All Activity

- Past hour

-

Well, it's also important to consider where they are currently allocating capital. -KW, is questionable for me based on said company's own shareholder returns last 5, 10 or 15yrs. But we will remain curious. -UA a classic dumpster diving investment down 90% from its peak. -Sleep county remains to be seen. -Andrew Peller which also don't seem particularly cheap or particularly high moat businesses. Whilst I acknowledge they have had a good 5yr run, that was after a long drought and it's by no means certain to me that they have had some sort of eureka moment and this will continue. For that reason, I'm generally a bigger fan of share repurchases than most of the above acquisitions. However only time will tell. Despite all that, I remain invested because of what I said previously, the better mouse trap that they have. And that helps enormously over the long term. I definitely do believe the insurance companies have turned a corner. They are much larger, more diversified across both lines of insurance, and geographically, and have better underwriting standards. Their float is now in excess of $40B and I think interest rates are going to be persistently higher for longer than people are currently expecting just as a function of global sovereign debt levels and inflation risks. Thats powerful with their total investment portfolio 3:1 leveraged. I do generally trust their prudent overall risk management as they have a lot of skin in the game.

- Today

-

Ah yes how conveniently you forget how the Shah got into power. It was the US and UK that orchestrated a coup that destroyed democracy in Iran to bring a dictator to power and so he could give 40% of Irans oil to western companies. The Shah was a US/UK puppet who was terrorizing Iranians. Also read up on the atrocities that followed the coup and understand the reason why the revolution took place.

-

No, i dont think thats likely. But its still cheap and the EPS will expand this year because the USD weakness has hidden some of the operational power (25% operating income growth this year). And 10-20% growth with a 3.4% dividend yield is always nice to have. Theres a thread about it.

-

Is there a reason you use 15 years as the benchmark? Buffett has said that 5 years is a good timeframe to use to evaluate a management team. That is my preferred measure. Does year 6 to 10 performance matter? A little, but much less IMHO. What about year 11 to 15? Interesting… but too long ago to matter much IMHO. For instance… back in 2013, I did not use a 10 or 15 year timeframe to evaluate Fairfax’s management team at the time (their investment returns). That would have been pretty dumb, given the CDS and equity hedge positions (that worked fabulously well from 2007-2009) would have completely skewed results. The best way to evaluate Fairfax in 2013 was to look primarily at what they owned at the time, how the positions had performed recently (prior 5 years), and what their prospects were (next 5 years). (I did that and then sold all my shares in Fairfax.) Imagine using a 15 year timeframe to evaluate management at BlackBerry back in 2013? It would have told an investor to back up the truck… Really? One of the benefits of using 5 years is it makes calculating rate of return easier. Fairfax has a very concentrated portfolio: Eurobank FFH-TRS Poseidon Fairfax India - primarily BIAL Orla Mining Do I care today that Eurobank was a terrible business in 2014? Nope. What I care deeply about is what kind of business Eurobank is today - and it is a very good business. Could that change? Of course… that is why I listen to every quarterly call). Holdings get much smaller after the big 5. But there are a bunch of stars in there as well. Fairfax’s hit rate the past 5 years is nuts. To this, add the returns on the holdings they sold in the last 5 years: Resolute Forest Products Stelco Sigma Orla (part) Poseidon (part) All were massive home runs (5-year returns). And then, of course, we should also add the gains on the insurance businesses they IPO’d/sold in the last 5 years… this needs to get counted somewhere… Digit Pet insurance Ambridge Euolife’s life insurance business More massive gains… After all, at the end of the day, we are trying to evaluate a management team on their capital allocation skills. It should be fair and balanced and look at all the important pieces. How has Fairfax performed over the past 5 years? They have smoked - absolute and relative to the S&P500. Especially if you use the correct cost basis: FFH-TRS cost basis is not the starting value of Fairfax’s share price. It is much less. Interestingly, the last 5 years had two bear markets: 2022 and 2025 (I think just qualified). There was also a historic bear market in bonds. Yes, the starting point (Dec 31, 2020) was very favourable. But that is when you look at performance vs the S&P500. For the past 5 years, Fairfax’s capital allocation has been best-in-class and it is not close. The fact that people don’t get it is not surprising - this is Fairfax after all.

