Xerxes

-

Posts

5,689 -

Joined

-

Last visited

-

Days Won

9

Content Type

Profiles

Forums

Events

Everything posted by Xerxes

-

Agreed about lack of Russian air superiorty. There is however, one school of thought out there that thinks that within the Kremlin, there must have been a calculus of a possibility of a what-if scenario where NATO would have intervined, thereby they kept their cream of the Air Force out of sight. I dont disagree with that view. That possibility must have been wargamed. But it is also clear that in the inital phase of the war, they failed to take out Ukrainian air defenses. The curious case of Russia’s missing air force | The Economist On the lack of coordination between its forces. Russian army was and always been an artillery-based army. Even in the second world war, while historian often give credit the sacrifices made by the Soviet Union (and rightly so), the one often overlooked point is that the Luftwaffe was tied down protecting the Reich against the Anglo-American heavy bombers and slowly decimated by them. How well would have the Soviet Union overall against the full wrath of the Reich with the full support of its Luftwaffe. What other major conflict did Russia fought since the end of world war, except for proxy wars. My own personal belief (clearly wrong now) was that Russia had really used the war in Georgia in 2008 as a test bed to modernize its doctrine and bring it up to date to something akin to a Western coordinated fighting machine.

-

For clarity, while the irony rings through, I would say that Ukraine could not have really made use of the nuclear arsenal. They were just based there as part of the Soviet arsenal while the nuclear code was controlled by Moscow. The same way the space program launching pads happened to be based on what is today called Kazakhstan. Had Ukraine refused to give up the nuclear arsenal back in the 90s, it is possible that Yeltsin with explicit U.S. backing would have gone in to secure them militarily, even though it might seem like a hard picture to imagine given what we today. Those were different times ….

-

The pledge was signed with then-Ukrainian President Viktor Yanukovych, who had the backing of Russia, in December 2013 in Beijing. It contained the following joint statement:

-

Amazing …. presidents/PM of Poland, Slovenia and Czech republic are heading to Kiev, a city under siege, to meet the Legend himself.

-

1991 Gulf War was a clear win with clear objectives. it did however created a thirsty and vengeful cabal of men bended on feeding their fantasy and going back to finish the job in “special operation to de-ba’athify Mesopotamia” in 2003

-

whilst it is true that the “special operations” has not been going well for Kremlin, the reports of Syrians and Chechens are (I think) more to inflame anxiety and racial tension, than a strategic pause for its conscript army. Persians and Romans always used armies pooled from “fringe provinces” from the other side of their empires to fight their wars and supplement their regular forces. the one thing Russian army does well is to obliterate cities into submission with its artillery. There are not going to be doing any street fighting. Grozny is mentioned a lot on reports as an example. And since West took its gloves off on its economic war, so will Moscow. Nothing to loose unless Zelensky comes to a point.

-

Enter the Siloviki https://amp.theguardian.com/world/2022/feb/04/putin-security-elite-siloviki-russia

-

Amazing !! He probably served under Generalfeldmarschall von Manstein, who got his field marshal baton at the siege of Sevastopol (in Crimea) ! We found a link you probably know this already. a fun anecdote. FLAK = Fliegerabwehrkanone

-

haven’t heard of that one. admitingly, C&C and Red Alert were just b-type games. the one game that I really liked and was realistic was called “Blitzkreig”. You played most of the campaign in world war 2 as Germans. With all the h/w relevant to that campaign based on historical events. I recall this very well because in the game the famous German 88 gun you could use it both as an anti craft artillery as well as anti-armour. Which is what exactly happened in the war. The 88s were first AAA and later on became famous tank killers. and much later they were actually mounted as part of the Tiger’ arsenal.

