Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

I think Wade Burton talked about public versus private on the most recent conference call (strengths and weaknesses of each). I think he said they are agnostic - they want the best investment. The more I hear Wade talk the more I like him. Very logical and rational.

-

@Txvestor , one of my central ideas is something changed around 2018 with how they picked and constructed their equity portfolio. But it was even more - they started to focus more on optimization (like what got started in insurance in 2011). All you have to do is look at the companies they owed then - the biggest positions. It was loaded with very poor performers (putting it politely): - Legacy: BlackBerry, Resolute Forest Products/Abitibi, CIB, Sandridge Energy, Recipe - Purchased 2014 to 2017: Eurobank, Fairfax Africa, APR Energy, Farmers Edge, Boat Rocker, EXCO Resources, AGT Foods Issues: some combination of weak management, weak balance sheet, weak profitability/cash flow (some had all three). Eurobank, EXCO and Recipe are much improved companies today. The jury is out on AGT. Fast forward to today… the portfolio is loaded with queens. Common theme: all have strong management, strong/solid balance sheets, strong/solid profitability/cash flow. Complete 180 from pre-2018. That has to be by design. The change is simply too stark.

-

As a starting point, more than last year. 2025 - “During the year we purchased 1,006,535 subordinate voting shares for cancellation for cash consideration of $1.6 billion, or $1,615 per share", said Prem Watsa, Chairman and Chief Executive Officer.” Fairfax thought their shares were very cheap a year ago - they were very aggressive with buybacks. The shares closed Friday at $1,625, about what they paid in 2025. But the value of Fairfax has increased quite a bit over the past year. And it is going up nicely every quarter. So Fairfax is a much better deal today than it was a year ago. As a result, I think Fairfax will be more aggressive. In terms of $, Fairfax has lots of options. They can be very creative when they are motivated (look how they funded the dutch auction in 2021). If value keeps growing and the shares stay at current levels (or go lower) it could get to a point where Fairfax acts (gets creative and more aggressive with buybacks).

-

Regarding buybacks, my guess is the persistency of current low stock price has likely caught Fairfax a little by surprise (like the rest of us). Beginning in Q4 of last year Fairfax has been very aggressive with share buybacks. And it seems to be having little impact on the share price (this has surprised me). Fairfax also been very busy on the capital allocation front in recent months (lots going on in addition to buybacks). If the share price stays at current levels, I think there is a good chance that Fairfax will get more aggressive with buybacks. They are very opportunistic. And also very good at sizing their bets.

-

The use of minority parters to fund their acquisition spree from 2014 to 2017 was brilliant. An important outcome is the size of Fairfax’s insurance business is overstated (net premiums, float, underwriting profit). And that is because of the minority interest in Allied World and Odyssey. At least that is how I think about it conceptually. When Fairfax takes out minority shareholders, the earnings (driven by NPW, float and UP) that accrues to common shareholders will increase. It is the same as buying another company. Of course, Fairfax also locked in a low purchase price - when they put each of the original deals together. That is icing on the cake. This given an elegant way to continue to grow in a soft insurance market. (Not that anyone cares.)

-

@SafetyinNumbers , the Fairfax story is full of nuances. The “lost decade” moniker I like to use is catchy but it does oversimplify the reality of what was actually happening under the hood. Fairfax’s insurance business was slowly getting transformed for the better - and it doubled in size from 2014 to 2018 (acquisitions). Basically the insurance spring was getting coiled tighter and tighter from 2010 to 2020 (in terms of earning power) - and then it doubled in size again from 2020 to 2025 (hard market). There are many stories like this… where the earnings power had increased significantly but it was being masked by losses from equity hedges/shorts/poorly performing equities. There are so many interesting angles to the Fairfax story.

-

@Maverick47, here is where the story gets even more interesting… 1. You lose $500 million for 11 straight years. 2. Lots of the equities purchased from 2014 to 2017 underperformed. 3. Interest rates are also very low for much of the time. And you still deliver a compound return of 4% over the 11 years. How did they do it? Fairfax has an exceptionally powerful business model. Just imagine what it is capable of if the company was firing on all cylinders?

