Xerxes

-

Posts

5,689 -

Joined

-

Last visited

-

Days Won

9

Content Type

Profiles

Forums

Events

Everything posted by Xerxes

-

indeed. But that craziness provided opportunity for the individuals to buy the stock well below book value and substantially.

-

I was thinking that it was a fake ad on FB using her credentials and face

-

-

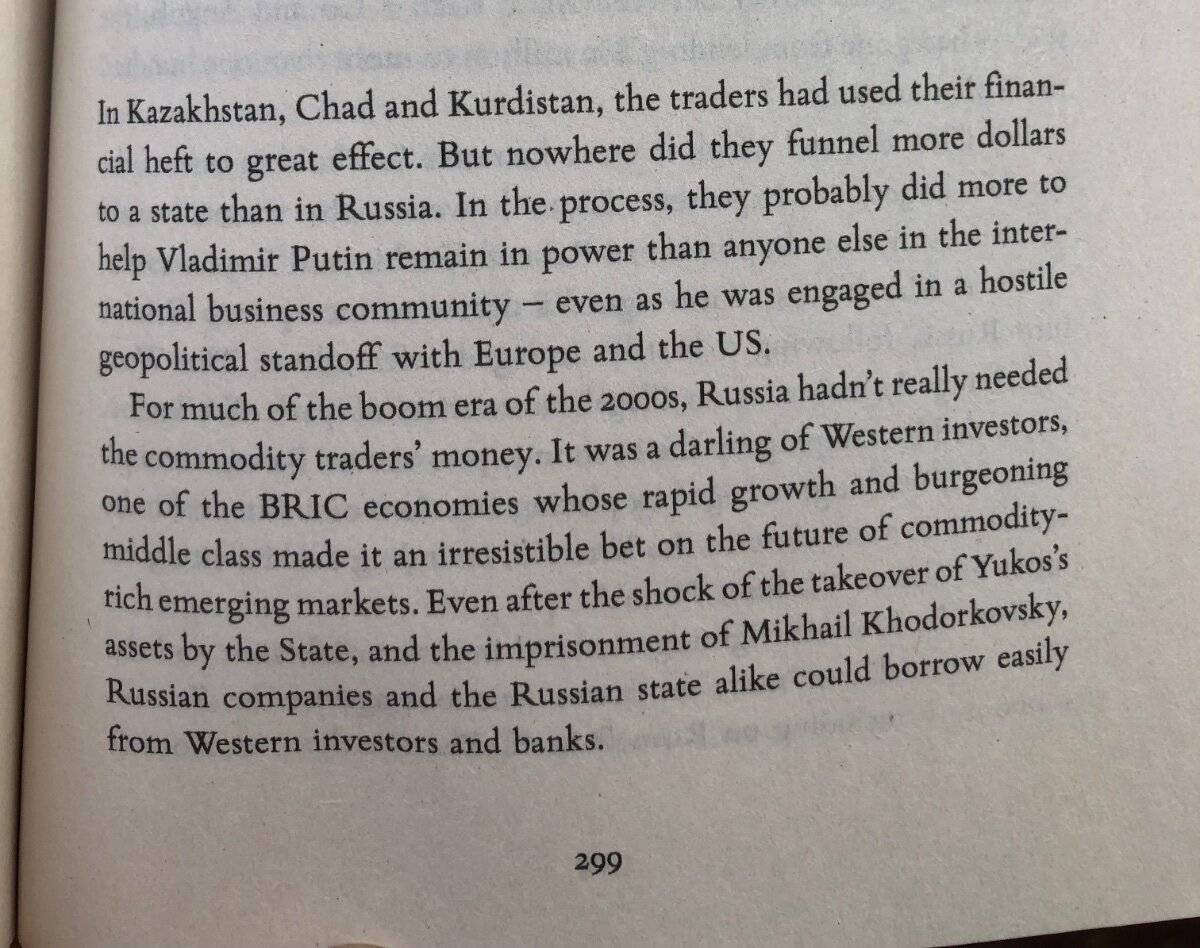

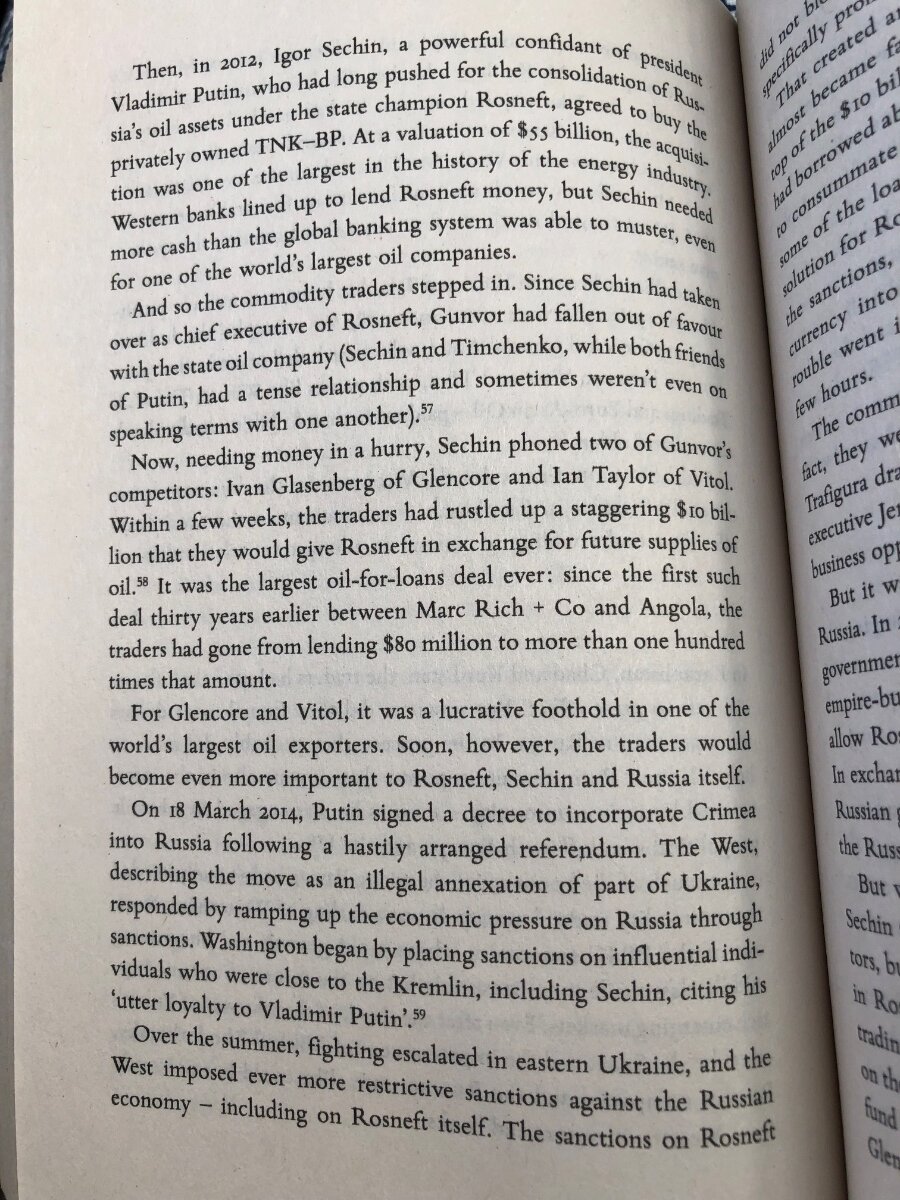

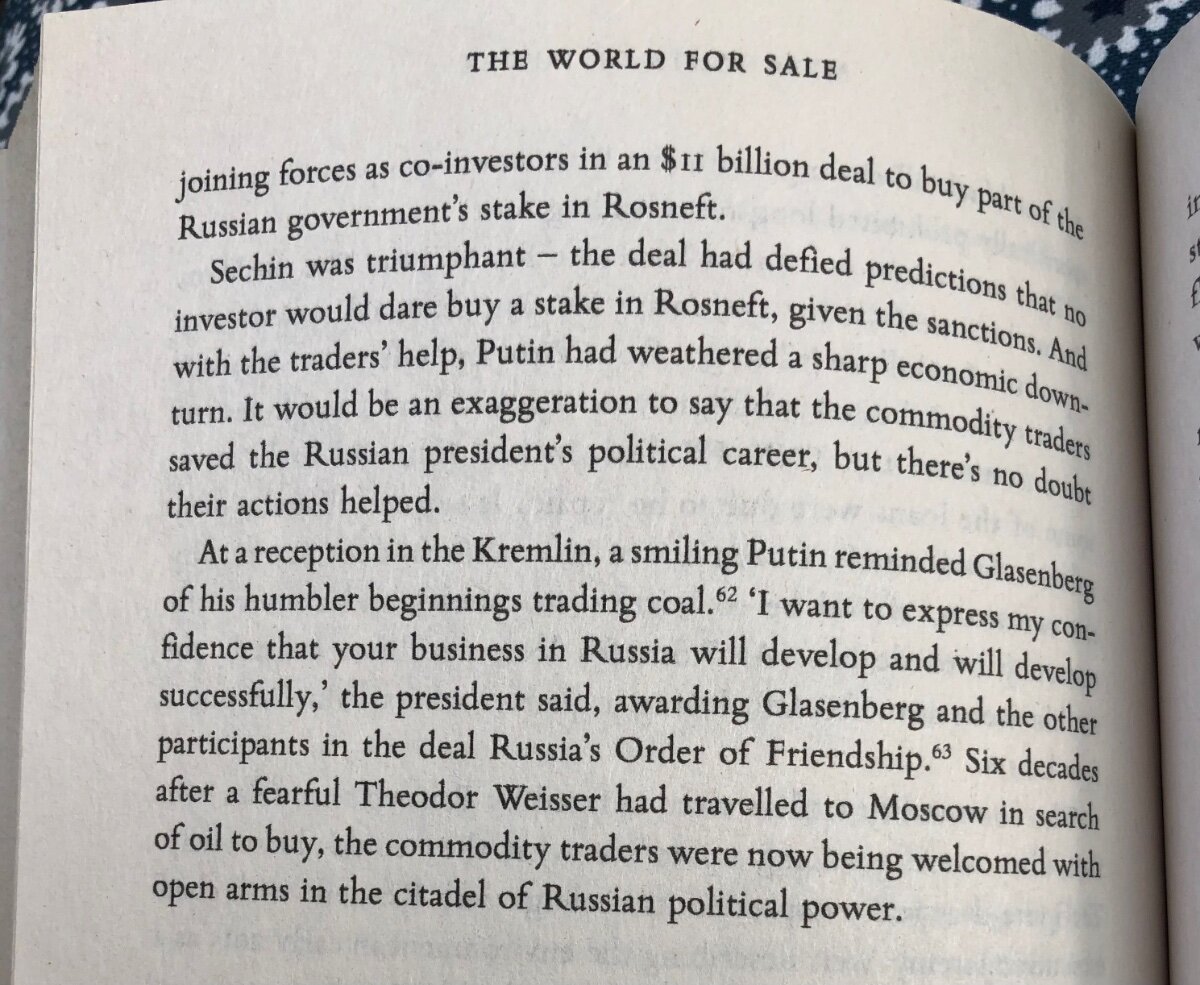

my pleasure. I finished reading the book. It was an incredible read. I think all of us read The Prize (most of us) this book weaves into the world of traders and who kept adapting as macro picture changed. I have heard a lot of Glendora, Marc Rich, Glasenberg, the commodity trader Andrew Hall at Citigroup and his oil trades, the rivalry between Xtransa and Glencore on the sought after coal assets, this brings all together. makes me wanted to listen Glencore’ investor day for fiscal 2020, when the virus start the spread

-

