thepupil

-

Posts

5,005 -

Joined

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by thepupil

-

Very interesting! I thought sufficiently OTM call options were fine (and had even linked an article that said a collar with a 20% band was kosher)

-

AGREED!

-

yep, and the general populace is okay at accumulating a little home equity w/ 74% of retiress and i think like 65% of americans owning their homes. basically these people lived paycheck to paycheck their whole working lives, never accumulated equity, or had some form of disaster that wrecked their prior accumulations (most commonly medical, which I sympathize with, our system is pretty terrible). it's likely these people didn't make the best choices in life, but there also could have been extenuating circumstances. they don't seem entirely unhappy https://www.newretirement.com/retirement/average-household-savings-home-equity-and-other-balances/

-

median retirement savings is only $172K in 60's, even at super aggressive 6% withdrawal rate (basically depleting/annuitizing the corpus), life only looks about $10K / year better than these folks for >50% of Americans. clearly many people do it and live off $25-$35K/year, but that doesn't mean it's pretty! these folks are pretty rent burdened at 40% of gross. https://www.synchronybank.com/blog/median-retirement-savings-by-age/

-

This isn't FIRE, this is geriatric poverty/not saving for one's whole life; this is what will happen to every american who has $0-a few hundred k or whatever in their retirement accounts in their 60's, no home equity, etc.

-

this is what retirement looks like for vast majority of americans who basically have no/little savings. in fact at a certain low level of savings, it's probably rational to get rid of all assets and become a ward of the state.

-

honestly, I've read what you have written a few times and fail to understand your argument. It'd be like if you were stating an opinion in a different language where i had 4th grade level comprehension. What I do understand sounds very much like a wash sale, but I don't understand enough of what you are saying to really argue with you. What i do know is that I've done my above method to maintain positions while harvesting tax losses with success many times (and not triggered wash sales per Fidelity/IBKR/turbotax). Generally as long as one 1) waits 30 days before/after 2) doesn't do anything hedge wise that's too close to a totally de-risking event you can avoid wash sale. Specific share allotment is key (which i heard they may be trying to get rid of)

-

fun discussion. repeat prior recommendation.

-

you'r in luck in that it's october, so as long as it fits w/i your risk tolerance, the simplest thing to do is buy more on October 11th Sell your specific high cost basis shares on November 12th or later, realizing a loss. bonus step: buy more December 13th or later once the procrastinators start tax loss selling additional nuance: if you can, try to double down in your tax deferred account, so your high basis shares on in your taxable and low basis are in your IRA for 30 days you'll be doubly exposed. If this is too much risk or you feel that you're letting the tax tail wag the investment dog, then you could double down, but also do a collar (on half the shares) to reduce risk (such as sell a 20% OTM call and buy a 30% OTM put. to avoid constructive sale, I recommend a pretty wide band on the collar https://www.nysscpa.org/news/publications/the-trusted-professional/article/tools-techniques-to-shield-and-defer-taxes-on-unrealized-stock-gains

-

High Quality Multi-family REITs - EQR, CPT, ESS, AVB

thepupil replied to thepupil's topic in General Discussion

cycles are quick lol. https://www.equityapartments.com/washington-dc/friendship-heights/wisconsin-place-apartments?mkwid=sC8omg1vW_dc&pcrid=432501756441&pkw=wisconsin place apartments&pmt=e&utm_source=google&utm_medium=cpc&utm_term=Wisconsin+Place+Apartments&utm_campaign=&utm_group=Wisconsin+Place+Apartments&gclsrc=aw.ds&&utm_source=google&utm_medium=cpc&utm_campaign=EQR_DC_Properties_Search_Branded_Exact_Null&mkwid=sC8omg1vW|pcrid|432501756441|pkw|wisconsin place apartments|pmt|e|pdv|c|slid||product||pgrid|39963762959|ptaid|kwd-43356067367|&pgrid=39963762959&ptaid=kwd-43356067367&utm_content=sC8omg1vW|pcrid|432501756441|pkw|wisconsin place apartments|pmt|e|pdv|c|slid||product||pgrid|39963762959|ptaid|kwd-43356067367|&intent=DC_b&gclid=CjwKCAjw49qKBhAoEiwAHQVTo3nqfUyElYJNGewJrf3y5E-iyLUfvM8rt1LzZHTZePlocJJ0ZCokoxoCtccQAvD_BwE##unit-availability-tile -

interestingly there's a bloomberg article out today pointing out how much the multifamily REITS can save on interest if rates hold. AVB, CPT, EQR, ESS, MAA, and UDR all have $4.3B maturing through 2023 at a n average rate of 3.1% and pre-funding these maturities now (before tightening) could save $40mm/yr (1%) across the complex, because for these guys 3.1% is expensive lol. they're doing bonds in the low 2% range. Article points out that average apartment REIT is at 70 bps spread and also points out that they all trade at 24-28X FFO (up from 16x). Cheap debt and "richly" valued equity = firepower to buy whatever (if they want). just thought it somewhat relevant.