-

What you fail to realize is that the Iranian behavior over the past 47 years has never been rational. Iran was not at war with the US at the time of the revolution, instead Iran chose to take Americans hostage - an action that would have caused the Soviets to nuke them. Iran chose to fund Hezbollah which bombed Marine barracks in Beirut in 1983. Iran chose war against the US, it was not forced into it. Similarly with Israel, Iran was not a war with Israel in 1979, as a matter of fact, Israeli engineers built the Teheran water system. Iran chose to start a war against Israel via proxy. As a matter of fact, is it rational to fund Hamas and Hezbollah which are dedicated to the destruction of Israel? If one country is dedicated to wiping out the other, the logical conclusion is that it risk being wiped out itself! Is it rational to attack a country that is not at war with you, let alone a country that is armed with nukes? Iran chose to attack two countries - US and Israel. If you think that is rational, what is not rational in your opinion?

-

Sorry I think your cognitive dissonance is leading you to rationalize what he said as if he meant someone else other than the Iranian regime currently running Iran that negotiated and signed the MOU. I get it, it must be jarring to vote for a guy thinking he'd be aligned with your views on Iran and to now find him inverting the standard talking points so violently. Trump, as many have said about him personally, will eventually always screw you over somehow. The GOP/DNC party line forever (essentially the Israeli self -serving caricature) is that Iran is an irrational, suicidal death cult.........Trump in one fell swoop re-characterizes them as rational, pleasant to deal with and only looking out for their people....he's also recently said that you know maybe they can keep their civilian nuclear enrichment as others have one and as regards ballistic missiles....more or less "why wouldn't they want to keep what others in the region have!" He's something else. I'm sure Miriam Adelson is wondering if $250m in political donations are refundable right now as she listens to this administration flip the Israeli talking points on Iran. I've always seen through the Iran caricature as just that (but at the same time recognizing the repression there) but I'm as shocked as anyone to hear a US President invert that caricature so publicly and forcefully! Crazy times.....Trump's great legacy was the switch in posture he instituted re: China.....a China engagement strategy was dogma in D.C. when he arrived, when he left in 2021 that had switched to containment......I wonder if this time around the dogma he'll dismantle before he leaves is D.C's unquestioning consumption of Israeli talking points as American foreign policy and move towards looking at Israel as just another ally and M.E. as a region that is better left to self-stablize after decades of the US/Israel attempting to 'fix' it.

-

Sure, when you line up their accomplishments side-by-side of course it's going to look like Obama is 100x the POTUS that Stumpy is...but what you don't realize is that Obama was black and that makes people uNcOmFoRtAbLe!

-

With all due respect, has the equity book outperformed the S&P over the last 15 years? By the way, there have been plenty of incredible opportunities in both US and non-US. Why buy Eurobank when you could have bought Aena, Halma, Diploma, Asml, Hermes, Sartorius Stadim Biotech, Safran? Why buy Blackberry, et all when Alphabet, Microsoft, Meta, Nvidia, Micron, Moody's, S&P Global, Idexx, Heico, Transdigm, GE, RSG & WM, and the list goes on were available? Why are we so proud of buying crappy businesses at 50 cents on the dollar when Nvidia was trading at 5 cents on the dollar 5 years ago?

-

@Parsad wealthy persons such as you should be able to get net-jets to take you to your favored destinations. https://blackjet.com/post/how-much-is-netjets-25-hour-card

