Cigarbutt

-

Posts

3,473 -

Joined

-

Last visited

-

Days Won

1

Content Type

Profiles

Forums

Events

Everything posted by Cigarbutt

-

Probability that covid will become endemic

Cigarbutt replied to LearningMachine's topic in General Discussion

Small additional comment. Assuming a virus evolution over a few months is a long enough window for adaptation and evolution to play out, efficiently killing your host is clearly not an 'advantage'. With the Spanish Flu episode, what killed the host was typically a secondary bacterial pneumonia, as a side effect of the initial virus invasion and before antibiotics were widely available. The particular matter with Covid-19 is that, like other 'successful' viruses, it is efficient at alluding the human immune system but it is also able to inhibit and delay the immune response in a way as to cause an unfortunate side effect related to this delay, in certain people, resulting in an exaggerated and delayed immune response that is out of proportion to the invader and that kills the host through some kind of self-inflicted immune storm. Of course, the virus does not really care about this unfortunate side effect in some people. This sentence is heavy with 'meaning'. Our investing styles are different. i tend to go for focused and rare bets, for opportunistic and easy killings in a way. This requires to reach a level of confidence equivalent to being able to challenge the CEO or Board. Despite this, there's always an impostor's syndrome involved which, i guess, must be felt by all who try to define their evolutionary circle of competence. -

Probability that covid will become endemic

Cigarbutt replied to LearningMachine's topic in General Discussion

Interesting question. A controversial one though as the origin of viruses is, itself, a very controversial topic. Viruses like coronaviruses mutate less than the typical viruses but it still provides an accelerated version compared to DNA organisms. Because of frequent replications, it's probably best (evolutionary standpoint, to 'survive') to keep a dense set of genetic information and to have genes involved simultaneously in multiple characteristics. The result is that mutations are very likely to be deleterious (the new variant disappears rapidly). Typically in viruses, it's very rare that the contagiousness or virulence do change significantly during a spread. Covid-19 is unusual because of the law of large numbers. Still, the significance of the vast majority of mutations is only to be able to track origins (signature of the virus). Everything is possible but the vast majority of isolated mutations are unlikely to change virulence (many genes involved) and unlikely to rapidly introduce significant changes in contagiousness (it seems there are some variants of that nature out there for Covid-19 because of the global spread and incredible number of replications). i would say this is just good or bad luck on very low odds and not from an evolutionary plan that would take longer to accomplish. From a purely evolutionary perspective, the best scenario would be to increase contagiousness and to decrease virulence but, because of the factors mentioned above and because of the ongoing process to quasi-herd immunity, this is unlikely to play out significantly. The large six-sigma squared event was when a mutation (or lab event?) opened the possibility to jump species. This is an area where humans can have an impact (positive or negative). i would offer the opinion that, at this point, the likelihood of a more virulent virus is higher from a new event at the source than as a result of an evolutionary process of Covid-19. In his book La Peste, Camus said it well (just like bear markets): "Everyone knows that pestilences have a way of recurring in the world; yet somehow we find it hard to believe in ones that crash down on our heads from a blue sky." ----- This post is quite useless for an investment board. So, here's an investment-related analogy for the virus mutation question. In 1998, Larry Page and Sergey Brin started to work in a small garage and developed a product that spread and gained market share. Let's say you switch one of the two co-founders for any member of this board, or even most other citizens in the world, you may end end with a more contagious product or a more virulent competitor but it would be highly unlikely. The initial mutation was the key one. i hope that makes some sense. -

^This trend ('tech' driven) is quite revolutionary for Lloyd's where tradition still relied on trusted person-to-person interactions. Even if 'fancy' words are used, this is basically a way to modernize and make interactions more efficient, attracting alternative capital (and fees) along the way. The 'lead' underwriter still does the technical work and the complex risks will still require personalized attention but the 'follow-only' syndicate can efficiently match the more commoditized risk products to alternative capital looking for uncorrelated (and reasonable) return. For some more information on foundational work, intent, process etc, write "Quarterly InsurTech Briefing Q3 2020 - Willis Towers Watson pdf" in Google, download the document and see pages 27-28.

