jfan

-

Posts

861 -

Joined

-

Last visited

-

Days Won

5

Content Type

Profiles

Forums

Events

Everything posted by jfan

-

I understand your use of long-dated warrants and moving out on the risk premium spectrum to maximize your returns. Why did you choose this strategy instead of using margin or personal leverage to purchase the equity of the royalty companies especially those who are overcapitalized.

-

Just curious why the producers and not the associated royalty companies?

-

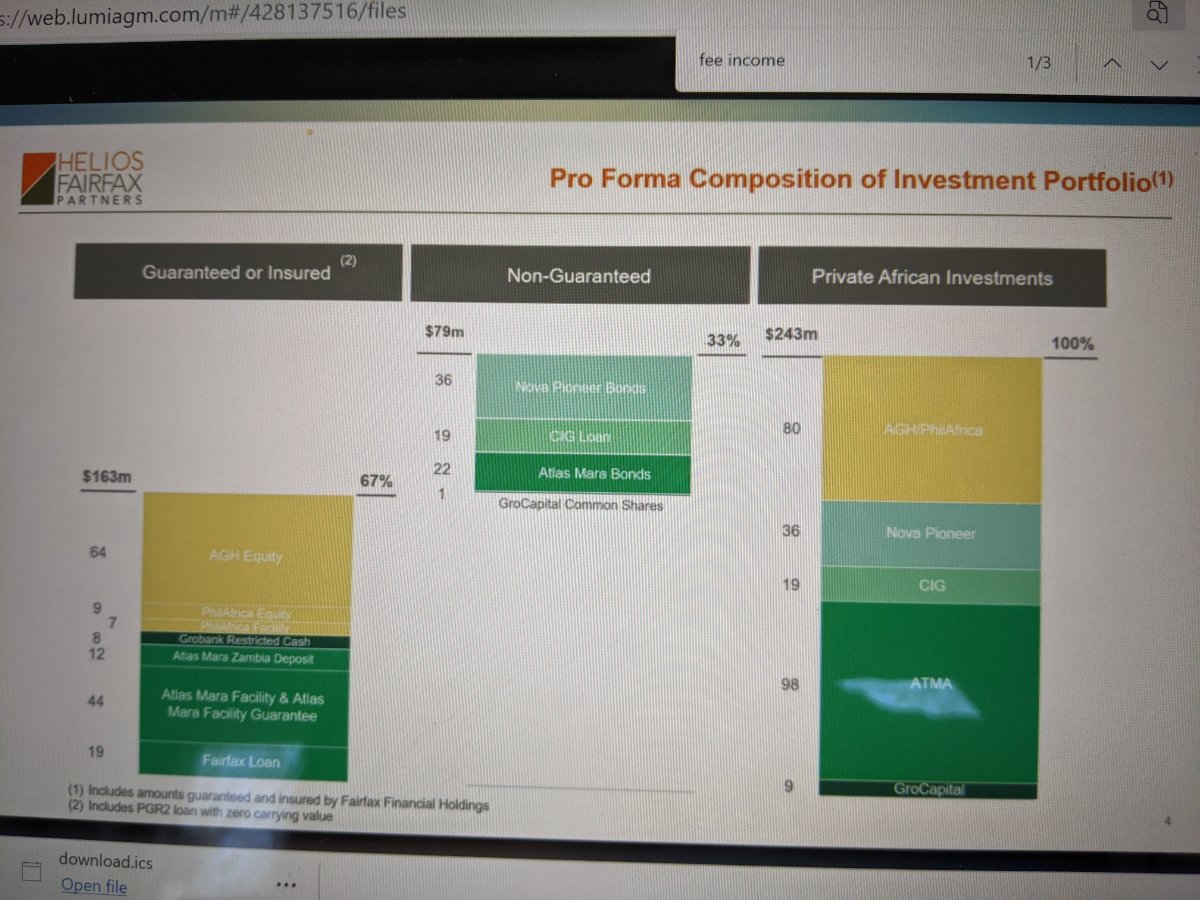

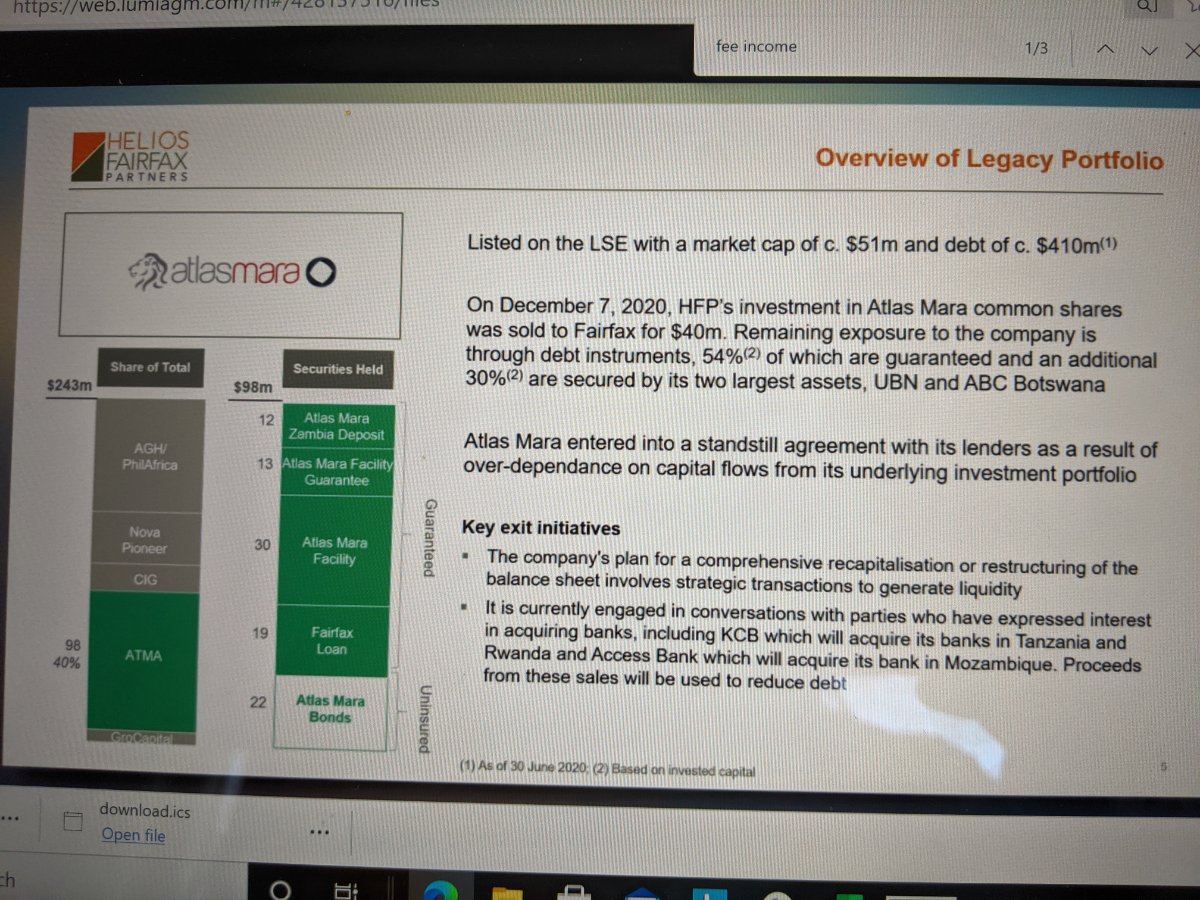

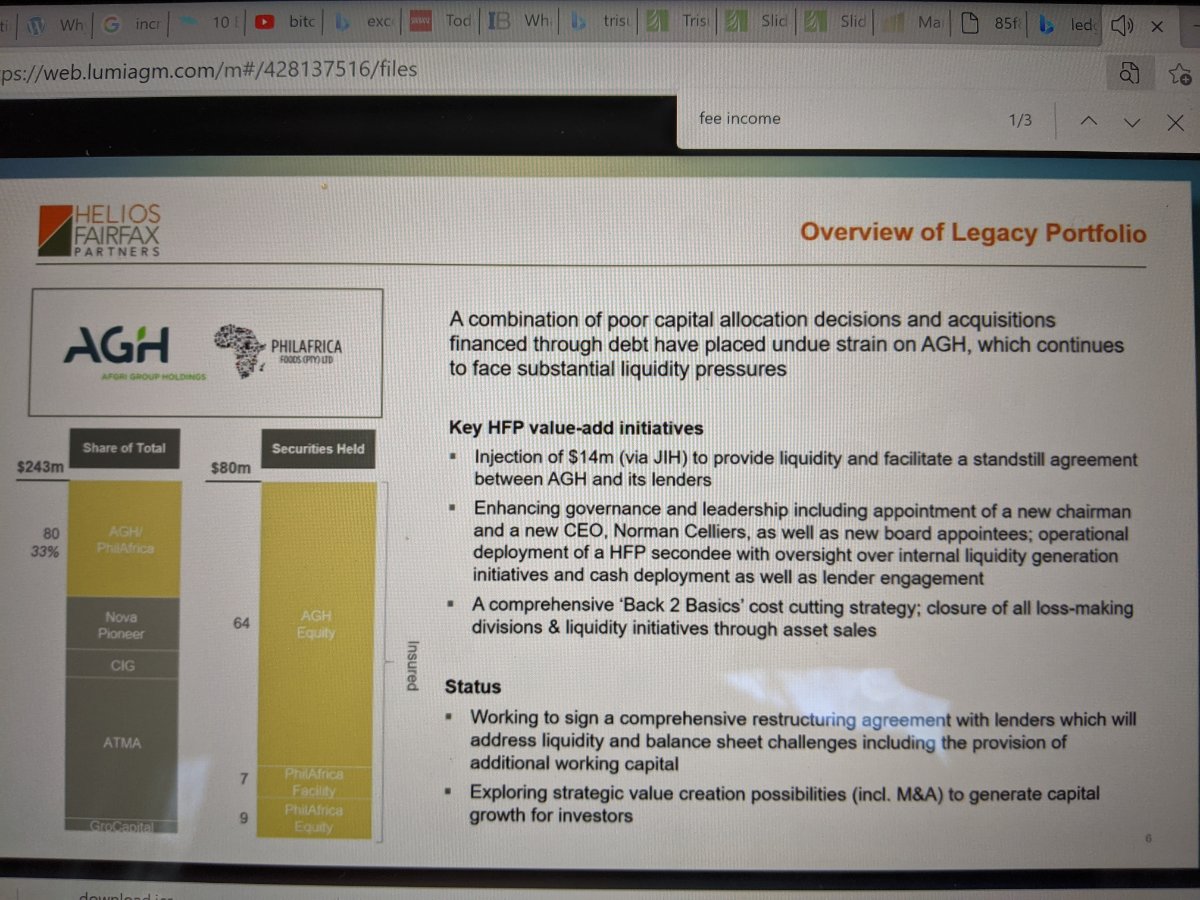

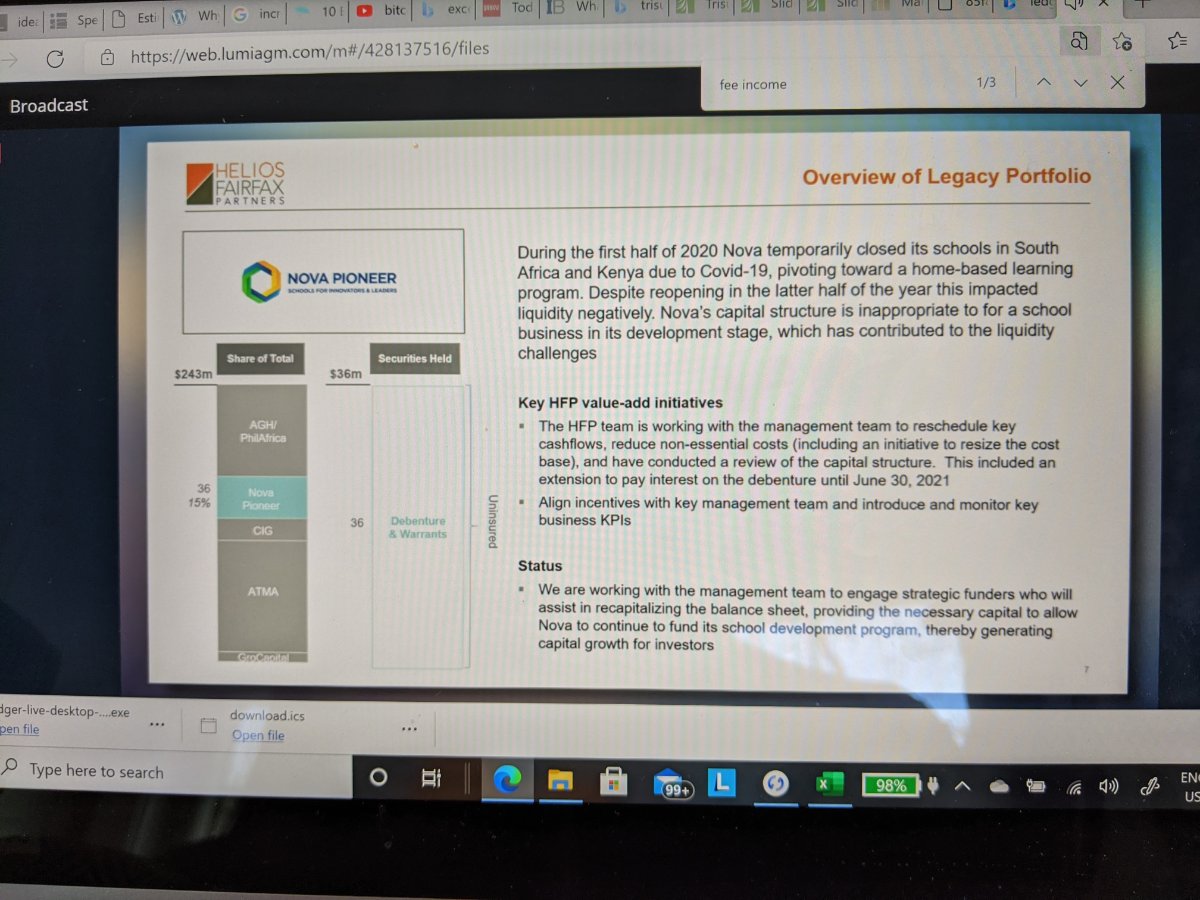

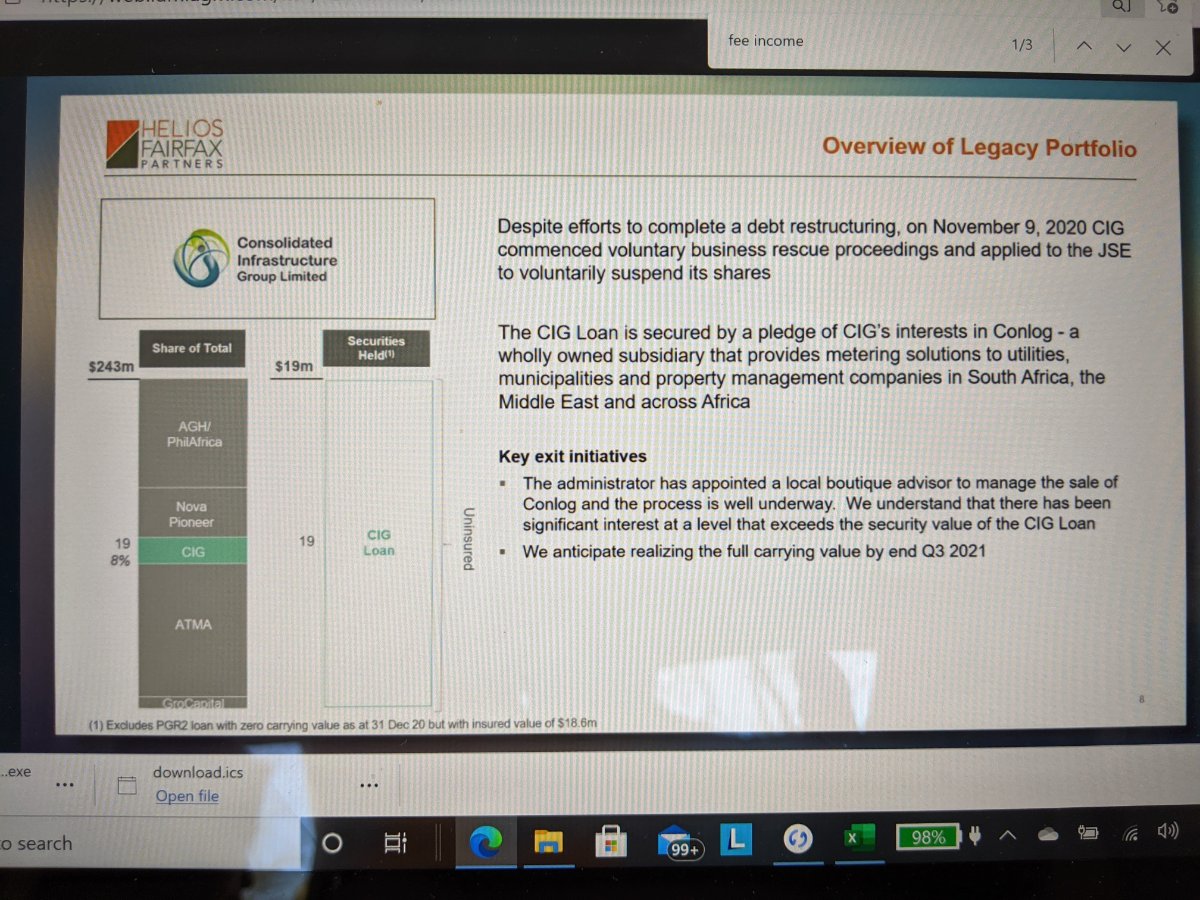

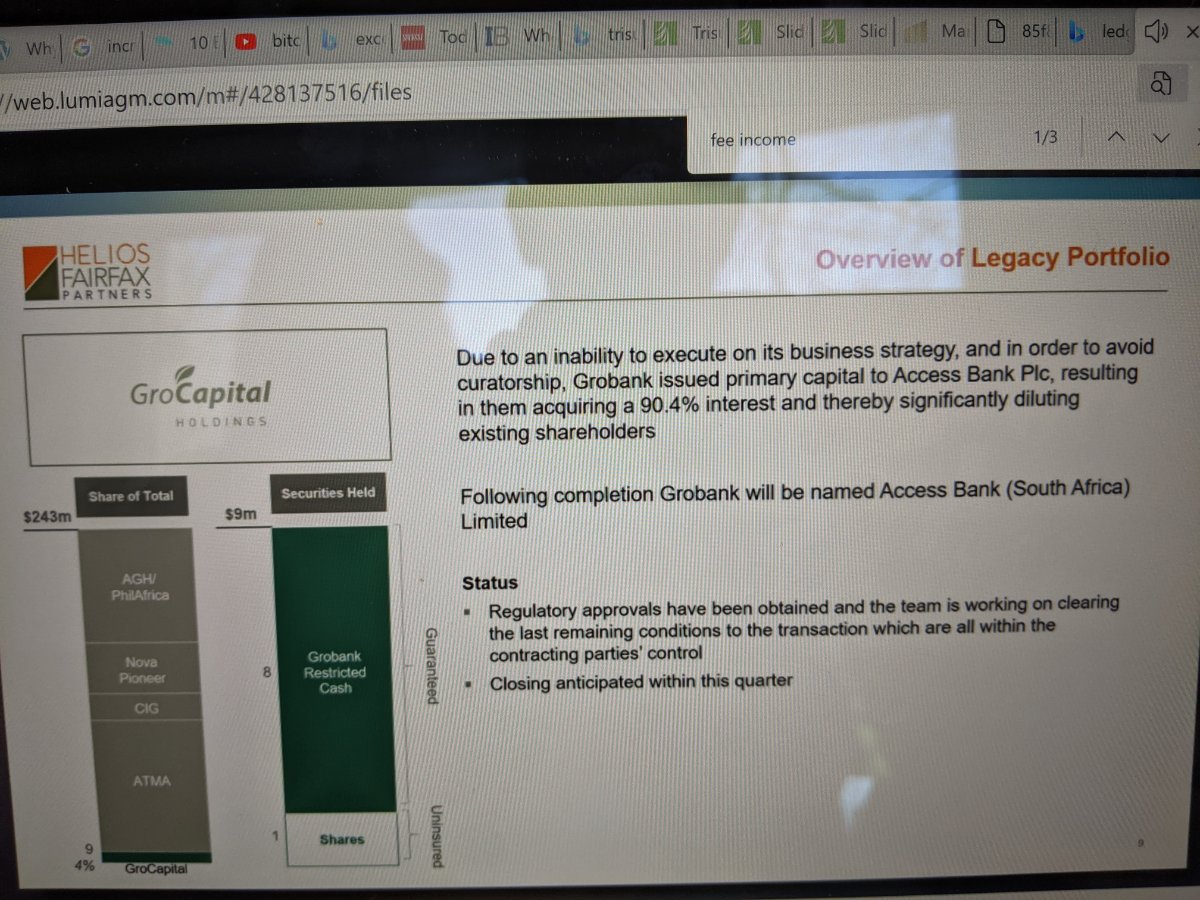

I thought on a Sunday afternoon to glance through their most recent quarterly report. Here are some observations (no specific order). First of, all I can say is what a disaster. Almost all of FAH's legacy investments have been impaired. 1) PGR2 Loan --> written down to zero 2) Atlas Mara 11% convertible bonds --> written down to zero 3) CIG common shares --> written down to zero The following looks ominous: 1) Atlas Mara Facility --> according their their "Models" --> expected recovery estimate 40.7% (down from 71.3%). One saving grace is that the sales of Atlas Mara Botswana to Access Bank subsequent to Sept 30, 2021 allowed them to recover $11,325 out of the original $39,507 loan. The other saving grace is that Helios negotiated a guarantee from Fairfax to cover this mess before merging ("Atlas Mara Facility Guarantee"). The following if you believe them: 1) Atlas Mara 7.5% Bonds --> estimated recovery 99.5% 