Cigarbutt

-

Posts

3,473 -

Joined

-

Last visited

-

Days Won

1

Content Type

Profiles

Forums

Events

Everything posted by Cigarbutt

-

^Some time ago, i had supplied the following quantitative input about fed easing: Now this needs to be complemented by a quantitative treasury stimulus input: The third (and last) cartoon is ready in the event of a potential outcome but won't be shared because of political correctess. :)

-

i don't know why but suspect that a lack of more convincing human and physical capital into the venture may be related to the poor risk-reward profile (amount invested versus potential benefits). There are a few relevant trials underway which will be made available for review between April and June 2021, hoping we learn something.

-

Just like when building an investment case, one should aim to build on previously established foundations. Occasionally, the process is a leap forward but often it is incremental but you need strong foundations. If you start with poor foundations, the likelihood of going in the wrong direction is high. The calcifediol study (IMO) has little or no value and it is hard to justify to build upon this work. Also, why would you want to 'mimic' a study with such poor foundations? The idea of 'replication' of a study is not simply to repeat the study. The most cost-effective conceptual way to go about this is to try to repeat the study with the aim to disprove the conclusions, in a way. That's why this Board is so interesting for investment thoughts when ideas get confronted and opposed in a constructive way. This is part fundamental analysis and part looking at incentives and incentives in those studies can be significant which is why independent replication is so important. The 'hormonal' study (and general line of thought) starts with a much stronger foundation even if it's about repurposed drugs. There is a clear and plausible mechanism of action through the ACE receptor. The study appears to be very well done and is a clear signal for replication to be done as soon as possible. Results appear solid but it's a sponsored study and, very often, the rate of favorable replication of sponsored studies is disappointing. All in all, there has to be a way to optimize the process (balance alternatives with established practices etc) but the Covid episode has shown that a huge amount of resources have been wasted because of poor foundations to start with and a poor process to follow. You must realize that an incredibly high number of 'researchers' are about to look for the next popular target.

-

-This is interesting and relevant from my perspective because of expected (hoped for) real estate (residential and commercial) local opportunities in the coming months or years as a result of larger than regional market forces. -On the CPI question and home prices Is a home a consumer product, an asset or somewhere in between? People collecting data for the rent part put emphasis on surveys and the validity is questionable but may represent a better reflection of the intrinsic value of 'shelter' value over time vs the 'asset' value of homes which can deviate more and can be influenced by interest rate levels (2020 was a great example of that). http://www.haver.com/comment/comment.html?c=210310SP.html A reasonable conclusion is that both curves (value allocated to rent and market home prices) should tend to align over time. It's possible that housing prices have recently been going up as a result of pent-up demand and supply constraints (similar argument in the mid 2000s) but it's also possible that housing prices end up reflecting main-street and 'consumer' levels and the more intrinsic shelter value. (my bet is on the latter) -On the "supply" issue i don't have any insights about the long term fundamentals of toilet paper retail pricing but anecdotally think that prices have gone back to their longer term trends. When there were supply-type issues earlier in 2020, i faced very similar dynamics. There is a private venture that requires monthly purchases of medical supplies, some of which (consumers started buying some of these products) showed exactly the same pattern: for short periods, prices went up significantly or products were simply unavailable. However, prices in that segment are back to previous longer term trends. For this supply aspect and consumer prices, you have now people who find money in their pockets and there is a huge part of the population (hospitality, leisure, healthcare; all very low productivity areas and temporarily at risk for mismatch between expectations of the employer and the worker) who are going back to work. So, it's not surprising that there are and will be supply side pressures for temporary price increases but i doubt that these price pressures will be sustained.

