All Activity

- Past hour

-

It's just like someone with severe TDS to go back to all the debunked law fare initiated against the Trump family. Look at the assholes that launched it - Fani Willis, Letitia James, James Comey, Joe Biden - all criminals trying to jail their major political opponent on bogus/fake charges - just like a banana republic. And of course, when Americans realized the lengths these assholes would stoop to - Americans rejected THEM and elected Trump. What idiots they were to try and put Trump in jail and remove him from the Presidential ballots. Americans are not stupid and understand corrupt politicians that have NOTHING to offer except "We don't like Donald Trump" Imagine that as your campaign platform.

-

Insurance - The Engine That Drives Fairfax

Maverick47 replied to Viking's topic in Fairfax Financial

This (flexible and intelligent capital allocation) is a really important differentiator for top notch insurance companies/conglomerates @Viking. There are plenty of publicly traded insurers who attempt to maintain underwriting discipline through an insurance cycle, but they unnecessarily restrict their capital allocation options. Too many of the insurance CEO’s limit their capital allocation decisions (when underwriting opportunities become less attractive) to share repurchases, dividends and possibly acquisition of other insurance companies. They either don’t appear to be able to think outside those boxes, or perhaps they just don’t have an optimal holding company structure for insurance company subsidiaries that would also allow them to acquire subsidiaries outside of insurance. If they are focused on Return on Equity, when profitable underwriting growth for the numerator is difficult to achieve, they typically will turn towards returning capital to shareholders as a means of reducing the denominator. This can result in a relatively efficient insurer, addressing the issue of “excess capital” if it would otherwise be invested in low return fixed income instruments and damage the Return on Equity measurement. But the problem can be that in their urgency to “return” excess capital to shareholders, they forget to consider whether the price at which they are repurchasing shares is favorable or not. Both Fairfax and Berkshire have been (and are) proving themselves to be adept at rationally scanning a much wider global opportunity set of places to invest any excess capital that can accumulate during softer markets. -

Anyone with a high allocation to Berkshire and Fairfax has likely under-performed and if the name of this site in any way selects for those types, it is likely that many have lagged the markets. But so what? What is six months over a lifetime horizon?

Anyone with a high allocation to Berkshire and Fairfax has likely under-performed and if the name of this site in any way selects for those types, it is likely that many have lagged the markets. But so what? What is six months over a lifetime horizon? -

Am I the only one here who's had a rubbish first Half of the year?

Eldad replied to thowed's topic in General Discussion

@thowed I think we own a lot of the same stuff. CRAWA saved me last year and TFII this year. But it has been a struggle for 2 years. Don’t worry, I’m pretty sure that means you are doing it right. -

Taking his cues from Trump, Carney's renovating the "Canadian Whitehouse". Canada’s Most Famous Fixer-Upper—the Prime Minister’s Home—Is Getting a Makeover https://www.wsj.com/world/americas/canadas-most-famous-fixer-upperthe-prime-ministers-homeis-getting-a-makeover-1a5b2b6d?st=85eDLt&reflink=desktopwebshare_permalink

-

Best Ideas 2026 - Half Time Report

treasurehunt replied to phil_Buffett's topic in General Discussion

Yes, I'm well aware that @whatstheofficerproblem is the man when it comes to LQDA, but I I don't think he turned in any picks in the best ideas thread. Or I missed the post with his picks. - Today

-

@Malmqky I prefer my Tencent undiluted. The Prosus guy is a nuisance. He is more of a threat to Prosus than the CCP is to Tencent.

-

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

Spekulatius replied to tnathan's topic in General Discussion

I would rather buy more AJG but I don’t own as much of it than you do. RYAN traded at a substantial premium to other brokers due to faster growth but the latter has largely evaporated. -

Am I the only one here who's had a rubbish first Half of the year?

Saluki replied to thowed's topic in General Discussion

I've underperformed this year too. A some of my midsize positions (NTDOY, META and CPNG) got cut down by a lot, and a few others that did well last year are just trading sideways or down a little. It happens. You can't outperform in the long run and the short run. -