-

as a holder of PSH and TFG which trade for 30-70% discounts and have inception to date ROE's above 10%, I can assure you there is no magic number. If the discount closes, it will be because people are willing to pay more for the stock. I recognize that is a captain obvious statement, but illiquid externally managed PFICs are the red headed stepchild of capital markets. discount could close in 1 year or in 10 years.

-

Why do you think rent / NOI falls for decent assets? It’s not clear to me. I feel like the entirety of getting wealthy is kind of a “leveraged basis trade”. Borrow at < 3% invest in stuff that makes more. This describes much of my financial life lol.

-

I think CLI's balance sheet risk is gone completely. they can (as you say) sell the remaining office and inject a boat load of capital into the multifamily. so I'd say CLI has none of the "omg 15x EBITDA debt" risk that Jim Chanos was tweeting about anymore. the biggest risk i see is simply execution and valuation on the multifamily side. you can drive a truck through the run rate NOI and the pro-forma NOI that gets you to an okay cap rate, and the disclosure on the land bank/land options is dogshit. I have little clue as to the credibility of the "$XXK / unit / site" they throw out in their NAV buildup. I think it gets sold, low $20's to $30. I've considered it as a replacement for some CDR/LAACZ exposure that I think is gone before year end ( in each I'm holding despite 70-100%+ appreciation this year as I expect them to transact above the current prices). as far as catalyst/clarity of incentives, to me it seems like one of the better things out there. just a question of what to pay/what worth.

-

clearly for sale, but what px? BTIG says $26 NAV on not entirely bearish assumptions. 101 sale de-levers office to virtually no debt, MF is levered but all non-recourse / asset specific (plus the pref), what are your thoughts here?

-

I agree. That said, it may be a (partial) hedge to have in-place, low cost fixed debt. Both as a company and as an individual. When I have a mortgage at 2.875% on a 30 year schedule and I'm using my savings to buy FRPH which owns multifamily levered with 12 year interest only 3% debt and has a $10mm agg royalty linked to inflation at its disposal (plus a bunch of cash)*, I feel somewhat secure. It's not that there's no risk, but rather that the risk is mitigated for some time (assuming NOI holds: assuming rents can keep pace with property taxes, insurance, labor costs, maint capex etc). I think it's certainly possible that rates rise and we no longer get the sweetheart leverage that we have and there's a situation where one owns a depleting asset (a liability at a below market rate of interest); this will not be great if one has to sell (subjecting oneself to worse cap markets), but may still work out well one doesn't. *or whatever corporate high quality borrower you prefer

-

I think this actually does occur in some markets, but not to the wild and dramatic degree that people associate with "gluts". In my DC/MD stomping grounds, my old apartment floorplan is available for $3,400/month. I rented a this from 2016-2019 for $3,100 - $3,300 / month. I locked in the first 2 years at $3,100 with free parking because there was a mini-glut due to a few buildings coming online which caused rents to decline from the mid $3's, so rent hasn't really grown there in 5 or so years. Not exactly "distress" but also maybe not what you expect when buying a 4 cap (or less) asset. Not far away, JBGS recently delivered 8001 Woodmont, which as of June 2021 was 4% occupied according to the supplemental and is currently offering 2 months free, albeit off a high price point (2 BR = $4K). This is how it happens. Nice new buildings come online, they offer incentives to fill em up, the existing supply might go from 95-90% occupied and they then reduce price by 10% or so. basically, developers are doing what they should do, bring on more supply when the market can bear it. And the supply gets absorbed as more yuppies move here. The bear case is they stop moving here and the construction continues and the landlords have to decrease rents more (I don't think that occurs). Construction costs, NIMBYism, permitting time, etc all provide a degree of protection from too much coming at once. https://www.8001woodmont.com/?gclid=CjwKCAjwndCKBhAkEiwAgSDKQeslUHvHYFm1KM34_wrZVeti9pyBwoY9YABWXRntEixM7_keTQ8KSRoC_skQAvD_BwE In certain submarkets though (like where FRPH's assets are) the densification seems to have almost played out and there aren't too many more building spots, so you probably start to see less supply availability (this is where @BG2008 chimes in about moats and water and stuff), and rent increases once the moratorium ends. Seehere: the land between the ballpark and 695 had pretty much been conquered by Yuppie amenitized apartment buildings https://www.capitolriverfront.org/live-here/residential-buildings but there are still some big things coming: https://www.bisnow.com/washington-dc/news/multifamily/wc-smith-plans-another-capitol-riverfront-project-with-520-units-109731 https://dc.urbanturf.com/articles/blog/dc-has-the-most-cranes-in-the-sky-of-any-city-nationwide/18114 https://www.bisnow.com/washington-dc/news/multifamily/dc-apartment-demand-hits-record-levels-as-recovery-accelerates-109539