-

Noice ;D Is this where that came from? www.amazon.com/Money-Game-Adam-Smith/dp/0394721039/ref=cm_cr_arp_d_product_top?ie=UTF8 The question is for thowed but i enjoyed that book a lot. Also, when one doesn't want to play the game, it's probably best to shut up. Despite the above and despite the humility required, here are a few comments. ----- The quote comes from chapter 17. Losers and Winners: Poor Grenville, Charley, and the Kids. The book was released in 1967, at a time when an investor dear to our hearts was also wondering about the Game. It deals about many topics (mostly temperamental), including the gunslinger attitude. Billy the Kid figured out that the older generations had "trouble figuring out the New Math, the New Economics, and the New Market." There are some who can figure it out but at times "the market does not follow logic, it follows some mysterious tides of mass psychology." Is 2021 a repeat of previous 'episodes', including 1999 and the go-go years? Who knows? The easiest way to deal with this is to ignore it and focus on individual names (and shut up about wider implications). There are many independent indicators that suggest that today's market levels are elevated (levitated?) and it appears to me low interest rates is an insufficient and perhaps a contrarian indicator. The other aspect (as Spekulatius and others mention) is that bubbles can only be identified in retrospect and catalysts are only defined afterwards. Also, what we don't know is what's in store. The chapter also has a small part on this aspect, describing how earnings projections are lagging indicators. That's why the 1930s was such a rough episode as markets started relatively elevated and had to adjust to very poor fundamentals and "the insecurity of anarchy." Below are two graphs showing how dependent we are about future developments and how projections can sometimes meet the pavement: The author concludes the chapter with a "final indicator" which does not need to be included here and is best summarized by part of the last sentence of the chapter:"emotions are universal and there is no stopping the flow of seasons."

-

Probability that covid will become endemic

Cigarbutt replied to LearningMachine's topic in General Discussion

The Rockefeller 'scientists' produce solid work but the sample is small. In short, this is something that needs to be monitored for non-linear changes (unlikely) and, even with some delay, vaccine makers are equipped with relevant experience to modify vaccines accordingly. Taking a wider perspective, this 'new' (entering an immunologically naive population) virus (and minor variants) is having an unprecedented opportunity to circulate (and to mutate). What is surprising (and comforting) is actually the relatively low amount of genetic drift (compared to other viruses). This Covid-19 thing suffers (at least so far) from a lack of genetic diversity and this is another factor that supports the hypothesis that it will become a relatively low-grade endemic problem (and likely less of an issue than the flu over time). The following discussed that aspect: https://www.pnas.org/content/pnas/early/2020/09/18/2017726117.full.pdf Figure 1 is worth a thousand words. ----- This post is pretty useless for an investment board. So let's use an analogy. This virus will run into difficulty (spreading and causing harm) the same way a company that has introduced a popular product maintains an echo-chamber type Board of Directors with little capacity to adapt. -

^i think the Treasury is in charge of the strong/weak dollar policy although 'discussions' can happen with the Fed. The Real Trade Weighted U.S. Dollar Index: Broad, Goods and Services is usually used as a benchmark. In the end (or at the margin), it's mostly a matter of confidence. Recently, i went through a KKR presentation and they had the following: They seem to expect a decline in relative value of the dollar (based on the fiscal deficit) but there are so many factors. They also showed this: How can you know you've gone too far if you haven't gone too far? Disclosure: i'm presently working with the assumption that the USD will remain, relatively, a strong currency.

-

The following is anecdotal, so of limited value. i've recently peripherally participated in online discussion pockets (university 'friends' of my children) related to investments (the students sound bright in general but are not studying and have limited fundamental knowledge about investments). The last discussion centered on how 'cheap' stocks tended to do well and the discussion helped surface the real definition of a cheap stock: a cheap stock. And there's even recent evidence to show for it (!): Our job is to fundamentally discount future cash flows. How does one reflexively discount marginal participation?

