thepupil

-

Posts

5,005 -

Joined

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by thepupil

-

Good point, yea assume that. more succinctly, do stablecoins circumvent KYC and/or reduce transaction costs for remittances/cross border payments?

-

Dumb question re the more reputable stable coins. if I am a Bangladeshi working in Saudi, can I send a stable coin home to my parents if 1) I have a mobile and/or internet access with internet but parents don’t 2) we both have mobile 3) neither have mobile does one/both sides need a bank? if so, what is the t-cost?

-

Tell me you worked for Capital Group without telling me you worked for Capital Group

-

yep...probably get same gross return buying MAA CPT EQR AVB PLD PSA HLT MAR INVH AMT etc. but then underperform with BREIT on the fees....but you get that sweet sweet volatility suppression.

-

-

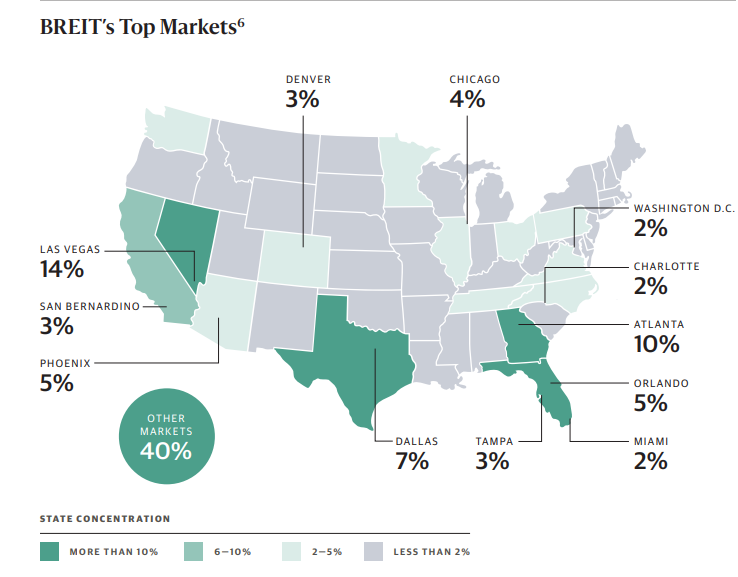

complex topic re housing policy, history, etc.... but I think $BX buying sunbelt apartments is more simple. $BX is simply raising a massive amount of long duration capital* and has loads of money to put to work. They have created a fundraising retail machine and are setting the price for desireable assts ever higher. Mass affluent have decided they'd rather invest in a $BX managed private REIT for their core RE than REITs because they don't like the volatility or whatever. https://www.breit.com/wp-content/uploads/sites/4/2020/10/BREIT_Fact_Card.pdf?v=1640618455 BREIT has $78 billion AUM and 2300 properties, including 137,000 units of multifamily. Atlanta is their #2 market. I don't know if this is correct and i can't find historical financials on BREIT's website, but I heard that BREIT is raising like $2-4 billion per month. Let's just say that's $1 billion. At 40% leverage that translates to $1.6 billion of apartment purchases per month going to a vehicle that has quasi-permanent capital (if they're only buying apartments) or $800 million if they're doing 1/2 apartments. Recall there are some months they may be raising more than $1 billion. At $300K/unit and $800 million, that's 2,600 units per month that $BX is buying. 31,000 per year. That's a Mid America (the largest multifamily REIT in the US at 100K units) every 3 years. Who knows how long it will last, but that giant sucking sound you hear is $BX hoovering up all the desirable real estate to put in its long duration low returning core private REIT sold to mass affluent / retail *what's odd is that it's not really permanent capital, technically 5% / quarter (20%/yr can redeem) so it's looong duration capital, but not permanent. it would be interesting to see what happens if the fundraising stops and you get net redmeptions > sustainable rate.

-

pretty much same here. -now 4-5% net cash/ SPACs in the investment portfolio -completely undrawn HELOC despite planning on using it to buy i bonds (just actually paid for them instead), -not cash out refi-zing despite HPA de levering me to 55% LTV, -cars paid for - sold my two most complex and levered businesses (Brookfield and Softbank) - have even considered stopping my buy $x k of index / month in the 401k - top of portfolio emphasizes the most excessively capitalized feels a little market time-y to me but I have lower conviction in the risk reward right of overall portfolio right now…trying to resist urge to go 10% or even 20% cash. I’ll never understand the “I think the market should trade for 10x earnings and am 100% cash” crowd, but I’m a little bit more of a pansy now than I have been In most Recent past

-

someone was arguing with him about a stock's fundamentals and Adam decided that the proper response was to doxx that person (via a link to the person's LinkedIn) and make fun of the college that person attended.