-

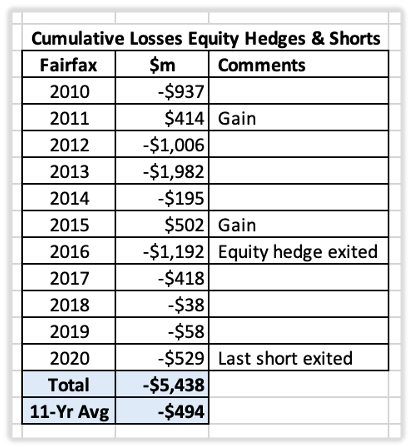

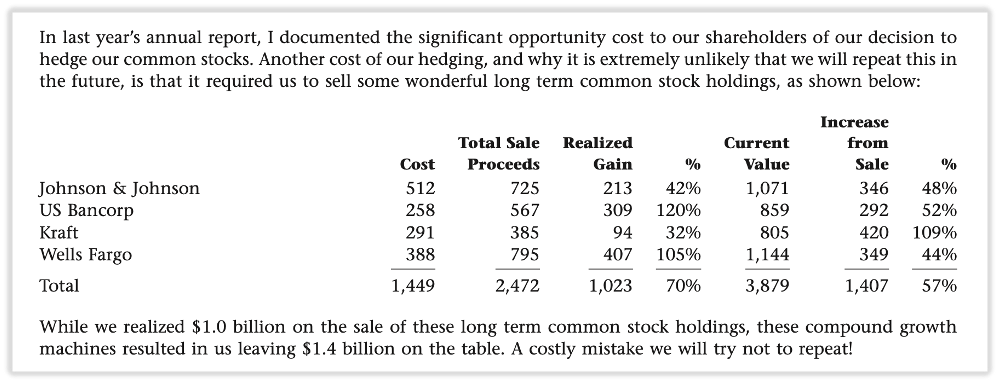

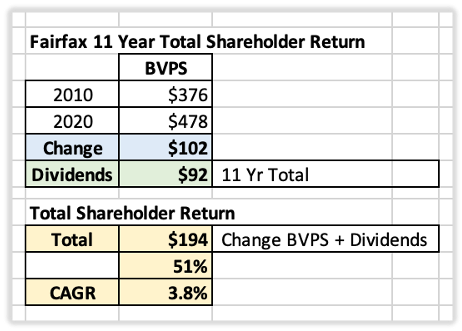

Equity Hedges and Shorts: Fairfax’s The Lost Decade (2010 to 2020) This is the sister article to the one I wrote yesterday. Fairfax's Version of The Big Short. Scroll up to read it. When Risk Management Became a Macro Bet “Those who cannot remember the past are condemned to repeat it." (George Santayana) What was Fairfax’s largest investment mistake? The equity hedge and short positions it maintained for much of the decade following the financial crisis. Between 2010 and 2020, Fairfax lost approximately $5.4 billion on its equity hedge and short strategy—roughly $500 million per year. To put that in perspective, Fairfax's shareholders' equity was about $7.7 billion at the beginning of 2010. The losses were significant. The opportunity cost was even greater. Capital remained tied to a bearish thesis while global equity markets enjoyed one of the strongest bull markets in history. Along the way, Fairfax was forced to sell some successful investments, limiting the benefits of long-term compounding. In Peter Lynch's language, some of the flowers were cut while many of the weeds remained. For shareholders, the result was a lost decade. Prem’s comment from Fairfax’s 2017AR Why Fairfax Put on the Trade To understand the mistake, it is important to understand why it was made. The roots of the strategy can be traced directly to Fairfax's greatest investment success: its credit default swap (CDS) position during the financial crisis. Between 2005 and 2009, Fairfax generated more than $2 billion in profits by correctly anticipating severe problems in the global financial system. That experience shaped management's outlook. Following the crisis, Fairfax became increasingly concerned that developed economies faced a future of excessive debt, weak growth, and deflation. In Fairfax's 2010 Annual Report, Prem Watsa wrote: "We worry that the North American economy may experience a time period like the U.S. in the 1930s and Japan since 1990." If that scenario unfolded, equity markets could struggle for many years. To protect shareholders, Fairfax steadily increased its equity hedges until much of its common stock portfolio was effectively insulated from a major market decline. Viewed from 2010, the concerns were understandable. The financial crisis was still fresh. Government debt levels were rising. Economic growth remained sluggish. Central banks were experimenting with unprecedented monetary policies. Many thoughtful investors shared similar concerns. The problem was not identifying risk. The problem was what happened next. “2010 was a disappointing year for HWIC’s investment results because of the two factors mentioned earlier. Hedging our common stock investment portfolio cost us $936.6 million or $45.61 per share in 2010. Our hedging program masked the excellent common stock returns we earned in 2010, of which a significant amount was realized ($522.1 million). We began 2010 with about 30% of our common stock hedged. In May and June, we decided to increase our hedge to approximately 100%. Our view was twofold: our capital had benefitted greatly from our common stock portfolio and we wanted to protect our gains, and we worried about the unintended consequences of too much debt in the system – worldwide! If the 2008/2009 recession was like any other recession that the U.S. has experienced in the past 50 years, we would not be hedging today. However, we worry, as we have mentioned to you many times in the past, that the North American economy may experience a time period like the U.S. in the 1930s and Japan since 1990, during which nominal GNP remains flat for 10 to 20 years with many bouts of deflation.” Prem Watsa – Fairfax 2010AR What Happened The feared outcome never arrived. Instead, the U.S. economy recovered. Interest rates remained exceptionally low. Central banks injected massive liquidity into financial markets through quantitative easing. Governments ran large fiscal deficits. Corporate profits expanded. Technology companies flourished. The result was one of the longest and strongest bull markets in modern history. Fairfax, however, remained largely committed to its bearish positioning. Over time, what began as a risk-management tool gradually evolved into a large macroeconomic bet. That distinction matters. Risk management seeks to protect against adverse outcomes. A macro bet depends on a specific economic forecast being correct. As the years passed, the line between the two became increasingly blurred. What Went Wrong? Many of Fairfax's concerns proved reasonable. Debt levels were high. Economic growth was sluggish. Central-bank policies were unprecedented. The world did face meaningful risks. The mistake was not recognizing those risks. The mistake was position size, duration, and flexibility. The hedges eventually became so large that they dominated Fairfax's investment results. The positions were maintained for more than a decade despite mounting evidence that the original thesis was not playing out. Most importantly, Fairfax underestimated the willingness and ability of governments and central banks to support economic activity and financial asset prices. The result was a decade of disappointing investment performance. The direct losses totaled approximately $5.4 billion between 2010 and 2020. The indirect costs were equally significant: Missing much of a historic bull market. Prematurely selling successful investments. Slower growth in earnings and book value. Significant damage to Fairfax's reputation. The loss of many long-term shareholders. The impact on shareholder returns was dramatic. Book value per share increased from $376 in 2010 to $478 in 2020. Including dividends, Fairfax delivered a total return of approximately 51%, or 3.8% annually. Over the same period, the S&P 500 generated a total return of roughly 332%, or 14.2% annually. Exiting the Trade Fairfax exited the strategy in stages. The broad equity hedge program was removed near the end of 2016 following the U.S. presidential election. In Fairfax's 2016 Annual Report, Watsa explained: "Unfortunately, the presidential election on November 8, 2016 changed the world for us, so we reacted quickly by removing all our index hedges and some of our individual short positions..." Several individual short positions remained, however, and continued to lose money. By 2019, Watsa publicly acknowledged the mistake: "Shorting is dangerous, very short term in nature and anathema to long term value investing." After another $529 million loss in 2020, Fairfax finally closed its remaining short exposure. The decade-long experiment was over. A Turning Point The removal of the hedges and shorts eliminated a significant drag on Fairfax's earnings power. For more than a decade, the strategy had cost shareholders roughly $500 million per year. Once the positions were closed, that headwind disappeared. The improvement in Fairfax's results after 2020 was driven by many factors, but the elimination of the hedge program was undoubtedly one of them. Investors evaluating Fairfax after 2020 were looking at a different company—one no longer burdened by a large and persistent negative carry. Why Did It Persist? No outsider can know with certainty. My best explanation is that Fairfax's extraordinary success with credit default swaps reinforced management's confidence in its broader macroeconomic outlook. Ironically, the same mindset that produced one of the company's greatest investment successes may also have contributed to one of its largest mistakes. That pattern is common in investing. Success builds confidence. Sometimes it builds too much confidence. Lessons for Investors The equity hedge and short strategy offers several important lessons. In many ways, they are the mirror image of the lessons from Fairfax's highly successful CDS trade. First, risk management can become dangerous when it evolves into a macroeconomic forecast. What began as a hedge gradually became a large bet on a specific economic outcome. Second, position size matters. The hedges eventually became so large that they drove Fairfax's investment results. Third, duration matters. Even a sound thesis can become extraordinarily costly if maintained for too long. Fourth, investors must adapt when facts change. Fairfax was slow to adjust as markets, economies, and policy responses evolved. Finally, trust matters. The strategy did more than cost shareholders billions of dollars. It damaged confidence in management's judgment and led many long-term investors to leave. Financial losses can eventually be recovered. Trust usually takes much longer. As Buffett has observed, companies tend to get the shareholders they deserve. Fairfax has long said it wants long-term shareholders. If that is the case, management must uphold its side of the relationship. From 2010 to 2020, it failed to do so. To management's credit, the mistake was eventually acknowledged, the positions were closed, and the company moved forward. Fairfax's performance since 2020 suggests the lessons were learned. That may be the most important takeaway. Every great investor makes mistakes. What separates the best from the rest is their ability to recognize them, learn from them, and avoid repeating them. ------------ Comments from Prem and other notes from Fairfax’s 2016AR. Prem discusses the reasons for exiting the equity hedges. He also provides a summary: from 2010 to 2016, total losses from equity hedges were $4.4B. These were offset by net gains on stocks of $2.7B and bonds of $2.2B. Fairfax’s investment portfolio had been performing very well. "Unfortunately, the presidential election on November 8, 2016 changed the world for us, so we reacted quickly by removing all our index hedges and some of our individual short positions and reducing the duration of our fixed income portfolios to approximately one year – all of which resulted in a $1.2 billion net loss on our investments in 2016 which, in turn, resulted in a loss in 2016 of $512 million or $24.18 per share." "When we removed our hedges near the end of 2016, we realized a loss of $2.6 billion in 2016, but that included $1.6 billion which had gone through our statements in prior years. As discussed earlier, since 2010 we have had $4.4 billion of cumulative net hedging losses and $0.5 billion of unrealized losses on deflation swaps (which we still hold), offset entirely by net gains on stocks of $2.7 billion and net gains on bonds of $2.2 billion. The volatility of our earnings caused by our hedges and long bond portfolios is over – and as I said earlier, we are focused on once again producing excellent investment returns." Prem Watsa – Fairfax 2016AR Equity contracts: “Throughout 2015 and most of 2016, the company had economically hedged its equity and equity-related holdings (comprised of common stocks, convertible preferred stocks, convertible bonds, non-insurance investments in associates and equity-related derivatives) against a potential significant decline in equity markets by way of short positions effected through equity and equity index total return swaps (including short positions in certain equity indexes and individual equities) and equity index put options (S&P 500) as set out in the table below. The company’s equity hedges were structured to provide a return that was inverse to changes in the fair values of the indexes and certain individual equities.” “As a result of fundamental changes in the U.S. that may bolster economic growth and business development in the future, the company discontinued its economic equity hedging strategy during the fourth quarter of 2016. Accordingly, the company closed out $6,350.6 notional amount of short positions effected through equity index total return swaps (comprised of Russell 2000, S&P 500 and S&P/TSX 60 short equity index total return swaps). The short equity index total return swaps closed out in 2016 produced a realized loss of $2,665.4 (of which $1,710.2 had been recorded as unrealized losses in prior years). The company continues to maintain short equity and equity index total return swaps for investment purposes, and no longer considers them to be hedges of the company’s equity and equity-related holdings. During 2016 the company paid net cash of $915.8 (2015 – received net cash of $303.3) in connection with the closures and reset provisions of its short equity and equity index total return swaps (excluding the impact of collateral requirements).” Fairfax 2016AR