-

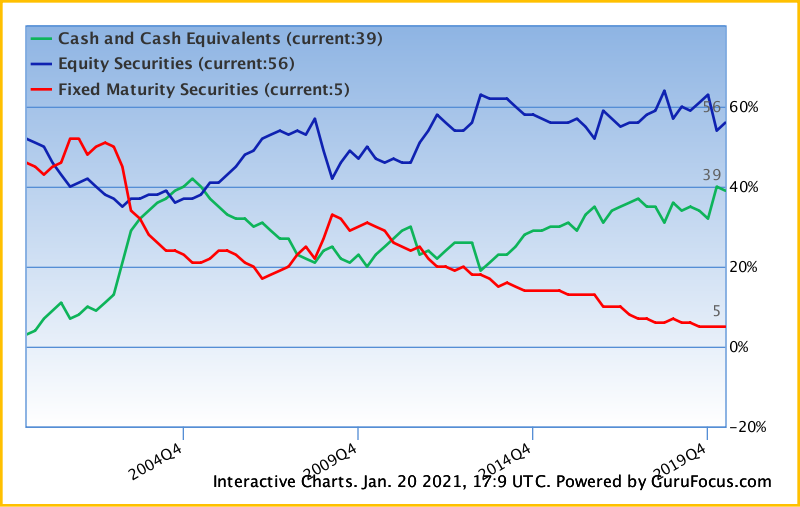

Another way to look at this -- they converted their long duration bond portfolio into a set of income producing real assets at BHE and BNSF. The yields are better and the risks are better than long duration bonds at this point in the bond market cycle. Further, based on Christopher Bloomstran's deep dive, they used the accelerated depreciation credits at BHE and BNSF as a secondary method of reducing tax payments and increasing cashflows. As well, based on Brooklyn Investor's charts, they have built up a large cash component in their portfolio to backstop insurance losses and to provide optionality for opportunistic acquisitions. This is not all black and white but the big asset allocation shift of the last ten years (see attached) has been the movement of funds from longer term fixed income to cash and equivalents. This movement raises two questions (the indirect one raised by wabuffo and a direct one). The indirect (and retrospective) one: Returns would have been better if the longer term fixed income portion would have grown proportionally to float. The direct one: Does the current (and growing) allocation offer potentially significant optionality value? (my answer is yes)

-

That is interesting and favorable for constructive discussions. The perspective covers many aspects that have been discussed here. Perhaps Sweden should be compared to Nordic neighbors instead of the UK. Also, the "laissez-faire" strategy remains, to this day, ill defined. Places where 'minimal' restrictions were applied typically showed relatively similar declines in mobility and social interactions and typically reported similar economic declines (costs). It has been very difficult to assess the cost of heterogeneity of response to various suggested or mandated restrictions. A few super-spreaders could negate the adaptive behaviors adopted by thousands. ----- The following is submitted as food for thought. (Relevant references for those interested found below) When evaluating the value (cost vs benefit) of various interventions, the concept of quality-adjusted life-year (QALY) can be used. It is felt these days that developed societies deem 50k per QALY to be an acceptable threshold. Using the numbers reported by Mr. Webb and others, it can be guessed that people who died of Covid each (on average) lost about 4 to 5 QALYs. One needs to guess also the QALYs lost as a consequence of surviving Covid even if it meant hospitalization, intensive care unit stay, respiratory support etc. Using the 50k per QALY 'benchmark', one comes up to a significant amount of potential funds (per capita) that could have been 'invested' to prevent QALY loss (per Covid casualty). For those who say that something like half of deaths were half dead anyways (basically true but you have to remember that we're all dead in the long run), under present social compromise, a massive amount of healthcare dollars are presently 'invested' in the very sick and the very old with very little to show for it. i don't have studies to prove it but it is safe to say that the investment of healthcare dollars presently 'invested' in older and sicker patients is much much more than 50k per QALY.. Below is an example of this application (i'm more confortable with joint replacement numbers but the study is interesting for many reasons). Basically, it's about the cost-benefit related to prostate cancer and various approaches (i gather that Mr. Webb announced in 2020 that he had metastatic prostate cancer and the use of this specific study is only coincidence). Whether socialized or privatized (anyways in the US, Medicare has become basically the only game in town for the 65+ population and related 'investments' in the last few years of life), the idea is to figure out what the mutualized payer is ready to pay vs the expected benefit. https://en.wikipedia.org/wiki/Quality-adjusted_life_year https://www.nice.org.uk/Media/Default/guidance/LGB10-Briefing-20150126.pdf https://www.ncbi.nlm.nih.gov/pmc/articles/PMC7026676/