2) Secured Philafrica Facility (with AGH's pledge of its Philafrica equity interest) --> expected recovery 100% but currently not being paid because it is subordinate to other 3rd party debt 3) CIG Loan (with Conlog equity pledged) has expected recovery of 100% with an "orderly" sales process of Conlog. The following had a small impairments 1) GroCapital Holding Ltd's 9.6% ownership of Access Bank (where the majority 90.4% interest was bought by a publicly listed Nigerian bank validating its value. 2) Nova Pioneer Bonds and Warrants were converted to Ascendant Learning Ltd equity (HFP now owns 56.3% of Ascendant) --> small impairment of the original bonds ($9 million --> small?) HFP has 3% unsecured debentures from FFH totaling $100,000,000. This gets adjusted downward if the reference legacy investments of AGH, Philafrica common, Philafrica facility, and PGR2 loan is lower than $102,600,000. (as above, the PGR2 loan was written off). <-- this is the "HFP redemption derivative" 82.3% of their cash and investments are Level 3 fair value disclosures. The big turnaround investment is in TopCo LP Class B LP Interest. This is the management fee portion of Helio Holding Groups of some of its investment operations. These are their assumptions: - 52.2% pre-tax profit margin, FCF growth of 4.5%, with discount rate of 21.7%. - the current AUM is $2.3 Billion (down from $3.6 billion because Helios Fund I is closing). The 8 year CAGR of AUM is expected to be 18.7%. So they are aiming for ~ $10 billion in future AUM. The other portion is in TopCo LP Class A LP interest. This is the carried interest portion. - They've tightened their target exit multiples of invested