-

@Txvestor, you make a good point. There are two (updated) posts coming on that topic… should be out shortly “Those who cannot remember the past are condemned to repeat it." George Santayana

-

Here is an AI generated summary of Sleep Country's recent acquisitions (Sleep Number pending). I think the IP angle is key given the size of Sleep Country's Canadian footprint. The UK acquisition last year also enhanced Sleep Country's capabilities. Given how slow the housing market is today in the US and Canada, this is likely the perfect time to be a buyer. This is right out of the Fairfax playbook. At the 2024 Fairfax AGM Alan Kestenbaum told the story of when he called Prem during Covid (when the steel industry was getting killed) wanting to do a big strategic transaction... Prem pushed him hard to do it. And a few years later it turned out to be a brilliant move. That is the value of having a parent who has the right temperament. https://www.mccarthy.ca/en/experience/stelco-signs-long-term-pellet-supply-agreement-and-option-to-acquire-25-interest-in-minntac-with-u-s-steel Common thread... these are all distressed purchases. All give Sleep Country capabilities they didn't have before. Shitstorms are opportunity. Very counterintuitive. It will be interesting to see where the funding for Sleep Numbers comes from. Probably partly from Sleep Country issuing debt. And partly from cash from Fairfax.

-

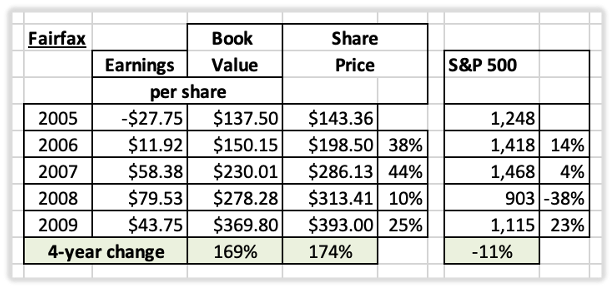

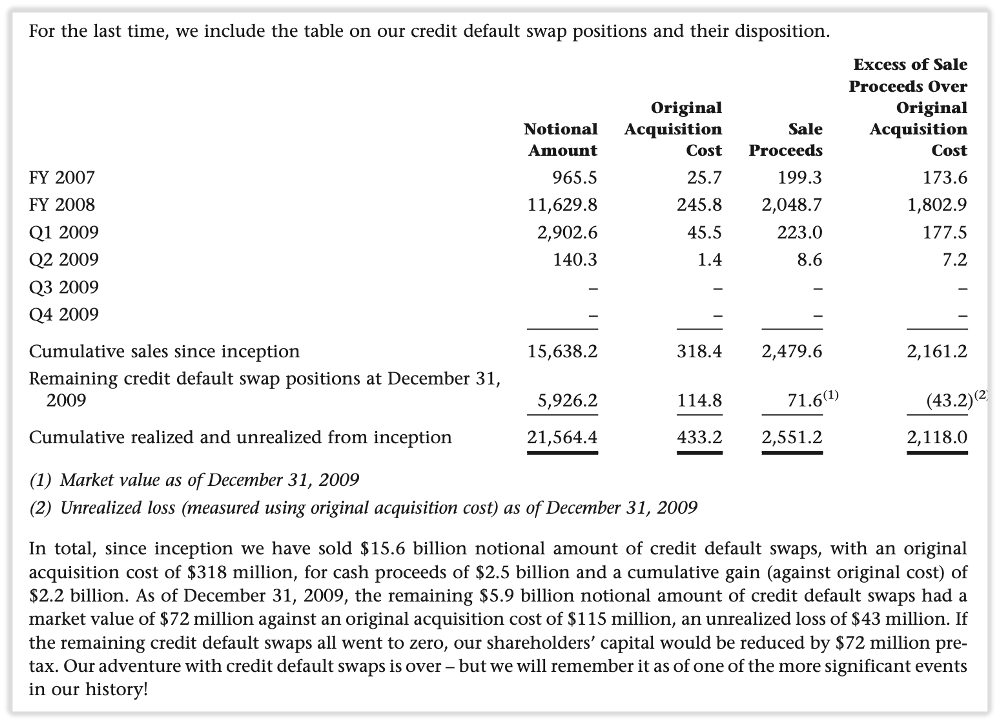

Credit Default Swaps (2005-2009): Fairfax's Version of The Big Short I am finally getting around to updating parts of my book. This is a fun one. “Sizing is 70% to 80% of the equation. It’s not whether you’re right or wrong, it’s how much you make when you’re right and how much you lose when you’re wrong.” Stanley Druckenmiller In The Big Short, Michael Lewis tells the story of a small group of investors who recognized the risks building in the U.S. housing market and positioned themselves to profit when the system eventually broke. The best-known participants were Michael Burry at Scion Capital, Steve Eisman at FrontPoint Partners, and Charlie Geller and Jamie Shipley at Brownfield Capital. A small Canadian property and casualty insurer could easily have been added to that list. Fairfax Financial. While the investors featured in The Big Short purchased credit default swaps tied directly to subprime mortgages, Fairfax built a broader portfolio of protection against systemic financial risk. The objective, however, was similar: profit from — and protect against — a severe disruption in the financial system. The trade would become one of the most successful investments in Fairfax's history. Insurance Against a Financial Crisis A credit default swap (CDS) is essentially insurance against default. The buyer pays a premium, and in return the seller agrees to compensate the buyer if a specified company or security experiences a credit event such as bankruptcy or default. The attraction of a CDS is its asymmetry. If nothing happens, the buyer loses only the premium paid. If credit conditions deteriorate, the value of the CDS can increase many times over. In The Big Short movie, a large investor in Burry's fund summed up the trade perfectly: “In other words, we lose millions until something that has never happened before happens?” Burry replied: “That's right.” That was essentially Fairfax's position. Management believed the global financial system was becoming increasingly fragile. Credit standards were deteriorating, leverage was rising, and financial institutions were taking risks that were poorly understood by both regulators and investors. As Fairfax explained in its 2005 Annual Report: “The company has invested approximately $250 in 5-year to 10-year credit default swaps on a number of companies, primarily financial institutions, to provide protection against systemic financial risk arising from financial difficulties these entities could experience in a more difficult financial environment.” Fairfax 2005AR The original concern centered on Fairfax's reinsurance counterparties. If a severe financial crisis occurred, would the institutions Fairfax relied upon remain financially sound? As management dug deeper, they discovered that many of these firms had significant exposure to mortgage-related assets and other risky securities. The more they researched, the more protection they purchased. Fairfax began building its CDS position in 2002 and continued adding through early 2007. Looking Wrong Before Being Right Initially, the trade appeared to be a mistake. The position was expensive to carry and Fairfax recorded losses of approximately $102 million in 2005 and another $76 million in 2006 as credit spreads tightened and financial markets continued to strengthen. Like Michael Burry, Fairfax looked wrong for several years before it was ultimately proven right. By 2006, however, cracks were beginning to appear in the U.S. housing market. Early in 2007, conditions deteriorated rapidly. Fairfax responded by increasing its CDS exposure. Then the financial system began to unravel. The Payoff As credit spreads widened and financial institutions came under increasing pressure, the value of Fairfax's CDS positions surged. By the end of 2007, Fairfax had recorded approximately $1 billion in gains. Another $1 billion followed in 2008 as the financial crisis intensified. Most of the positions were sold during 2008 and early 2009, locking in extraordinary profits. In total, Fairfax invested approximately $433 million and realized gains of roughly $2.1 billion. For perspective, Fairfax's common shareholders' equity at the end of 2008 was approximately $4.9 billion. The CDS trade materially strengthened the company's balance sheet at one of the most difficult periods in modern financial history. How did Fairfax compare with some of the investors featured in The Big Short? Scion Capital: approximately $2.7 billion FrontPoint Partners: approximately $1 billion Brownfield Capital: approximately $50 million Fairfax Financial: approximately $2.1 billion Fairfax sized the position exceptionally well. The Impact on Shareholders Shareholders were major beneficiaries. From 2005 to 2009, Fairfax shares increased approximately 174%, while the S&P 500 declined 11%. During one of the most challenging periods in modern financial history, Fairfax dramatically outperformed the broader market. Lessons for Investors The CDS trade highlights several characteristics that have long defined Fairfax. First, Fairfax excelled at risk management. The original purpose of the CDS position was not speculation. It was protection against a financial crisis that management believed was becoming increasingly likely. Second, management was willing to follow the evidence wherever it led, even when that meant taking a highly contrarian position. Third, Fairfax demonstrated patience and temperament. The trade generated losses for years before producing extraordinary gains. Finally, Fairfax sized the opportunity aggressively. Identifying a great investment is important, but as Druckenmiller observed, returns are often driven as much by position size as by being right. Fairfax continued adding to the position as the evidence strengthened and the opportunity improved. The CDS trade ultimately delivered both protection and enormous profits. More importantly, it revealed the core strengths of Fairfax's investment culture: independent thinking, deep research, patience, conviction, and a willingness to act when risk and opportunity are mispriced. Those qualities helped Fairfax execute one of the greatest investments in its history. ---------- COBF and the Trade of a Lifetime The period was also memorable for members of the Corner of Berkshire & Fairfax (COBF) investing forum. At the time, Fairfax was the target of a high-profile short attack and its shares traded at what many forum members believed was a deeply discounted valuation. Many investors on the forum understood Fairfax's CDS position and recognized its potential value. As conditions in the U.S. housing market deteriorated, they believed Fairfax was likely to generate enormous gains if a financial crisis unfolded. Yet the stock price appeared to reflect little of that possibility. As a result, a number of forum members made concentrated investments in Fairfax shares during 2005 and 2006. A few went even further, purchasing long-dated call options (LEAPS) on Fairfax stock, which traded on the NYSE at the time. For some, it became the investment of a lifetime. ---------- Brian Bradstreet Explains the CDS Trade The following excerpt is from Fair and Friendly: The First 25 Years of Fairfax (2010). Bradstreet explains how Fairfax's concern about reinsurance counterparties eventually led to one of the most successful investments in the company's history. When I looked at that, I got scared. The more I looked into those reinsurance companies, the more scared I got. The investment markets were bubbly. There was a lot of crazy risk-taking. We ourselves on the fixed-income side were being offered Ponzi-type stuff that came with an AA or AAA rating. So I began to fear that the reinsurance companies we were relying on to pay us might buy this junk and get into trouble and we wouldn't get paid. That would blow us right out of the water. And so I asked, How can we protect ourselves? With the help of our analysts, I started researching all these reinsurance companies to see how many treasury bonds they did or didn't own. If they owned a lot, I could rest easy. If they didn't own a lot, that meant they might not be able to pay us. What we found was that pretty well all of them, including the best of them like AIG, were taking enormous risks. That was our initial screening. Then we started to dig more, company by company, and we realized they owned all these asset-backed, mortgage-backed, high-yield bonds, which were pronounced as safe as treasury bonds but were in fact pure risk. One way to protect ourselves was to buy credit default swaps (CDSs), which were just appearing on the market around this time. They were basically bankruptcy insurance on the reinsurers. But I soon realized that we couldn't buy enough contracts on enough reinsurance companies to be diversified and fully protected. Then it occurred to me, Why don't we buy protection on the companies that are standing behind what the reinsurance companies are buying? If I was worried about the high-risk mortgage business, for example, why not buy insurance on the mortgage insurers in the United States? So we did. The next step was to buy insurance on the mortgage-lending companies like Fannie Mae and Freddie Mac, which were supposed to be government-backed but weren't in legal terms. Fannie Mae, for example, had $80 of exposure for every $1 of common equity, so it was a very good bet to fail. We bought our first contracts in 2003 and our last ones in December 2007. We just kept buying more and more, first five-year, then seven-year, because they were so cheap. By the end of 2006 we had invested $276 million in CDSs that the market valued at $72 million. At any other place I would have been kicked out on the street. Not here though. I remember going into an investment committee meeting where Prem asked, "What's the best idea we've got?" Francis Chou, who's a pretty shy guy, piped up, "Buy more credit default insurance." I didn't have the guts to say it. Brian Bradstreet – Source: Fair and Friendly: The First 25 Years of Fairfax ---------- In Fairfax's 2009 Annual Report, Prem Watsa closed the chapter on the company's credit default swap strategy. Fairfax had invested approximately $433 million and generated cumulative gains of roughly $2.1 billion, making it one of the most successful investments in the company's history. The trade protected Fairfax during the financial crisis, materially strengthened its balance sheet, and helped position the company for the years that followed. As Prem noted, it would remain "one of the more significant events in our history."

