thepupil

-

Posts

4,184 -

Joined

-

Days Won

4

Content Type

Profiles

Forums

Events

Everything posted by thepupil

-

I generally agree w/ you. I tend to focus on public RE stuff that i think has a lot of margin of safety built in / would withstand increase in rates pretty well (probably not thrive, but withstand). But on well located single family homes I guess the supply/demand picture appears so favorable (for owners/sellers) that it's hard for me to really be all that bearish (and in fact think the price increases are relatively sustainable<--not the rate thereof, but rather the levels achieved). Example a $1.3mm house in blue state land w/ $1,300/month of taxes and insurance is $5,600/month at 2.875%. At 4.5% it's $6,500/month. If SALT goes to $80K, then the buyer's income increase / property tax deductibility covers pretty much all of that. so you could have a situation where rates increase but prices don't collapse because of other factors. (ie rate increases carrying cost by 17% in my example, but SALT would decrease carrying costs by a good by 8-15% should i focus on the propsective $12k/year in carrying costs or the fact that every house has 10 willing (and very well qualified) buyers? it's not clear at all to me that we're in a bubble or that prices will go down. it's clear to me they can't go up 20% /year lol, but i wouldn't hold my breath waiting for collapse and i definitely wouldn't pay 6 figs of t-costs and uproot my family betting on big price decrease. as noted earlier, my own area influences my views. DC is <5% investor owned, has much better price/income ratios than NY/SF, a low beta economy (some would say countercyclical), and no land for new SFH. if I was talking exurban property somewhere w/ cheap(er) build costs and still plentiful land, maybe i'd have a different veiw. to use a more median home . 2.875% --> 4.5% = $3,500/yr on a $400K house. there may easily be other factors (general inflation/wages) that push people's ability to pay byu more than $3,500/yr that keep prices stable from here even if rates go up.

-

mortgage rates = 10 yr swaps + mtg basis (simplified) there's no law that 10 year tsy rates must be at or above inflation. financial repression has kinda been the current / past / and potentially go-forward policy. the rate is subsidized by fed/government. Not saying it will ALWAYS be that way, but I don't think 4-6% inflation will automatically lead to 4-6% 10 yr. no one is entitled to any kind of return, particularly buyers of government bonds (or owners of real estate for that matter).

-

Yea good point. Maybe to use a real example and to articulate myself more clearly: Stock for stock decreases risk in the event of a bad deal, makes it less disastrous. XOM’s purchase of XTO was bad. Would have been worse if they room on $30B of debt vs $30B of stock. you can always buy back stock after you know how merger goes, and if the merger made a sense per share value will be higher even without repo. Debt/cash funded bad deal potentially hurts a company more. it also allows for mergers to be more about relative value than absolute. Generally I’m a dilution / stock issuance apologist, it offends me less than it does most. https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/how-not-to-do-m-a-a-look-back-at-exxon-s-deal-for-xto-10-years-later-55076990

-

Like if $AAPL took out $PTON at 100% premium in stock (about $30B), would $AAPL potentially be a 1% better company in terms of adding fitness to the ecosystem, being able to potentially bring down music royalties costs, increasing % revenue that’s subscription, etc. I would say yes. I think that’d be cool.

-

It’s all case by case. Some of the worst (AOL / TW,worst for TW) and best (1% of $FB for Instagram) are stock for stock. I generally like them because I think it decreases downside if they’re occurring well above my basis. I think stock for stock accompanied by big offsetting repo’s is underutilized.

-

not buying bitcoin when i first heard about it (2012 time frame) selling in 2016 to clean up portfolio... oh what might have been

-

while from a conflicted source (realtor) this describes the state of things around here. objectively less frenzied than 2020, prices not going up at same rate, but if you price right 20-50 showings, 10+ offers. there are currently 2 homes for sale in the neighborhood of several hundred. 5 traded last quarter. There are simply far fewer sellers than buyers and incomes and borrowing rates allow one to pay up. low inventory, robust end buyer (DC area has virtually no SFR for now) demand, same as it was in 2019 and 20 years prior when my next door neighbors won a bidding war to get their house. it’s hard for me to conclude this is a bubble rather than simply strong fundamentals. I came to the same conclusion in 2019 when i bought (though still felt like a top tick) This is market specific ($1-$2mm everyday mass affluent single family homes in close to city In NWDC/MD/NoVa) for which no new supply exists.