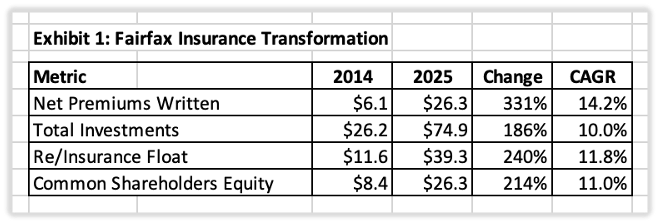

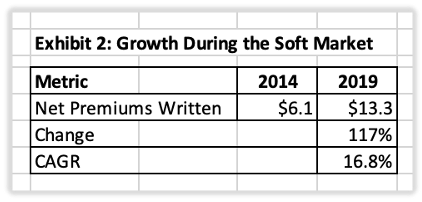

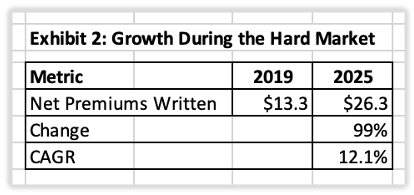

Article 4 into our deep dive into Fairfax's insurance business. What did they do in the last soft market? Fairfax's Insurance Transformation (2014–2025) One Insurance Cycle. One Management Team. One Remarkable Transformation. One of the best ways to evaluate management is to examine what it accomplishes over an entire business cycle. The eleven years from 2014 to 2025 provide an excellent test for Fairfax. During this period, the company navigated both a prolonged soft insurance market and one of the strongest hard markets in decades. The result was one of the most significant transformations in Fairfax's history. Several observations stand out. First, Fairfax dramatically expanded its insurance franchise. Net premiums written increased from $6.1 billion to $26.3 billion, while float grew from $11.6 billion to $39.3 billion. Second, shareholders ultimately participated in that growth on a per-share basis. This outcome was far from inevitable. Fairfax issued shares and partnered with outside investors to help finance several acquisitions. Over time, however, strong organic growth, improved underwriting profitability, rising investment income, share repurchases, and the purchase of minority interests largely offset that dilution. Finally, Fairfax created value under two very different insurance market conditions. During the soft market, management focused on expanding the business. During the hard market, it harvested the benefits of those earlier decisions. The transformation can be divided into two distinct phases. Setting the Stage In 2011, Andy Barnard was appointed Chief Operating Officer of Fairfax's insurance operations. His priority was not rapid growth. Instead, management concentrated on strengthening underwriting discipline, reinforcing Fairfax's decentralized operating model, recruiting talented leaders, and building a stronger insurance culture across the organization. These efforts attracted little attention from investors at the time. In hindsight, they laid the foundation for everything that followed. Phase One: Growing Through a Soft Market (2014–2019) “Someone’s sitting in the shade today because someone planted a tree a long time ago.” Warren Buffett Much of the period from 2014 to 2019 was characterized by a soft insurance market. Pricing was generally weak, competition was intense, and attractive underwriting opportunities were limited. Many insurers responded by chasing premium growth. Fairfax took a different approach. Rather than competing aggressively for underpriced business, management used the soft market to expand through acquisitions while maintaining underwriting discipline. Despite operating in a difficult insurance environment, Fairfax more than doubled net premiums written during the soft market. Premiums increased from $6.1 billion to $13.3 billion, representing compound annual growth of 16.8%. Most of that growth came from acquisitions rather than increasingly aggressive underwriting. Fairfax was deliberately expanding its insurance franchise while many competitors focused primarily on writing more business. The most significant acquisitions included: Brit (2015): $1.7B Various international insurance businesses (2015–2016): ~$1.0B Allied World (2017): $4.9B Between 2015 and 2017, Fairfax invested approximately $7.6 billion to acquire eleven insurance businesses. These acquisitions significantly expanded the company's geographic reach, product offerings, and underwriting capacity. The timing proved important. Late in a soft market, attractive underwriting opportunities are often scarce, but acquisition opportunities can be plentiful. Weak industry profitability frequently depresses valuations, allowing disciplined buyers to acquire high-quality insurance businesses at attractive prices. In effect, Fairfax was buying insurance assets when they were on sale. This strategy required significant capital. Fairfax issued shares and brought in minority partners to help finance several acquisitions, accepting short-term dilution in exchange for the opportunity to build a much larger insurance franchise. Whether that trade-off would create long-term value remained an open question. By the end of 2019, Fairfax had assembled a much larger and more diversified insurance business. Investors now had to wait for the next phase of the insurance cycle to see whether management's strategy would pay off. Phase Two: Growing Through a Hard Market (2019–2025) The insurance market began to harden at the end of 2019. Premium rates increased, underwriting conditions improved, and attractive growth opportunities emerged across much of the industry. Fairfax entered this environment with a significant competitive advantage. Years of acquisitions had created a much larger insurance franchise through which to deploy capital. Rather than pursuing additional acquisitions, management shifted its focus to organic growth. The results were exceptional. Between 2019 and 2025, net premiums written increased from $13.3 billion to $26.3 billion, representing compound annual growth of 12.1%. Unlike the previous phase, this growth was driven primarily by improved market conditions and disciplined underwriting rather than acquisitions. The hard market validated decisions that had been made years earlier during the soft market. Fairfax entered the cycle with a much larger insurance franchise and was well positioned to capitalize as pricing and underwriting conditions improved. The result was strong premium growth, improved underwriting profitability, and significantly higher float. Just as importantly, it answered the question investors had been asking since the acquisition program began. The larger insurance franchise was creating real shareholder value. By 2025, growth on a per-share basis closely matched the growth of the underlying business. Much of the dilution incurred while building the insurance franchise had been offset through organic growth, improved profitability, share repurchases, and the purchase of minority interests. What Was the Impact? Viewed as a whole, the results are striking. Between 2014 and 2025: Net premiums written increased from $6.1 billion to $26.3 billion. Total investments increased from $26.2 billion to $74.9 billion. Float increased from $11.6 billion to $39.3 billion. Book value per share increased from $395 to $1,260. Shareholders fully participated in the growth, with per-share results slightly exceeding the growth of the underlying business. More importantly, Fairfax successfully adapted its strategy as the insurance cycle evolved. During the soft market, management expanded the insurance franchise through acquisitions. During the hard market, it used that larger franchise to drive strong organic growth, improve underwriting profitability, and generate significantly more investment income. What Have We Learned? The transformation of Fairfax's insurance operations was not the product of a single acquisition or a favourable insurance market. It was the result of disciplined capital allocation across an entire insurance cycle. As the insurance industry begins to soften again, many investors assume growth opportunities will disappear. Fairfax's experience suggests otherwise. The opportunities change, but they do not disappear. Successful management teams adapt. They allocate capital differently as conditions evolve, but they remain focused on the same objective: creating long-term shareholder value. Over the past eleven years, Fairfax demonstrated exactly that.