-

That is how I look at it. I think higher interest rates were a modest headwind to Q1 results. The benefit from IFRS < the hit to the carrying value of the bonds (please correct me if this is wrong). Higher interest rates means investment that roll off can be reinvested at higher rates (than what was available 6 months ago when rates were materially lower and expected to go lower). This is a positive for interest income. Although the actual impact on interest income depends on the rate that was being earned on the bonds that are rolling off. Another important consideration is the bigger picture. Higher bond yields likely impacts pricing in the insurance market - in a bad way (accelerates the soft market). The bottom line, there are many variables at play. Sometimes the result is a tailwind. Other times it is a headwind. What matters is how they sum together. And then of course, timeframe matters. What is a headwind this quarter might turn into a tailwind looking out 1 or 2 years. It is very difficult for an investor to understand/model all of the puts and takes. Of course, Fairfax does this. As a result, it really boils down to "Do you trust management?" I do today. (For those who think have blinders on I didn't from about 2012 to 2019. I try and be as fact based as possible.)

-

In a rising interest rate environment, duration matters. Having a short duration portfolio results in a smaller hit to the balance sheet (than having a longer duration portfolio). I really like how Fairfax is positioned today with its bond portfolio.

-

@Maverick47, I agree. Thorndike's book is insightful in so many different ways. Fairfax also seems to have figured out in recent years the “other masters of capital allocation.” They are partnered with a pretty talented group. Another interesting angle: success begets success. In important respects, Fairfax is just getting started. When you do capital allocation well, compounding and time becomes even more powerful… that whole snowball thing.

-

The key to understanding Fairfax over the past 5 years has been following their capital allocation decisions. Not the historical operating metrics. One reveals the future. The other communicates the past. This is as true today as it was in 2020. Many of the traits that Thordike identified that make a successful CEO also - not surprisingly - make a successful investor. Such as "think independently."