-

^Some aspects about 1-the USD dollar being the supreme currency and fuel for trade deficits and 2-how waiting for something that will take a long time to happen may not be the best strategy. Something which hasn’t been noticed or discussed has to do with a rule issued by the Commerce Department (February 2020) that allows currency manipulation potentially to be considered as a domestic subsidy under U.S. countervailing duty laws. The US, directly as the supplier of the international reserve currency and indirectly by exploring the fiscal room (and financing the consumer to continue to drive the trade deficit) has driven the global ‘recovery’ which most countries (especially developing and aiming for hegemony) desperately needed. If a true (global) downturn happens, domestic interests will dominate and even then the USD as a safe haven is likely to shine (relatively), even in a race to the bottom. Hopefully the next crisis will not be completely wasted. There are ways to correct the various trade and fiscal imbalances but all are painful. The easier way is to hope for growth to resume at a higher rate than the growth of the imbalances. However, it looks that we have globally entered the slippery part of the curve. Unfortunately, history shows that, at some point, the most efficient way to correct inequality is to make the rich suffer. The Coolidge prosperity era perhaps contained the seeds of its own destruction or is it only a cyclical thing? This thread is about inflation picking up and many (Fed, Japan, (and many here..) etc) suggest that inflation is on its way and, obviously, it’s a very real risk and the CBO has been recurrently planning for inflation to pick up but I bet that it will be darkest before dawn (because of the massive debt overhang) . The above is from "forecasts" released in 2020 but the 2021 recent release is similar. Cynics may contend that these guys are lagging indicators which is kind of true but they lag a lot longer than what the crowd is implying now and the career risk for painting a true picture is high so..Those into multi-dimensional models will recognize the typical pattern in (debt) addiction with a declining trend being associated with diminishing returns on renewed enthusiastic episodes. When comparing to what happened after WW2, sure, total debt was quite high compared to economic potential but private debt was low and there was significant growth potential …ahead. When comparing to the 70s, the same relatively-low-private-debt-some-growth-potential also applied. Since Bretton Woods, things have slowly been going downhill. Just like the Dutch Disease for exporting countries or the silver windfall from Spanish conquests, the USD currency privilege is a curse in disguise. Of course, this has been ‘known’ for a while. But this too shall pass. An interesting aspect is the concern with creeping taxation without adequate restraints which is exactly my concern with rising debt levels. But of course, the two ‘issues’ are joined at the hip. The above was released in 2011 so it's not as if the recent trends should come as a surprise, viral or otherwise. The bankruptcy-related gradual-and-then-sudden theme is interesting for inflation but the misery index that’s been associated with the 70s had roots going deep in the 60s, way before and inflation numbers had been creeping up for years. Also, in the 70s, the labor force was consistently growing above 2.0% and this growth is firmly below 1% now (and decreasing, likely going negative in this decade). In a contrarian way, the deflation risk remains the most significant in this ‘reflation’ environment.

-

The Aug 2020 study shares several methodological flaws which are fundamental (there is a pattern). From reported peer review, the study you mention has the following weaknesses: small number of patients, ICU admission as a subjective outcome, and the unusual dosing regimen. There are also many more that are easy to spot. From a proprietary review (just complemented with short review and and an investment parallel): In the study you mention, they report a comparison of some variables after randomization, but before actual 'blind' intervention: D-Dimer (ng/mL) (mean +/-SD) 'treated' group: 650.92 +/- 405.61 control group: 1333.54 +/- 2570.50 Because of the wide dispersion in d-dimer levels and because of small numbers, they come to the conclusion that there is no statistical difference for d-dimer levels between the two groups, a conclusion which is obviously very suspect. Any difference when comparing groups after randomization is suspicious and attempts to adjust results after the fact is even more suspicious. Also, the d-dimer variable is incredibly important. For the financially focused, the d-dimer level for somebody coming to the hospital is similar to the Altman Z-score for a company potentially entering distress. The importance of this aspect was sort of suspected when the study was published but the importance of elevated d-dimer levels for Covid has been consistently and repeatedly demonstrated since then. Higher d-dimer levels indicate that the the Covid disease process is more advanced, has entered an unfavorable immune response profile and has involved the coagulation profile. Higher d-dimer levels indicate that there is higher risk (exponential type of rise with linear rise in d-dimer levels) for disease severity, ICU admission, poor outcome and death. The difference in d-dimer levels in the two groups after randomization, in itself, goes a long way in explaining the measured differences in 'treatment' outcomes and makes this study essentially valueless. Just for fun (in the unlikely event that there is one other person in the world who wonders), more recent reports about d-dimers and Covid show a very similar correlation matrix (sensitivity and specificity, but even more convincing for d-dimers) with area under the curve on the left showing excess risk between the d-dimer phenomenon and the excess bankruptcy risk described for the Altman Z-score: From the covid stuff (2021): From the bankruptcy stuff (2013): The study you mention is like if the FED would have set up two groups last year, 'randomly' selected: one group receive support and the other group does not and they report that the group they supported did much better, forgetting to discuss that evaluation of their data indicates that the 'randomization' process resulted in the 'untreated' group starting out with wildly worse Altman Z-scores. An option then would be to keep on repeating the same mistakes, over and over again. What is there to lose?