-

iSavings bonds yielding 7.12% currently

thepupil replied to Spekulatius's topic in General Discussion

right! forgot about that. true -

iSavings bonds yielding 7.12% currently

thepupil replied to Spekulatius's topic in General Discussion

I'm kind of torn on these. my biggest issue is the after tax upside. I live in high tax state and have a high marginal tax bracket. So as long as that's true making 7% all ordinary income on $20K/year ) isn't really that exciting to me because it gets chopped in (almost) half by taxes. Of course, I can defer and I won't always be in high tax bracket (once stop working), but then I'm tying up capital in something that yields 0% real for a long time which I think I can beat. I feel like I'm rich enough to no longer care about that extra $200-1000 of relative value to extract from that juicy uncle sam 7% bond, but not rich enough to where I can afford to deploy $10-$30K per year into something that generates no real return. -

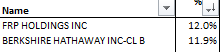

Just let FRPH overtake it (via addition) Think COBF bout to own a decent chunk of this float.

-

The thing that I’m most tempted and terrified to buy more of is…Softbank

-

I think this is true if you want to invest in the more "idiosyncratic" smaller stuff and try to buy at discounts to NAV and sell at NAV and rinse repeat. Unless one is inclined to enjoy doing this, I wouldn't recommend it. It's time consuming, boring, and not efficient from a tax perspective (I happen to love it though, tis an affliction) I'd recommend investing in with @BG2008 and just have him do it for you, investing in the REIT index, or maybe Brad Johnson's firm (I know nothing about him other than website/twitter DYODD) https://www.evergreencap.com/company/our-process. You could also find an RIA that sells BREIT to get Blackstone's giant portfolio<--Do I think this is much better than the REIT index? Not really, but just a thought. https://www.breit.com/ There are numerous passive options to own high quality real estate. The US is blessed to have democratized ownership of property at relatively low cost (setting aside some more greedy products/structures out there) What are you trying to solve for? Do you need/want liquidity? What returns are you trying to make? how much do you want to do? Are you open to tax complications (K-1's, etc?). Will this investment be in a tax advantaged account or taxable or both? What is your desired level of diversification/volatility?

-

Take stream of monthly gross long exposure and monthly long contribution (if long only just your return). For a given month average the month end long exposure w/ prior month’s. Monthly return / monthly avg exposure = return on invested capital. String your monthly ROIC together to get your annualized ROIC. compare to annualized return. The difference is tour cash drag.

-

https://www.google.com/amp/s/www.cnbc.com/amp/2021/11/03/house-democrats-propose-increasing-salt-cap-to-72500-through-2031.html this would be wild for blue state high income real estate. A couple making $500K would have an extra $16-$20K / year for mortgage payments, at current rates improving purchasing power by some $200k+ for the record, I don’t really agree with the policy, though it would be wonderful for me.

-

NYC is back and so is New Jersey! https://twitter.com/thepupil11/status/1456013721067786240?s=20

-

starter position in CLI. Rumored 400K lease w/ $AMZN at previously out of service office building is the kick in the pants to get me involved. along w/ some other developments/lease ups AND most importantly the fact that it's clearly up for sale / restructuring. small position. I'd be bigger if a) the gap b/w price and NAV was larger b) the multifamily was not encumbered/levered w/ the preferred JV structure c) i had a more precise view of office NAV BTIG fluff piece says $25-$30, that's kind of where I think things shake out, so only really interesting if corporate event w/i say a year or so.

-

To follow up, I bought 6 of the January 21, 2022 expiry $115 puts on the March 2022 future. The market value of these is immediately marked down to $80, from the $200 I paid for them. This gives me the right but not obligation to sell 6 of the MArch 2022 10 year note futures, expiring in January. If the 10 year note were to declinne by 20% (a highly highly highly improbably scenario involving several hundred bps of movement over a short time frame, this would be worth $11K from a cost of $200. In the other 99.9% of outcomes, I will lose my $200 bucks and not tell my wife I wasted a nice dinner on an experimental futures options trade. it seems the shorter expiries have all the liquidity, so you may want to set aside whatever you're willing to lose and roll twice or thrice. In my view this is the most direct way to hedge a rise in rates that are most relevant in determining 30 year mortgages. Many bothan spies dollars died in bringing us this information. As a further wrinkle, I've discovered that the "10 year future" actually is a 6.5-10 year future and one may want to go to the "ultra 10 year note future" for a true 9.5-10.0 year note type of exposure. good times.