From the book, The World for Sale. By Javier Blas & Jack Farchy I vividly recall the Qatari-Glencore investment into Rosneft whenever that was in the mid-2010s. Glencore is currently engaged into take over attempt of the Canadian coal producer Teck Resources. Perhaps in this new fragmented world, the commodity traders, have a stronger role to play than the last ten years that was underpinned by stability and globalization.

-

https://apple.news/Aq5sSRBBETOeo7LmXfVc1fQ RUSSIA HAS REACHED A DEAD END An indifferent response to a warlord’s march on Moscow heralds the dawning realization that Russia has no good way out in Ukraine. JUNE 29, 2023

-

Luca. By now you should know that whenever West does something stupid (coup d’état, invasions, etc) the next generation in the West usually has a hard time remembering. They “file it” under “ohh that was the Cold War so it was ok” and move on some other fun things. Don’t fight it. There is no use.

-

Kashmir’ is very much Pakistan/India’ Taiwan. The pillar upon which their foreign policy and their relationship toward each other has been shaped. IMHO. There was once upon time an East Pakistan, lost forever (to Pakistan government that is), and now called Bangladesh as a sovereign state.

-

Fiction or not. An interesting read.

-

I almost think the fact that there were popular support for his person in Rostov, probably means his life will be extended, at least until there is no rumbling should he falls. But dead man walking indeed. And he knows it. As a historical analogy, the fall and disbanding of the Janisseries comes to mind. How they became a corrupt power within the Ottoman court over centuries, effectively a state within an state, and kingmakers, rotting the regime from the inside. Until a sultan decided that this was it. Auspicious Incident - Wikipedia I think Western media should be looking at the power dynamic between Wagner and Kremlin before 2022. There must be something there that has been unexplored thus far. This cannot just be a Game of Throne like episode, with warlord deciding to make a run for the King' Landing.