-

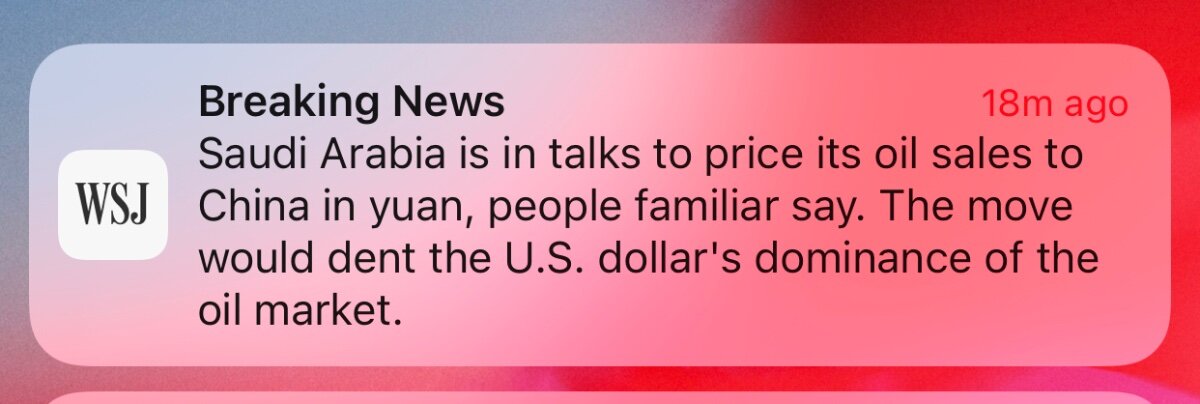

Some allies. Decades of friendship capped by a sword dance tournament with Trump in Riyadh and you get this.

-

for the next 10 years, all of the Call of Duty , Command & Conquer (90s game) games will be based in Ukraine and Russia. We are back to having them as the good ol’ reliable villians. they will probably resurrect Red Alert as well.

-

China will only buy the dip on Russia if it is well below book value with sufficient margin of safety. (i.e. they will get involve if it is 10x worth for it for them, i.e. having the Russian on the rope with massive concessions). In other words highly unlikely. There is no honor among autocrats everything is transactional. It has to be well worth it and right now not sure why PRC would supposedly be gaining beyound symbolic gesture. The future superpower (PRC as they see themselves) cannot be associated with what it looks like (and certainly is) a balatant and naked aggression that is getting so much attention. The Ukrainian blood that is being spilled is buying Taiwanese perhaps another decade of independence. The "Russia needs help from China" news is either exagerated up by U.S./allies intelligence community or it is very real but leaked by the U.S. intelligence community. Either way it was good to leak it, as it will pre-empt China and force it to take a posture. On Russia, the Oligarch cannot do anything. They have been de-fanged long ago, despite Western fasinations of them. There will be no "upraising" by the peasants and population, another fancifull Hollywoodish dream. The only threat to Putin is from within its own security establishment, ex- and current FSB. That said, they will also be pariah in a post-Putin world if ever that happens. Sometimes, crisis tend to focus the mind as it did for Zelensky the Comedian. Perhaps current crisis is also focusing Putin's mind. Power respects power. If he cannot pull it together, the only way out in Kremlin is in a bodybag through a palace coup. Thus self-preservation will have him focus his mind after all he is not dumb ,... just getting old, and for whatever reason it seems, he accepted the wrong inputs by his intelligence chiefs and miscalculated on a biblical scale. Some years from now, consipracy theories will develop that it was Western intelligence that fed that wrong intelligence to Kremlin, making Putin walk into a trap, de-fanging its warmachine, and its economy and sending it back to the Brezhnev era. This would be an interesting novel.

-

I have little understanding/knowlege of Oxy or its assets or what supposedly Buffett read in the earning call transcript that he didnot know about Oxy that was new, but just from the outside looking in, it seems this is not just an "oil-tracker" investment. He could have those buy investing in more liquid and deeper pool of assets like Chevron or Exxon. Maybe he seeks some sort of passive control on these O&G assetes and is willing to pay up for that control premuim. But none of that could have happened with Icahn around. I just dont think it is a concidence.