-

Smart people tell me I should care about crypto…and I just really struggle to do so. this along with my hatred of Tesla is mainly because I’m a “small dicked fit wit”.... I think it in part stems from the fact that every time i've invested in silver and gold, i end up buying to sell other stuff that i like more and it's not a worthwhile activity for me because i never end up owning enough for diversification bennies and don't have the discpline to HODL something in whcih i have no conviction.

-

I pay my nanny $60K / year ($23 / hr plus $400/month healthcare premiums) with 2 weeks paid vacation 5 sick days and paid snow days. This is the rate for well referenced/experienced nanny’s in suburban DC. would be closer to $50K if paying under the table though there are modest tax benefits for going above board. Great time for “low skilled” labor (though I wouldn’t describe a nanny as “low skilled” but you get my point

-

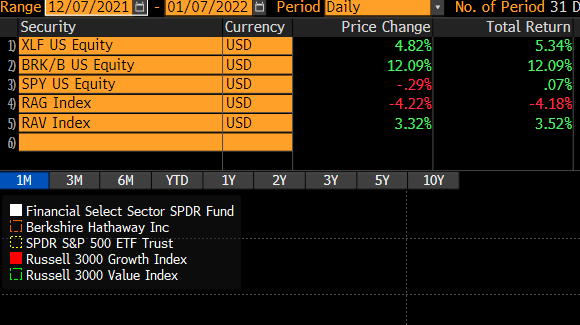

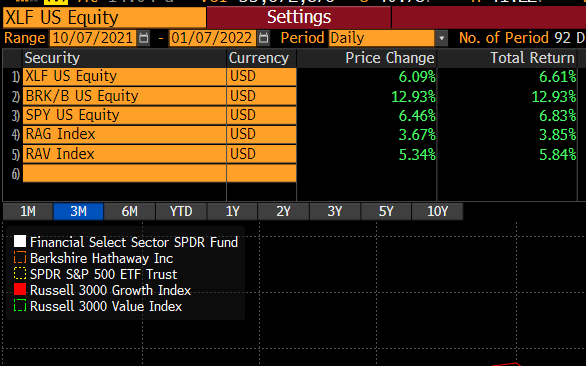

sorry, thought this was about Berkshire and not general value rotation. The answer is yes, there's a broad based value vs growth rotation occurring. I personally hate making money this way lol. It feels so unsustainable and arbitrary. I prefer takeouts and blow-out earnings/reports from my holdings, but I'll take it. Whatever.

-

For recent time periods: Berkshire>Financials>Value>Growth Over 5-10 yr time frame: Growth>Financials>Berkshire>Value

-

Amazing! Congrats

-

2021: I made about 55% on a consolidated basis. Have precise data for interactive brokers (+68%) and Fidelity looks like (+22%). NW increased by about 60% marking house to market, but I arbitrarily wrote down the residence to cost to stay hungry, so only went up 30%. Lots went right. Little went wrong. I started the thread to obnoxiously tout my own returns. Now others may do so and one-up me (particularly on a long term basis) My LT results are very market like with more vol and higher tax drag

-

iSavings bonds yielding 7.12% currently

thepupil replied to Spekulatius's topic in General Discussion

Just couldn’t resist, bought $10k for my kid today, bringing total December purchases to $30k, will do $30k more in late January. At the risk of making a macro prediction, it wouldn’t surprise me if CPI > short term rates for a long time and this remains a nice “arbitrage” for a while -

This was 2011-2013…definitely recall some 40 yr 221d4 (construction to perm), but maybe I’m misremembering??? It was long ago. but ya those are the folks, walker dunlop, greystone, Wells Fargo, PNC, Red Capital, Berkadia, Arbor Capital, I’m sure many others and I’m sure some of the lesser well known ones I listed don’t do it anymore. my impression was regular for profit owners of buildings could take these out and the info here says so (for profit and non profit borrowers, no income m/affordability requirements for units) and again my info is way stale on this, but we were doing 7+ $1B + securitizations/ year and we’re just one player so while it’s not huge, a fair number of people take these out. https://www.hud.gov/program_offices/housing/mfh/progdesc/purchrefi223f here’s some more stuff, note that it takes a really long time to get one, so you obviously couldn’t use in a bidding processes https://blog.stacksource.com/beginners-guide-to-hud-multi-family-loans-d07531e0e6f3

-

You’ll have to get a quote from a mtg banker. I suspect smaller loans would be 4ish% and big ones below 4%

-

Ginnie Mae we’ll do a 40 yr amortization construction loan that converts to permanent, tough to get, but I used to fund them (as well as 80-90%LTV 30-35 yr permanent loans on big buildings… like $50mm loans)…also do senior housing and nursing homes homes look up 223f and 223a7 221d4 loans ginnie Mae hud https://www.mandtrealtycapital.com/FHA/HUD_Multifamily/fha_multifamily.html