capital to 2.5-2.6x from 2.1 - 2.6x. There is some description of Helio Fund investments. Major themes include: 1) fuel distribution 2) electronic payment processing 3) telecom 4) financial services 5) agricultural distribution 6) consumer goods 7) insurance Helios fund IV has 3 investments (consumer good, insurance, and electronic payment processor). Reflecting on this, my past decision making was poor. FAH was an abject failure. HFP on the other hand has a much better chance. At least, I don't think it will go to zero. Just have to figure out, when to incur my losses. That being said, if I was looking at it today, might be worth a small position (aka lotto ticket) for African exposure. Alternatively, could just invest with Helios Investment Partners instead.

-

Random thoughts on portfolio construction for a novice

jfan replied to jfan's topic in General Discussion

I am glad you enjoyed the writing. Thanks for the encouragement. It is very much appreciated. I must admit that, although I believe ancient philosophy and history is full of useful pearls. Both subjects seem daunting for me. But perhaps I'm just afraid of spending time reading, sitting, and thinking because there is not enough action, nor is there an end goal, and its really hard work. The fun thing about the Principles You test is that you can share it with your significant other and compare your similarities and differences. It certainly worth do even if it is for a good laugh. -

I wrote a short substack on some of my random thoughts on portfolio construction for a novice investor. I thought I would share with all you experts. Thanks for your time. https://thequestionableinvestor.substack.com/p/portfolio-construction-part-2?r=981jm&utm_campaign=post&utm_medium=web&utm_source=copy

-

It is on his website. https://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/pbvdata.html

-

Pete Hamblin-Watsa along with the holdco investments and debt +/- any non-insurance businesses (like KitchenPlus? William Ashley?) out of Fairfax Financial the insurance business. It would make FFH a pure insurance platform to which they can access the capital markets with and reduce the complexity of FFH holdco and their investments. Damodaran's price to book value for P&C is currently 1.5. I wonder if this would help the market recognize the value of the insurance business they've built. This would allow the insurance business to expand their surplus since we are in a favorable market at better multiples. Also, Hamblin-Watsa could become an asset manager (if they desire) or use it as a platform to seed other talented asset management businesses (eg Mosaic, BDT capital partners). Broaden the talent pool and investment abilities, new funnel of investment ideas for the insurance companies to put into the portfolio. With a $40 billion investment portfolio, 1% management fee, 80% earnings margin, 20x multiple, it would be worth $6.4 billion less $4 billion debt = $2.4 billion. This might also give them the capability of discarding their turnarounds which undoubtedly consumes alot of time and energy. Berkshire tried buy operating businesses from family and founder operators that didn't require turnaround activity. They could just seed operators like Mosaic and BDT to do it for them. disclosure: as my kids often tell me..."Daddy...you don't know anything."