-

Am I the only one here who's had a rubbish first Half of the year?

thepupil replied to thowed's topic in General Discussion

nope. my IBKR accounts (2/3 of assets i control) are up ~4.5% and SPY and REITs are up 9-11%. my fidelity accounts (the other 1/3) are up 8%. my 401k's and stuff (currently all TIPS) are up 8%-9%. Trust (which basically just owns global indices minus fees) and I don't control is up 8.5% or so. mediocre year so far. I've not been particularly excited about my portfolio for like 2-3 years. think generally have bought things at okay-ish discounts but actual value coming in a little shy of underwriting as my (mostly) real estate oriented stuff continues to grapple with money having an actual cost. feel like most of my ideas are pretty stale...been some small wins here and there but nothing too additive...the last few sell-offs (Iran / Tarriff / etc)...I've generally way outperformed as market fell, but then not really taken advantage of the bounce...there's a younger more aggressive version of me that would have rotated/found a way to make more on the way up...but that hasn't been me of late....i also just take less concentration/risks generally....i'm playing a little scared because...i don't want to give up the last ~6 years of wild gains over which my NW has like quintupled (inheritance + compounding + saving + a little bit better than mkt returns)... -

I know a bunch of you have done great things in 2026 (Officer with Liquidia, GFP picking stuff up with amazing timing etc.), but it just hasn't been working for me. There have been one or two mistakes (e.g. trying to play oil - seemed obvious at the time) but generally longer-term holdings have just not had a great time. Decent chunk of FFH, decent chunk of CSU & subsidiaries, TVK (unfortunate situation) and not trimming enough Gold & Royalties. Recently buying Exchanges as they've continued to go down. Not seeing the switch up at the end of March. Ooof. Other things have worked, thankfully, but I'm pretty flat for the year, which is quite the underperformance to the S&P. Anyway, I know it's only 6 months, and I'm happy to leave these things to do their thing, as I'm not really a trader. Just good to get it out sometimes. Anyway, hopefully I'm the only one, but please grumble alongside me if you've struggled too.