-

iSavings bonds yielding 7.12% currently

thepupil replied to Spekulatius's topic in General Discussion

I have $150K unused HELOC capacity. I'm using $40K of that to buy i-bonds this month/next month (i thought about doing $60K, but decided not to give $20K to my kid, for now, even if i could just never tell him about it and get it later). I don't really love the prospect of 0% real return (- federal tax), but am getting em now while borrowing rates are very low and they pay a risk free nominal 7%. I can always re-evaluate. my HELOC cost ~3% the biggest risk is there's some huge opportunity for that $40k w/i the next 12 months, but i have much more than that in spare IBKR margin and will still have a lot of HELOC unused. I don't want to tie up my equity in i-bonds but i'm happy to tie up my unmonetized home equity. But honestly, I thought about just buying some starter positions in midstream MLP's EPD/MMP instead...will probably make the divvy 8-9% w/o huge depreciation and would be better use, but I'm kind of reloading the gun (only 103% long and unused HELOC)...have even thought of...gasp...holding a little cash it's odd that I can borrow from a bank with a 2nd mortgage and lend to the US government and make a nice NIM -

I generally agree w/ you. I tend to focus on public RE stuff that i think has a lot of margin of safety built in / would withstand increase in rates pretty well (probably not thrive, but withstand). But on well located single family homes I guess the supply/demand picture appears so favorable (for owners/sellers) that it's hard for me to really be all that bearish (and in fact think the price increases are relatively sustainable<--not the rate thereof, but rather the levels achieved). Example a $1.3mm house in blue state land w/ $1,300/month of taxes and insurance is $5,600/month at 2.875%. At 4.5% it's $6,500/month. If SALT goes to $80K, then the buyer's income increase / property tax deductibility covers pretty much all of that. so you could have a situation where rates increase but prices don't collapse because of other factors. (ie rate increases carrying cost by 17% in my example, but SALT would decrease carrying costs by a good by 8-15% should i focus on the propsective $12k/year in carrying costs or the fact that every house has 10 willing (and very well qualified) buyers? it's not clear at all to me that we're in a bubble or that prices will go down. it's clear to me they can't go up 20% /year lol, but i wouldn't hold my breath waiting for collapse and i definitely wouldn't pay 6 figs of t-costs and uproot my family betting on big price decrease. as noted earlier, my own area influences my views. DC is <5% investor owned, has much better price/income ratios than NY/SF, a low beta economy (some would say countercyclical), and no land for new SFH. if I was talking exurban property somewhere w/ cheap(er) build costs and still plentiful land, maybe i'd have a different veiw. to use a more median home . 2.875% --> 4.5% = $3,500/yr on a $400K house. there may easily be other factors (general inflation/wages) that push people's ability to pay byu more than $3,500/yr that keep prices stable from here even if rates go up.

-

mortgage rates = 10 yr swaps + mtg basis (simplified) there's no law that 10 year tsy rates must be at or above inflation. financial repression has kinda been the current / past / and potentially go-forward policy. the rate is subsidized by fed/government. Not saying it will ALWAYS be that way, but I don't think 4-6% inflation will automatically lead to 4-6% 10 yr. no one is entitled to any kind of return, particularly buyers of government bonds (or owners of real estate for that matter).

-

Yea good point. Maybe to use a real example and to articulate myself more clearly: Stock for stock decreases risk in the event of a bad deal, makes it less disastrous. XOM’s purchase of XTO was bad. Would have been worse if they room on $30B of debt vs $30B of stock. you can always buy back stock after you know how merger goes, and if the merger made a sense per share value will be higher even without repo. Debt/cash funded bad deal potentially hurts a company more. it also allows for mergers to be more about relative value than absolute. Generally I’m a dilution / stock issuance apologist, it offends me less than it does most. https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/how-not-to-do-m-a-a-look-back-at-exxon-s-deal-for-xto-10-years-later-55076990

-

Like if $AAPL took out $PTON at 100% premium in stock (about $30B), would $AAPL potentially be a 1% better company in terms of adding fitness to the ecosystem, being able to potentially bring down music royalties costs, increasing % revenue that’s subscription, etc. I would say yes. I think that’d be cool.

-

It’s all case by case. Some of the worst (AOL / TW,worst for TW) and best (1% of $FB for Instagram) are stock for stock. I generally like them because I think it decreases downside if they’re occurring well above my basis. I think stock for stock accompanied by big offsetting repo’s is underutilized.

-

not buying bitcoin when i first heard about it (2012 time frame) selling in 2016 to clean up portfolio... oh what might have been