-

i don't know. That's what i'm trying to figure out. :) Outside of personal proprietary stuff, here's a graph that is quite representative. Note that by including or excluding some insurers (or some specific lines), one can get a slightly different pattern. Also note that, using the US (re)insurance industry as a proxy, total loss & LAE reserves have increased by about 15% over the period. This has been a mostly unusual soft cycle and the reserve release pattern of the last few years has been a very unusual and long-lasting contributor to insurers' bottom line. As far as FFH is concerned and for this specific aspect (reserves and hardening cycle), one should hope for a massive negative development pattern because (IMO) FFH likely would show a relatively better pattern and this negative development would help to sustain the hard market and would allow significant market share (and float) growth during a period where policies are written very profitably.

-

^So could BRK have done better by ‘managing’ duration in its fixed income component of float? This is a relevant question going forward, whoever is in charge of capital (asset) allocation as the present posture can be seen as a drag or as an optionality feature. Thanks to Brooklyn Investor: The asset allocation in BRK’s fixed income ‘portfolio’ has been very unusual. Longer duration exposure has remained minimal up to the last quarterly report. It’s interesting to remember that BRK, when it acquired General Re in 1998, acquired a portfolio of longer duration fixed income securities (mostly non-taxable munis) valued at about 24.6B (if my numbers are correct). So, what about BRK’s fixed income duration strategy? Here’s a (borrowed) table showing the return on the fixed income side for insurers at large over the last 10 years: 2019 2.4 2018 2.2 2017 2.3 2016 2.0 2015 1.7 2014 1.8 2013 3.1 2012 2.6 2011 2.4 2010 3.3 Added below the table are the results (%) for RNR (which happen to be on my working desk now). When assessing the fixed income side of (re)einsurers’ portfolios over the last 10 to 20 years, several tentative conclusions can be reached: -yields are coming down, absolutely and relatively to the 10-yr yield -managers have not used duration to increase yields -managers have moved up the risk ladder (yield searching) -it’s no fun to manage the fixed income side of float -Mr. Buffett has achieved, at this point of the underwriting/investing cycle, a lower return than the industry ‘benchmark’ (especially since 2014 with the growing cash pile earning basically 0%) So, could BRK have done better with duration? Maybe. But: -Mr. Buffett was always clear that he viewed longer term fixed income as poor allocation. -FFH which has played the duration game with positive results has reported, at best, a mixed picture with ‘macro’ calls in the last 10 years. -The whole industry at large has not exploited longer duration fixed income opportunities. For example RNR, despite a progressively longer insurance reserves duration with acquisitions started with an effective duration of 3.2 years in 2010 and reported a duration of 2.9 at 2019 year-end. It’s also instructive to look at a previous kind of cycle (leading to the housing b****e). As an example of the insurance industry’s investment income pattern, here is what RNR reported (net investment income over total investments, %) for the 2003 to 2009 period: 2003 3.1 2004 3.4 2005 4.1 2006 5.0 2007 6.1 2008 0.4 2009 5.2. An argument could be made that BRK ‘lagged’ leading up to the 2007-9 episode (it’s hard to derive the exact yield on the fixed income part because of the way BRK reports) but the opportunistic use of cash during the last part of the phase to buy fixed income-like instruments at very advantageous terms largely made up the difference and more. I think it was possible, in the last 10 years, to produce investing profits by playing the long duration game (even with ‘risk-free’ instruments) and there may be an ultimate puff left but humility suggests to wait for a full cycle (whatever that means as the new to-be Treasury person who used to promote Fed put instruments has suggested that true financial crises are a thing of the past, at least for this generation) before reaching the conclusion that there is little comparative optionality value in BRK’s fixed income portfolio and that Mr. Buffett has become passé.

