thepupil

-

Posts

5,004 -

Joined

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by thepupil

-

Wife gets Pfizer vaccine on Monday (DC hospital, government affiliation, risky patient facing but not “front line” as in ER / ICU / covid unit) Sister got Moderna vaccine today (South Florida hospital, large hospital system, risky patient facing but not "front line" ) All the staff at my grandpa’s long term care facility have been vaccinated but I don’t think he has (he’s 94) Dad vaccinated today. He is 68 and has an autoimmune disease that makes him high risk, but that’s not why he’s getting the vaccine. He’s getting it because my sister is an employee of the hospital and the hospital is enacting a program where employees can bring in a 65+ year old of their choosing. The roll out is so weird. Mom vaccinated today because of sister's hospital employement (sister just called and asked if she could bring her in). Grandpa vaccinated today because he's 94. Wife 2nd dose today because she works in a hospital. After today, I am the last remaining in my immediate family to have not been vaccinated at least once. Just an anecdote about the vaccine rollout is. It seems pretty consistent across my friends/family that if you have work at a hospital or long term care facility or know someone who does, you're getting vaccinated or have a date (my cousin is a nurse practitioner in Tennessee at a hospital and just got hers too, my hygienist aunt in Tennessee has not gotten it yet).

-

yea, I think i understand the general rules regarding exclusive benefit/fiduciary duty as well as the general concepts of self dealing. I am just surprised there isn't an exception for money management at market terms. There very well may be. The way I interpret it, If I wanted to manage my own IRA or my immediate family's IRA for a reasonable fee such as pass through expenses + 0.5% or 1.0%, that would be a prohibited transaction and force the accounts to cease to be IRA's. There's got to be someone out there who has dealt with this? or do all the small managers here invest their IRA's separate from the funds they manage This seems pretty clear that it’s a no no https://www.richeymay.com/wp-content/uploads/2016/11/Considerations-for-IRA-Investment-into-Fund-Structures.pdf Can I invest my IRA in my own fund? A. Yes, as long as your IRA investment does not provide benefit to you personally. For example, avoiding personal benefit would include that you do not charge fees for managing the funds, do not own 50% of the fund, either personally or combined with other disqualified persons, do not use your IRA to draw in other investors, or your fund is self-sustaining without your IRA investment. Q. Can I charge fees to my family members? A. It depends on whether or not they are disqualified persons. Typically, lineal ancestors or descendants are not allowed; certain lineal ancestors or descendants of the spouse may not be allowed and other family members (i.e. cousins, brother/sister) are likely okay. For specific questions on which family members are or are not allowed, please consult tax counsel. Q. Is there a limit on the amount of retirement funds I can allow in my fund? A. Depending on the circumstances, if any class of interests in an investment entity is funded by 25% or more of retirement assets, there could be a trigger of fiduciary and prohibited transaction rules. Consult with your tax counsel or other professional familiar with these rules.

-

Yes, Reits are best in tax deferred accounts. Lots of good suggestions in this thread. Under current law REITs are pretty tax efficient in a taxable account as well, but I wouldn’t assume the 20% deduction lasts too long. https://www.reit.com/investing/investing-reits/taxes-reit-investment

-

I invest my own money as well as that of my parents and sister. I do not take compensation other than (hopefully) making my family wealthier. About 60% of my investment assets are in IRA's/HSA, and about 30% for my parents/sister. Occasionally, I contemplate forming a partnership (in 5-10 years once certain goals are met). Let's set aside whether or not this is a good idea for the purposes of this thread and details about set up (SMA's, Onshore, offshore, etc). My question is: does anyone manage immediate family member's and/or their own IRA's in exchange for compensation? Or for free The basis of my question is that most of what I find on the internet tells me that if there is any benefit accruing to you from your own or your family members' IRA it's a prohibited transaction. This could even include a "marketing benefit" such as "I have all my and my family's money (including) IRA in the fund so I'm well aligned" or pass through expenses such as audit and admin. I recognize this is firmly in the "consult a lawyer" camp, but I'm wondering if anyone has dealt with this. Let's say hypothetically, I'd want day one GP investment to be $xx and initial AUM to to be Y. Whether I can use IRA money has a significant effect on that.

