer products, looking for markets with “non-cyclical growth and strong brands but without a clear market leader.” In those industries, the consolidators would win “almost automatically” through synergies and greater scale. He acquired some 25 companies, including the Coty cosmetics business from Pfizer. Then he split up the company, took the detergents business public, and merged it with the British Reckitt & Colman into Reckitt Benckinser. After starting with a mid-size private chemicals business, the family now had stakes in two public companies: Reckitt Benckinser and Coty. Along the way, five of the heirs were paid out. Harf also joined the board of directors (and later became chairman) of Interbrew, which subsequently merged with the 3G-controlled Brazilian AmBev to form Inbev, the world’s largest beer company. Harf witnessed firsthand 3G’s playbook of industry consolidation and cost-cutting. Around 2010, he was ready for a new chapter. He pitched the family on using JAB as a 3G-like platform for private equity-style deals. He brought on two additional executives, Reckitt-Benckinser’s Dutch CEO Bart Becht and the French Olivier Goudet from Mars. To align their interests with the family, the three would invest their own capital into JAB as well as receive options. Today, the family owns 90% of JAB and its executives the remaining 10%. Harf struck another deal with the family: they would refrain from making public comments and even, according to one source, take an oath of secrecy. In exchange, he would compound their capital and protect their privacy by being JAB’s public face. In his investments Harf was looking for consumer brands with steady growth, robust cash flows to support leverage, and in industries ripe for consolidation. Beer and chocolate had produced a small number of global players. "Coffee,” however, “only had Nestlé, the industry was fragmented." And it offered a growth tailwind because Millennials were "the best coffee drinkers ever.” This started an acquisition spree up and down the “coffee and breakfast” value chain: from Keurig pods to coffee roasters and chains serving sandwiches and donuts. JAB’s focus was on maximizing cash flows to support debt and enable further acquisitions. For example, they extended payment terms to their coffee suppliers to up to 300 days, three times as long as Nestle. Only some of the companies seemed to fit the theme of market consolidation and were re-assembled into larger entities. The above timeline also omits that JAB tried its hand at luxury goods with Jimmy Choo and Bally. Today, many of its portfolio companies are public again: Keurig is now Keurig Dr. Pepper Snapple, JDE (Jacobs Douwe Egberts) consists of the former Peet’s, D.E Master Blenders, and Mondelez's coffee business. Krispy Kreme is public and Panera is going public via SPAC. Harf made a comment that left no doubt about his perception of himself and JAB: So what did I miss? First, German outlet Manager Magazin highlighted that JAB’s executives now derive substantial additional compensation through the private equity business for which they’ve raised some $17 billion from investors like the Peugeot and Santo Domingo families, Byron Trott, and Singapore’s GIC. The magazine reported that JAB had hired executives from Mars for an expansion into petcare, which would be majority-owned by the private equity funds. It seems that one of the hires downloaded confidential documents before leaving which resulted in a lawsuit between Mars and JAB. Thus, a conflict of interest became apparent in which JAB’s capital and reputation could be at risk for a venture that benefits the management team and outside investors. Harf also seemed to have entrenched himself personally at every level of JAB’s subsidiaries. JAB hired a designated successor, David Kamenetzky, who was supposed to restructure and simplify the web of companies and implement more formal oversight. The new structure was supposed to be “modeled after public companies,” which I interpret as a kind of formal board of directors. Harf’s position at JAB had been built on trust and a long-standing relationship with the family. And, I would argue, it was entrenched by pursuing JAB’s hands-on and increasingly complex investment strategy. Reportedly, Harf didn’t want to retire as originally planned. Perhaps understandable given the ongoing turnaround at Coty. It also echoes the careers of many other investors whose passion keeps them in the business Under the new structure, Kamenetzky would have had power over Harf’s contract. And yet Harf had the right to fire Kamenetzky. And that is exactly what he did. In the end, it seems like the magazine’s scathing articles may have had an effect. The family recently appointed a new vice chairman and designated successor to Harf.

-

Thanks for the update. With the ongoing hard market, good-enough investment performance, and still conservative fixed income side, the stock seems cheaper now than at $360 1.5 years ago - I just wonder when we'll see them play more offense. Will they add a whole lot more capital to the mortgage side given that rates have essentially doubled? Also just hope they don't cut the flowers to water the weeds with respect to the potential digit ipo and other things.

-

Maybe they never will and Fairfax will just sell down from “74%” to the reported/speculated (?) ~30% in the IPO

-

This is why it’s crucial to have an economic model vs an accounting model. That distinction is key IMHO and what the market misses. The earnings power is obfuscated by the crazy accounting treatment of these companies which Buffett has written about at length. Prem doesn’t do himself any favors with the way he lays it out in the reports but it’s getting better at least.

-

+1. if/when to sell when things start going right and the valuation reverts to fair value (to be clear I agree we are far from fair value in this case) remains an underrated difficult part of the whole game. Buffett’s approach looks wiser and wiser the older I get. insist on a significant safety margin on the buy but then let things run. Benign neglect, as long as you can sleep well at night. I’ve said a few times here that FFH IV is IMHO closer to $1,500/share than most believe. Do the math on the holdings and capitalize your estimate of normalized underwriting profit on the recently-exploding float level. And then factor in what they’ve said and done on the share count as they flip to highly cash generative. Maybe I am truly the biggest FFH fanboy around.

-

“it has also entered into forward contracts to sell long dated U.S. treasury bonds (notional value $1.7 billion Dec 31, up from $300 million Dec 31, 2020” I’d missed this before. Thanks for sharing. So instead of shorting stocks they are shorting long term treasuries. I like that risk/reward much better but we prob gotta stop saying they “stopped shorting”