sholland

-

Posts

177 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by sholland

-

I think @Spekulatius is right and I am wrong. The human brain consumes ~20W of power. An Nvdia H100 consumes about ~1000W for similar performance. Seems highly likely that chips will be more efficient than the human brain someday. Thanks for the pushback.

-

Thanks Viking! I will read the book immediately.

-

It is my understanding that Berkshire’s insurance operations struggled until Ajit Jain was hired. The Fairfax Way seemed to indicate that Fairfax’s insurance operations struggled until Andy Barnard was put in charge. Do members of this board agree or disagree with my assessment that Andy Barnard is to Fairfax as Ajit Jain is to Berkshire?

-

Datacenters in space are a terrible, horrible, no good idea. TL/DR: huge obstacles in power, thermal regulation, radiation tolerance, and communication. https://taranis.ie/datacenters-in-space-are-a-terrible-horrible-no-good-idea/

-

Disagree with this take. I believe optimization is linear thinking and staying on Ray Kuzweil’s computing power curve is exponential thinking. Superintelligence will give a decisive economic and military advantage. The U.S. will do whatever it takes to stay on the Kurzweilian curve. Image from https://situational-awareness.ai (I just read through this entire thread and surprised no one referenced Leopold Aschenbrenner’s Situational Awareness)

-

You are looking for stocks that went from $200M to $200B or more. So I Googled 1000 baggers and found this.

-

Thanks @petec and @SafetyinNumbers. I found your arguments persuasive. Additionally, I asked Grok the following question: Why is it more favorable for Fairfax Financial to own part of Fairfax India as a listed stock on the Toronto stock exchange as opposed to owning all of Fairfax India as a private Indian company? Specifically, I am interested in the capital treatment ramifications if Fairfax Financial bought all of Fairfax India. To spare follow board members the long winded answer I have summarized Grok’s answer as follows: Fairfax Financial, as an insurance holding company, is subject to Canadian regulatory oversight by the Office of the Superintendent of Financial Institutions (OSFI). Its regulatory capital is defined under the Regulatory Capital (Insurance Holding Companies) Regulations (SOR/2001-424), which includes shareholders’ equity, subordinated debt, and crucially, minority interests (NCI), minus goodwill. The adequacy of this capital is assessed on a consolidated basis, incorporating guidelines like the Minimum Capital Test (MCT) for property and casualty (P&C) insurers, adapted for holding companies. The listed partial-ownership structure is more favorable because it incorporates non-controlling interests (NCI) into regulatory capital, allowing Fairfax Financial to control and consolidate Fairfax India and leverage external capital. Full acquisition and privatization would eliminate this NCI benefit, require significant funding, and likely result in a net reduction in available capital, harming ratios and increasing the need for additional capital reserves under OSFI rules.