-

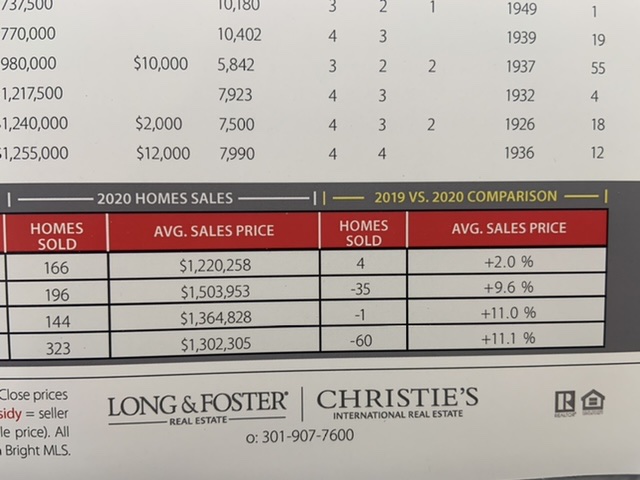

Suburban DC Maryland data; price up 10%-11% for the zip codes with only SFH, collapse in transactions. Note the hopeful tone from realtor that prices will “come back down to earth” easy to understand why this actually hurts realtors as they get paid on transactions. Not taking my 10% to the bank, but happy to own some expensive ass dirt with eroding tiny structure on top for well below the average dirt+house cost of $1.5mm

-

FMBL trades 0.77x book, 11-12x earnings, and has 2x+ the amount of capital to be well capitalized, and has close to $10B $8B of deposits across just 25 branches, 40 ish % of which are non interest bearing. The attraction of FMBL is a function of how much one values safety and over capitalization of that excess capital will never be returned to you. I value it because even if never returned it makes the earnings stream safer. Staying with the theme of illiquid overcapitalized SoCal family go’s, LAACZ seems reasonable to me. Whether you think PMV is $3K/share or $4K plus, $2500/ share = 4% yield growing at mid single digits with an option on some kind of change. Even hair cutting Apple, Berkshire continues to be very reasonable priced. In a world where SPACs trade at 20% premium, EQC at 93-100 cents of NAV offers reasonably priced optionality. BSM and DMLP offer close to 10% yields with direct exposure to hydrocarbon price/volume with low to no leverage. Can still be bad investments though if production collapses. I actually think GOOG and FB, even MSFT are not unreasonably priced. Not cheap, certainly some tax and regulatory risk, but, not crazy to me. Multi family REITs (including non urban) are at 5 caps and can borrow at 1-3% and have low leverage. What I don’t understand about the 50%+ cash crowd is I think there are plenty of securities out there that are highly likely to preserve amd grow purchasing power over time out there. I don’t think any of the above will CAGR at 15% for the next 10 years, but I’d be surprised at less than say 6% (unless say EQC doesn’t find a deal).

-

the barbarous relic

-

me (seeing my large position in PSTH covered calls go from $20.5 to $23.5): is this what being a growth/SPAC guy feels like? guy (loaded on TSLA and crypto) up a gazzilion percent: no, this is definitely not what it feels like.

-

Wife gets Pfizer vaccine on Monday (DC hospital, government affiliation, risky patient facing but not “front line” as in ER / ICU / covid unit) Sister got Moderna vaccine today (South Florida hospital, large hospital system, risky patient facing but not "front line" ) All the staff at my grandpa’s long term care facility have been vaccinated but I don’t think he has (he’s 94) Dad vaccinated today. He is 68 and has an autoimmune disease that makes him high risk, but that’s not why he’s getting the vaccine. He’s getting it because my sister is an employee of the hospital and the hospital is enacting a program where employees can bring in a 65+ year old of their choosing. The roll out is so weird.

-

About -10%. about 90% market exposure. (I don’t consider 7% in EQC or 15% in PSTH covered calls to be market exposure). This excludes some hedges/puts.

-

Russell 3000 Value +3.1% Russell 3000 Growth +0.25% Yes.

-

Wife gets Pfizer vaccine on Monday (DC hospital, government affiliation, risky patient facing but not “front line” as in ER / ICU / covid unit) Sister got Moderna vaccine today (South Florida hospital, large hospital system, risky patient facing but not "front line" ) All the staff at my grandpa’s long term care facility have been vaccinated but I don’t think he has (he’s 94)

-

COBF 2020 Returns (pre-tax, after fees, etc)