-

The Outsiders - by William Thorndike: In Search of the Great CEO, Company and Stock - Part II Part II has three components: Conclusion to the article above Appendix: The Outsider Paradox - Top Performance, Cheapest Stock Applying the Outsider Framework to Prem Watsa and Fairfax ------------- The Search for the Next Outsider For investors, the enduring value of The Outsiders is not the stories of eight exceptional CEOs. It is the framework Thorndike developed for identifying them. 1. Start With the Objective The Outsiders focused on a single goal: maximizing long-term value per share. They did not optimize for revenue growth, earnings growth, corporate size, or prestige. Every important decision was evaluated through the lens of whether it increased value on a per-share basis. 2. Evaluate Capital Allocation Capital allocation was their defining skill. How has management invested cash flow? When have they repurchased shares? Have acquisitions been disciplined? Was debt used prudently? Have they issued equity intelligently? Over time, a surprisingly small number of decisions can have an outsized impact on shareholder returns. 3. Look for the Right Principles The Outsiders followed a remarkably consistent playbook. They focused on cash flow rather than accounting earnings, thought independently, repurchased shares aggressively when undervalued, remained patient with acquisitions, and used leverage selectively and intelligently. These principles shaped both operating performance and capital allocation. 4. Study the Culture The Outsiders built decentralized organizations that empowered managers, encouraged entrepreneurship, and rewarded owner-like behaviour. Headquarters remained lean, bureaucracy was minimized, and decision-making was pushed downward. Over time, this culture became a competitive advantage. 5. Assess Temperament Perhaps the most important factor is temperament. The Outsiders were rational, analytical, patient, independent, and willing to be different. They behaved like owners and made decisions based on facts rather than consensus. Thorndike's most important insight may be that exceptional CEOs often do not look exceptional. They are rarely the most charismatic, visible, or celebrated leaders. In fact, many are overlooked because Wall Street tends to focus on quarterly earnings, operating metrics, and short-term forecasts rather than capital allocation and long-term value creation. The irony is that the characteristics that make Outsider CEOs successful often make them difficult to identify. Their companies can be complex, unconventional, and occasionally misunderstood. Yet those same traits frequently create opportunities for patient investors. More than a decade after its publication, The Outsiders remains one of the most useful frameworks available for identifying exceptional management teams and businesses. The challenge is not finding companies that look successful today. It is identifying management teams that can create extraordinary value per share over the next decade. ----------- Appendix: The Outsider Paradox — Top Performance, Cheapest Stock One of the most surprising findings in The Outsiders is that many of the best-performing companies often traded at lower valuations than their peers. At first glance, this seems illogical. If these CEOs were exceptional capital allocators, shouldn't investors have rewarded them with premium valuations? Often, they did not. Different Objectives The explanation lies in a fundamental mismatch between what Outsider CEOs were trying to achieve and how Wall Street typically evaluates companies. Outsider CEOs focused on maximizing long-term value per share. Wall Street focuses primarily on quarterly results. These are not the same thing. Many of the decisions that create the most value over a decade can make short-term results less predictable. Share repurchases, acquisitions, asset sales, tax strategies, balance sheet decisions, and opportunistic investments often take years before their full impact becomes visible. As a result, Outsider-led companies frequently looked different from their peers. They were often more complex, more opportunistic, and less concerned with meeting quarterly expectations. Most importantly, they refused to manage their businesses for appearances. The Capital Allocation Blind Spot Wall Street's analytical framework naturally emphasizes variables that can be measured and modeled quarter by quarter: revenue growth, margins, earnings, underwriting results, and other operating metrics. Capital allocation is different. Its impact is often measured over five or ten years, not five or ten weeks. Yet Thorndike's research suggests that capital allocation decisions frequently have a greater influence on long-term shareholder returns than operating decisions. This creates an uncomfortable reality: one of the most important drivers of long-term performance is also one of the hardest things to analyze. As a result, it often receives less attention than it deserves. Why Discounts Persisted Wall Street prefers businesses that are simple, predictable, conventional, and easy to model. Many Outsider companies were the opposite. Their structures were more complex. Their strategies were unconventional. Their results could be lumpy. And their CEOs typically spent little time cultivating analysts, investors, or the financial media because they viewed those activities as a poor use of time. As a result, these companies were frequently misunderstood, occasionally controversial, and periodically out of favour. That often led to valuations that failed to reflect the quality of the underlying business. The Final Twist Ironically, undervaluation often became another source of shareholder returns. A misunderstood company frequently has a cheap stock. And a cheap stock gives a skilled capital allocator the opportunity to repurchase shares at highly attractive prices. The very characteristics that made Outsider companies difficult for Wall Street to understand often became an additional driver of long-term performance. That is the Outsider Paradox. The qualities that helped these CEOs generate extraordinary long-term returns were often the same qualities that caused their companies to trade at discounts in the first place. In many cases, those discounts did not hinder shareholder returns. They amplified them. ------------- Applying the Outsider Framework to Prem Watsa and Fairfax The value of The Outsiders lies in the framework. William Thorndike identified a set of characteristics that repeatedly appeared in exceptional CEOs and capital allocators. The obvious question for investors is whether those same characteristics can be found in companies today. Fairfax Financial provides an interesting case study. 1. Start with the Objective For more than four decades, Fairfax has focused on growing long-term value per share rather than maximizing earnings, revenue, or corporate size. The results speak for themselves. Fairfax has compounded its share price at approximately 19% annually (US$, including dividends) over forty years. Like the Outsiders, management appears to measure success by the value created for each share rather than the growth of the enterprise itself. This distinction may sound subtle, but it influences every important capital allocation decision the company makes. 2. Evaluate Capital Allocation This is Watsa's defining strength. Thorndike's Outsiders viewed capital allocation as their most important responsibility. Fairfax operates much the same way. Over the past decade, capital has been allocated across insurance operations, fixed income, equities, acquisitions, divestitures, and share repurchases with unusual flexibility and discipline. Larger recent examples include: Acquiring Brit, Allied World, and other insurance businesses during a soft insurance market, effectively doubling the size of the insurance platform. Selling ICICI Lombard in 2017 while simultaneously seeding Digit Insurance, a move that transformed one successful investment into another. Expanding aggressively during the hard insurance market from 2019 to 2025, roughly doubling the size of the insurance business again. Initiating Fairfax total return swaps in late 2020 and early 2021, gaining exposure to 1.96 million Fairfax shares at an average cost of approximately $373 per share. Reducing bond duration ahead of the sharp rise in interest rates in 2022, protecting book value while positioning the company to benefit from higher reinvestment yields. Selling the pet insurance business in 2022 for $1.3 billion, generating an after-tax gain of approximately $1.0 billion. Repurchasing 7.1 million shares over the past 8.25 years, reducing the share count by 25.7%. Holding Eurobank through a multi-year recovery, generating approximately $4.8 billion of value. Monetizing a portion of the Poseidon/Seaspan investment in 2026, realizing an $837 million gain after years of patient ownership. Another characteristic that stands out is Fairfax's willingness to partner with talented operators and capital allocators and then give them significant autonomy. Like many of Thorndike's Outsiders, Watsa appears more interested in allocating capital than managing day-to-day operations. 3. Look for the Right Principles Fairfax consistently exhibits many of the principles Thorndike identified. Management thinks independently, acts opportunistically, focuses on economic value rather than accounting optics, repurchases shares when they trade below intrinsic value, and remains patient when attractive opportunities are scarce. Most importantly, capital allocation is not a supporting function at Fairfax. It is central to the business model. 4. Study the Culture Watsa thinks and acts like an owner. Most of his net worth remains invested alongside shareholders, creating strong alignment between management and owners. Fairfax's communications consistently emphasize long-term value creation, capital allocation, and per-share results. The organization is also highly decentralized. Operating managers are given significant autonomy, headquarters remains lean, and decision-making is pushed down to the operating level. These are characteristics Thorndike repeatedly observed among his Outsider CEOs. 5. Assess Temperament Perhaps the strongest similarity is temperament. Throughout its history, Fairfax has repeatedly made decisions that were unpopular, unconventional, or early. The company expanded aggressively during soft insurance markets, invested heavily in Eurobank when Greece was deeply out of favour, shortened bond duration ahead of rising rates, and repurchased shares aggressively when Fairfax traded at a substantial discount to intrinsic value. These decisions reflected a willingness to follow the economics rather than the crowd. That willingness to be different is one of the defining characteristics of an Outsider. Verdict Thorndike's framework was designed to identify exceptional capital allocators. When Fairfax is evaluated through that lens, the similarities are difficult to ignore. The company is focused on long-term value per share. Capital allocation sits at the centre of the corporate strategy. Management behaves like owners. The culture is decentralized. Decision-making is rational, opportunistic, long-term in nature, and often unconventional. Most importantly, the results are consistent with the framework. Over four decades, Fairfax has compounded shareholder wealth at approximately 19% annually while displaying many of the same behaviours Thorndike observed in his original group of Outsider CEOs. Performance alone does not make a company an Outsider. What distinguished Thorndike's CEOs was the combination of exceptional results, disciplined capital allocation, shareholder alignment, rational decision-making, and the temperament to act differently when circumstances demanded it. By that standard, Prem Watsa and Fairfax belong in the conversation. Fairfax's forty-year record places it firmly in the same league as the companies profiled in The Outsiders. And when evaluated against the framework Thorndike developed, Prem Watsa and Fairfax appear to check virtually every box. If The Outsiders were written today, Fairfax would be difficult to leave out. P.S. In 2015, when asked to identify contemporary CEOs who fit the Outsider mold, William Thorndike included Prem Watsa and Fairfax among his examples (Talks at Google, approximately the 31:15 mark). More than a decade later, the evidence appears considerably stronger.