-

Very highly unlikely Kremlin, to their credit, achieved a great strategic surprise when they massed their troops at the gate of Kiev. And then wasted it. That was 2022. And that feat will not repeated. To be honest with everyone I dont know what to make of this whole episode. I dont know what to make of Pregozhen. Don't understand how a mortal man can be so loud ... it is surreal and still does not make sense to me. Anything that I listen on TV, just repeats the facts shown and build narrative after the fact. That said, I do think that historically coup d'etat have very binary outcome that are determined almost straight away when support materializes (or not), and in case it did not. Mortal men taking selfies in Rostov with the chef does not mean support. The pillars of the Russian state, the oligarchs and the support system did not flinch, and by not flinching they supported their Tsar. It was a very strange coup d'etat if ever that it was. As it was NOT explicitly directed toward the organ of the state (the office of the president) but toward ministry of defense. A very strange coup d'etat indeed. Dr. Ian Bremmer, from Eurasia Group, this morning had a great interview with Bloomberg Surveillance. The good doctor is absolutely right. The one thing we did not need was an totally unstable character Pregozhen somehow getting to the top.

-

Thank god the Secretary of State dumbed it down for mere mortals in the west.

-

lol. On a different note who would have thought, even in the early days of 2022, that there would be joker-like-character turned warlord that would capture so much bandwidth, and hurl so many insults at Kremlin in a back and forward comedy show, then march to Moscow only to turn around. Oh and his name is Putin’ Chef but he is not really the chef at the Kremlin.

-

This whole episode can be summed up as : the enemy of my enemy is my enemy !?!?! Huh !

-

Agreed. The economic decoupling has largely happened. Sure few % up and down here and there on the markets. But changing of the guards at the Kremlin is not going to mean much if it is just changing of the guard. The market will either open higher or lower and no doubt business media will build story around whichever comes. We are in the bull market of intellectualization of geopolitical content.

-

Nor did a young Peter the Great have much in forces as insurrection was breaking out in Moscow, before pillars of state and interest group moved to protect the Tsar and decapitate the insurrectionist. With mini-nukes the aim is definitely not about being effective. Nor is the aim about Rostov, which is a Russian city. Anyway, all speculation on my part. I barely read anything on this “developing story” beside few tweets shown above. And what is on CNN yesterday.

-

With “Putin’ Chef” barreling toward Moscow at the head of a rebel army, perhaps that is more of an opportunity for Kremlin. A use of a low-yield tactical nuke would kill many birds with one stone: (1) break the post-1945 nuclear taboo and normalize its usage (2) showcase an actual red line being crossed with the pillar of state being threaten by an insurrection (3) not use it directly against Ukraine (4) kill a tiresome Captain Rohm (5) intimidate Ukraine and others

-

As far as Prigozhin is concerned he is like the Captain Rohm of the SA in the 1930s. A useful idiot until his services was no longer required.

-

Neither Shoigu nor Gerasimov are going anywhere. They are the Keitel and Jodl of Kremlin. Loyalists. Anyone remember Marshal Voroshilov (one of the original 5 marshals of Soviet Union). He led the disasterous Russian-Finland war and was still around to tell his tale.

-

I am going to get shot for saying this in an FIH related thread. But I would be careful of these orders you see coming out of Paris Air Show. Just like when the automakers were falling over themselves to place POs for chips few years ago, you have the same phenomena happing in the aerospace industry. Lots of airlines FOMO buying production slots in the out years of 2030s. Take it for what it is, the directionality of India trajectory. But that is about it.

-

The catastrophic event would have pulled the metal vessel apart "like taffy," according to Naval History Magazine. "Complete destruction would occur in 1/20th of a second, too fast to be cognitively recognized by the men within the submarine." An implosion is basically the exact opposite of an explosion. Instead of pressure from within moving outward, you have pressure from outside rushing in. Similar to an explosion, there is unlikely to be much left of the vessel and its cargo. "I know it's no great comfort to the families and the spouses, but they did die instantaneously. They were not even aware that anything was wrong," journalist David Pogue said on CNN.

-

-

100%. Cannot have it both ways.

-

same here. I got 5 little nephews and nieces. I outsource all the hard work to my siblings. Just enjoying quality time with them.

-

I recall few years ago, Norway “donated” one of its many many high peaks to its neighbour who was otherwise barren of any high peaks. (don’t remember if it was Finland or Sweden). I thought that was nice. Unrelated: i am curious John. What are your thoughts about Greenland seeking full independence from Denmark.