-

...so you recognize that the costs and outcomes could quite possibly be asymmetric and you make a decision. ---) Pascal's wager argument SJ Why would causation be an issue in prospective randomized clinical studies. My main gripe is even after 8 months after the Spain pilot randomized study showing over 90% improvement with Calcifediol, no prospective randomized clinical study was done. ... @Investor20 i think this is not the place to argue about specifics unrelated to investments. For your own potential benefit though, you may want to take a look at this: https://poseidon01.ssrn.com/delivery.php?ID=183110124086122101102097088025096087053071017088069085030106035014016005029027087109054039038069096025084085005094125105002042006001104046005072005101012083042059078008088037095080105104083120004038106070084060095065106024068114073027110069084125095117087006109028100094022026117111096105026&EXT=pdf&INDEX=TRUE It's a study (labeled as high level evidence by the authors) looking for a peer review which has recently been released and that shares authors with the 'spectacular' Barcelona study that you mention. Let's see if you can come up with an objective opinion about the authors' conclusions and their significance. ----- Easy paths (paths of least resistance) are great but can lead astray. The fundamental problem with the Pascal's wager analogy is that you need an underlying assumption that there is only one god. That's why some prefer to use a 'cocktail' approach (add selenium, zinc etc etc). The added level of uncertainty with Covid was significant but where do you draw the line? How do you balance the need to keep an open mind and the possibility of doing stupid things? And yes 'easy' solutions are popular these days but are 'we' on the right path?

-

^To be fair, the potential 'link' between vitamin D levels and covid risk etc makes (anecdotal level assessment) more sense (slightly) than the 'link' with other conditions such as chronic fatigue, autism...etc, however the overall level of evidence is still in the basement of the hierarchy of evidence. So far, an obvious link between the transmission pattern of the virus and vitamin D (sunlight exposure as surrogate) appears to play a very secondary (if any) role. For those interested, there are methodological ways to try to go around the correlation analytical risk that is embedded with the potential link between vitamin D and Covid risk. There was recently a genetic type of assessment that came out and there is this population level assessment that was carried out in Europe during 2020: https://www.medrxiv.org/content/10.1101/2021.03.04.21252885v1.full.pdf TLDR version: Once using a way to control the correlation risk, vitamin D levels or 'deficiencies' are not linked to Covid risk. @StubbleJumper Apologies for pursuing this 'policy' topic but there is an investment correlation: when people come here to share investment thoughts, various ideas may be 'recommended'. To be convinced, individual anecdotes may be interesting but a higher level of evidence may be necessary. Let's say someone in Ottawa notices your astute comments in this thread about the link between Covid and vitamin D, and you obtain the decision power to mutualize the cost of vitamin D supplementation for the 38M population. What do you decide? Now is a good time to suggest expenditures because there is a mountain of free money to distribute. 10 bucks per person is only 380M after all.

-

A potential win/not-lose aspect is that: "One pill every two weeks fights diabetes, cancers, heart failure, and 18 other diseases". :) Covid-19 was recently added to this list. Isn't there an analytical risk here? Disclosure 1: over the years, i've had to periodically participate in committees which had to decide if the single payer should pay for certain propositions (there was typically a few participants whose main line of argument was: what is there to lose? a similar line of argument is used now to justify the 2T fiscal shot in the arm). Apologies: i tend to focus (too much?) on second and other higher order effects (the 'unseen' ones). Disclosure 2: i'm in the process of being enrolled in a study (based on strong foundations) which will follow people at relatively high risk to be exposed and to contract covid over the next few months. One arm of the study will receive vitamin D supplementation and the other arm will get a placebo. (i may receive a placebo but will watch for the side effects; you must be aware that the placebo group will also report side effects?)

-

i just want to mention that fleeing is too strong a word. For a while now, US government debt held by foreigners has grown (at a rate slightly less than GDP). https://fred.stlouisfed.org/series/FDHBFIN https://ticdata.treasury.gov/Publish/mfh.txt After the GFC, this ratio (US gvmnt debt over GDP) has grown and sort of peaked in early 2014 at 34.8%. At yr-end 2020, it's at 32.9%. The most liquid market in the world has become very crowded(!?). For a contrarian, crowded trades are interesting because of potential reversals. In this case however, my bet, at least for a while, is with the momentum crowd who can control the yield curve. Don't fight the Fed, they say.