-

The Outsiders - by William Thorndike: In Search of the Great CEO, Company and Stock - Part I "It is impossible to produce superior performance unless you do something different." John Templeton Among the hundreds of investing and business books published over the years, few have earned the reputation of The Outsiders. Written by William Thorndike and highly recommended by Warren Buffett, the book examines a deceptively simple question: What makes a great CEO — and how can investors identify one before the rest of the market does? The answer challenges much of what investors, business schools, corporate boards, and Wall Street traditionally believe about leadership and corporate success. More than a decade after its publication, The Outsiders remains one of the most valuable studies ever written on capital allocation, leadership, and long-term shareholder value creation. The Study Thorndike approached the problem differently than most business writers. Instead of studying popular CEOs, admired companies, or management theories, he started with a measurable outcome: long-term shareholder returns. His logic was straightforward. If the primary responsibility of a CEO is to create value for owners, then the most useful measure of performance is the return earned by shareholders during that CEO's tenure. To qualify for inclusion, a CEO had to clear two hurdles. First, the company had to generate exceptional returns relative to the broader market. Second, it had to materially outperform industry peers. The second hurdle was particularly important. Companies operating in the same industry are generally dealt a similar hand. They face many of the same competitive pressures, economic conditions, and regulatory constraints. When one company consistently outperforms its peers across multiple business cycles, investors should pay attention. Thorndike also insisted on long measurement periods—typically fifteen years or more. This reduced the role of luck and ensured results reflected decisions made across multiple economic and market cycles. ----------- The Winners Thorndike's search ultimately identified eight extraordinary CEOs: Tom Murphy — Capital Cities Broadcasting Henry Singleton — Teledyne Bill Anders — General Dynamics John Malone — TCI Katharine Graham — Washington Post Bill Stiritz — Ralston Purina Dick Smith — General Cinema Warren Buffett — Berkshire Hathaway Collectively, these CEOs generated shareholder returns of roughly 20% annually over exceptionally long periods while dramatically outperforming both the S&P 500 and their industry peers. The performance was remarkable. What made the study enduring, however, was not the outcome but the pattern behind it. These CEOs operated in different industries, faced different circumstances, and possessed very different personalities. Yet despite those differences, they consistently approached capital allocation in much the same way. That common framework is the real subject of the book. ----------- The North Star: Long-Term Value Per Share The most important lesson from The Outsiders is that all eight CEOs shared the same objective. They focused on maximizing long-term value per share. This sounds obvious, but it is not how most companies are managed. Many CEOs focus on revenue growth, earnings growth, market share, asset growth, or corporate size. While those metrics may matter, they are not the same as creating value for shareholders. A company can grow earnings while destroying value if it issues too many shares, overpays for acquisitions, misuses debt, or reinvests capital at poor returns. Conversely, a company can create substantial shareholder value without becoming significantly larger. The Outsiders understood this distinction. They were not trying to build the biggest company. They were trying to increase the value of each share. That was their North Star. ------------ Capital Allocation: The Mechanism The strongest common thread across all eight CEOs was capital allocation. Thorndike's central conclusion is that a CEO's most important responsibility is not operating the business. It is deciding what to do with the capital the business generates. Every CEO has two jobs. The first is operational: running the business efficiently. The second is financial: allocating capital intelligently. Most executives spend their careers preparing for the first role. Few spend much time preparing for the second. Yet over long periods, capital allocation often has the greater impact on shareholder returns. Capital can be raised through operating cash flow, debt, or equity. It can then be deployed in five basic ways: reinvestment, acquisitions, dividends, debt reduction, or share repurchases. Every dollar can only be used once. The CEO's job is to determine which use creates the greatest increase in long-term value per share. The Outsiders approached these decisions as investors. Acquisitions were not empire-building exercises. Debt was neither inherently good nor bad. Dividends were not sacred. Share repurchases were not automatic. Every decision was evaluated through the same lens: price, value, alternatives, and expected return. At its core, capital allocation is simply the process of exchanging one asset for another and asking: How much value are we giving up, and how much value are we receiving in return? ----------- Why Most CEOs Struggle with Get Capital Allocation Thorndike's work is important because capital allocation is a surprisingly rare skill. Most CEOs spend their careers learning how to operate businesses, not allocate capital. They learn how to manage people, improve operations, grow sales, and execute strategy. Those abilities are essential. But they are not the same as deciding whether to repurchase stock, issue equity, acquire a competitor, pay down debt, or simply hold cash. Buffett and Munger often criticized business schools for teaching finance as a theoretical discipline focused on formulas and models rather than intrinsic value, opportunity cost, and owner-oriented decision making. The Outsiders approached capital allocation differently. They thought like investors first and managers second. Every decision was evaluated from the perspective of the shareholder, not the corporation. That distinction explains much of their success. ------------ The Pattern: A Few Big Decisions Matter One of the more surprising lessons from The Outsiders is that exceptional capital allocation rarely looks busy. The best CEOs were not constantly making deals, restructuring businesses, or announcing major initiatives. In many cases, decades of outperformance could be traced back to a surprisingly small number of decisions. Long periods of patience were often followed by brief periods of decisive action. They waited when opportunities were scarce and moved aggressively when the odds shifted decisively in their favour. That combination of patience and conviction appeared repeatedly throughout Thorndike's study. It is also one of the clearest lessons for investors today. ------------ A Shared Set of Principles Beyond capital allocation, Thorndike identified a common set of principles that appeared repeatedly across the eight Outsider companies. Emphasize Cash Flow Over Accounting Earnings The Outsiders focused on cash flow rather than reported earnings. Their objective was to maximize the cash generated by the business and then allocate that capital intelligently. Strong operations produced more cash. Superior capital allocation compounded it. Over time, the two reinforced one another. Build Decentralized Organizations The Outsiders operated with lean headquarters, flat organizational structures, and empowered front-line managers. Rather than concentrating authority at head office, they pushed decision-making closer to the customer and the business. The benefits were significant. Decentralization encouraged entrepreneurship, rewarded initiative, and attracted managers who thought and acted like owners. Over time, this became a powerful cultural advantage, leading to stronger businesses, lower costs, less bureaucracy, and better operating results. Think Independently These CEOs relied primarily on their own analysis rather than Wall Street opinion, consultants, or conventional wisdom. They were analytical, data-driven, and willing to reach conclusions that differed from the consensus. That independence often allowed them to see opportunities others missed. Practice Disciplined Share Repurchases Few areas better illustrate the difference between Outsider CEOs and conventional managers than share repurchases. Most companies buy back stock when business conditions are strong and valuations are high. The Outsiders often did the opposite. When their shares became materially undervalued, they repurchased stock aggressively and, at times, in extraordinary amounts. Henry Singleton's repurchases at Teledyne remain one of the greatest examples of capital allocation in corporate history. By retiring a massive percentage of the company's shares when they were deeply undervalued, he created enormous value for remaining shareholders. Be Patient with Acquisitions The Outsiders felt no need to be constantly active. They waited for attractive opportunities and acted only when the economics were compelling. When those opportunities appeared, however, they were willing to move decisively and at scale. Use Leverage Intelligently Most of the Outsiders employed leverage at various points in their careers, but they did so thoughtfully and selectively. Some used conventional debt. Others benefited from unique forms of leverage, such as insurance float. In each case, leverage was matched to the predictability of cash flows and the resilience of the underlying business. The Outsiders understood that leverage can amplify both gains and losses. Used recklessly, it can destroy value. Used intelligently, it can significantly enhance long-term returns. Leverage was a tool to increase value per share—not a strategy in itself. How the Principles Worked Together These principles were not independent. They reinforced one another. Strong cash flow created financial flexibility. Decentralization improved operating performance. Independent thinking enabled unconventional decisions. Patience prevented value-destructive acquisitions. Intelligent use of leverage provided additional capital. Together, they formed a coherent system for compounding long-term value per share. ------------ The Personality Traits - A Different Kind of CEO The Outsiders shared more than a common approach to capital allocation. They also shared a remarkably similar temperament. They were not the CEOs who typically attract public attention. Few were described as charismatic visionaries. Most avoided the spotlight and had little interest in cultivating a public image. They spent minimal time with analysts, journalists, and management gurus. Few appeared on magazine covers. None became celebrity CEOs. Instead, they were known for a different set of qualities: rationality, analytical thinking, frugality, pragmatism, flexibility, patience, humility, independence, and integrity. They were opportunistic when circumstances warranted it, contrarian when the facts supported it, and bold when the odds were in their favour. Several came from engineering or quantitative backgrounds. All eight were first-time CEOs. More than half were under forty when they assumed the role. Only two held MBAs. These traits mattered because superior capital allocation often requires making uncomfortable decisions. Repurchasing shares during periods of pessimism, making acquisitions during downturns, holding cash while competitors are expanding, or ignoring prevailing market opinion all require a combination of analytical conviction and emotional discipline. The defining characteristic was independent rationality. For investors, this may be one of Thorndike's most important insights. The Outsiders' advantage was not simply that they understood capital allocation better than their peers. They possessed the temperament required to execute those ideas consistently over decades. They looked ordinary. Their results were extraordinary. Keep reading for Part II

