John Hjorth

-

Posts

8,662 -

Joined

-

Last visited

-

Days Won

18

Content Type

Profiles

Forums

Events

Everything posted by John Hjorth

-

Blake [ @Blake Hampton ], I would certainly like to read your elaboration on that matter, - but in the AAPL topic in the Investment Ideas forum, not here. I hope you hereby pick up the glove thrown on the ground in front of you. Thank you.

-

@Blugolds, Respectfully, and for backdrop information purposes only, what is your nationality?

-

@Dalal.Holdings, Second quote of what you wrote here for my commenting, without the intent to become too political. Yes, the missing / lacking contributions to the common defence within NATO according to agreements within NATO in certain individual Western state budgets for now many years for several Western European states is a fact. And that fact is a disgrace and simply put so embarrasing for those Western European states. On that, the war in Ukraine has been a wake up call some places. The Danish Navy Officer Anders Puck Nielsen calls this concept of milking of state defence budgets over time by politicians in power 'the collection of the peace dividend'. It has come at a price, payable and due, now.

-

Here you go, attached. If what you see in those stats for you is 'living in La La Land', then so be it. The energy transition in Europe away from oil and gas started a long time before the Ukrainian-Russian war. Danish Energy Agency - Energy in Denmark 2022 - English - 20241103.pdf Danish Energy Agency - Energistatistik 2023 - Danish - 20241103.pdf

-

Thank you, @UK, So what comes first?, Ukraine getting run over, or Russian war machine running out of steam.

-

And then we have : AP News - World News [October 22nd 2024] : US defense chief promises Ukraine what it needs to fight Russia but goes no further. - - - o 0 o - - - Now how the h*ll does all that add up?

-

Like Richard [ @RichardGibbons ], I'm curious too, @mranski, What is it that you're saying about universal heathcare above, and compared to what? - I'm not sure I understand it.

-

I Need a Laugh. Tell me a Joke. Keep em PC.

John Hjorth replied to doughishere's topic in General Discussion

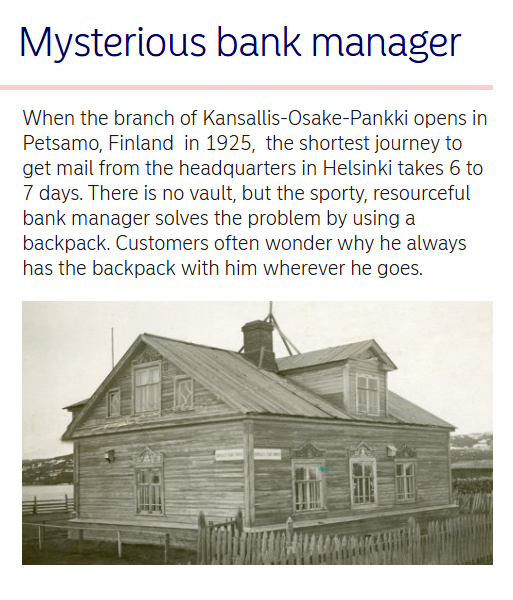

Modern banking cash management in Finland, anno 1925 or thereabout, according to the timeline on Nordeas website :