-

Right. I don't get it. We didn't have 6% inflation before covid, so what has changed? What has clearly changed is the attitude of governments, and the general population, towards running large budget deficits. To take the example of Canada, the Federal Government ran a $400bn deficit in 2020 (16% of GDP vs. 4% in 2009), and has not produced a budget in two years. This government now has a ~50% of winning a majority this spring (if an election is called), and there is very little appetite for austerity. One of the 'classic' causes of inflation is the government printing money since desired spending > taxes. The political dynamics around deficit spending ('build back better') are likely to be very different post-lockdown vs. post GFC so the low inflation experience of the 2010's is unlikely to be repeated. Deficit source: https://tradingeconomics.com/canada/government-budget As far as attitudes and sentiment, we may have entered the reflated roaring 2020s. In Japan (potential leading indicator), in the last 20 years or so, the consensus view is that inflation is coming (there is still some disagreement on timing). The sky is the limit? Inflation is coming? (the 2013 'spike' happened as a result of sales tax) The last reading for Japan (Jan 2021 YOY): -0.6%. If the idea is to wait for inflation to reach 6% before going through fundamental reforms, this may shape up to be an amazing ride.

-

This is not the type of topic which is exciting but begs the question: is this a free market anymore? Anyways, some people appear concerned (excess reserves, excess deposits, regulatory ratios): https://www.bloomberg.com/news/articles/2021-03-09/banks-press-fed-to-preserve-600-billion-in-balance-sheet-leeway?srnd=markets-vp When thinking about all these 'temporary' measures, i see that the BOJ has recently instituted a complex multi-tier excess reserves system with a category of 'marginal' excess reserves and a way to compensate financial institutions to hold the massive amount of reserves that the system has created. The BOJ is also trying to find a way to temporarily increase its holdings of common stocks. It's OK because real prosperity is just around the corner.

-

Yeah, if the stock market goes straight up the rest of the decade I'm selling everything in early 2029 The 20s was a period when the decade started with a cyclically adjusted PE of 5 and ended at 30-35 (low and declining interest rate period). Perhaps an unrealized aspect is the amount of real (and revolutionary) productivity enhancements that were happening: electrification, household appliances etc. The 20s (and the 30s) came with some noise (the type of noise JK Galbraith describes) but, with the initiation of consumer installment loans, the stage was slowly being set for the amazing inclusive growth that was to occur from 1945 to 1975.

-

This is not a material transaction for FFH. It's interesting though (i used to have a map on the wall trying to make sense of the maze etc). 'Commonwealth' was acquired in 1990 (!) and made its way to Northbridge. The initial 'Commonwealth' had a sub of its own that was writing policies (essentially oil and gas property in the US). This US sub of a sub did not turn into a butterfly and was eventually put into runoff and sold to an another internal runoff sub in 2013 (capital of about 20M) and was moved around after. Its residual capital is at about 8-9M and appears mostly to a be a liquid portfolio. Its value may have lied in its footprint (licensing).

-

Of course, you're right. But this stuff is sooo fascinating... Just think of the oncoming emission of coordinated and consolidated excess reserves into a world already awash with excess reserves. What has been happening in certain balance sheets is puzzling, to say the least: https://www.yardeni.com/pub/peacockfedecbassets.pdf On a first-level analysis concerning what others are asking, reading the Z.1 financial accounts (especially since the GFC) would suggest that low interest rates have been, on a net basis, a positive contribution. i guess my position is similar to yours (ie we need higher interest rates) but the second-level answer (going above short term implications) is more complicated in a way, perhaps the same way an investment's +NPV may necessitate negative investment cashflows for a while. But yes, this board is no place to discuss the anemic secular growth of real wages for most in a declining productivity world and it does not matter (directly and in most cases) if your job is to micro-select within available opportunities. --- BTW thank you for your inputs in general and more specifically about the book you recently suggested: For good and evil: the impact of taxes on the course of civilization. i just made it to part 2 (the Romans) and am enjoying the topic, style etc. i agree with most of what the author says so far and only have reserves at the margin (of course, that's where the fun is).