-

In case somebody is interested: https://science.sciencemag.org/content/early/2021/01/11/science.abe6522 Warning: Not exactly as entertaining as a NY Post article. TL;DR: -"They" use 'models' and some of the underlying assumptions are questionable but there are a few interesting messages (absent a significant and unexpected mutation pattern). Their review of previous knowledge about other CVs is very strong. -This virus was very unusual in the sense that it entered a globally immunologically naive (virgin) population. -CV is likely to become endemic and is likely to concentrate in younger cohorts. -The vaccines are likely to speed up the process to endemicity. -The authors suggest the possibility of (eventually) using other waves of seasonal vaccines to older and other at-risk populations and to allow the virus to spread in the young, an interesting possibility based on the specific attributes of Covid-19 vs other CVs, the flu etc. once the population is no longer naive (immunologically speaking). There is still a lot to learn but virologists are bound to become nobodies again during 2021.

-

You are using the assumption that reserve releases will continue at the sub level. Why is that? There is also a reserving cycle which historically correlates quite well with the underwriting (soft and hard) cycle. What is interesting is that the reserve cycle typically crystalizes over time (especially long tail lines) and the correlation can usually be made only in retrospect. It would probably be reasonable to base the capacity to grow at the sub level based on investment profits at the sub level and financial flexibility at holdco. If interested, look at the hard cycle that happened around 2003-2006 (and the preceding soft part): Note that it took many years for the large amplitudes to develop.

-

"You don’t have to fight about everything you disagree with. Fight when it matters, and when you do fight, make certain you can win."

-

Let's forget about sunk costs (argumentative and otherwise?). How can we learn from the Dakotas? It seems they are focusing on healthcare workers first, with a slight adaptation from the 'national' guidelines. One could argue for or against that modification but it appears that frontline workers have been going through a rough (mostly bipartisan) patch (especially in the Dakotas). i see that the protocol in North Dakota includes to vaccinate people who, themselves, vaccinate others (again another area to argue). i assume you are from Ontario. As you know the neighboring other-solitude province has been reporting terribly high numbers (cases, hospital capacity, deaths etc). Well, despite this previously sunken past, it looks like the vaccine rollout is evolving relatively well: https://covid19tracker.ca/vaccinationtracker.html Word has it (as of 2 days ago) that, in my province, 50% of elderly people living in the most at-risk homes (the "CHSLDs") have received their first doses as well as 25% of relevant frontline healthcare personnel. (irrelevant addition: i'm periodically giving a lending hand to push the plunger but will wait my turn according to national guidelines)

-

"Happy states are all alike; every unhappy state is unhappy in its own way" (slightly modified Anna Karenina principle) https://www.statista.com/statistics/1109011/coronavirus-covid19-death-rates-us-by-state/