I know a bunch of you have done great things in 2026 (Officer with Liquidia, GFP picking stuff up with amazing timing etc.), but it just hasn't been working for me. There have been one or two mistakes (e.g. trying to play oil - seemed obvious at the time) but generally longer-term holdings have just not had a great time. Decent chunk of FFH, decent chunk of CSU & subsidiaries, TVK (unfortunate situation) and not trimming enough Gold & Royalties. Recently buying Exchanges as they've continued to go down. Not seeing the switch up at the end of March. Ooof. Other things have worked, thankfully, but I'm pretty flat for the year, which is quite the underperformance to the S&P. Anyway, I know it's only 6 months, and I'm happy to leave these things to do their thing, as I'm not really a trader. Just good to get it out sometimes. Anyway, hopefully I'm the only one, but please grumble alongside me if you've struggled too. -

Article 3 in our deep dive into Fairfax's insurance business. The Insurance Cycle: How Great Insurers Exploit Opportunity The P/C Insurance Cycle Understanding Hard Markets, Soft Markets, and Why They Matter Before investors can understand Fairfax's growth history, they first need to understand the property and casualty (P/C) insurance cycle. Unlike most industries, insurance pricing moves through long periods of expansion and contraction. These cycles influence growth, profitability, capital allocation, and ultimately shareholder returns. They also help explain many of Fairfax's most important strategic decisions over the past forty years. Understanding the insurance cycle is therefore essential to understanding Fairfax. What Is the Insurance Cycle? The property and casualty insurance industry moves through recurring periods of strong and weak pricing. These two phases are commonly known as hard markets and soft markets. Hard Markets Premium rates rise. Underwriting standards tighten. Capacity becomes scarce. Profitability improves. Soft Markets Premium rates fall. Competition intensifies. Capacity becomes abundant. Profitability deteriorates. These cycles often last for many years and can swing to extremes. Successful insurers therefore manage their businesses with a long-term perspective rather than reacting to short-term conditions. Understanding where the industry sits in the cycle is important because it affects an insurer's growth opportunities, profitability, and ability to create long-term shareholder value. Why Does the Cycle Exist? The insurance cycle exists for much the same reason financial markets experience booms and busts: human behavior. When profits are strong, insurers become increasingly willing to compete for business. New capital enters the market, underwriting standards loosen, and pricing gradually weakens. Eventually, profitability deteriorates. As returns decline, the process reverses. Capital leaves the industry, underwriting standards tighten, and pricing improves. The result is a repeating cycle driven by greed and fear. Like Benjamin Graham's Mr. Market, the insurance cycle provides investors with a useful mental model. Markets are not always rational, and neither are insurance companies. Reinsurance executive Paul Ingrey captured this process in his well-known Underwriting Cycle Clock, which illustrates how insurers repeatedly move through periods of discipline, optimism, overexpansion, deteriorating profitability, and recovery. The cycle persists because industry participants repeatedly make the same behavioral mistakes. Exhibit: Paul Ingrey's Insurance Underwriting Cycle Clock Reinsurance executive Paul Ingrey developed the "Underwriting Cycle Clock" to illustrate how strong underwriting profits attract capital and competition, eventually leading to weaker pricing and deteriorating underwriting results. As losses mount, capacity leaves the market, discipline returns, and the cycle begins again. The lesson is straightforward: the cycle is driven by human behavior. Companies that remain disciplined while competitors chase growth are often the long-term winners. Source: Arch Capital Group Limited Why the Cycle Matters The insurance cycle creates opportunities for disciplined insurers. During soft markets, the best companies focus on underwriting profitability and preserving capital. Growth becomes secondary to maintaining discipline. During hard markets, those same companies can deploy capital aggressively, write more business, and earn attractive returns. Many insurers struggle because they do the opposite. They pursue growth aggressively when pricing is weak and profitability is poor. By the time a hard market arrives, they often lack the capital needed to take full advantage of the opportunity. The most successful insurers are therefore not those that grow the fastest. They are the ones that remain disciplined throughout the cycle. For investors, the key lesson is simple: the insurance cycle itself is not the risk. The real risk is owning an insurer that cannot navigate it effectively. The Berkshire Hathaway Model No company has exploited the insurance cycle more successfully than Berkshire Hathaway. Warren Buffett understood that insurance companies possess a unique advantage. They collect premiums today while many claims are not paid until years later, creating float that can be invested until it is needed to pay future claims. Most insurers invest this float conservatively, primarily in bonds. Buffett combined disciplined underwriting with superior capital allocation. Because insurance cycles unfold over many years, Berkshire never felt compelled to chase premium growth simply to satisfy quarterly expectations. When pricing became unattractive, Buffett was willing to let business shrink and patiently wait for better opportunities. That flexibility became one of Berkshire's greatest competitive advantages. During hard markets, capital flowed into insurance. During soft markets, it could be allocated to stocks, wholly owned businesses, acquisitions, or share repurchases. A soft market therefore changed where Berkshire invested capital—not its ability to create value. Fairfax and the Insurance Cycle Fairfax has followed a remarkably similar approach. During the prolonged soft market from roughly 2014 through 2019, Fairfax expanded primarily through acquisitions. Purchases such as Brit and Allied World significantly increased the company's insurance platform while industry valuations remained depressed. Fairfax was effectively buying insurance assets when they were on sale. When the market turned in 2020, management shifted its emphasis toward organic growth. Strong pricing allowed Fairfax to expand premiums while maintaining underwriting discipline. As a result, Fairfax grew successfully during both phases of the cycle. Acquisitions drove growth during the soft market. Organic underwriting drove growth during the hard market. Equally important, the company improved the quality of its insurance operations throughout the process. Like Berkshire Hathaway, Fairfax is more than an insurance company. It is also an investment company and a capital allocator. Prem Watsa's significant ownership stake and voting control have allowed Fairfax to manage the business with a long-term perspective. That has helped the company remain disciplined through multiple insurance cycles while allocating capital wherever opportunities have been most attractive. When underwriting opportunities become less attractive, Fairfax can redirect capital toward acquisitions, public equities, private investments, debt reduction, or share repurchases. A soft market may slow premium growth, but it also creates opportunities elsewhere. What It Means for Investors As the insurance market begins to soften, investors often assume the industry's best years are over. For many insurers, that concern may be justified. But Fairfax is not a traditional insurance company. Like Berkshire Hathaway, Fairfax combines disciplined underwriting with investing and capital allocation. Changes in the insurance cycle influence where capital is deployed, but they do not determine whether value can be created. Poor insurers become victims of the cycle. Great insurers use the cycle to their advantage. Fairfax's forty-year record suggests it belongs in the latter group. Throughout multiple insurance cycles, management has followed a consistent approach: remain disciplined when opportunities are scarce, act decisively when opportunities are abundant, and allocate capital with a long-term perspective.