-

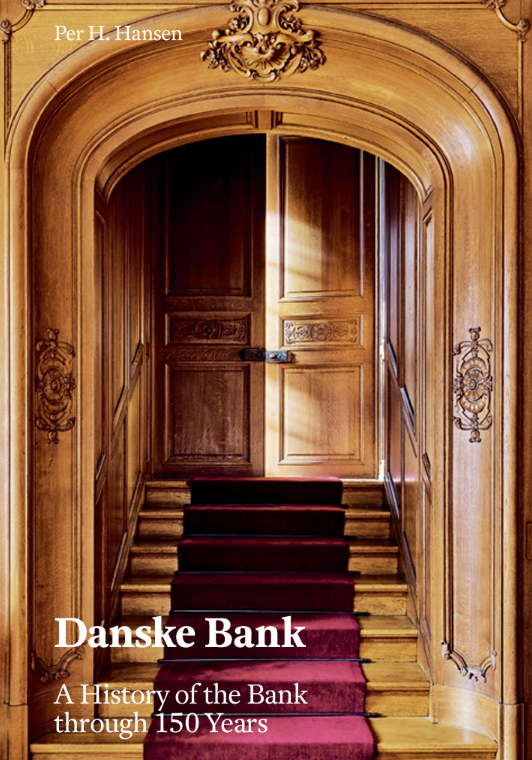

This book was released by Danske Bank A/S in June 2024, while the bank celebrated it 150 years of existence through think and thin, through tailwinds and headwinds, ups and downs. Also at that time the bank moved from its existing headquarters for 149 years in Holmens Kanal 12 i Copenhagen to its brand new premises in a newbuilt part of the centre of Copenhagen called the Post City located between Tivoli and the harbour. To me, it's an awesome book, because it's simultainously the story about the early days of Danish banking, and the industrialization of Denmark. And in the early days, the eternal, never ending competition between Isac Glückstadt, the Banker and C.F. Tietgen, the Industrialist and Entrepreneur. So far, I have only found the book available in ditgital versions, in English and Danish language, the book in English langauge can be downloaded from Danske Banks website on the page section called Our History, and the book is also attached here in both English and Danish language. - - - o 0 o - - - Edit : Today I have called Danske Bank to hear if the two language versions of the books exist in physical versions, after yesterday talking to the publisher about it, who could did not know and referred me to the bank. I turned out the books has been printed as hardbacks this year as an anniversary employeé gift, the Danish version given to all Danish employeés. On a Danish internet market place called DBA [www.dba.dk] I found the Danish version of the book, and snatched it immediately. And on eBay I found the English version in an antiquarian bookstore in a suburb NW to central Helsinki, Finland. So I suppose the English version of the hardbach was given to the Finnish employeés in the bank. I feel confident both these books will become collectors items for connaisseurs, kenners, genießer and banking nerds. Danske Bank - A History of the Bank through 150 Years - 20241101.pdf Danske Bank - bankens historie gennem 150 aar -20241101.pdf

-

I Need a Laugh. Tell me a Joke. Keep em PC.

John Hjorth replied to doughishere's topic in General Discussion

I think it's time for an old joke here : I'm this night reading "Danske Bank, A History of the Bank through 150 Years', released in June 2024 by Danske Bank. I have to say : It's great!

-

Buffett/Berkshire - general news

John Hjorth replied to fareastwarriors's topic in Berkshire Hathaway

@Charlie & @rogermunibond, Personally, I think Jim Grant in the above doesn't really hit the disc with this assessment. The calculation for Berkshire is just so different on 'riding and rolling US Treasury Bills' than for almost everyone else, because - no matter what your view may be on it - a material part of those T-Bills can be argued to be financed by insurance float. Insurance float held by the undisputed world champion in generating, holding and maintaining insurance float. It is a low margin business, yes, so it requires scale. And scale there is, indeed. -

Here is a fairly new YouTube video by Anders Puck Nielsen [Personally, he is growing on me] : YouTube - Anders Puck NIelsen [October 28th 2024] : Nuclear weapons and security guarantees for Ukraine.

-

Small initial starter position in JYSK.CPH [Jyske Bank A/S] at DKK 486.20 today. It dropped 9% today on a 2024Q3 report that was as about as expected, and on the introduction of a New Strategy, which I read as basically 'more of the same, as usual', while all analysts and commentators are screaming 'booh-booh', combined with a <thumb down>. P/B~ 0.68, P/E ~5.4, ROE ~ 13.5%, ROTCE ~ 14.8%, ongoing dividends and share buybacks, the bank running without any major challenges for now.

-

Awesome post, @Pelagic!, Thank you! We'll eventually see how this turns out, over time. I'm sure, we'll in the end eventually know, because the Russian State simply is incabable of controlling and limiting the flow of all kinds of information World Wide during a[n] <undefined> number of information channels out of control af the Russian State. [, the Russian State still 'anchored in the truth of the past'.]

-

@Warner, Thank you for sharing, and thereby providing insights to Russian thinking [, in general] to CoBF members, also presented by you in a polite manner here.

-

At least those North Korean soldiers according to the available intelligence are located in Russia, not in the by Russia occupied parts of Ukraine. Now that may perhaps eventually change at some time in the future, and what happens then? Vladimir Putin is desperate, and can't keep up momentum in the Russian warfare, so cash and transfer of military technology to North Korea against North Korea providing more meat to fodder the meat grinder. It's just a business deal between two business men, who don't give a damn about their respective citizens. Please note that South Korea is on its toes now because of this.

-

Thank you, @Spekulatius, - - - o 0 o - - - YouTube - NATO News : NATO Secretary General - Statement on the deployment of DPRK troops to Russia, 28 OCT 2024. - - - o 0 o - - - What is next? - - - o 0 o - - - Today, I looked nosy at retailing stuff [canned food stuff, normally not present here] placed on the kitchen table, delivered earlier today by nemlig.com. I got asked to keep my chopsticks off those things. It turns out The Lady of the House now has started prepping

-

Is this about the book 'Patriot', or another book, @Spekulatius ?

-

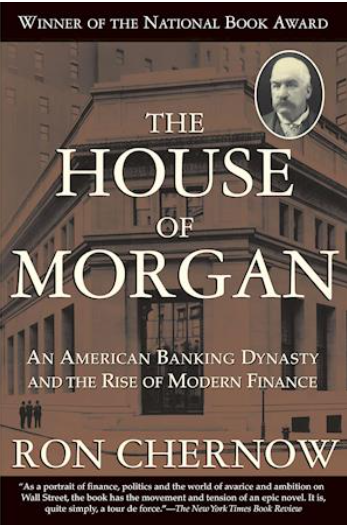

Based on an exchange about the book between Mike [ @boilermaker75 ] and @Xerxes in a topic that I intercepted by reading CoBF, I ordered the book on 15th October 2024, and it arrived at my place here in Denmark this morning. This edition is the '20th Anniversary Edition' a with a new foreword by Ron Chernow dated September 2009. [Imagine a better point in time to release a new edition?!]. For me, only available as a paperback, at a price of DKK 199.00, which I really consider ridicously cheap for a brick like this of 811 pages including indicies. By trading through the Danish Internet bookstore saxo.com I pay no p&p, because of a subscription/ membership that cost me DKK 79.00 monthly. I have never experienced a book to never arrive, which has happened from time to time earlier with i.e. Amazon and others. The history of Banking in the United States is an aweome one, and its history is actually in a way a mirror of the development and evolution of USA since banking took its beginning to what USA has evolved to be today. So I'm really looking forward to chew my way through this one during the coming winther.