-

I agree with you, but I don't really see this as a new phenomenon. It's the tailwind of the past decade. Maybe it's strengthening or just continuing? but you could've said the same thing in 2010/2015/today, no?

-

Yes. Now this doesn't invalidate your overall point. There's also a huge pool of capital, think pensions or foundations that may have held 10-70% in nominal bonds, mostly corporate investment grade or treasuries, where bonds have nothing really to offer them. Everyone has to reach for yield now thanks to years of financial repression. Buying Multifamily (but really ALL "alternatives" and equities) is one way to produce yield. this is basically the multidecadal bull case for BAM, BX, KKR, etc. It's not clear to me there's anything unique to MF or sunbelt MF regarding this. basically, central banks force those who want to make a real return out of fixed income. period.

-

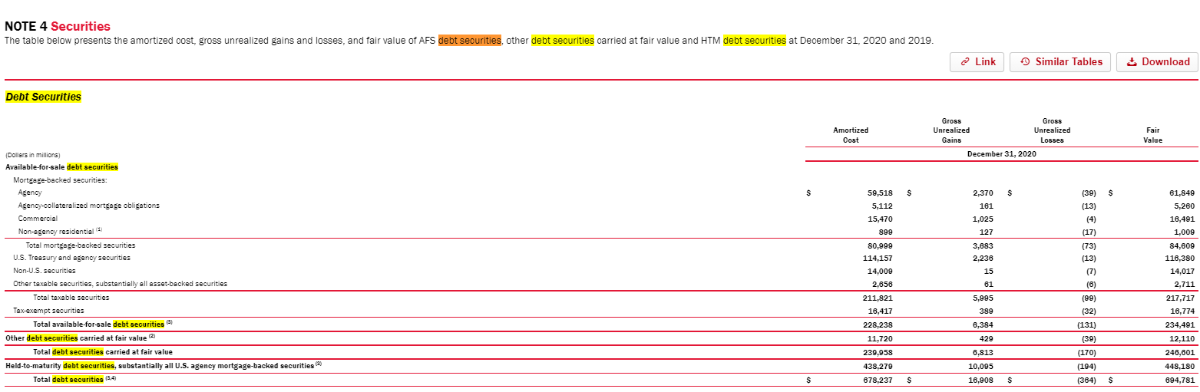

As an example, Bank of America owns $600-$700 billion of "Debt Securities", about 2/3 of which is Agency MBS. In no world, is Bank of America comparing its MBS holdings to the prospect of buying multifamily. They're totally different. As for why they won't hold cash, well they're earning $10-$11 billion of interest on that portfolio which is low, but it's far more than zero.

-

-

the end buyers are totally different. The holders of treasuries and MBS are sovereigns, the Fed, banks and insurance companies, etc. the nominal cash flows of those are guaranteed by the most powerful country in the world. Inflation protection is not the point. No one is buying agency MBS expecting inflation protection. They are buying MBS to pick up some spread relative to treasuries by bearing prepayment risk and weighted average life variability. I don’t see them as comparable at all given their vastly different capital treatment and risk characteristics.

-

i like kuppy because he wrote a promotional piece on JOE that jived with me, bought calls, made 600 or so bps from 100 and moved on. followed JOE forever but he highlighted how the perception would change and catalyzed the move up. would i trust all his numbers or details or risk big money on one of his themes? No, absolutely not.

-

CXP being taken out by Pimco after strategic review involving 90 interested parties. about a 5.3% cap rate on NOI that’s down a bit. Stock about 100% off low, -20% from pre covid peak, -50% to those who bought CXP as a non traded REIT at $40 (someone told me this, this has not been confirmed by me)

-

It’s not a “loophole” and life insurance is available to everyone*. All life insurance bypasses estate tax. This is just a way of doing non traditional investments in a life insurance wrapper. it’s like variable life insurance but with hedge funds, credit etc. *though your standard Northwestern Mutual one will probably have higher commish and will invest in the general account and make a low single digit IRR.