-

Given the complexity and difficulty forecasting all the volatility, I use a much simpler model to predict as few things as possible. I use their long-term geometric mean for total investment returns (which includes interest and dividends, share of profit from associates, realized and unrealized investment gains/losses and underwriting profits, interest expense, corporate overhead). I know I lose the granularity but with such variability in each factor, I would prefer to reduce the error in predicting each item and be more robust over time. ** The geometric mean since in inception is 7.7% with the most recent business cycle/10 years between 3-4%. This is on a base of $43.2 billion (2020) investment portfolio. This gives a ~ $48 - $125USD/share Earnings attributable to FFH shareholders and Minority interest after paying out preferred dividends. With minority interest at 23%, FFH shareholders own ~ $37 - 97USD/share earnings. Personally I believe it is not a stretch to think that they can keep it at 3-4%, the normalized EPS to FFH shareholders, should be ~ $37 - 50 USD/share. At today's market price, this is about 9-12% earnings yield. Layer on their historical tangible BV per share growth of 2.8% and a median 3.2% stock dilution drag, I think I'm looking at a 9-12% total return. Things I would like to see from them: 1) reduce their debt before buying back shares 2) stop making concentrated bets on deep value turnarounds (recognize that they don't have operational turnaround expertise or be effective activists) 3) Be more like Howard Marks and recognize that value investing doesn't have to be confined to their narrow definition and be more flexible and creative as they can be with building insurance start-ups. 4) simplify their corporate ownership structure and spin-out some of their holdings to shareholders 5) Stop using their shares as acquisition currency ** they have changed their presentation of their average total return from prior years (2019 onward) Viking - thanks for all your granularity and spreadsheets! Much appreciated

-

https://oilprice-com.cdn.ampproject.org/v/s/oilprice.com/Energy/Crude-Oil/Worlds-Recoverable-Oil-Resources-Shrinks-By-9.amp.html?amp_gsa=1&_js_v=a6&usqp=mq331AQIKAGwASCAAgM%3D#amp_tf=From %1%24s&aoh=16262691500785&csi=0&referrer=https%3A%2F%2Fwww.google.com&share=https%3A%2F%2Foilprice.com%2FEnergy%2FCrude-Oil%2FWorlds-Recoverable-Oil-Resources-Shrinks-By-9.html For my confirmation bias

-

Thanks SD. I was getting worried that I would have to get rid of my truck and switch to a Tesla. So forecasting oil prices is a bit of a mug's game. If I could summarize: It ultimately depends on the supply:demand balance. The demand is fairly consistent over time (maybe declining over time) with Electric vehicle adoption. But the supply is driven by nation state politics, the ease to accessing capital, and difficulty finding new supply or squeezing out any extra from producing fields. Nations need $80-90 oil to fund their spend. Efficient producers need $40 oil to be cash flow break-even. I've read a bunch of white papers by Goehring and Rozencwajg. They do a fairly decent job explaining commodity concepts. Are there any other good sources to learn more?

-

Can someone please point the error in my thinking? (I'm not an expert in anything) If the historical relationship between Gold and the total Monetary base is ~ 0.001, and Gold to WTI fluctuates somewhere between 10-30, and Oil to Natural Gas is ~ 10:1. IF we still believe in mean reversion of these relationships, the current Gold to Monetary base is 0.0031 with the price of Gold at $1800. Assuming the Monetary base doesn't contract and stays steady....are we talking about $5800 Gold, $290 WTI (assuming 20:1 ratio), and $29 Natural Gas prices in the future? I know this is a very superficial understanding and ignores all the supply-demand dynamics and geopolitical posturing, but am I crazy that there is an alternate reality where commodity prices might be sky high?

-

Thanks SD for the details. Much appreciated. It will be very interesting to watch how things develop. Owning large areas of land servicing local carbon-producing industries creates the potential captive customers that may need long-term contracts for their carbon credits. They also mention hydrogen generation as a future opportunity both in terms of the commodity itself and the ability to generate CO2 for their oil operations. Do you have a sense of what stage they are at here? Just curious about using blockchain for carbon credits. I came across a few very nascent tokens such as XELS, Universal Carbon (UPCO2), and Climatecoin. How legitimate are these platforms? Found a couple interesting primers: https://www.globalenergyinstitute.org/sites/default/files/020174_EI21_EnhancedOilRecovery_final.pdf https://www.iea.org/commentaries/can-co2-eor-really-provide-carbon-negative-oil https://www.netl.doe.gov/sites/default/files/netl-file/co2_eor_primer.pdf Jfan

-

Thanks SD. Just curious about a few things: 1) does wcp.to already collect carbon credits and are they verified with a 3rd party agency? 2) how long do these carbon credits last before expiration? I know they vary depending on the carbon capture method. With the co2 permanently placed into the ground, will they be indefinite? 3) is it very inexpensive to purchase dry c02 from heavy industry? Thanks for your insights Jfan

-

-

It was interesting how Prem gives alot of air time to his insurance managers to discuss their business segments. Although he gives credit to his investment team, it would be encouraging that he has Wade and Lawrence to speak about their philosophy, learnings as well. I know that Buffett doesn't, but Fairfax isn't Berkshire. Perhaps next year?

-

I was browsing through their website and under corporate it states the Wade Burton is hwic chief investment officer. Has that always been the case?

