Xerxes

-

Posts

5,689 -

Joined

-

Last visited

-

Days Won

9

Content Type

Profiles

Forums

Events

Everything posted by Xerxes

-

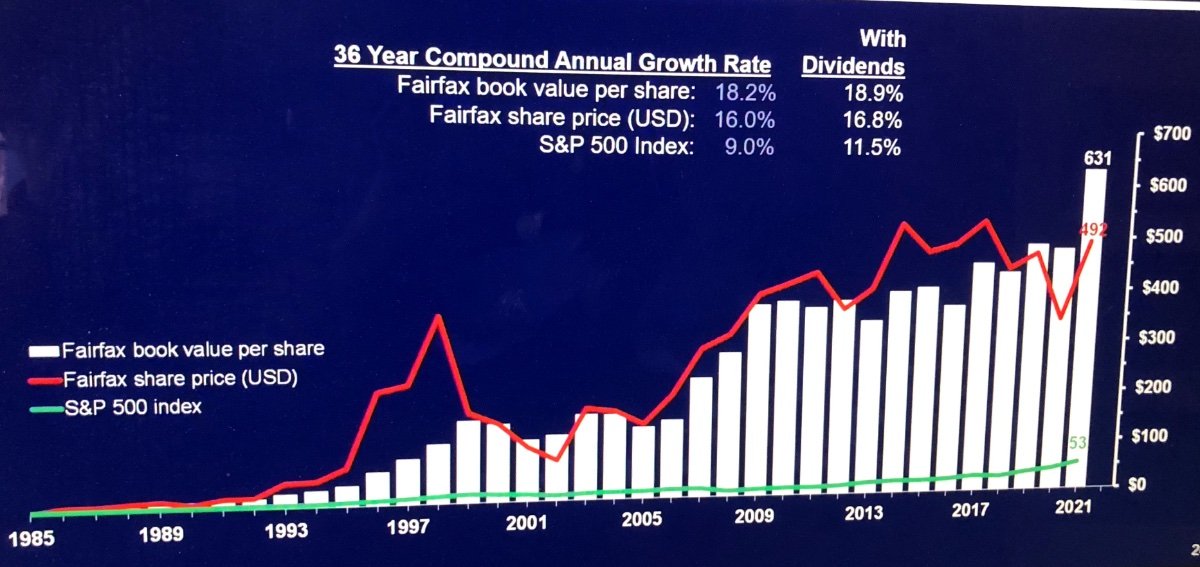

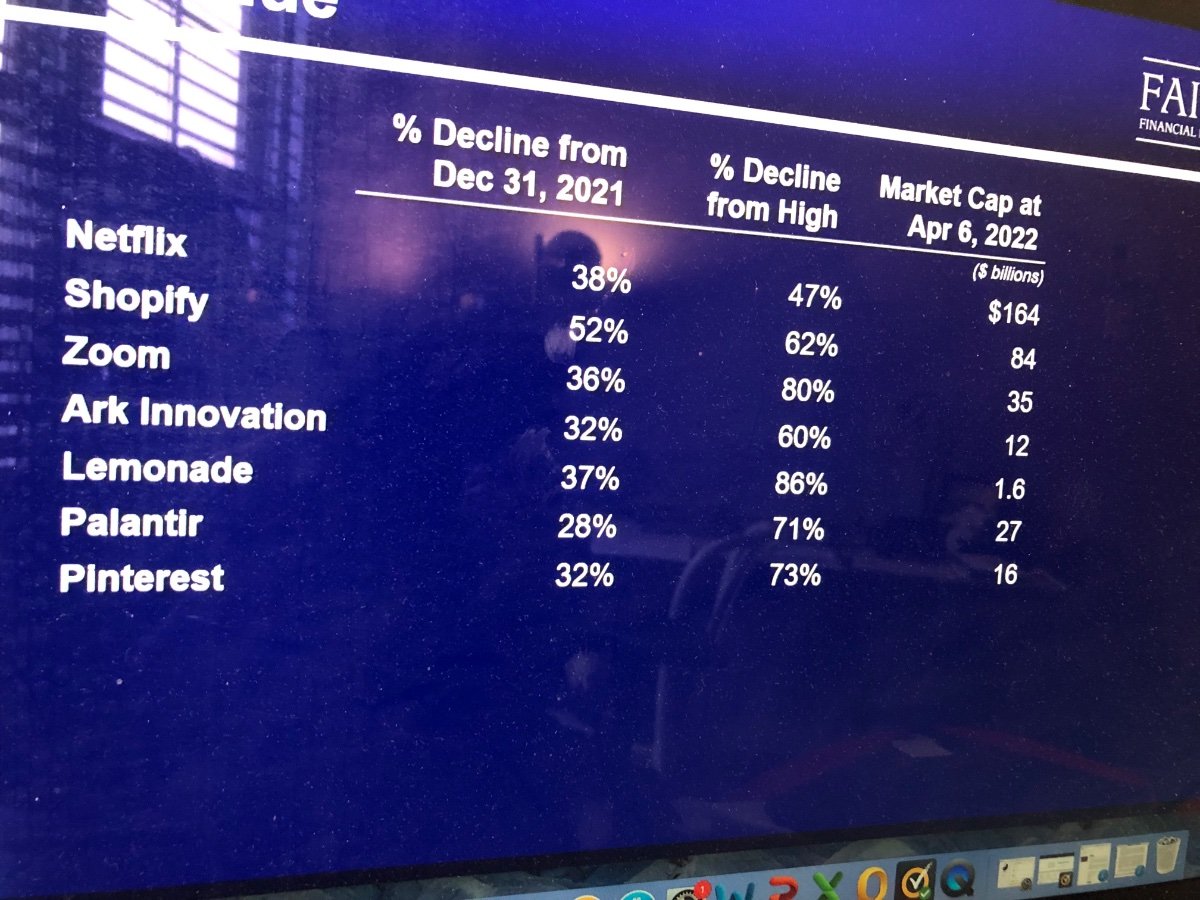

I think this might be the first time I see FFH share price and book value shown in the same currency (USD). annual reports shows them in CAD and USD, respectively, for some weird reason that I cannot fathom

-

Movies and TV shows (general recommendation thread)

Xerxes replied to Liberty's topic in General Discussion

i saw the three hours movie in 3 sittings. I can only tolerate an hour on tv. The moment I saw that re-imagined Times Square in the opening scene, I knew we were in for a treat. yeah definitely film noire. And very well done. I hate reboots, but this one I ll take. -

Guys I am NOT talking about massing armies. Or doing war maneuvers. all of which they have done on and off as early as April 2021. the average joe sitting in Moscow coffee having that latte didn’t see it coming. (An actual all out invasion). Even the spy chief on public TV was off the rail when talking with Putin and that was not staged.

-

Everything is relative. If there was 10,000 trolls in 2014 and 50 trolls in 2022, it doesn’t make my argument wrong. Now I was neither paying attention to the trolls then and now. But I have seen the comparison argument in the western media a lot (The Economist even had an essay on it calling the contrast with 2014 odd), which made the whole thing confusing to decipher leading up to the war. Anyways. Point taken you saw some trolls. Agree to disagree.

-

I am telling you guys the whole thing was made up in Putin’ brain on the go. Even internally at the highest level they were probably shocked. If soldiers were not ready, don’t think their people were ready in contrast to the 2014 annexation. it was an internal shock and awe as well as an external one.

