Xerxes

-

Posts

5,689 -

Joined

-

Last visited

-

Days Won

9

Content Type

Profiles

Forums

Events

Everything posted by Xerxes

-

@SafetyinNumbers Please ignore my question; i realized there is a thread on it

-

Why say Strathcona Resources vs. Athabasca. They both have similar market cap and have a strong capital return policy. I know neither very well, just wondering your take

-

Barrick Gold talked about the need to redomicile to U.S. probably accelerated under Trump. There was no mention of this on conference call, and we know it is “been there done that” for FFH, but do folks here see a risk that the operation business environment would become such that FFH would need to redomcile out of necessity, for tax or other reasons.

-

The year : 1902 Reformer: Lord Fisher, First Sea Lord Target: a bloated Royal Navy By 1907, the Navy was costing £31 million pound. About £5 million pound less when the reform commenced in 1902. All that even as the fighting capacity of the Navy increased, both through introduction of new hardware, re-allocation of resources, elimination of fiefdoms and removing old ships which till then was used to “show the flag”. I think Lord Fisher would have been a good portfolio manager.

-

for what is worth from the conference call: Gautam Khanna Great. And then my last one, just on the new administration and how is TransDigm kind of working constructively with them and your thoughts on DOGE, and I'll just leave it open ended, but... Kevin Stein That's a great question. I anticipated this earlier, I think, in the Q&A. DOGE is -- it's a great opportunity for the U.S. to improve and streamline what they're doing, specifically with government DoD, DLA procurement. We think this is a really good thing. We've been engaging with the DoD over the past several years and have suggested a number of improved forecasting, inventory management and improved buying practices that would save the government money and save us time and energy in production. So we invite all inquiry and assistance. I've met with some of the DOGE folks in D.C. It's important to remember that TransDigm is a very small supplier. I think we're 0.3% of the DLA budgets and this amounts to less than 1% or somewhere around 1% of our revenue, are these types of products that would fall under a concern of DOGE. We see this only as an opportunity for TransDigm, the government, the DoD to improve what we're doing together. So we warrant any and all inquiries and work together to come up with a stronger solution in the future. So that's really where we're at. It's a small part of our business is supplying spare parts to the government. The bulk of what we do is either falls under TINA today, which is fully cost disclosed? Or is commercial of the type or competitive that's the bulk of our business falls under those 3 categories. So we invite the work that we need to do together to improve how we work together with the government. So that's, I guess, our answer.

-

In 2018 AGM, Prem has said and I quote (based on memory) "we want FIH to be as far as possible from FFH" A comparison was made (again from memory) to self-sustaining ships going on a voyage of discovery, while not putting mainland to risk.

-

There is also BAE that straddles both sides of Atlantic. I agree w/ you that the return from the European names will be poor. Referring strictly to their willingness to return cash in a politically charged defense environement. If you are looking for additional material, I think good source of material for A&D is the Aviation Week; i have been getting a print copy for almost +10 years now. A good weekly podast is the following: Defense & Aerospace Report Podcast [Feb 09, ’25 Business Report] - Defense & Aerospace Report Comes out every weekend and is the first thing I listen to Monday morning. More : (these are all recurring weekly podcasts) DEFAERO Strategy Series [Feb 11, 25] Bendett & Eugene Rumer on Russia, Ukraine On-going Conflict - Defense & Aerospace Report DEFAERO Daily Pod [Feb 10, 25] Trump Week Three & Byron Callan’s Week Ahead - Defense & Aerospace Report

-

yeah. IT ain’t sexy enough for me. And the prevailing view on land system is not looking bright, even with the largest land war in Europe. Gulfstream though is a gem. what is striking for me about GD is that since it’s corporate transformation in the 90s and very early 2000s, (I.e exiting aerospace and coming back to it via Gulfstream purchase) has not reshaped its portfolio, except for the bolt-on w/ IT in the 2010s, in contrast to the rest of cohort.

-

@Spekulatius @Hektor you gents do know about Electric Boat, don’t you ? no I don’t mean a boat that is electric. But rather the name of shipyard business owned by General Dynamics for decades now.