-

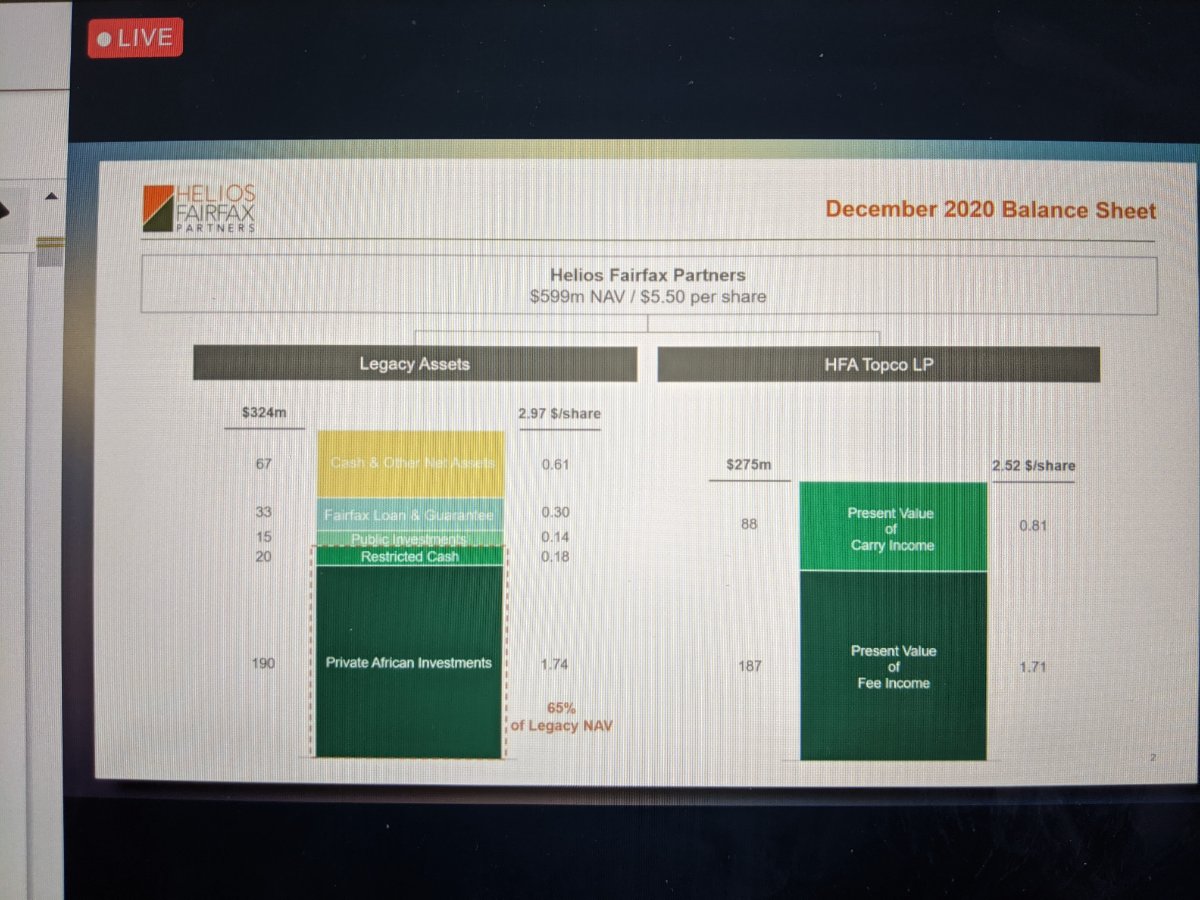

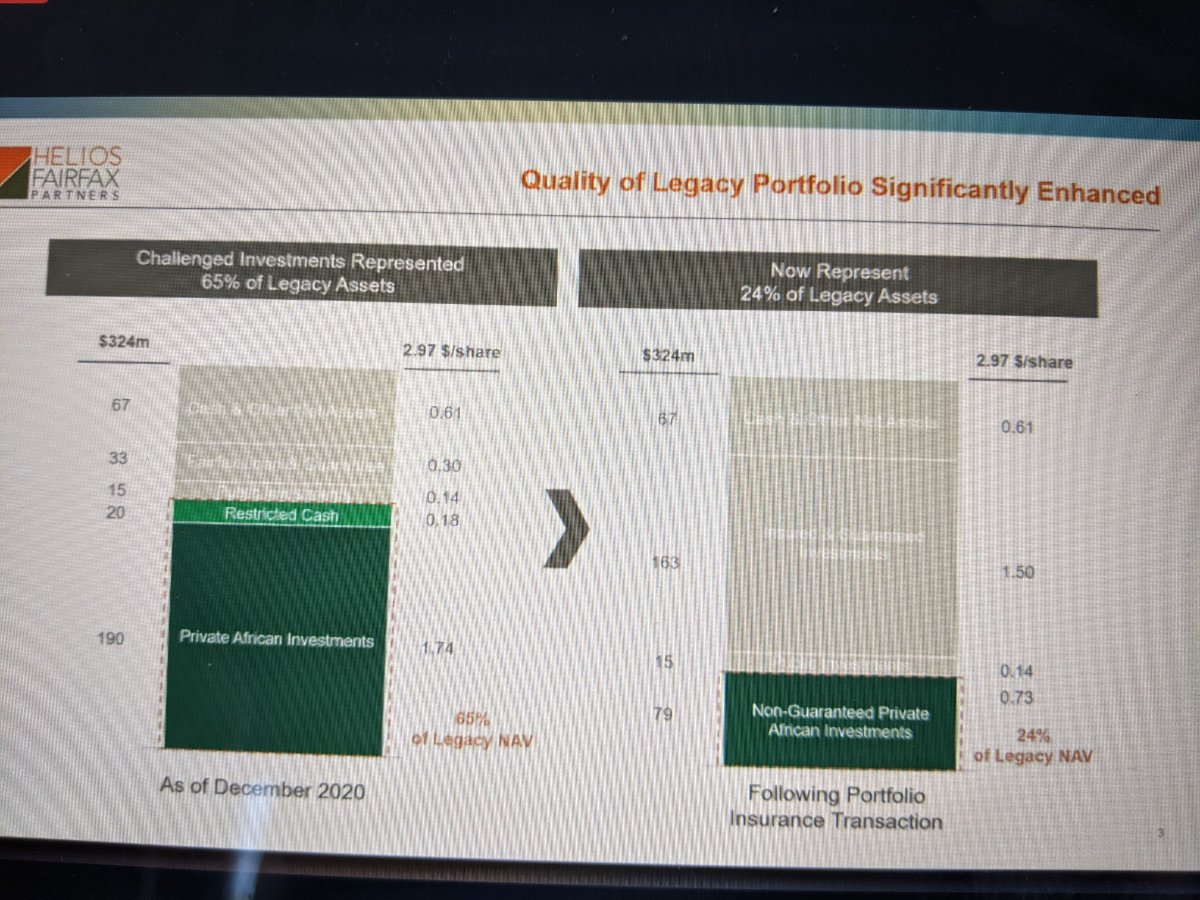

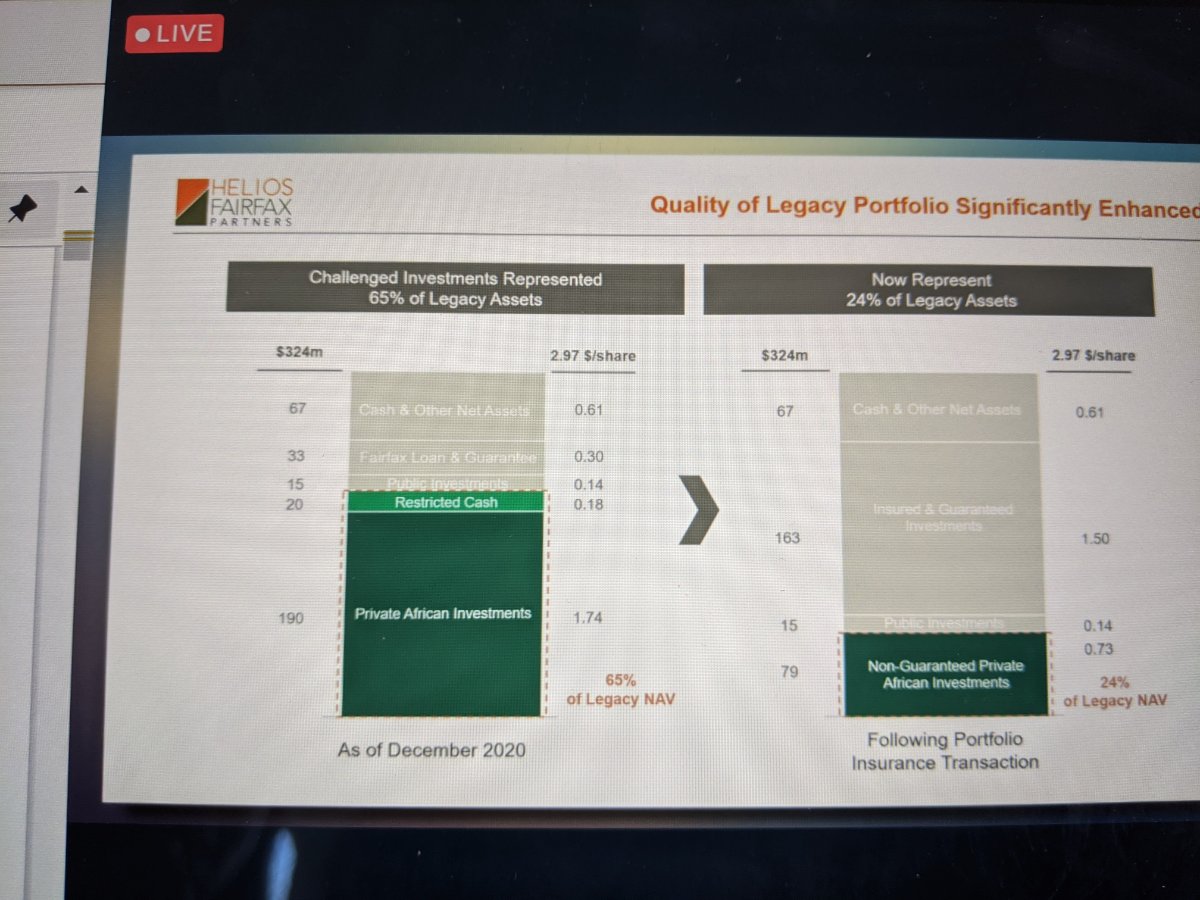

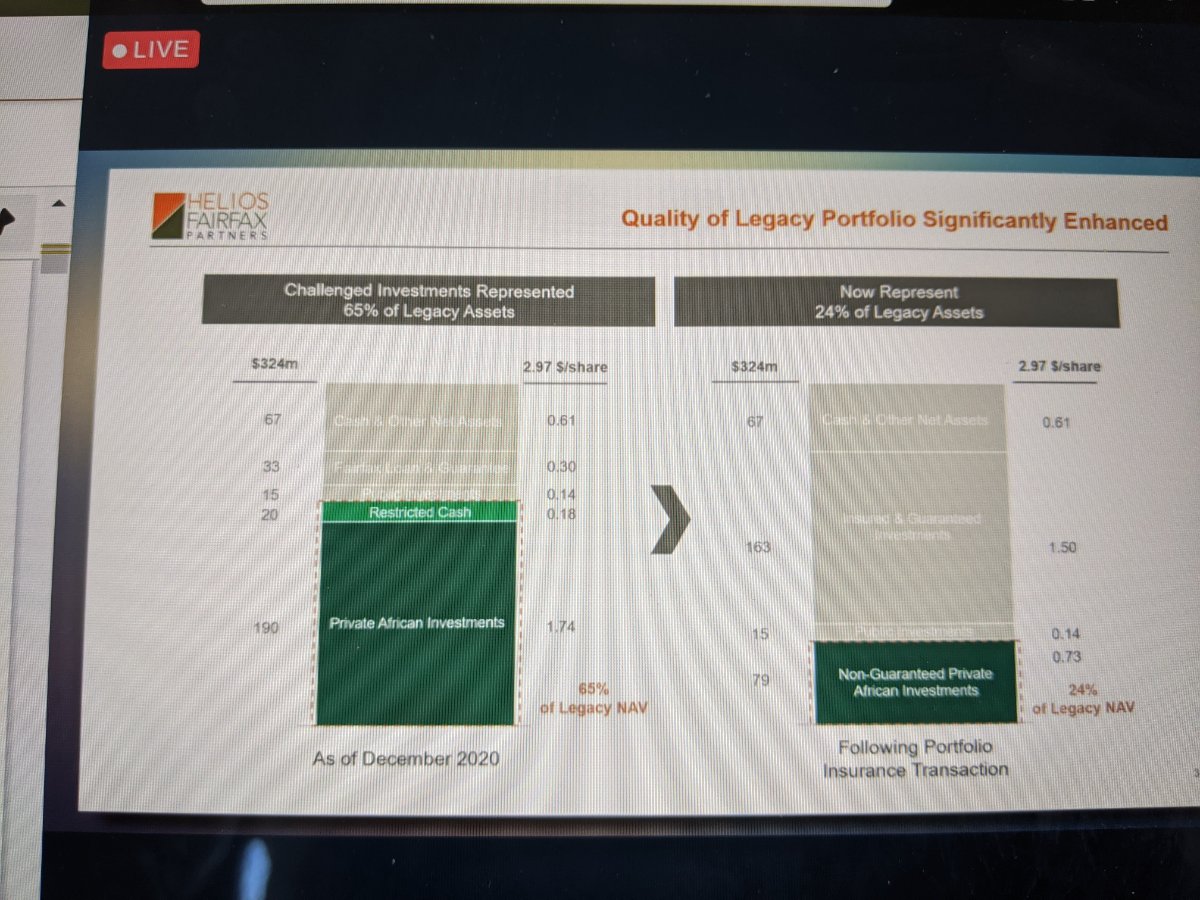

I attended. I think I was the only outside passive shareholder there. Got all my questions answered. I didn't take extensive notes but here are a few observations: 1) These guys are honest and not afraid to openly discuss the poor investments made in the past in the presence of Fairfax leadership. They said prior investments were loaded up too much with debt, poorly timed, and lacked execution. 2) In order to consummate the deal, fairfax had to provide them with insurance to set the floor on asset devaluation from their prior investments. 3) Helios brings in some existing carried interest and fee revenue that they present valued at 22% and 19% discount rates respectively. 4) I asked about the competitive landscape among asset managers in Africa. They said that it was very specific to each country. They prefer to focus on larger economies that may have lower margins. They spoke of how capital flows were very cyclical and many of the larger players are questioning their continued activities there. In their 3rd fund, they looked through 400 potential investments for 12 picks. 75% were proprietary (i guess they meant no other bidders), and of the 25% that had other offers, only a very small # were based on price. Most were based on how the asset manager can add value to the transaction. 