-

Alternative Asset Managers Getting into the Insurance Business

Xerxes replied to Canalyst's topic in General Discussion

Timely thread: Private markets have grown exponentially | The Economist There is also the new (not so new) kid on the block: TPG -

I just finished reading this book. It covers the internet sector and I think provides a good framework to aleast help investors not to brush off high valuation out of hands. Somestimes it makes sense and is warranted. The author talks a lot on CNBC and Bloomberg and i have watched (and liked) his interviews in the past. Nothing But Net: 10 Timeless Stock-Picking Lessons from One of Wall Street’s Top Tech Analysts: Mahaney, Mark: 9781264274963: Books - Amazon.ca

-

I don’t know about CNBC but she has one with Bloomberg from 5 days ago. It is on YouTube. On Icahn, something tells me that Buffett was always interested to expand on Oxy but wasn’t going to show his hand with Icahn there. When Icahn left or was leaving, he jumped on it ….

-

So no one is going to say it .... Fairfax !

-

A Russian debt default may be 'imminent'. What does that mean for bondholders? | Fortune Russia owes roughly $40 billion worth of euro- and dollar-denominated sovereign debt, approximately $20 billion of which is held by foreigners, the Financial Times reports. The relatively small sums—the U.S. paid out $137.2 billion in interest payments on foreign-held debt in 2020 alone—means a Russian default is unlikely to pose a major systemic risk to the global financial system, but it will be enough to roil investors with exposure to Russian debt and downgrade the country's status as a trusted borrower. Up until a few weeks ago, when Putin invaded Ukraine, Russia was considered one of the world's safest bets for sovereign debt investment, due to the country's low GDP-to-debt ratio and its sizable foreign reserves. Russia likely still has enough cash to pay back its debts, but recent sanctions on Russian oil and gas exports may have closed off a major revenue stream for the country and strained its cash flow.

-

RTX they are in business of selling picks and shovels, anything aerospace. Fully platform-agnostic. The commercial side is well balanced by the former Raytheon defense assets. most people gravitate toward Boeing and the likes for aerospace exposure (guess because of name recognition), far better to have a business where the aftermarket earnings goes over multi decade than the one that is lump sum with delivery of the aircraft.

-

You got to be f&&&ing kidding me. I talked about Russia, Ukraine, genocides in Rwanda, Burma, former Yoguslavia etc. I talked about fucking Gorbachov, I talked about Franco-German wars, the mongoles, Golden horde in Crimea, U.S. foreign policy, I talked about how Trump's greatest achievement was to create peace between the Arabs and Israel, ... but the moment someone makes a comment about Israel and its lands, you get all the retards in the world, rolling over themselves up to draw red lines around Israel and profess their support. No comments about children being thrown in the fires in Burma ,,, that is all good. But we fuc*ing cannot talk about Israel. Let's get this clear and see if we can through your head => Israel won its lands through wars of conquest. PERIOD. There is nothing wrong with that. PERIOD. And it doesnt matter who started the war, Nasser or "name the Arab tyrant" of the day. PERIOD. They have it now and as far as I am concerned they can keep it, since they are better steward than the alternative. PERIOD. But doesnt change the fact that they are responsible for popluation there yet they seem to have no problem treating Palestinean like shit and throwing them out of their home for fun. PERIOD. Are Palestineans any better, nope, since they refuse to accept the inveitable for decades. PERIOD. Now, that doesnt change the fact that everytime someone says "israel", retards line up to support and profess their love for Israel. PERIOD. That is what it means controlling the NARRATIVE. Who knows maybe 50 years from now, in an unlikely scenario that Russia somehow keeps swaths of Ukraine and de-populates some of the cities and replace the locals with Russians and throws them out of their home, we would be so tired & numb of seeing footages Ukrainian throwing stones to Russian troops that we wont care either. Now, now, now before you get too excited to point out the difference between Russian naked aggression in Ukraine and Israeli wars to defend itself in 1967 and 1973, no one is making that comparision. But the END RESULTS is the same, a population controlling (subjugating) another and making rules. Hence wars of conquest. If this cannot get through your biased, brainwashed head, nothing else can. PERIOD. I am done with this thread.