-

Nice. A blend of fact and fiction when it comes to Israel. Israel DID have nuclear weapons in 1973 and used it as BLACKMAIL to get critical weapon delivery from Nixon and Kissinger. Now I would have done the same thing if I were them. Nothing wrong with that. But let us not assume that Israel is too noble to blackmail. And to this day, we don’t know if Israel attacks USS Liberty on purpose or not in 1967. What was that for ? It is thick with controversies. Hell, an Iraqi mistake with USS Stark in the mid-1980s came out cleaner than that. Back on Ukraine, it needs to take the loss so that it can grow to be the fortress that needs to be. After this round 2, Ukraine will have the most advanced, combat-ready military force on the continent. That is an asset. Yes no one can trust Putin with any settlement. But you can trust that Trump doesn’t want another 2021 Kabul situation. And you can trust that once there is a ceasefire there would a reckoning in Moscow to take stock of what was accomplished. That will keep them busy. The question is Zelenskyy the man to lead Ukraine toward that settlement.

-

because banks are “financial services” companies and they are providing financial services to a corporate client, who has decided to take a position on itself and needs a product that fits the needs. Ideally banks makes their dough via fees And not taking a directional position for or against the corporate client. I.e so they would have been long the FFH shares to balance the TRS, if the risk officer was clear minded

-

We don’t know. He may be wanting something somewhere else. Not everything is and revolves about Ukraine. Russia clearly cares about Ukraine far more than America cares. ex: no trouble from Kremlin when (not if) Greenland is annexed etc. That is the whole idea as to why great power want to talk to each other directly. Quid pro quo. But like John Bolton said on CNN, in Russia they are probably drinking vodka directly from the bottle after yesterday announcement.

-

Easy answer: Rhienemetall, SAAB, and Thales etc US defense contractors are primarily long-cycle defense business. Driven by long term security needs. And not directly influenced by ebbs and flow of War in Ukraine. If anything the war Ukraine has shown the reliability of Western product portfolio and offering in a real setting. Just as 1991 Gulf War demonstrated Western weaponry in a real setting and opened up the market for Gulf nations to place POs for Abrams, Hummers, Patriots etc. even though Saddam was defanged.

-

Hard cold truth (mostly anyways)

-

Not exactly. Your knowledge related to FFH and investment in general have been compounding since 1998 by holding FFH since. Surely that unique knowledge and viewpoint cannot be squeezed into four years for those that ticked high CAGR by buying four years ago for the same overall financial return.

-

in the 90s when I was a teenager, my dad took me there and helped me open an account. i stayed ever since. on a more practical matter, they always reverse charges when i asked them. that said i never used RY for my mortgage. The rates are always too high .., and we always the underdog banks like National Bank and/or BMO coming with good mortgage product undercutting RY and/or TD.

-

I do everything myself as well. It is just that you cannot “click” for DRIP yourself. So you need to call them. Once they add that functionality I will no longer need to call them for that. now specifically to international trading, my understanding is that certain markets like Europe, London or Hong Kong you can trade directly yourself. For others, like Singapore or Japan, you need to call them. I suppose that is when Royal Circle comes handy. https://www.rbc.com/newsroom/news/article.html?article=125959

-

My mistake. I though we were talking FFh

-

I guess you mean 2007

-

thank you. I agree about Udaipur. An oasis in the desert. With amazing coffee. I read on The Economist that India has about 40 or so UNESCO sites with 10 million tourists every year, while Dubai has about 10 million tourists but with no UNESCO site. i think there are a lot of upside if the government leans-in into tourism. LOTs to see …

-

I don’t know much about Ashoka, but was told by my tour guide, in no uncertain terms, that only three people have the “the Great” next to their name in India: Ashoka, Alexandre and Ackbar. Assuming I am not mixing up Ashoka with someone else.