-

This may interest some and the topic has economic and potential investment implications. Recently (two main references listed at the end), it has been suggested that the Coronavirus episode has subtracted a full year or more of expected life expectancy in 2020 (US data). The underlying assumptions for the raw inputs are open for debate but are quite reasonable. The method used however is highly questionable and the ‘message’ potentially misleading. First, at the population level, even if the 1+ year loss in life expectancy is taken at face value, this is NOT an extinction-level type of event. Second, the following discussion makes abstraction of individual consequences. At the individual level, death, especially if unexpected, is likely to be a tragedy. Whoever questions that should sign up to be a volunteer at an oncology clinic for a few days (BTW, this is a relatively easy thing to do if you are inclined and can be a great learning (humane) experience for adolescents). One thing that you may come away with going through this type of volunteer work is the amazing thirst for life that individuals typically have (even problematic, especially the way the issue is framed by those offering care). People are often ready to invest ($, suffering, debilitating side effects etc) in exchange for often questionable quality of life of limited duration. Anyways, absent these very real individual considerations, the point of this post (respectfully submitted) is that the impact of this virus on the population (economic wise) has been (and will be) mostly inconsequential. It’s great if you can benefit from market swings related to the perceived impacts but i’d be really surprised if this topic is materially mentioned again in 2022 or after. In a conceptual way (assuming a few aspects), this is like if the entire population had decided to take a sabbatical and to dip into their savings (or incur more debt..). Also, the 1+ year life expectancy loss is a misrepresentation of reality. The classic methodology uses a ‘periodic’ aspect which means that the method assumes that the excess deaths for the measured period will continue to apply in the future (hysteresis level of about 100%) which, clearly, does not apply anywhere close to 100% for the coronavirus episode. There are factors that will stay after the virus is gone or becomes endemic and the net effect is still unknown but the periodic effect on future periods is likely to become close to 0% over a relatively short period of time. This is why the impact on life expectancy from the deaths of despair is so much more significant. The US has decoupled from developing countries in terms of the evolution of life expectancy in the last 10 or 20 years. In some years, life expectancy in the US has even decreased(!). This is due to many reasons but the biggest one is the rising incidence of deaths due to drug overdoses (a phenomenon that has continued to increase in 2020). This phenomenon involves younger cohorts of potentially very productive individuals and has shown a much enduring (and growing) pattern. Correcting for this methodological flaw means that the life expectancy loss in 2020 in relation to the pandemic is about 50 times less than the 1+ year reported. https://www.cdc.gov/nchs/data/vsrr/VSRR10-508.pdf https://www.pnas.org/content/118/5/e2014746118#T1

-

^The supply of money is kind of straightforward but ‘demand’ for money (like money velocity) are fuzzy concepts. Who doesn’t want free money? Money supply should correlate to underlying economic growth (as an endogenous source of money demand). However, for the last 20 years (variable but increasingly), money supply has outstripped real economic growth and it feels like the Treasury-Fed industrial complex’ strategy is to continue on the same trajectory (more and more money supply and less and less growth). --- Gold prices are determined by a variety of factors (some of which shared with cryptocurrencies) but it seems the three following factors are most significant now: 1-gold seen (perception to a significant degree) as an alternative to fiat money and as an inflation hedge 2-gold seen (again mostly a perception) as a safe haven 3-gold being attractive as a result of the ‘wealth’ effect In the 70s, gold did well as a result of 1- and, to some degree, because of 2-. 1- makes sense if one believes that recent inflationary forces are more than transitory. With the Treasury directly crediting bank accounts and with debt growing faster than the underlying economy, there is bound to be at least some inflationary effect but unless this translates to endogenous money creation through the private system (unlikely under present leveraged circumstances) in correlation to productive growth, the deflationary forces should take over. 2- makes sense if one looks at what happened to gold held by central banks. The US central bank remains the largest owner and, for the last few years, mostly in emerging economies, there has been significant net buying. 3- makes sense as ultra-low interest rates have driven a wide search for alternatives to cash and low yielding securities (low opportunity cost of not holding them). The problem with 3- is that it’s proven to be quite a powerful transmission mechanism (feeding easy money into asset price inflation) but eventually a detrimental and mean-reversion one. What happened to housing pricing in developed countries in 2020 is a clear example of that (risk-free rates down ++ and the spread between the 30-yr fixed mortgage rate and the risk-free 10-yr way down). Housing has become quite unaffordable for the bottom 60-80% and people are bound to notice eventually. The negative side of the wealth effect (and the impact on gold prices) is that the whole assumption (and now a subterfuge) rests on the capacity of the productive forces of the market to take over when the markets get eventually weaned from this artificial support (support in place for more than 10 years at this point). Who knows what will happen in 2021 (?) (related to the reflation aspect and the impact on growth and related tax receipts) but an interesting trend to look at will be the evolution of income levels without government transfers (the more enduring part of the reflation trade). --- Comparing the 70s and now is interesting. In 1971, the US unilaterally abandoned the gold standard (there’s nothing wrong with that per se but perception about the value of the USD changed for a while). Inflation forces had clearly taken hold during the 60s, way before. In the 70s decade, the CAGR real economic growth was 3.2% (despite two negative reading years), the federal debt held by the public was about 25% of GDP and the demographic profile still looked quite favorable. In the 2010s decade, the CAGR real economic growth has been 2.3% (no negative reading years and with huge artificial support), the federal debt ratio is now at around 90% and the demographic profile looks a lot less favorable. Real rates have clearly entered negative territory and there is a climate of apprehension with barely rising inflation expectations. And the Fed appears ready to intervene at any minute. And the worry is that 1-inflation is about to take off? 2-the Fed won’t be able to keep rates down? Opinion: one should discount the possibility that 2- will be the least of their problems and 1- will remain the unachievable goal absent more 'heroic' attempts.