-

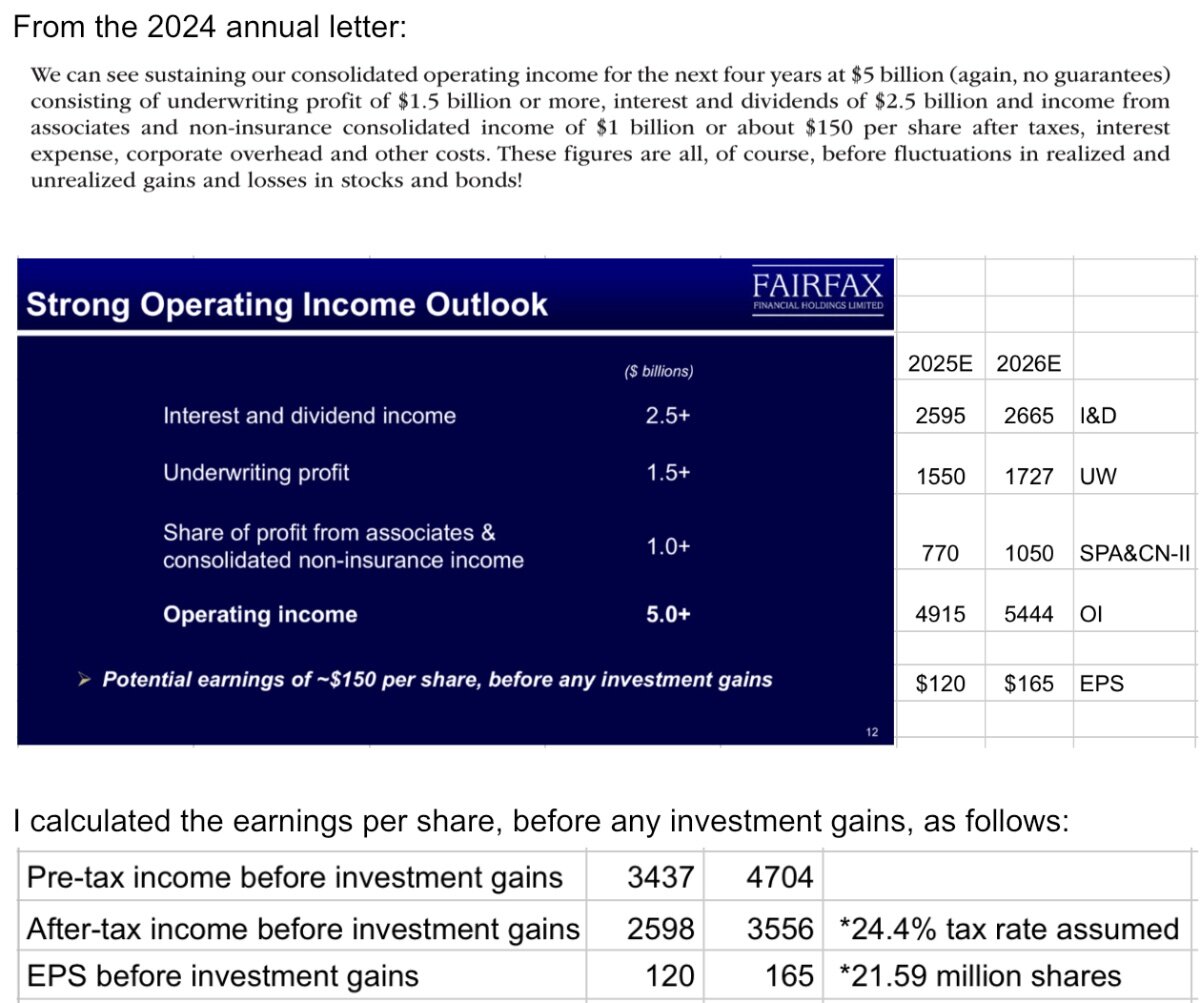

Thanks @Viking for sharing your work. I thought it would be interesting to compare your work against Fairfax’s outlook. (I 2nd @roundball100 ‘s nomination)

-

Quote from a different topic predicting FIH will be bought out like KW, but thought I should follow up here. I would love to own some Fairfax India, but have passed because of the high ownership by Fairfax Financial, and I am worried about a takeunder. Please elaborate why Fairfax Financial wouldn’t take advantage of a market downdraft and execute an takeunder with Fairfax India.

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

sholland replied to twacowfca's topic in General Discussion

https://www.wsj.com/finance/banking/fannie-freddie-ipo-big-banks-6d8884aa?mod=Searchresults&pos=1&page=1 “At least one bank suggested that the government issue shares in the IPOs that get preference over the Treasury Department’s senior preferred shares to mitigate investors’ risk, people familiar with the matter said.“ Not my base case, but I think a share issuance with priority above SPS is feasible and can mark-to-market the SPS. Warrants, common shares, and JPS may be worth zero in such a scenario. It’s enough of a risk for me that I exited after being a shareholder for 11 years. Trump always assumes negotiation dominance. The government currently owns 100% of earnings. I am sure the Wall Street geniuses can find a way to maximize value to U.S taxpayers without sharing any with JPS and common shareholders. I don’t know how this plays out. An inconveniently long time is almost as bad. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

sholland replied to twacowfca's topic in General Discussion

https://www.wsj.com/finance/banking/fannie-freddie-ipo-big-banks-6d8884aa?mod=Searchresults&pos=1&page=1 “At least one bank suggested that the government issue shares in the IPOs that get preference over the Treasury Department’s senior preferred shares to mitigate investors’ risk, people familiar with the matter said.” -

Thanks! Most recent copy just linked per your suggestion.

