sholland

-

Posts

178 -

Joined

-

Last visited

1 Follower

sholland's Achievements

")

-

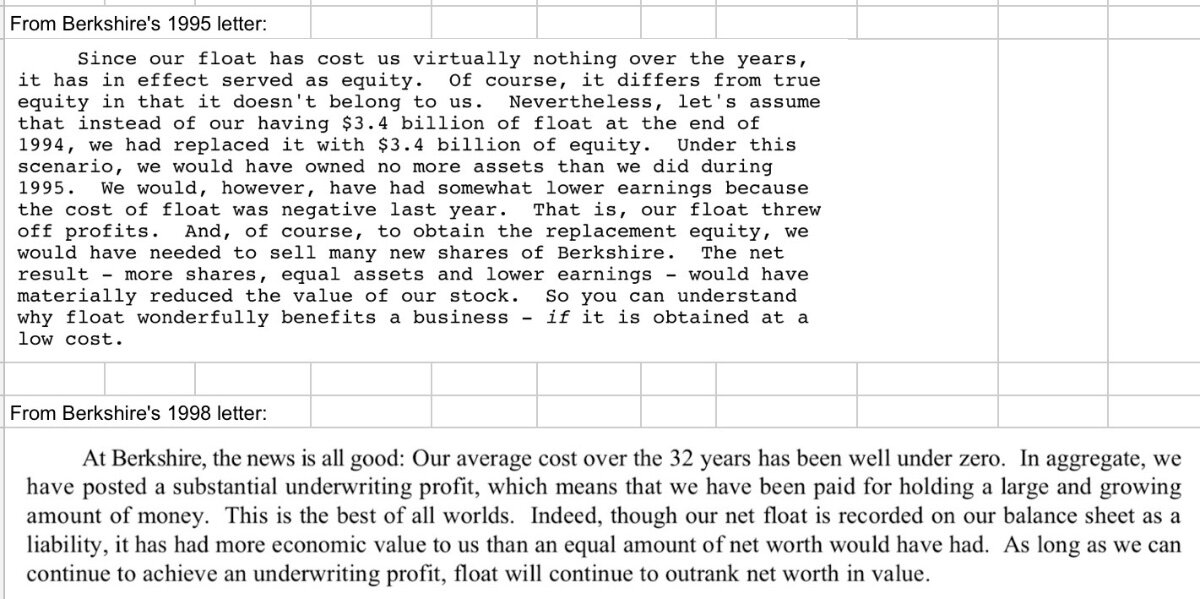

@Viking thanks for starting this thread and for all that you do! Feel free to ignore my request, but I would love it if you wrote an article for this thread expanding upon Buffett’s following quotes about how float can be worth more than book.

-

I believe the Strait of Hormuz will remain effectively closed for a long time.

-

Depends on how long the SoH stays closed. Seems to me that losing >10% of the world’s daily oil flow for much longer crashes the world’s economy, not to mention the hits to LNG, fertilizer, helium, etc. Could be even worse if more attacks to more infrastructure. I am holding lots of cash. If I am wrong and peace breaks out soon then I pay some opportunity cost, but if I am right then cash will be king.

-

I expect that the Strait of Hormuz will be jammed up indefinitely. Talk of the strait being reopened in the timeframe of weeks seems fanciful to me. This could be the biggest energy crisis ever. I believe that the best way to play my variant perception is with a large block of cash and to wait for opportunities to arise as losing 10% of the world’s oil volumes shocks the foundation of the world economy. If I am wrong and peace breaks out soon then holding cash should be only a small lost opportunity cost.

-

I am at 1/3. I believe Prem is over 90%. I am also curious how others think. Depends upon what other opportunities you are weighing the opportunity cost against. PS - Welcome to the board!

-

https://oilprice.com/Energy/Natural-Gas/Qatar-LNG-Hit-Turns-Into-Multi-Year-Crisis.html 17% of Qatar’s LNG export capacity offline for 3-5 years.

-

Kelly Partners Group

-

Small trading sardine in Sable Offshore Corp. Production restart happened over the weekend.

-

I am having the same problem as @zhuanquan Prem said “…about $150 per share after taxes, interest expense, corporate overhead, and other costs.” $6440 pre-tax income minus $3151 of investment gains minus the 2025 tax rate of 18% is $129 per share, not $150. (I am pretty sure that tax rate is different between operating income and investment income, but I don’t have a better number and it doesn’t matter that much anyways.) @Parsad I don’t understand how you are saying that we are double counting corporate overhead and interest expenses. Perhaps I can understand not counting corporate overhead dedicated to investment functions (don’t think that is what Prem is saying, but maybe). I do not understand how interest expenses on non-insurance companies is double counting.

-

Yes, it’s in the annual letter

-

$35.5B market cap divided by $70.0B portfolio minus $10.5B total debt (excluding debt at consolidated non-insurance companies which is non-recourse) = 60% (40% discount). This seems like a decent sanity check with the high quality underwriting that Fairfax has.

-

Worth watching. I would surprised if the percentage allocated to mortgages and RE changes much because of the acquisition of KW.

-

As a mechanical engineer who has used CAD for over 30 years, it is hard for me to fathom AI/LLMs reducing the number of CAD seats. When I used to work in R&D I used to say if we knew what we were doing we wouldn’t call it research. New designs are very much an iterative process with lots of testing. Even after product launch it was a rare drawing that didn’t have any revisions. Perhaps the manufacturing engineers wouldn’t need as many seats as I could imagine AI figuring out how to manufacture the designs, but that seems like a marginal impact in the distant future.

-

There are over two dozen small nuclear research reactors located at universities across the U.S. I don’t think SMRs would be any special security problem.

-

Sold all my Chapters Group. Still trading at a cheery consensus while Constellation Software and Topicus have had large draw downs and both now roughly half the P/S multiple of Chapters.