-

This year: "Net adverse prior year reserve development at U.S. Run-off of $216.4 principally related to continued deterioration of asbestos, pollution and other hazards exposures ($213.7), and strengthening of other loss reserves ($6.7), partially offset by net favourable emergence on workers’ compensation loss reserves ($5.5). Net favourable prior year reserve development at European Run-off of $65.9 principally related to improvement in RiverStone (UK)’s employers’ liability and public liability exposures ($49.4) and improvement in Advent’s marine and property exposures ($9.5)." (my bold) ----- -Overall for FFH, reserve releases are holding up nicely (better than anticipated), a phenomenon reflected overall (to various degrees) in the industry. -On the asbestos front, FFH appears to simply follow industry trends in slowly catching up to the eventual result (not better or worse). One day, i will (not on an empty stomach) go through all disclosures and figure out the eventual asbestos costs for policies written before 2001 (2001! no wonder they say long tails can wag the dog). In February of 2020, we had exchanged on this and i had submitted the opinion that there was likely 350-400M left to be recognized over the next 5 to 7 years. This year's increase in reserves may have been extra conservative because asbestos reserves were transferred to Riverstone UK in early 2020. My understanding is that FFH is on the hook for further adverse reserve development in the sold reserves portfolios through a contingent value instrument-type of arrangement with CVC.

-

*cough* BITCOIN *cough* Many thanks for this - terrific summary, and many 'rhymes' to remember here, I think. A fascinating aspect is that during the actual financial-engineering-zaitech period and even at the height of the 1989 bu**le, there was widespread optimism (general sentiment) and widespread institutional sentiment about future prospects for earnings growth, stock market return etc. ie the typical institutional investor did not consider that zaitech was speculation, it was felt to be justified by underlying fundamentals. Now, it's quite obvious but it wasn't at the time, at least for the involved and vested people. Where are they now? Moving away from the present period for the US markets, this reminds me of the time i was following large US banks in the period leading to the 2007-9 adjustment phase. The above does not show the phase before 2005 (but the pro-cyclical (within quite an unusual musical chair cycle) picture had been occurring for some time for the buyback activity) and, at the time, it was felt that buying back shares at increasingly high prices was sound capital allocation. A lot of buyback activity doesn't make sense over the full cycle but if you happen to hold during the 'right' period, it doesn't really matter. For the Japan bu**le, a lot of the insights came from Mr. Shiller (the 1996 Why Did the Nikkei Crash? is interesting about the perception of market fundamentals) who, very recently, reproduced an opinion (this time in the NYT). His point is pictured in the introducing video: https://www.nytimes.com/2021/03/05/business/stock-market-prices-bubble.html Identifying bubbles is not that hard. Profiting from them can be hard.