-

My west coast philosopher friend asked me about my investment thesis in Fairfax. I wrote something up last weekend and it occurred to me that people on this board might possibly be interested. Huge thanks to @Viking and others for their contributions to this board. Much of this writeup is inspired/plagiarized from them. https://docs.google.com/document/d/1cFtEu-cW4kVN21Q4_o3Kk-USHgWUpmVBVGwkafcXTz4/edit?usp=drivesdk

-

Not only is FFH trading @ ~9.5x earnings but those earnings have good visibility for the next four years. In his 2024 annual letter Prem states “We can see sustaining our operating income for the next four years at $5 billion (again no guarantees), consisting of underwriting profit of $1.5 billion or more, interest and dividend income of at least $2.5 billion, and income from associates of $1 billion, or about $150 per share after taxes, interest expense, corporate overhead and other costs.”

-

Thanks for this. For those wanting more detail, the link to the white paper is attached below. https://www.karenclarkandco.com/news/publications/

-

@Viking Yes, I believe consolidated non-insurance income should be part of operating income, and I have updated my image below. @Haryana You may be correct, but Fairfax presents underwriting profit in their financial statements without adjustments for IFRS and run-off/life-insurance. So for purposes of comparing Viking’s estimates to management’s operating income outlook I believe adjustments for IFRS and run-off/life-insurance should not be part of operating income.

-

These are the only two mentions of tariffs in last Fridays conference call.

-

Thanks @Viking for sharing your work. I thought it would be interesting to compare your work against Fairfax’s outlook.

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

sholland replied to twacowfca's topic in General Discussion

https://www.bloomberg.com/news/articles/2025-07-31/trump-asks-bank-ceos-to-pitch-on-fannie-freddie-stock-offerings?taid=688bcfa0aafb050001831daa&utm_campaign=trueanthem&utm_content=business&utm_medium=social&utm_source=twitter&embedded-checkout=true -

From the book The Once and Future Crum & Foster by Marc Adele:

-

What is your thesis on naked puts on CB expiring Nov 2025?

