SafetyinNumbers

-

Posts

2,814 -

Joined

-

Last visited

-

Days Won

37

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

Feedback has been that generally people didn’t like this interview so what questions do you think could have made it a more interesting discussion?

-

I think it has everything to do with ROE. With the same earnings power, the company with the a large amount of intangibles will have a lower ROE vs the one without. P/BV only matters in context with ROE.

-

The buyback wouldn’t buy on the close. They usually try not to trade near the market open and close. Also can’t guarantee it’s not an uptick in the MOC facility. I understand there was a cross by Scotia earlier in the day which is more likely to be them but could also just be another Scotia client. We’ll find out by January 10.

-

EUROB was halted for a few days because they did a reorganization where they merged the holdco into the operating company. I wonder if there was a build up of passive rebalancing or something like that which caused the volatility.

-

You can ask any question you want live. They take questions from non-analysts on the conference calls as well. They also do an investor trip to India annually.

-

The difference should be captured in ROE. If you are going to switch to P/TBV then it should be compared to ROTBV as well.

-

That makes sense to me but no idea what they will do. FFH would likely put up at least another billion itself.

-

They don’t want to take it private. That’s a big difference. With an operating business, it’s always an option and often preferred. It’s been happening a lot lately because the market structure has changed such that stocks that don’t screen for quality and not in benchmarks are targets for management teams.

-

probably better to look at the dollar amount and not the percentage. They would have control as GP anyway.

-

Arguably the only reason the discount is as small as it is now is because the airport is so big. It makes it a much easier bet for institutions.

-

10% of shares outstanding a year is a crazy number to expect. It’s essentially a go private and as soon as the buying is done the discount will widen again and the buying wouldn’t have as much economic benefit. Better doing it slowly at bigger discounts.

-

IDBI can issue new equity for the CSB stake. The LPs put up the new cash. It’s not that difficult to see how it can happen. There is still going to be a public listing.

-

Not only a CEF but also a CEF of private equity investment with a sponsor unlike all of its PE peers known for using very conservative valuations. It’s easy to see in the track record that the monetized and public equities have well outperformed the private names. Are they just bad at buying private names or are they conservative in their valuation assumptions? One look at the discount rates and terminal growth rates used and it’s pretty obvious.

-

Zero chance FIH will issue equity in my opinion. They can contribute CSB in kind for IDBI shares and put up some cash.

-

I don’t think we can compare operating companies to closed end funds. Terravest stock really took off when it was insight of being added to the TSX Composite. FIH has no hope of that. ELF, UNC and EVT are closer to FIH and they have done buybacks, capital return and stock splits but the discount hasn’t closed much because there is no passive demand and active investors have high return expectations.

-

What are some Canadian examples? Is it percentage of shares outstanding that matters or percentage of float.

-

Why would it ever liquidate assuming FFH is still around?

-

FIH does get dividends from its portfolio companies. BIAL has the potential to start paying a dividend in 2029 when its latest capital program is complete which will help with new investments and buybacks.

-

Isn’t that what margin of safety is?

-

You are correct! My mistake. I changed it above and acknowledged your help. The commentary on the over/under of a 20% CAGR is still interesting though as clearly most investors expect less than that.

-

What over/under would you set for forward 5 year returns? I don’t think this is true mathematically. Buying stock below book increases BVPS while earnings power stays the same means a lower ROE all else being equal. Obviously, it’s still better than buying above BV because the goal is to compound BVPS faster. We disagree on the odds of things generally but I think a good approach for anyone else analyzing forward returns is to spend time thinking about what’s needed to create a 15-20% ROE using the framework below on an reported basis. I emphasize reported basis because while Eurobank stock has gone up a lot since 2020, for example, we have only booked our share of their earnings but none of the multiple expansion so that’s all future ROE as we sell our proportionate share into their buyback over the next 5 years.