-

^A poster just suggested that a conglomerate discount could apply going forward and it made me look back to a report put out by Alice Schroeder in 1999: The Ultimate Conglomerate Discount. And there was this more complete quote: "“I’ve heard Warren say since very early in his life that the difference between a good business and a bad business is that a good business throws up one easy decision after another, whereas a bad business gives you horrible choices—decisions that are extremely hard to make...One way to determine which is the good business and which is the bad one is to see which one is throwing management bloopers—pleasant, no-brainer decisions—time after time after time.”—Charles Munger, 1998 Annual Shareholders’ Meeting, as quoted in Outstanding Investor Digest"

-

There are only a handful of supra-regional projects going right now in North America for electricity infrastructure and one of them is the connection theme developed by PacifiCorp in the western part of USA. With the developing distributed energy aspect and with the integration of variable energy producing sources, counter-intuitively, there is a greater need for regional and supra-regional connections. One of the other similar projects i've been following is a connection between my province north of the US border to Massachusetts. The plan is to meet the new challenges with modern transmission infrastructure and will involve export of excess energy from hydro-electricity to Massachusetts. The project has entered the construction phase. The aspects that characterize these projects are: operational complexity, very long-term perspective, ability to coordinate a vast and complex array of interest groups with conflicting objectives and very deep pockets, all attributes of BHE. In the 'regulatory' 4-page letter, the word 'transmission' appears 57 times and is a typical example of BHE's ability to navigate complex regulatory hurdles. https://www.energy.gov/sites/prod/files/2020/11/f81/BHE%20FINAL%20letter%20to%20DOE%20re%202020%20Congestion%20Study.pdf In the letter, there is a reference to a 'congestion' report which shows, on page 8, the tremendous potential for investments in the "WECC". https://www.energy.gov/sites/prod/files/2020/10/f79/2020%20Congestion%20Study%20FINAL%2022Sept2020.pdf BHE's message: We're here to help.

-

This aspect is interesting because it may explain (IMO) some of the cash build-up at holdco. When Mr. Buffett made the PCP acquisition, he paid a normalized PE of 18 (earnings yield of about 5.5%). The idea then was that the rest of the return would come from growth (organic and acquisitions). From 2003 to 2015, operating earnings had grown at a CAGR of 15-16%. When announced, many people suggested that the switch in investment mindset (pay more for growth) was the right one and many suggested that he had under-paid for the acquisition (i just checked for fun what people here said at the time). So, for this specific transaction, the outcome is likely to be satisfactory over time but the price paid was too high as a result of assumptions that were initially too optimistic. Of course, it's easy to say in retrospect.

-

^He has expressed similar sentiments concerning the Kraft-Heinz ownership (especially the 'expensive' Kraft part). With Precision Castparts, the acquisition made in 2016 contained the assumption that return on capital trends would return to previous levels. The goodwill paid for above-normal earning power was too high but has become a sunk cost.