5) I asked about stakeholder alignment. They said there are 3 parties. The fund LPs, Helios investment manager, and Helio Fairfax shareholders. Helios partners invest along side their funds (I assume personally) to align with their LPs in addition to their management fees and carried interest. Helios is aligned with HFP by being equity owners of HFP shares. HFP is aligned because fee and carried interest sharing between with Helios and LPs. 6) HFP will co-invest with all of Helio's future funds. In fact, there may be investment opportunities that would not be fitting for the funds but better within HFP's structure. 7) I asked about inflation risk management. They said they are USD return focused and of this currency risk, they manage very carefully. They look to invest in businesses that have the ability to pass on these currency risks and have less import reliance. 8 ) They are looking for secular growth or consumer non-discretionary (not cyclical), growth rates that are multiples higher than gdp, capital light except for situations of high revenue visibility. Sectors of interest include financial services and tech, clean energy and power, telecom/internet infrastructure, consumer non-discretionary. 9) Their portfolio assets now are $0.61/share in cash, $1.50/share in insured and guaranteed investments, $0.14/share in public investments, and $0.73/share in non-guaranteed private African investments. The present value of carry income was $0.81/share and present value of fee income was $1.71/share. 10) I "feel" Fairfax Africa shareholders may have gotten lucky that Fairfax Financial was able to put this one off.