-

Cubsfan, Grow up & stop whining just because someone uttered the word Israel. Good thing I stated they had won their land fair and square. Victors had always written their own narrative from the dawn of mankind, whether wars were just or not. If nothing else, get that through your head.

-

There is no such thing as unfair or fair in war. In a war, you set out to win & completely obliterate your oponenent and then hire bunch of latte-sipping analysts re-write history. Like how Israel done it. They got the Arab lands (fair and square through wars of conquest, IMO), and they can write their own narrative. Several decades later, only the bravest Westerner is allowed to critize Israel, before being called an anti-semitic and shamed into going back on what they said. And even when they critisize Israel, they have to bow and dance and explain themselves. For every geoplitical action there is an equal or greater geopolitical reaction (a bit different then Newtonian mechanics). So only a fool would dismiss the long term liabilities of a certain action that we are taking now with Russia. It is a gamble. If it works and somehow Russia get rid of Putin in a not too distant future that is great. But it can also backfire and backfire badly. I would remind everyone, that it was not long ago (last August) when U.S. made a complete mess in Afghanistan, and now it is Russia who is the one making a mess, and sleepy Joe is beaming in pride. Situation changed in a matter of six months. Things that may look very clear now, may look very different 5 months from now. Putin rolled the dice, gambeled and in my opinion lost big time (even if he reduces Ukraine to ashes). Credit goes to Zelensky (who IMO signed his own death warrant with his heroism). Right now we are the one rolling the dice and keep getting double-sixes.

-

Cycles of violence. Worth looking at the history Franco-German conflicts. Same year might be off. - 1806: Napoleonic invasion and subjugation of Prussia - 1815: Battle of Waterloo: everyone knows about Duke of Wellington, little people know that there would be no Waterloo without Blucher and his Prussian seeking revenge. - 1870-72: Creation of German Empire and the elevation of King of Prussia to Kaiser. This was done in the famed Hall of Mirrors in the Versailles Palace in France, after Otto von Bismarck had Napoleon III on the run. Loss of Alsac-Lorraine territories - 1914-18: French re-took the Alsac-Lorraine territories. In 1918, Maraschal Foch and his German counterpart sign the armistice in his train carriage (which i believe was his warcarriage). Treaty of Versailles few years later (1921?) and subjugation of Germany. The treaty was signed in the very same hall of mirrors where German Empire was proclaimed. - 1939-40: German conquest of France. French surrended signed in the very same train carriage that Foch took German's cease-fire. After that Hitler had the train carriage destroyed and in his mind the shame was forever removed. In Sept 1984, severn decades after the start of the First World War, German Chancellor Kohl and French President Mitterrand held hands. That is 178 years from the Napoleonic invasions. Think of everychild now in Ukraine and one of them is thinking ....

-

I disagree with that statement. Sounds like we are saying that, "we are doing all the hard work of choking you to death, but you got to do some legwork and remove the guy we dont like". Sanctions are stupid and work only to create an entire generation people that know nothing but misery, The moment sanctions goes up, at that very moment, almost instantiously, black markets comes into business. And whoever controls the border and ministries and flow of goods, controls the black market. We are making headlines about going after Oligarch yachts and mansions, but at this very moment, we are creating a new class of oligarch in Russia. We do not know the names of this new class of enterprising Russians that will circumnavigate the sanctions, because they are being created at this very moment. But you will know them and hear their stories 15 years from now.

-

LOL ... Yes, i do indeed like my lattes in fact, i love coffee, that first sip in the morning kills me ! Damn, i hope that does not mean that I am projecting myself and actually that it is me who up just woke and realized the world is one big ugly place. Seriously though, some of those scenes that you see, where black people (students or otherwise) trying to leave Ukraine, and they are being held back by Polish or Ukrainian police at the border really pisses me off. I dont see much coverage of that. Granted I dont have full context but I assume this is not the time to let or not let people to escape to safety based on the color of their skin. This crisis has really shown the best and the worse of us.