-

-

Hahaha “The guy (Ackman) who bought it when it dropped by 20% sold it yesterday” I ll give Prem credit for saying we don’t have the skillset to see if Amazon other bets would have paid off or not. Thats fair.

-

Netflix down %30, just in time for Prem to make a comment about it at tomorrow’s AGM

-

Movies and TV shows (general recommendation thread)

Xerxes replied to Liberty's topic in General Discussion

The new Batman looks really good. I like the style. Highly recommend "Tokyo Vice" on HBO (Canadian Crave). About an American journalist working stories on the Yakuza in the Tokyo underworld in the 90s. Really well made. -

Fairfax = Fair and Friendly.

-

Viking you probably know better than me, but I ll say it anyways. You better off staying with what you know (FFH) and riding it out … than diversifying into its lesser branches (Recipe, Resolute etc). There is no need to make a move and “locking in” gains. Only to go down the quality ladder.

-

Russian state prepared their people in 2014 for what was coming. In 2022, complete opposite. No preparation. Despite the obvious signs of an army massing near the border and even going to Belarusia. I believe (with no evidence) that even foreign minister Lavrov didn’t know what was in Putin mind only weeks away from the invasion. I believe what Russian state says and what Putin decides to do are two different things. And things happen the way they did, because he chose to make it a fait accompli no time for internal dissent. On nukes, Russian state is doing is job in signalling what they have told to signal, that is there is no escalation to that. But If it does happen i don’t expect it to be signalled in advance. it is already a long war and the day is still long. We are at year 8 and counting.