-

How do you see a mine expand their operations without making large costs, exactly? I'm just thinking about the difference between an existing mine that might be underproducing, on maintenance and repair, or has adjacent brownfield expansion opportunities vs a mine that has probable reserves that requires building of infrastructure to gain access to the commodity. With commodity price inflation, wouldn't the first mine be better position to capture profit vs the second that requires rapidly inflating capex and thus be less valuable?

-

Does this depend if the asset (mine) is already existing and needs less cap ex to expand in the future vs an outdated asset that needs significant upgrading?

-

What a great discussion. Thank you for all the perspectives. This year has been a interesting/painful/hopeful experience in understanding the importance of position sizing and its effect on your portfolio. I think when it comes to position sizing it depends on a bunch of additional factors: 1) Past stock picking skill/experience that in turn depends on ability to make good decisions, process information, ability to see around the corner, mentorship, team-based vs individual-based work, full-time vs part-time 2) Recent performance - Druckenmiller in an old interview gave advice that when he had a poor performance streak, he would size down future positions to regain confidence. I suspect that he recognizes the possiblity of poor cognition or bad investment framework 3) Ability to exert control/influence the direction of the business 4) Illiquidity - I think taking large positions in illiquid investment requires a little bit of all the above or a huge degree of trust in the management of the underlying business 5) Personality - Do you enjoy high risk or are you risk adverse? Are you holding on in the volatile times because you are confident vs feeling like a deer-in-the headlight? Can you stomach the pain on selling out a large losing position after a period of under-performance? What is your time-frame preference (ie can we hold something for 3-5-10-15-20 years)? Just some of the questions I had to ask myself.

-

What resources do you use and what kind of investing method?

jfan replied to Arski's topic in General Discussion

Being in a similar situation, I would say that it depends on how this hobby is going to fit in your life/regular work. More important than the source of information is your strategy of how you are going to learn. Concentrated investing in small caps requires lots of working knowledge of the industry, a track record of correct thinking, and lots of time monitoring the situation +/- access to management. In the beginning, the best approach (after making plenty of mistakes and not listening to experienced investors coupled with an ego) in my opinion, are small bets across a continuum of styles with a structured investment process to evaluate how correct your thinking is with a 3-5 year holding period. The rest of your portfolio, just dollar-cost average in a index are regular interval. It is most probabilistic that you will have more FOMO and action at the beginning, and I would use this tendency to learn on a larger case series to inform your future self. Once you prove to yourself that you can learn from your mistakes and successes, then re-evaluate your style. The appeal to concentrated investing is you don't have to track a large number of positions, but you have be damn sure you are right in the end, you can handle the volatility, possible long periods of underperformance, and have the ability to track the right things to inform your holding. If you aren't in the industry and willing to dedicate hours analyzing, scuttlebutting, talking to management, it is probably better to have smaller positions, extremely long holding periods, learning a bit of technical analysis to placate your trading tendencies, and diversifying across very deep value <--> growth styles (or Peter Lynch's 4 different buckets). -

Gbtc

-

Appreciate your thought processes on this. I don't know if this is the right way to think about it but here is my logic. Single customer in Y1 and Y2 provides $120 each year. Assuming that after year 2, it becomes an annual subscription renewal option with a 10% churn rate (ie 10% chance of losing them as a future customer), the expected revenue in Y3 ~ 90% x $120, then in Y4 ~ 90%^2 x $120, and so on and so on. After 10 years, the probability of this customer remaining will be ~ 35%, with an expected revenue of 35% x $120. It will take until year 25, for the probability to drop down to 7%. Taking this expected revenue stream, I discounted it back to present value (10% discount rate), which would give me a present value of ~ $600 for this single customer. Assuming that there is no significant CAC, and the net profit margin once stabilized is 30% (you are right, will likely be much lower if the gross profit margin is 50%), each customer would generate a present value of ~ 30% x $600 of value = $180. If the payback period is 1 year, then the CAC will ~ $120 and the value per customer would drop to $144 or [($600-120)*30%] (This number is an over-simplication as it doesn't account for growing cash flows with increasing deferred revenues, maintenance R&D, S&M to update software versions, subscription vs usage revenue models) So in 3 years, with 100,000 customers, $180 * 100,000 = $18 million of value on $12 million of revenue or $3.6 million of earnings on a 10% churn rate. It would be more valuable if they can reduce their churn rate over time (if they can drop their churn rate to 0%, then maybe you can think about a value of 10x $3.6 million earnings = $120/0.1 *30% x 100K customers = $36 million) If there is a possibility that the churn rate increases significantly after Y3, then the product is no good, led by an incompetent management team and it would become un-investable. SAAS should be inherently sticky because it allows businesses to see how their clients are using them and give them the ability to layer on needed/desired features. If they can't do that, then trying to sell their poorly functioning intangibles is likely an impossible task. Figuring out their growth rate is more difficult and probably more qualitative than quantitative. This is where I think about the quality of leadership, focus on experimentation, innovation, solving difficult problems, customer focus and delight, open source innovation vs proprietary, degree of industry collaboration, ability to not only grow vertically in their software stack but also to adjacent markets, ease of customer adoption, organizational structure, very large TAM etc. So if I can buy it at $18 million discounted back by 7.5-10%, or at $13-15 million today coupled with a judgment about their ability to reduce their churn rate and skill to grow in a manner that it unexpected (via the above qualitative features) as the free option beyond year 3. Then there is a greater probability of having a reasonable return. (aka Shopify --> Shopify Capital, Amazon --> AWS) Welcome any push-back on my logic.

-

CCO.to

-

I'll take a stab at this: Assuming for each customer, the first 2 years of revenue is $120 each, with a 90% decrease after that. It would take ~ 25-30 years to lose that customer. The PV10 for a customer would be ~ $600. If in 3 years, there are 100K customers, the approximate value (using 30% Net margins) of the business is $18 million. This # doesn't account for any customer acquisition costs. If my personal hurdle rate is 10%, then the max value I would purchase it at would be $13 million or 11x current sales. To make the math easier, I would eliminate it (deal-breaker) if there is a potential of increasing churn rate after year 4 by filtering out maligned management teams.