-

Are you buying via Prosus or the ADRs/HK listed shares? I’m buying via Prosus for a few reasons, but dislike the company outside the Tencent investment..

-

https://finance.yahoo.com/markets/stocks/articles/tencent-ramps-buybacks-share-rout-002809157.html This is best price/quality thing I see now alongside Nintendo. The flaws of both are well-known. Pick your poison.

-

"People who live in glass houses shouldn't throw rocks" Strains credibility when a Trump supporter complains about corruption elsewhere. I know you think Trump can do no wrong but some might view the present level of corruption in the 'first family" will likely be found to have been unprecedented.

-

I went long the Iran sell off in spring this year and I had decent sized position in the June 2026 ES with average price in 6400s but I sold that shit like a dumbass at 6640 and watched as the ES rallied another 800 points. Sure I picked off 30 points here and there jumping in and out during the vertical rally but it was like getting the vacuum cleaner consolation prize when I could have won the brand new car on Price is Right For second half I am hoping there is a decent sized crack in the markets that I can take advantage of - coming into this year I thought after 3 straight years of double digit returns in the SPX, this could be a year when the markets are UNCH and I still think that

-

Hey if Berkowitz wants to hand you cheap stock, all you need to do is hang on. The historical migration to Florida will go on for years. It's the happiest state I know!

-

Sold all the VOO I bought earlier this month

-

Thank you, Mike [ @cubsfan ], Yeah, it's also about trying to relate to the issues at hand discussed in in the JOE Investment Ideas forum, especially related to time horizon. The plan to execute on going forward presented at the JOE AGM looks good to me.

-

Another idiot academic loses her University teaching position: https://jbhe.com/2026/06/indiana-university-lecturers-contract-ends-following-lesson-linking-maga-to-white-supremacy/ https://indianacapitalchronicle.com/2026/06/11/iu-lecturer-disciplined-for-white-supremacy-lesson-faces-termination/ Jessica Adams, a full-time lecturer on IU’s Bloomington campus, found herself in trouble in September when a student said she used a graphic identifying “Make America Great Again” as an example of covert white supremacy in her class on diversity, human rights and social justice.

-

-

Exactly - they've absorbed the lessons of opportunity, hard work and individual accountability - and left the "experts" that tell everyone else what to do, like teachers and social justice warriors - to ruin those important concepts. Those useless degrees could just as easily be earned by watching TV all day.

-

+1 I wouldn’t have even heard of the company without @whatstheofficerproblem

-

Sold remainder of $PSMT. Small position that I didn’t have a lot of confidence in that worked out really well, Cost basis $60.