Xerxes

-

Posts

5,689 -

Joined

-

Last visited

-

Days Won

9

Content Type

Profiles

Forums

Events

Everything posted by Xerxes

-

On the topic of war crimes or not. There is no point arguing. This is like shorting a good short against a rising market (public sentiment). It doesn’t pay to swim against the current. From my point of view, Putin, Rumsfeld, Cheney, Bin Salman, are cut all from the same cloth. Blood thirsty men bent on domination. The middle two are born in the U.S. so we classify them as “ambitious men” or if we want to be very extreme about them we would say “very ambitious men with great political acumen”. But never as what truly they are. no one answered my question from pages ago: are General Lemay and General Westmoreland to be considered as war criminals. If not why not ? They had one thing in common, they fought wars against Asians.

-

I don’t believe Biden got emotional and let loose the “Putin must go”. He is smelling blood and like any other good politician he is positioning for that eventuality … and working on this re-election campaign at the same time. the job was left to his state secretary to give the formal government position.

-

Message from Kim. I am here too on a different note Shoigu (Russian defense minister) had disappeared for more than 15 days, only to re-appear briefly yesterday, and then today the word is that he had an heart attack. I would too if my armies (my raison d’être) was melting around me

-

War is over !! waste of a beautiful tiger

-

Well done Spek !!

-

Reading your first paragraph I am not sure where the disagreement is. Except that natural gas is a question for Western government to solve and not NATO. As for your second paragraph, let’s be clear on definitions. “military intervention” for me means just that: no-fly-zone, bombing Russian positions etc, which you said you are also against, which is where I am standing too. I got no problem with re-painted Mig-29 being sent under the radar to Ukraine. But that is not called a NATO military intervention. So again don’t see any disagreement, except for definitions. on third paragraph, I am glad

-

Just imagine how off Russian intelligence was about Ukraine, and how off their perceived view of Russia’ national security could be … that completely deranged view, amplified by sanctions, and the need to not back down would be the deciding factor to go the tactical-nuke or not

-

fully agree. Donesz were just pawns in Putin’ hybrid war. Even he didn’t want to annex them. But just to keep them forever in state of limbo.

-

How many people who are posting on this thread have actually lived in a country at war or one that has been invaded. Or served in the military ? having an ice-cream in NYC while cheering for the invasion of Iraq or watching it unfold in 2003 doesn’t count “as living in a country at war”

-

i don’t think anyone here has said they should lay down their arms or anyone here disrespected them. I think people in this thread need to stop thinking in binary terms. Right now both sides (Russian & Ukrainian) are just gathering as much bargaining chip as they can even as they exhaust themselves on the battlefield, so that they got the most bargaining chips when the talk restart. But at some points both sides need to give in. What they will give or not is up to them. For instance if Zelenski says no formal recognition of Crimea, well guess what war continues, even if Russia is depleted it will just not end. If there is no mechanism to safeguard Ukraine’ safety against the wolves than that won’t work for Ukraine either. I.e de-militarization is non-starter. as far as Afghanistan is concerned, we empowered ISI, funnelled into it Saudi money (along with Bin Laden) to wage their jihad along Stingers (which came down some years later). But I don’t recall U.S Air Force flying sorties against Soviet positions. if what you are saying is that World War 3 is worth having for Ukraine. Then the answer is no. I am sorry but it is not. Everything short of that vortex that will push our insane leaders to do insane things. I ll remind everyone that the Soviet almost went nuclear early 1980s because they mistook a NATO exercise for the real thing. Just because they themselves had simulated a real pre-emptive nuclear strike during an excerise. Nothing to do with Ukraine. Just like World War One was not worth having because Austria-Hungry decided to punish Serbia by an invasion. and of course WW2 is just a by-product of the first war. frankly this current war is doing more damage to Russia than the Soviet-Afghan did in 10 years. At least that was amortized.

-

https://www.bbc.com/news/world-europe-60859337.amp Russian warship destroyed in occupied port of Berdyansk, says Ukraine

-

Often it is the aggregate of small things that changes the course of the war. The battle at the airport in the early days of the war (already been a month!) was probably instrumental as well as Zelensky’s initial appearance. It ceased to be “special operation” for average Russian troops and general staff the moment that initial onslaught failed. it is clear that the Russian army does not want to fight this war *cough* special operation. There is funeral of a Russian read-admiral (I think) on YouTube. He was born in Ukraine and died fighting for Kremlin. You can imagine how conflicted everyone is. Shooting brothers and sisters. Russian killed 20,000 people during the siege of Grozny. No one bat an eye.

-

Mao is probably responsible for 30 million death give or take 5 million. Not mention keeping Pyongyang on a life line when his “volunteers” crossed the Yalu River sent back the Americans south of the 38th Parallel. PRC & US were in state of war for more than 20 years from the Korean War till mid-1970s: Were Kissinger and Nixon wrong to go there and break bread with the mass murderer and formally recognize China and dump Taiwan. No. it made sense. The stakes were MUCH higher, than what happened 20 years ago.

-

Was General Lemay responsible for war crimes. If not why not ? Was General Westmoreland responsible for war crimes. If not why not ? There are no saints. I am for one glad that NATO stepped in and stopped Serbia. But guess what, 25 years is not today. And Serbia did not have nukes and Russia was not strong enough than to protect it.

-

the security camera footage at the beginning of the clip showing the Russian tanks rolling in looks like something like the movie Seven Samurai, when the bandits walk in.