-

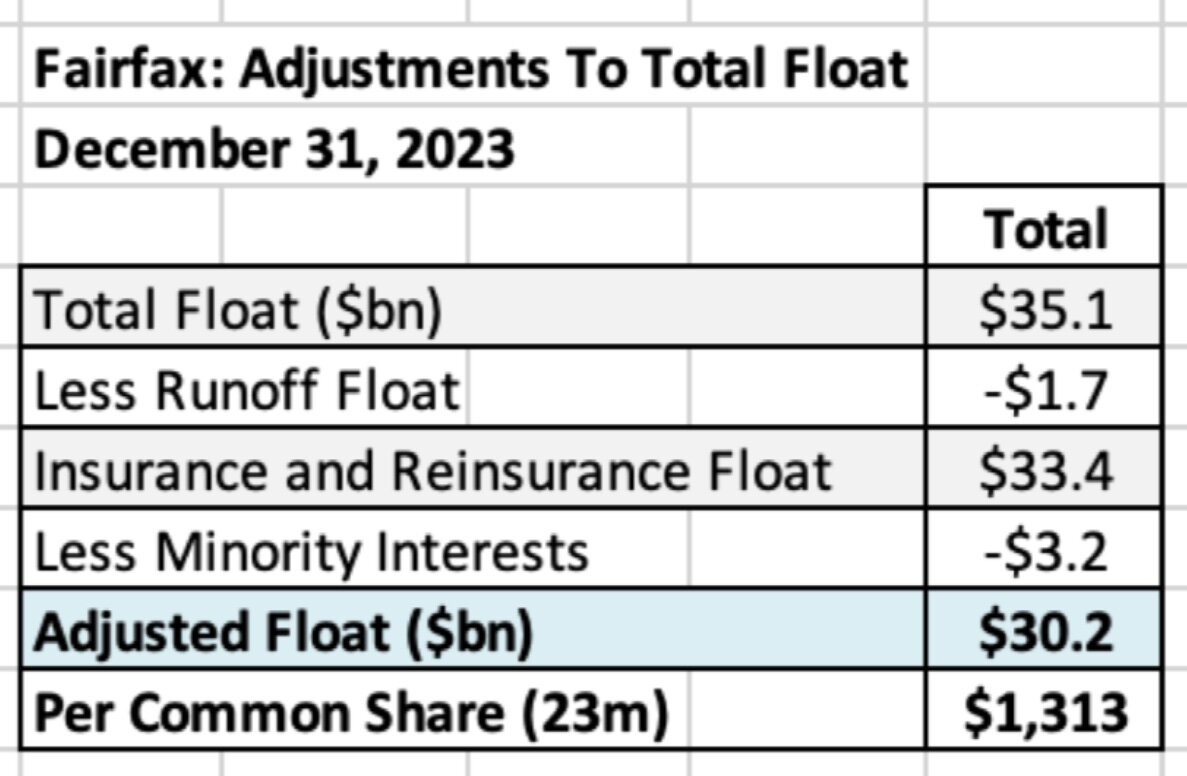

I am trying to recreate Viking’s chart, but for YE2024. Where are the YE2024 minority interests specified? I can’t find it in the annual report.

-

TSE:TAL no position. Do your own due diligence. Have owned in the past.

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

sholland replied to twacowfca's topic in General Discussion

SCOTUS has said that government can do whatever it wants with Fannie and Freddie. I don’t see any reason that the government can’t reinstate the Net Worth Sweep. My investment (speculation) is placing heavy dependence on Trump’s letter in which he indicates that he wouldn’t “…steal the retirement savings from hardworking Americans who had invested in Fannie Mae and Freddie Mac.” -

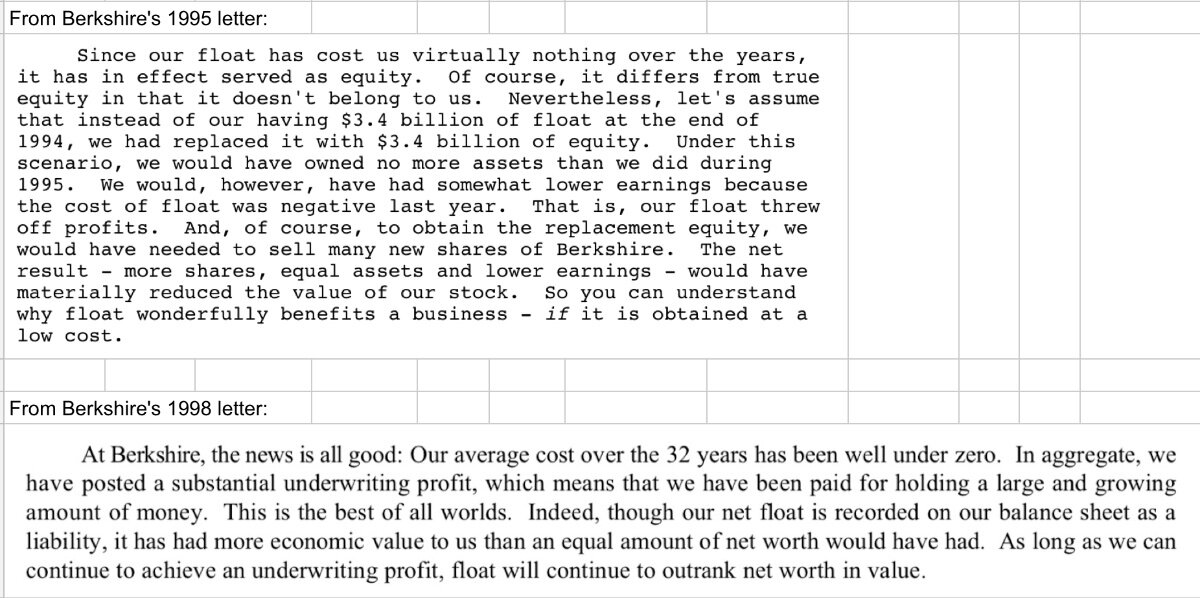

As long as an underwriting profit is achieved, float is more valuable than an equivalent amount of equity (book value)