-

@Hamburg Investor, great post. I found reading the two books produced by Odyssey and C&F to be quote helpful in providing a historical perspective on insurance (what has been going on under the hood). One of the challenges with Fairfax is understanding just how much has changed over the past 10 years - it really is staggering (insurance, investments, capital allocation, earnings etc). (I mean this in a good way.) And it is continuing…

-

Yes, having a shareholder friendly management team is also important (in terms of who ultimately gets rewarded over the long term).

-

Paradoxically, being perpetually undervalued becomes one of the drivers of outperformance. It is very counterintuitive. I am reading The Outsiders by William Thorndike. Many of the Outsider companies went through periods when their stock was cheaper than peers - even though their performance over the long term was much, much better than peers. Outsider CEOs/companies are like great artists… they are mostly celebrated in posterity.

-

On Public vs Private: And joining Berkshire allows Taylor Morrison to hop off the Wall Street treadmill. The weight of analyst expectations and public guidance would take a toll on anyone. “If you were to really be honest about it,” Palmer told Fortune, “sometimes I feel [like] I live my life in six week increments. Earnings, call a board meeting, earnings, call a board meeting. It’s a treadmill you’re on twenty hours a day.” This relentless quarterly cadence compresses long-cycle businesses into short-cycle reporting — a structural mismatch that can distort decision-making for even the most disciplined operators. Happily, becoming part of Berkshire changes all that. “I think one of the things we’re so excited about is homebuilding runs in five-, seven-, ten-year cycles,” she said last week. “Berkshire thinks in seven-, ten-year, or longer cycles. That alignment is rare.”

-

@gfp, thanks for the colour. I guess this also means Blue Ant shifts from being an associate holding (22.5%) to a mark to market holding (19.9%)? Regardless it is a very small holding for Fairfax. Just thinking about my equity tracker…

-

@boilermaker75 and @73 Reds and @pine, thanks for sharing. My three kids started down a similar path 4 years ago (early 20's). Today they each have almost 100 shares of Fairfax (they have all been aggressive buyers in recent months). The kicker is in Canada we have lots of tax free accounts (FHSA, TFSA, RRSP, RESP). And capital gains are taxed at a low rate (50% of the gain is tax free). What is better than a high CAGR over 20 years? A high CAGR that is tax free. In 20 years time, I think my kids will be very happy with the result. The set-up for young people in Canada to grow wealth with financial assets is amazing.

-

I think Fairfax's P/C insurance business has changed dramatically over the past 15 years: Andy has had time to execute his vision Expanded aggressively through acquisitions from 2015 to 2017 Pivoted in India (from ICICI Lombard to Digit) Dramatically reduced the size of runoff Seeded interesting opportunities like Ki and Digit Life and Re-insurance Expanded aggressively in hard market Completed a range of 'bolt on acquisitions': Singapore Re, GIG and Albingia Began taking out minority partners: Brit and Allied World Reduced its catastrophe exposure (historically speaking) Still have the opportunity to take out minority partners in Allied World and Odyssey at very favourable prices The net result is its insurance business in 2026 is a completely different animal than its insurance business in 2011. It is remarkable all the different things Fairfax has accomplished over the past 15 years (there is a very important lesson here... Fairfax was very aggressive in growing and improving the business in a soft market...). This makes it very difficult to use historical numbers for insurance for Fairfax that are pre-2011 (CR etc). So let's look at the past 15 years. How many years did Fairfax have a CR over 100? I think it was one. And it was caused, not surprisingly, by historically large cat losses. Most of the years from 2011 to 2026, insurance was in a soft market. Hard markets are the exception. Fast forward to the next 5 years. Will Fairfax write at an average CR of 100? Absent a historic level of catastrophes over multiple years, I don't see it. Not as a baseline forecast. Importantly, there is a high likelihood that reserve releases will trend higher than normal in the coming years (on average - with some volatility by quarter). That is usually what happens when we come out of a hard market. This will be a tailwind to the CR. Again, I just don't see how we get an average CR of 100 over the next 5 years. Building that into a baseline forecast isn't being conservative - it looks extremely bearish. And I am not sure how that approach ever leads to optimal results for an investor.

-

+1