-

More or less, yes. Though, I think you'd probably be overhedging by going at the money and therefore hedging any move in the 10 year note. Perhaps you only want to hedge for a given X%, that would decrease cost. My logic is this. The mortgage rate is a combination of a number of things. Mortgage rates are determined by Fannie/Freddie's guarantee fee (Constant) Servicing Fee (constant) Rates along the part of the curve where MBS lie (roughly 10 years) the mortgage basis (or the difference in expected/modeled yield b/w the tsy/swap rate and mortgages). differences b/w various banks (ie if a banks backlog is overwhelmed, they'll increase rates to slow down demand) The most straightforward and largest component of this is the treasury rate at the part of the curve where 30 yr MBS lie, hence my recomendation of 10y futures. You could either short roughly your notional in 10y futures. Or could cap your downside w/ futures options. It depends on what you're trying to solve. If you only want protection from a huge move, I'd buy some further out of the money. for fun, I just tried to buy a few hundred dollars of 10% OTM options on the June 2022 future which expire in April. They show up as costing pretty much nothing. I'm trying to see if i can get a fill to make sure this is actionable

-

This is not the right part of the curve for hedging a (standard US 30 year) mortgage. if he intends to take out an ARM, I agree, but don’t think that’s the intent. why hedge a rise in the mortgage rate, which is 10y tsy + swap spread + mortgage basis with an instrument linked to <1yr rates?

-

I would keep it simple. conventional mortgages may amortize over 30 years, but MBS are far closer in duration to the 10y note than the 30y bond. therefore I’d hedge with the 10 year, futures trade in $100k increments and there are futures options as well if you wish to cap your downside. far simpler and more direct and a true hedge. Gregmal’s may be a fine investment idea, but has little to do with your desired hedge.

-

I repeat my prior feedback. There are plenty of companies discussed on this board. Not all of them engage in buggy whip manufacturing or own real estate. You appear to be inclined to invest in high growth companies of the future. For ones where you have insights to share, please feel free to do so. You also appear bearish of real estate. there are numerous real estate (long) idea threads. Please feel free to share your thoughts regarding their intrinsic values and your rebuttals to the echo chamber / bull cacophony that can sometimes occur when Greg, BG, RealAssets, and I form a circle and start moving our arms up and down. there are numerous types of investors on this board. high quality posts on the companies of the future would be welcome. high quality denigration of ideas is also welcome. have at it.

-

there are a wide variety of styles and posters on this board. some post about #neversell amazing companies like Constellation, some post about crappy NAV / RE holding companies, some post about hongkong net nets, some post about canadian energy companies, some post about blue chip tech companies, banks, options on banks etc . you can choose to contribute/engage with what floats your boat. what companies/investments do you like? why? Are they discussed here? if not, start a thread, if you dislike the discussion or derive no value from it, move on.

-

many threads on housing / RE 1. Gregmal expresses aggressive, bullish, extremely confident view, that's likely expressed in real life in slightly more nuanced, maybe slightly less one dimensional fashion than it is in a message board rant. 2. Pupil: thanks Greg, I agree mostly, though I'd nitpick on a) immaterial nuance number 1 b) immaterial nuance number 2. I'd also point out here's how our view may be wrong. 3. Someone else: expresses more bearish view 4. Gregmal to someone else: you're an idiot 5. Someone else: no you're an idiot. 6. Pupil : while i mostly agree with Gregmal, I agree with someone else on this point. 7. Gregmal: pupil you're a wimp 8. Pupil: Gregmal you're too confident and make so much mor emoney than i do. i hate you!!! 9. someone else: you're both idiots 10. everyone takes their ball and goes home.

-

My parents first house they bought in Fort Lauderdale in the 80’s was $40K. Steps from the ocean, infested with snakes and cockroaches . Then that coke money poured in to SoFla and the rest is history!!* *parents were actually wiretapped because a tenant was dealing, house got raided lol