-

The Dutch auction and periodic won’t close the discount. That is not the intent. What will compress the discount is the airport going back to its full pre-pandemic capacity and showing in the numbers. The buybacks is just to get ready for that inflection point. After all the discount is based on book value, which itself is based on a calculated intrinsic value. The real economic picture for the airport need to “kick in” …

-

there was this podcast on it as well. https://www.fool.com/podcasts/industry-focus/2021-05-12-wildcard-is-nelnet-a-hidden-gem

-

Understood. Cheers. I would just mention that the wrinkle would be that Russia has veto power in the UN Security Council. We can argue the flaws of the system, but for now it is what it is. UN was pretty much ignored by Bush, Cheney and Rumsfeld as they prepared to march the legions to Gaul for glory in 2003. So not only Moscow & Beijing can veto everything they can also ignore it as a dead body (Ala John Bolton) A UN move would be symbolic, but agree that if works would be a clever way to go around the NATO dilemma.

-

Who is saying it doesn’t ? The escalation ladder is what we are talking about. What response they expect vs what is given. Given all mishaps we saw in the past 8 weeks, I would say it is more likely than not that there is a huge mismatch on the escalation ladder and threshold. Moscow has a clear threshold and we don’t what that is. That said your point & Spek point differ that he is talking about direct conventional limited response within Ukraine by NATO. You are taking about U.S. increasing its supply of weaponry to UN. This is not going to be Gulf War & Kuwait 2.0. Pipeline carrying Russian gas does not need to be blown off, to add more damages to the Ukrainian infrastructure, the end customer can just stop receiving it and default on its contractual obligations (and deal with its consequences). Why blow off pipeline. (Other than have more business for Brookfield Infrastructure at a later date) I guess we have different perspectives.

-

That is a great point ! But i would say that point had a shelf-life that ended by the invasion. Now, the perspectives are very different. If before we were toying with the Ukrainians, not being able to decide how much we ought to care, it is different now.

-

makes sense, now that you put it this way

-

Well said, it becomes normal to use thereafter. The Dow will drop 15% after the first use of nuke in the war, but then ends of closing the week on the positive, after the markets realize hey the world didnt end. Sad but true.

-

What we consider as an escalation to WW3 (grouping all things nuclear) is probably seen by them as a legitimat extension of their current conventional war ... and not seen as escalation to WW3. Hence my example about Japan. West has a very different sandbox in term of how to view escalations when compared to Russia. i.e. a mismatch in the escalation ladder. I am not suggesting that they are ready to set the world ablaze for the hell of it, but I do suggest that they view tactical nukes as a natural extension of their forces currently fighting. Another tool in the toolbox, just like the flow of Western equipment to Ukraine, is another tool in the Western toolbox in its undeclared war against Russia. The Western perspective is that the use of tactical nukes leads to WW3. That equation does not (in my opinion) hold for Russia. Anyways, just my opinion. Their concern for their troop safety (pulling from Kiev) is more of a concern in fixing a very flawed strategy of launching war on three axis, which has now been unified under the leadership of one general.

-

Said differently: Did the Japanese military caste who held sway over the foreign affairs and governement at large made the right bet when they put their plan in motion for a pre-emptive strike at Pearl Harbour. Which was very much similiar to what they did in the 1904-05 war with Russia. i.e. pre-emptive strike being a normal course of action to start a military conflict. It made sense from their point of view given the sandbox and their calculus. Washington may have thought otherwise ... but that didn't matter, the point is that the Japanese did it like that despite conventional thinking.

-

The remaining NG trade with Europe is the counter-weapon that Europe will deploy and I agree with that. But overtime that is slowly going away anyways. We in the west might see the use of any kind of nuclear weapons as a taboo (thereby your dealth cult comment), but clearly their military doctrine allows them to deploy as a first-use on the battlefield against enemy military formations. All I am saying is we cannot hold & apply conventional Western thinking. I for one have been mostly wrong abouy my assumptions about Russia in the past 2 months. So I will not assume that they will not trigger their tactical nuke based on some sort of conventional business case.

-

-

Great post, until the day it isn't and a tactical nuke is indeed dropped ... And disagree with your last paragraph, that was the whole point of this invasion. A RESET. Putin would have been in box 10 years from now, if there was no invasion, with Ukraine propsering while Russia stagnated. Now he is back at it and fully in charge, traitors gone, oligarch with questionable loyality gone, and the world on the edge. Him and his will draw from power from that. If you are anybody in the Russian societ today, you EITHER WITH HIM or are AGAINST RUSSIAN PEOPLE.

-

You get 2 out of 3 right. The first two paragraphs. China cannot understand & control Vlad Putin anymore than we do. Kremlin will not seek permission from Dehli nor Beijing to address what is considers as its national security. The events in 2022 will make Russia subservient to Beijing over time, but the latter will have no influence today now that the war has been launched. Only one person does. And only that one person knows his red line threshold.