-

^NY and IL have entered the vicinity of functional herd immunity with vaccines coming. In NYC, positivity rates have levelled and are recently trending down (but still high). IL and the Chicago area had a huge second wave that peaked in late November and early December and all numbers (cases, positivity, hospitalizations and deaths) are significantly trending down. In my jurisdiction (CDN province), it appears that only a small minority (less than 1-3%?) of vaccines are given to people not belonging to pre-defined priority groups. In my jurisdiction (like elsewhere including the US), there is a clear movement to move away from the pre-defined two-doses regimen in order to postpone the second dose with the goal to reach an optimal number of people with the first dose. This outcome has been the result of constructive discussions between people sitting in offices and people on the ground with some kind of expertise. There is some uneasiness with this adapted strategy because the vaccine studies were devised with a fixed schedule. However, at the group level, this is likely to help reach herd immunity faster. Looking at the groups at risk in the next few weeks (similar to a threshold analysis in a bankruptcy according to priority rules), the sub-groups most likely to benefit will be the 60-69 and 70-79 living in the community. These two groups compose lower proportions of people reaching hospitals, ICUs and the morgue but numbers are still significant and this group is clearly at risk for quality-life years lost. At the individual level, postponing the second dose has positive and negative aspects. The negative aspects include that this adapted protocol was not studied and means that there will be less protection in between doses. The positive aspects include that efficacy reaches about 90% with the first dose at day 14 to 15 with the mRNA vaccines, immunity has been shown not to decline significantly for a few months and, from previous vaccine knowledge, a delayed second dose may very well result in a stronger 'boost' (longer lasting immunity).

-

^The following is useless for stock picking. It may be food for thought though for the following academic question: WTF is going on in today's markets? https://www.factorresearch.com/research-improving-the-odds-of-value-ii TL;DR: Minding the usual limitations about how to measure 'value', the author suggests that, usually, typical contrarian value seekers of the bottom seas will tend to struggle when interest rates are flattening. Article published before the very unusual 2020 year. In theory, with the yield curve steepening, the typical 'value' investor should be recomforted but: 1-the 30-yr rate is only at 1.87%*, 2-the 10yr-2-yr the author uses is at only 0.99% now and 3-real rates have had a tendency to be more and more negative (a perplexing situation for which, AFAIK, nobody has a reasonable explanation). https://www.quandl.com/data/USTREASURY/REALYIELD-Treasury-Real-Yield-Curve-Rates *It's interesting to note that, in the various interest rate threads of the past (before 2019), simply mentioning the possibility of the 30-yr rate below 2% would have sounded as weird as saying now that this specific yield may go negative in the (foreseeable) future.

-

Ramping up has been difficult and there's more to come but there are many reasons to be optimistic about the vaccines. https://www.scientificamerican.com/article/the-best-evidence-for-how-to-overcome-covid-vaccine-fears1/ https://www.kff.org/coronavirus-covid-19/poll-finding/vaccine-hesitancy-in-rural-america/ TL;DR version: There are hard-liners but there is a lot of simple hesitancy. This may be overcome with local leaders (as simple as having a nurse in the family) and by avoiding unnecessary confrontation. i think an effective vaccine rollout will help business at gyms and the related alternative supplements.

-

Gary, nwoodman posted a link to a 100 page report that provides the best overview of the insurance industry that i have read. Perfect for the non-insurance type like me. It answers your question. The link to his post is below. - https://www.cornerofberkshireandfairfax.ca/forum/fairfax-financial/fairfax-2020/msg444399/#msg444399 1- Is the simple answer: as long as rate increases > loss cost trends then, given time, we should see better EPS? (All else being equal.) It takes time as written premiums become earned premiums. From nwoodmans link, the report estimates 75% of EPS for P&C is investments returns; 20% is renewal and 5% is new business. Only 25% of earnings for most insurance companies is underwriting? 2-Plummeting bond yields has got to be killing 75% of earnings of most P&C companies. For the 25% bucket to make up this decline we are going to need to see big price increases or large price increases for insurance over many years. Perhaps this is the biggest reason we are hearing the hard market may run for years. 3-For Fairfax, they have underperformed on the investing side for so many years the bar is now very low. Improving CR and better investment results happening at the same time would definitely juice the stock price. The set up for 2021 is encouraging. Hi Viking, For 2-, there are many factors (very unusual soft phase) already baked into the hardening phase and it's hard to 'forecast' the extent but capital (from retained surplus and alternative sources) is ample and this is bound to limit the upside. For 1-, it's likely that most lines are written for a profit at this point and this may continue for a while. What we will find out over time (a topic we had discussed about a year ago) is the reserve release profile of the last few years. Of course all companies appear to be equally comfortable with their reserves but some are more equal than others. To get a better 'feel' for this, one has to go to AM Best and others for tedious and boring reading but the link that nwoodmans provided mentions this aspect on page 27. A way to ride this aspect would imply to invest in consistently profitable firms (underwriting side eg TRV, RNR) but this does not fit opportunistic investing, if that's your thing. For 3-, an interesting aspect compared to before is that FFH is likely to provide some positive return on capital from the underwriting side. It's the investment side that is still difficult to figure out (my perspective). Hi Xerxes, (your inputs elsewhere about the Middle East were interesting; still, i'm not sure this is the right forum to discuss such 'hot' topics because of the potential for polarization. You may want to look for an old mini-series released in 1986 "On Wings of Eagles" about the hostage crisis. The series was poorly made on many levels but gives an interesting insight into some aspects.) To link your post with Viking's, the bar is indeed very low for the return aspect but the bar for the downside aspect (status quo part; capital scarcity episodes are dead) remains IMO ill defined.