-

Short rates are falling. Long rates not much yet. Plus they have duration locked in for a few years and they might be in the process of stepping up lending against real estate with the KW deal. If credit spreads widen over the next 5 years at some point, that could supercharge returns given the leverage. Parts of the market are softening. Float growth will slow but float per share might still go up as they use less reinsurance and buy in minority interests at Allied World and Odyssey. Their share of Ki will also go up as the Class C shares are extinguished on IPO. Ki is obviously a big one on the insurance side. The TRS are continuing. Goodwill amortization and purchases of stock above book value lower equity meaning the same earnings result in a higher ROE all else being equal. Cats are a smaller portion of the business than before. Partially because they have grown other lines but also because they are more global than before. Cats ticking up would just help pricing anyway so they would make it up pretty quickly on price if we are using a 5 year window. BIAL, Poseidon and Eurobank still have carrying values well below fair value. There likely a few more of those like AGT, Dexterra etc… plus the stuff they own is still growing. SCR and GFR could provide very big gains if oil prices stay flat but a lot more if the oil price goes to $80+. As discussed above. Buybacks above BV boost forward ROE. We agree that Fairfax is defensive and a dislocation can boost forward returns making the 20% bogey more likely. Anyway, that’s what makes a market.

-

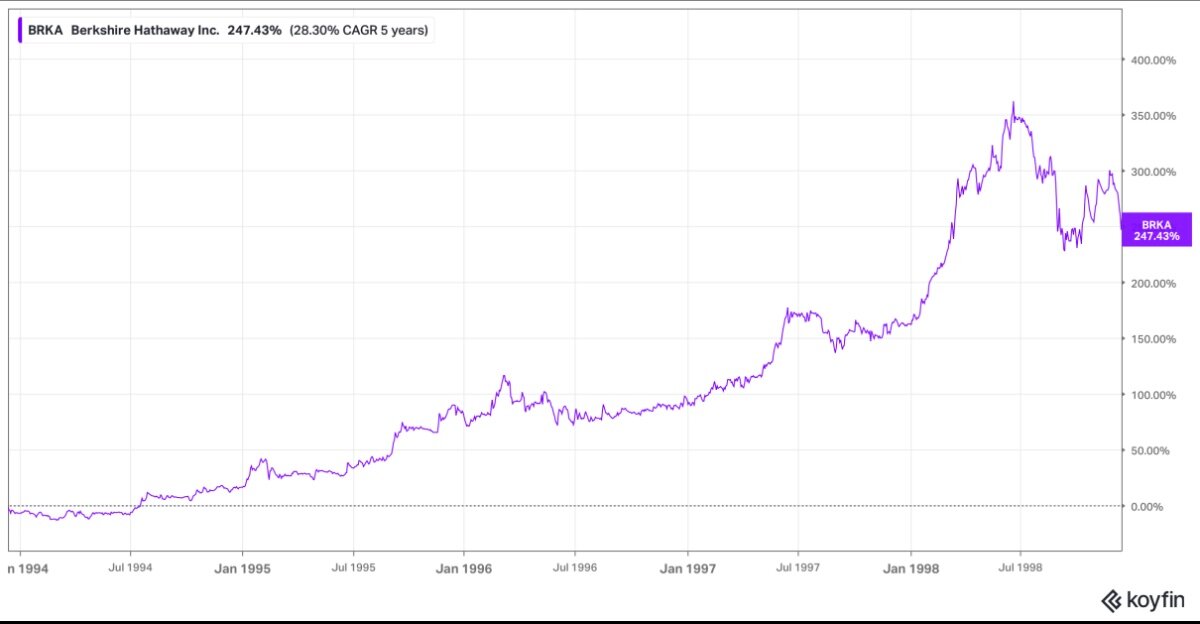

Congrats on the quote @kodiak Charlie and I were chatting about this earlier today. The forward return for BRK from Dec 12, 1993 to Dec 12, 1998 was ~247% which equates to a CAGR of ~28%. That is an excellent return and well exceeds my 10% hurdle but If that was the over/under for FRFHF over the next 5 years, I would bet the over, but it’s not an easy bet. For the 5 years ending 2025, FFH will have compounded BVPS over 20% and this seems entirely possible for the next 5 given the set up. To match Berkshire, the P/B multiple would have to expand to 2x. The right tails get interesting because the higher the CAGR in BVPS, the higher the multiple is likely to get at some point over the forecast period. I initially made an error that was corrected by @Marco Van Basten and miscalculated BRK’s return as a 20% CAGR over the forward 5 year period from this date in 1993. That over/under for FFH is much easier to bet the over on.

-

FIH has rights on investing every new investment outside of insurance in India so they have to be involved. My guess is a GP/LP structure where FIH is the GP. If that’s not the case, tnen they presumably would be compensated in some other way,

-

For long term investors it’s not a distraction and helps grow the network which for an entity that expects to be around forever is valuable.