-

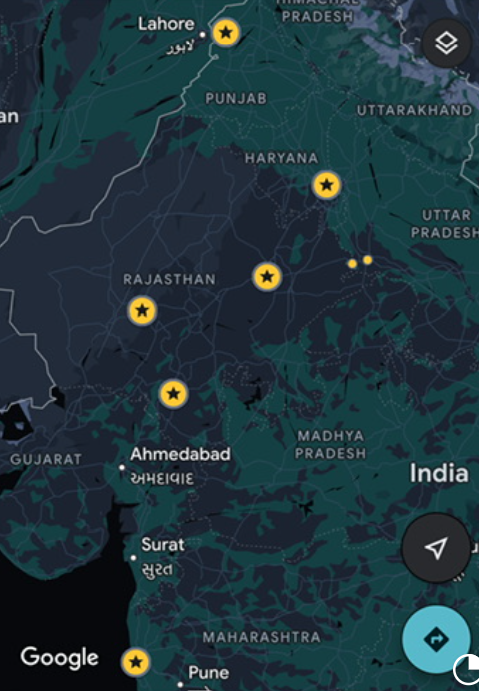

I figured i drop in a few words about my recent vacation to India. In short, I loved it. Everything. The people, the locations, its absolutely diverse geography and its history. I structured my trip around three different historical regions: mogul history, Rajputs and Punjab. And stayed in the north. Saw eight cities, so must have packed and unpacked 8-9 times, changing cities every 48-36 hours. The yellow dots and stars shows the geographical breadth of my travel. The first four location are part of the Golden Triangle: Delhi, Agra, Fattehpur Sikri, Jaipur. I was with a group as it is more fun with others. The last four cities, it was me, myself and I. I went to see Jodhpur, Udaipur, Amritsar and Mumbai. I did almost all of my booking through Booking, even getting taxi to drive me from Jaipur to Jodhpur and then from Jodhpur to Udaipur. I booked Indigo Airline for flight to and from Punjab. Delhi, Agra and Fattehpur Sikri are of course the heartland of India' Moghul history. From the Red Fort, to the Agra Fort, and Taj Mahal. Generally speaking, i found more than a few Persian words in the Hindi language. No doubt the remnants of the official court language at the imperial court, before Persian was replaced by English. For those listening to the Empire podcast; the last few months, they had one episode per Moghul emperors. It was pretty good listen while I was travelling. The host of the podcast is William Dalrymple, who actually lives in Delhi and author of many books on India. His podcast covers all of history, but his own personal passion (and books) is and are India. Amazon.ca: William Dalrymple: books, biography, latest update The last of powerful Moghul emperors was Aurangzeb, who sat on the throne for 50 years and was intolerant compared to his predecessors and waged wars. When he was gone, Moghul rule would continue for decades, but its intrinsic value would decline sharply. While that of the East India Company would be raising as it stepped into the power vacuum. The rest is history as the Indian subcontinent traded one imperial master for another. In Rajasthan, there five historical cities that one can see. I opted for three of them: Jaipur, Jodhpur and Udaipur. Each city has its own ceremonial king, but of course the political power is subordinated to Delhi as the seat of the Federal Government. Between these cities, Jaipur was the most renowned and wealth, given that its rulers had allied themselves with Ackbar the Great and had entered imperial service. Same with Jodpur to a lesser degree. Udaipur in contrast had resisted the Moghul rule. PS: I had masala tea, in the same shop that President Macron and Prime Minister Modi had had tea, when they visited the Pink City. In Pujab, I went to Amritsar to visit Sikh's holiest site, the Golden Temple. Loved it. Also went to the Pakistan-India border to watch lower the flag ceremony. It was pretty awesome and unique experience that I wont forget. The flight though was pretty long. The flight back was 20 hours ordeal, taking off from Mumbai going north, before turning West with a sharp 90 degree turn and making its way back to Canada, dodging both Russia and Iran for good reason. For what is worth, I hope these few words will inspire some of you to visit India. It is an amazing place. The food is great. The people are wonderful. Sure, at some point jumping city to city for like 8 times over 3 weeks, will exhaust you and you just want to go home, to shovel some snow and go to Costco. It happened to me, by the time I reached Mumbai, i was ready to go home. Lastly, if you go to India, go see India, and not some airport in the south, because Fairfax owns it.

-

-

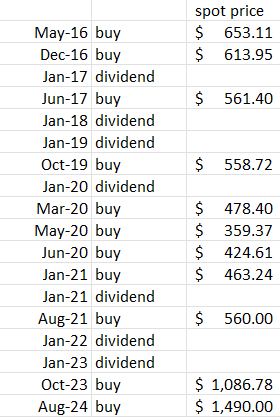

First bought in 2016 as a tracker position at $653 CAD. Leaned-in in the past 5 years. Three-quarters of shares were bought post-2020. Nothing has been sold. Based on my archives, my average cost bottomed at $494 CAD in January 2021, then average cost has been going up. Today's average cost is at $660 CAD.

-

Thanks. My experience with Royal Circle is that when I call them, someone very polite picks up right away and execute my Do-DRIP and Don't-Do-DRIP executive orders. I have not taken advantage of its research report. Once I looked at the App for it and could not find it.