-

I am not sure I understand this comment about “those pushing theories” or whatever that suppose to mean. People in Mariupol got to do what’a right for them. No one knows that better than themselves. Not even Zelensky and certainly not people who are “pushing theories” behind the safe keyboards. when we are talking (at least me) i am talking is at Zelenski level. And this is not a theory nor a movie. His decisions will change the course of history. I bet he didnt know that 12 months ago, back in spring of 2021, the immense weight that he would be carry on his shoulders. Are we really surprised about the kangaroo tribunal being set up, given that Biden had said Putin is war criminal. There is always tit for tat, and this is not a theory.

-

Greg sorry what is MSM. I have seen this few times. Do you mean MSNBC?

-

@changegonnacome admitingly I think most of us (me anyways) had our central tenet of belief turned upside down when it comes to Russian military in 2022. NATO reigns supreme, while the emperor has no “conventional” clothes (except for 6,000 km/h Dagger and other Doomsday machines). Even the massive $600 billion FX/gold didn’t help it if there was no market to trade FX. I think there is possibility sometimes from now, that this war will be seen as a trap set for Putin by the globalists with poor Ukraine as a bait. Once Putin walked in …. “Look at the crumbs on his jacket. He did it !!”

-

If we are doing analogies I ll go with V2, in terms of being fast making it invincible. The hypersonic dagger goes as fast as 6,000 km per hour. God that is fast ! This was just a opportunity to test it without its nuclear warhead. another Russian doomsday weapon that is scary (it’s name escapes me) is a nuclear torpedo that detonates near coastal era, unleashing a tsunami …. Or so the legend goes ! there is yet another one which is fully classified. But we have a picture.

-

To be fair, I think Viking meant what Putin really wants. I.e what will really bring closure. Not just the formal demands.

-

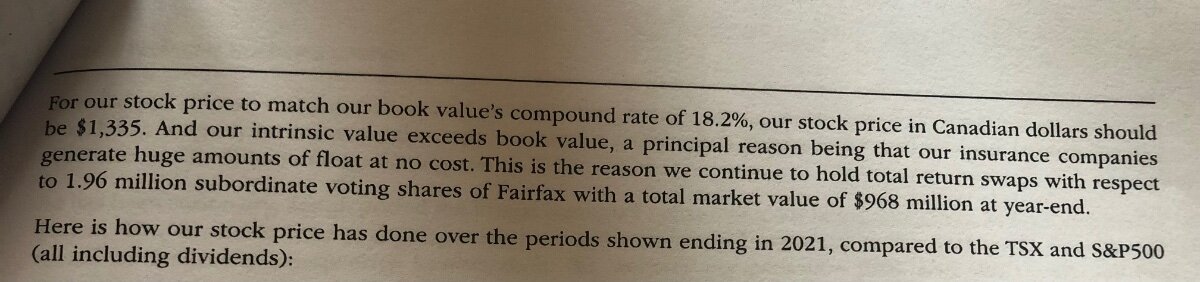

Ok @Candyman1 here is the statement from the letter, while doesn’t offer any clue as to when TRS will be liquidated it offers some clue on the perceived margin of safety it has, as seen from Watsa

-

I don’t have an answer either on those two questions. the only thing that I can think of as a tangible Russian “ask” is the control of the Black Sea coast and related cities (Odessa, Mariople). Everything else they don’t need anymore (I.e Kiev) they will pound & burn and inact such a high cost on the poor Ukrainian, and forever keep the city under the spectre of threat as a “hostage”. that is the only think I can think of. fully agree with Spek, that we are now in war with Russia, in all but name.

-

Mike Wilson of Morgan Stanley has been also pounding the table as early last August (I think) that today is more reminiscent of post-WW2 and not 70s. I have tried looking for that interview but cannot find it.

-

No one is under any illusion that a permanent cease fire would mean swaths of eastern Ukraine de-populated either by choice or by Moscow, to give the re-drawn map more permanency. Living under Russian yoke, or anywhere proximate to it, is not a life worth living. I ll push back on the Chamberlain/Munich comment (re: how Neil would be a good speech writer). I get it. Who doesn’t want to pound their chest and be Churchillian, all day long, in face of adversity. But that is the version of history where that scenario played itself out. This is not Lord of the Rings, where it always have a good ending, no matter how many times you watch it. Can you imagine Emperor Hirohito getting all Churchillian as the atomic bombs were being dropped in 1945. “We will fight to the last man, we will fight in the mountains” It is not like he knew that post-war Japan would thrive economically. At moment in 1945, Hirohito needed to be a Chamberline not a Churchill, while full knowing they were being subjugated and the post war economic prosperity being unknown to him. Btw And there were 2 atomic explosions because Americans had only 2 bombs. If they had 15, they would have nuked every city (saving Tokyo for the last) from south to north and north to south, all day long and every day. That is what that war was. Eradicating the Japanese race from the face of the planet unless unconditional surrender is tendered. Edit : before anyone gets excited and points out Pearl Habour etc. it doesn’t matter … that is what the war evolved into. Unconditional surrender means only one thing. Subjugation or destruction.

-

Well BRIC was a narrative as a portfolio of letters. As long as one letter (C) pull the rest of portfolio. The narrative worked well enough till ‘08. Now the new narrative de-carbonization etc. until it isn’t. for me it makes sense : the money distributed in the Covid era end up in the low/middle class who buy houses, more cars, dishwashers etc unlike ‘08-09 money printing that just inflated assets.