thepupil replied to Broeb22's topic in General Discussion

2020 My IBKR consolidated accounts show a return of -4%. These comprise about 60% of assets. My ~35% in fidelity accounts performed better, as did the 5% in my wife's Roth IRA which was in VTSAX (ha!). It's difficult to tell their actual performance because of inflows due to rollovers. If I add up all the dollar profits from non IB accounts its about 4% of my ending NW and 2x the IBKR $ losses, so I think overall return is bout 2% My NW grew about 30% from savings, mortgage amortization, and home price appreciation, which is a consolation prize in a humbling year. Here's to being very levered long SFH and having a good year professionally! (though 10% HPA is not sustainable and will reverse at some point) I endured a ~40%+ drawdown in the beginning of the year as I went into this very poorly positioned with heavy financials and office exposure. Several of my holdings have not recovered though in my opinion value grew (Berkshire/Tetragon); while others have endured permanent impairment (office). While I recovered, I think that initial drawdown did impact my overall ability to recover more strongly. I'm a bit more timid these days. My biggest mistakes were in portfolio management. I manage my parents/sister's money and they each outperformed their net exposure (albeit slightly) w/ far lower weighting to tech stocks than the broader market. My own portfolio suffered from undue concentration and premature doubling down in the initial February / March timeline and theirs did not as I run theirs with a greater diversity of idea types and w/ a greater tilt toward business quality. I can handle missing out on the triple digit gains of the most growthy/tech-y crowd (I know how I'm wired and why I'll never be good at that), but there's no way around it: I completely failed to take advantage of what was one of the better opportunity sets of my short investing career. May write more detailed analysis of what went wrong at another time. John, I'm terribly sorry about your brother. -

My largest position is PSTH covered call. Long PSTH, short December 40 call, bought for $20.50, it’s at $21.30 now. Think it will be hard to lose more than 10%-15%, with upside of close to 100% if market gets very excited about a deal. I don’t know if it’s my favorite idea, but it’s my biggest. And I always have to show love for Tetragon. This year is the year lol.

-

Berkshire is so delightfully reasonably priced and safe. What’s wrong is that I can’t find 10 such ideas of equal quality and safety and resign to slumming it with crappy real estate co’s and holdco’s.

-

Wife gets Pfizer vaccine on Monday (DC hospital, government affiliation, risky patient facing but not “front line” as in ER / ICU / covid unit)

-

Good point, I made about 40% on AIV and EQR is up about 36% over that time, could’ve just stuck to the good stuff. I’m with you in hoping for some AIV destruction!

-

Don’t get me wrong, I went from 25–>45 bps in AIV today (getting crazy!) and understand why people are buying it, but think that it was much more interesting to buy the package in the low to mid $30’s at 60% of NAV including the apt portfolio, than CrapCo/RemainCo is right now at 55% of company NAV. Think my fellow AIV holders have a long and tough road ahead of them.

-

I don't recall Buffett ever buying gold the commodity (Berkshire (probably not buffett) did buy GOLD (Barrick Gold) recently) Are you thinking of this? He made a little in silver back in the day. https://www.gurufocus.com/news/906807/warren-buffetts-giant-silver-trade-

-

Oh yes, economics absolutely apply. I’m just saying it’s different than other commodities given the ratio of that which is above ground to being produced. Gold has responded to big supply growth in the past (digging deep here but I recall the Spaniards encountering this issue when they raped the Americas of gold/silver and experiencing inflation (because of too much money which was then gold and silver)). I think a similar thing happened in the California gold rush. Here it is. My AP Euro teacher would be so proud right now: https://en.m.wikipedia.org/wiki/Price_revolution#Background My point is it’s not as pure of a commodity supply/demand dynamic like a consumable(food, o&g, etc). That’s all. I’m not trying to say economics does not apply. For the same reason, if gold were below its cost of production, I don’t think it would be a good argument to be long of gold, because if no one wants to buy the cubic Olympic swimming pool of above ground gold, the cost to produce it doesn’t matter.

-

The supply of above ground gold is much larger than the amount mined every year (since gold is durable and rarely lost/destroyed and has been mined for 1000’s of years). Gold price is more driven by changes in demand than changes in supply (vs a mix of both) unlike say a consumable hydrocarbon or almonds. Here’s a source that estimates 197K tons ever mined vs 2-3k / year https://www.gold.org/about-gold/gold-supply/gold-mining/how-much-gold

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

thepupil replied to twacowfca's topic in General Discussion

one of my favorite investment managers said to me once, "the return per unit of risk ended up being okay, the return per unit of stress however, made this a very bad investment". no position in Fannie/Freddie (though i guess indirectly via PSH, but I don't even know if Ackman has a material position). Good luck to you all. -

https://www.alicoinc.com/news/detail/1352/state-of-florida-approves-option-agreement-with-alico-to Always great doing biz with the government in a business friendly state. Another $14m straight to the bank. Not this first transaction of this nature and I'm expecting more of this in the future. Stock is wildly undervalued. party like it's 2005, what's next some TRC? And yes I'm aware that ALCO has changed drastically since its land bank value trap days, Trafelet drama and all that stuff.

-

This saddens me as well. Always liked Picasso; will hold off on further commentary.

-

I think the option to pay in stock is good from a credit perspective as it gives OXY a way to issue equity in bad times and probably allows OXY to argue that the interest on the prefs need not be included in any kind of credit metric, just a speculation, no basis in fact for this, i feel like 5XEBITDA would know this.