-

Yup, great guy, great thoughts - at least about himself, great plans for himself, great world view - we should naturally all accommodatingly adjust to it, bending and tilting in the dust for all that and him. - - - o 0 o - - - Add to that an impeccable reputation, and you have a person - really, really - special! : Under the Olympic Winter Games in Sotji, Russia 2014, a reporter dared to ask 'the man' him self - in public - about the presence of 'small green [unmarked] men' on Crimea, where he stated those were 'self defence forces, that had nothing to do with Russia'. When futher asked and confronted with why they were driving in military vehicles clearly equipped with Russian license plates, he simply did not reply. - Works great, for a great guy!

-

This may overlap to other areas of science in general, so not only related what's going on in the pharma industry related to GLP-1 [but let's keep it here related to GLP-1] : Does any of my fellow CoBF members have any concerns and / or qualifications related to this scientific method running science alone based empirical and statistical evidence, making science 'powerfull' as a basis only by using giant samples [, because 'big pharma' has the access to the means to do so'], with the normative side of things, with regard to recognition and knowledge, running, not following similar suit, thereby leaving the question 'Why does it work?' unanswered, perhaps not even paid any really attention to? - - - o 0 o - - - Just mentioning it here : Isen't that also what AI is about? [Like : Several thousands years of evolved Chineese medicine working, without even anybody really knowing why ...]

-

Here is a thread of posts on X by former Ukrainian Minister of Economy Tymofiy Mylovanov about the above Q & A mentioned by @Spekulatius above, analyzing and digging a bit into what is Vladimir Putin actually saying here. - - - o 0 o - - - The man is totally ignoring and disregarding that he [Russia] is the agressor against Ukraine, and the decision maker triggering this war, simply alleging just and exactly the opposite, which is just brain spin in a delutional mans head, also anchored in his own world view, which is characterized, almost ravaged, by his eternal being huffy, miffed by what happened to Russia in connection with the downfall and dissolution of the Soviet Union. Everytime he says 'Russia', he actually means 'my Russia' - because he does not give a damn about the consequenses of his decisions for his own people, especially the youngsters getting killed in and by this. No relation and connection to todays realities, a world view based on '... in the old days ...', just an anachronism. He actually had an incredible , - really once-in-a-lifetime -, opportuny by his appointment about 24 years ago, where he could have taken initiative to, and being the leader of, building a competitive, advanced and modern Russia based on democracy, respect for civil rights, capitalism, rule of law and respect for capital, based on Russias enormous oil and gas reserves. His agenda eventually turned out to be the exactly opposite. The real agenda was totally different : a cleptocracy. In stead he now is actually saying that he won't settle with being a gas station manager, [in the meaning that that's not 'fine enough' for him?]. The man is totally incompetent, - and dumb as an unplaned board. - - - o 0 o - - - Another very short way to express it : He is offended, huffy and miffed by, that he is by the way he has been behaving - starting with how he internally in Russia has treated and handled his political opponents [opponents may both be co-citizens and foreigners resident in Russia] - being considered 'not house-trained' [hitting western peoples 'poo-poo - I'm holding my nose'-filter] by his constantly ongoing lying and such.

-

It's a fascinating phenomen to observe, how different the big luxury companies have evolved with regard to performance in last quarter, especially Hermes overshadowing or overshining everyone else and shooting out the lights, and Kering not doing well at all.

-

Post by Jeff [ @DooDiligence ] in the Novo Nordisk topic about the Danish Gefion project, including a video, double posting the video to here : Here is another video with NVIDIA CEO Jensen Huang at the same gathering about the Gefion project :

-

Novo Nordisk Foundation just invested approx. DKK 700 milion, together with the [Danish] Export and Investment Fund of Denmark, the fund contributing DKK 100 milllion, in a public-private partnership about Denmarks first AI supercomputer : Novo Nordisk Foundation - News [October 23rd 2024] : Denmark’s first AI supercomputer is now operational. Subtitle : New supercomputer built on NVIDIA DGX SuperPOD will accelerate research and provide new opportunities in academia and industry. - - - o 0 o - - - In need of hosting for messing around with AI? - Call Novo Nordisk Foundation! -We will likely see much more of such in the near future, I think. The first 'renters' are immediately ready!, ref. the article content. ['Those who have the ability to do it, also have the obligation.'] I can't come up with a name of a Danish hosting company, that I know of, able doing something like this.