-

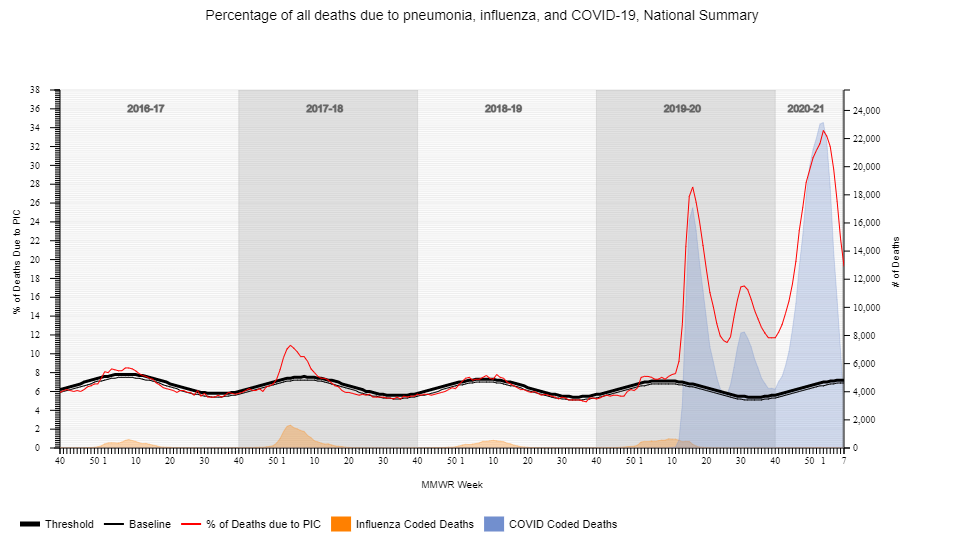

@Investor20 Of course I agree with your self-evident truths but reading your assertions typically triggers the following slogan: with enough ‘ifs’, you could put Paris in a bottle. Looking past the fundamental aspect, one has to wonder: what is the driver behind all this? 1-Positive tests versus reality -Just like with everything else, there are false positives and there are false negatives -To suggest that a single positive test is the driver of conclusions does not add up to the real world -It has become clear that most excess deaths (quite an objective measure) happened secondary to a direct effect of Covid as a significant contributing cause Yes, you can find stuff that questions the above notions but the weight of the evidence has become very strong. 2-Hospital-acquired Covid This has been studied (healthcare workers and patients). The conclusions are variable but the weight of evidence suggests strongly that the number of hospital-acquired cases is much lower than the 25% mentioned. A very interesting sub-aspect of this discussion is that most hospitals adapted (to various degrees) and adapting (basically through basic tools of distance, masks or other equipment, basic hygiene measures and basic protocols) meant significantly reducing in-hospital transmission. i have access to data from a nearby and major metropolitan hospital that became a designated center for Covid in a city that reported one of the highest community spread in the world and they have convincingly shown that the risk of in-hospital transmission can be effectively brought down to near zero (without using ivermectin, h-chloroquine or other various supplements). If you want evidence and more discussion, see below. https://jamanetwork.com/journals/jama/fullarticle/2773128 https://www.cambridge.org/core/journals/infection-control-and-hospital-epidemiology/article/universal-masking-is-an-effective-strategy-to-flatten-the-severe-acute-respiratory-coronavirus-virus-2-sarscov2-healthcare-worker-epidemiologic-curve/9301E77612122039190A29CB7223F9C4 3-Aiming intervention at the root of the problem The virus started somewhere around Wuhan and ended up, somehow and for an unusually high number of cases, at the morgue. Effective interventions have been defined along the chain of events and there’s more work to be done. The document you mention contains the word chloroquine 76 times. Consider the following: https://www.cochranelibrary.com/cdsr/doi/10.1002/14651858.CD013587.pub2/full?cookiesEnabled https://www.bmj.com/content/372/bmj.n526 Of course you can indicate that hydroxychloroquine has not been appropriately studied because people did not take the ‘miracle’ drug with various co-supplements etc etc etc or as a magic ‘cocktail’ etc etc etc but a lot of time and precious resources have been allocated to this question and results have been deeply disappointing. The person who is chair of this WHO committee works in my province in critical care and he has helped to feed the thought process involving the evaluation of ‘alternative’ solutions. One of the conclusions is that alternative pathways need to be considered cost effectively. However, campaigns of disinformation and misinformation are like diseases and need to be eradicated. https://www.ncbi.nlm.nih.gov/pmc/articles/PMC7188430/

-

Dude you think it's the "conspiracy-related groups" theories that have not resisted the test of due dilligence? You are living your life wide asleep aren't you. Try to open your eyes. A blind person can see it. i'll continue the discussion for the following reason: you post in the cryptocurrency thread and i'm trying to understand this interesting topic (it may take a long time becoz of mental retardation) but perspectives such as yours may be helpful. 1-Who is they? 2-Heart and related diseases have actually gone up during Covid and that's an interesting discussion (even potentially constructive despite opposing views). Typical report from developed countries (you are from Belgium? the Netherlands? i assume that the same pattern played out there, especially during March to June 2020): See below for full reference. What became very obvious during the spring of last year was that people who had significant symptoms (heart attack or stroke especially) consciously decided to avoid or delay consulting appropriate resources. There's a bunch of people who died or who suffered irreversible complications from waiting. It's hard to allocate the cause of this phenomenon but the two main ones are 1-individual decisions based on their own assessments and 2-individual reacting to the institutional message (excessive?) that may have caused them to avoid necessary care. i don't have a clear answer here. What i can tell you though is that the cardiologists and neurologists (i guess part of the "they" people) became very concerned and organized to improve the message. So, overall, the evidence is that the virus, through a direct or indirect response was associated with increased heart and related morbidity and mortality was significant but this excess mortality explains a small part of the very significant excess mortality that happened over the course of this pandemic. https://www.jacc.org/doi/10.1016/j.jacc.2020.10.055 Of course, i could be wrong. Please enligthen me. i want to see the Light. :)