-

Gary, nwoodman posted a link to a 100 page report that provides the best overview of the insurance industry that i have read. Perfect for the non-insurance type like me. It answers your question. The link to his post is below. - https://www.cornerofberkshireandfairfax.ca/forum/fairfax-financial/fairfax-2020/msg444399/#msg444399 The simple question is not so simple. The hard market that followed 2001 allowed FFH to increase premiums significantly especially at OdysseyRe (see page 18 slides) and, by 2005, overall float had increased by 50%. FFH was still swallowing reserve deficiencies of the past but the best was yet to come with the buildup leading to a capital scarcity episode for which they were ready for. https://s1.q4cdn.com/579586326/files/2011%20AGM.pdf

-

i'm basically clueless here but, historically, "sudden" inflation episodes have been preceded by years of inflationary build-up. And we're not in 1974 anymore. If interested read what Mr. Bernanke described in 2003, the few paragraphs after "For illustration, I will emphasize the U.S. "Great Inflation," the experience of the late 1960s through the early 1980s." https://www.federalreserve.gov/boarddocs/speeches/2003/20030203/default.htm He then made some interesting observations about expectations and credibility. And that's after some amount of monetary and fiscal stimulus for a virus where 99% of people survive.

-

Thanks wabuffo for being gracious with your time in helping everyone reach a deeper understanding on this. To help understand deeper your perspective, I wanted to go further with the analogy of Fed Reserve as the Recorder's Office, which keeps a record of who owns each property. ... Your idea of a closed-loop system is a good one especially for the loop related to the central bank's expanding balance sheet. For the other loop (regular banks making loans and taking deposits), you have to think of it also as a closed loop (there is some hoarding and the international flows murk the issues) and you want to integrate a flow component (the velocity part). For the longest time, it was thought that money supply was strongly linked (or should be?) to underlying real economic activity and it seems this link has been breaking down (it is suggested by some that the elastic can be stretched much further, even to the MMT extent but that remains to be seen). This is a fascinating topic with many layers and many perspectives but i wonder about the real value of the discussions although the interest may have nominal value under certain circumstances.

-

^wabuffo's answer is excellent. There's a visual complement: In my limited understanding, velocity has been going down for a while and M1 (and M2) don't include reserves (required and excess).

-

Somewhat related, today i reviewed the back to school protocol with the youngest (13). She has to go through a one-week on-line transition before a still clouded outlook. While doing so, she mentioned: "I'm not sure i like school anymore... What!!!!!!!!!!!!!!!!!. My children cumulate 58 years of schooling and this is a first. This persistent on-line stuff for younger kids is a poor set-up. There are many reasons for the length of this process but a major contributor was because "my ignorance is just as good as your knowledge" (Isaac Asimov).