-

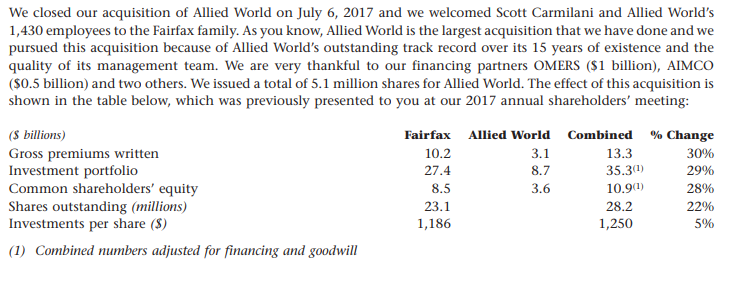

Not to be nitpicky here but just to clarify, I'm not sure I would have called the stock fairly valued during this transaction. Fairfax issued 5.1 million shares at a P/B of only 1.06 to acquire Allied World. Of course it has worked out great over the years, but I don't remember it being an obviously good move at the time. From the 2017 annual report:

- Yesterday

-

Not just in Canada. If US markets are closed you can pretty much bet that some weird things happen in other markets that are open. I had for example an order open for more Prosus (PRX) for 38.41 that got filled for 38.215 which also happened to be the low in IBKR today. Small potatoes but good stuff . I think the liquidity totally sucks on days like this and if some ETF rebalance or something similar at the end of the day, they just take whatever they get. It’s OPM, who cares, right?

-

Cheap drones are the new Molotov cocktails for their age. We have fast fashion in retail and now fast destruction in defense.

-

Hard to beat this advertisement:

-

Unusual dump at the close in Canada today on both FIH.U and FFH - got filled on several orders near the close. What a weird finish to an otherwise very slow day with US markets closed. Fairfax India went from 17.90 to 17 in a few minutes

-

Funny that i have a very large % ADBE position but don't pay for them. Funny enough. I integrated my AI agent with a MCP for GIMP this week. So now i can tell my agent to edit stuff and It opens GIMP on my computer and starts editing the image there. Instead of just "attempting to regenerate a new image" with nano banana or whatever. Im 100% confident this is underway with ADBE to where they will make a MCP that is callable via API's to paying customers that charges on a token system that will enable your AI generated image to get cleaned up at the pixel level using their software suite. There will always be cheap chumps like me using GIMP. But ADBE will remain and it will become standard and more robust within all enterprises. the freemium offerings are just to ensure that new rising generation of workers continue to stay in and close to the ADBE ecosystem.

-

I recently listened to a podcast that perfectly captured where we are today: we are currently in the "command line" era of AI. Everything is in its infancy and exploratory phase. The technology relies on us forcing static prompts into isolated models, doing the heavy lifting of copy-pasting and workflow coordination ourselves. But the truly interesting phase is going to happen when the infrastructure layer—the chips, power, cooling, and data centers—finally stabilizes. Once these physical bottlenecks clear, the market value will inevitably migrate upward, splitting into a few distinct waves: The Agentic Orchestration Plane: Autonomous software layers that act as the hands and feet for AI, plugging directly into the deep, messy, legacy systems that actually run global enterprises. Proprietary Data Fabrics: High-performance retrieval-augmented generation (RAG) networks that monetize proprietary, domain-specific data context rather than raw, commoditized computing power. Verticalized AI-Native SaaS: Hyper-specialized software giants scaling up usage and adoption within their own niche verticals, moving from seat-based licenses to full task automation. There is a investment arbitrage sitting in the market right now. Because Wall Street is looking at this through a clouded window, it is pricing many SaaS giants like dying, low-margin utilities. The market is completely blind to how early this cycle is, and is missing the impending transition of these software platforms profitable, consumption based autonomous execution engines. While the hardware grid is heavily priced in, the data, orchestration, and security layers quite attractive as everyone is chasing the capex in semi's and datacenters.

-

Added to BOLSAA and PRX (Prosus) on this quiet day.

-

This is probably a bubble.. but it is too obvious, and too many people are calling a bubble, which probably means it is not ready to pop. So other than identifying the current bottle necks (that everyone already knows and has bid up).. lets have some fun and put our minds together instead of trying to time a top guess what the next rotation will be. I'll start... I think the next rotation will be into small cap stocks. YTD VB is outperforming VOO. To me small cpas seem like low hanging fruit in terms of benefiting from AI. Large bureaucratic organizations are slow to move, and rolling out AI across a large organization is expensive, but I could see smaller companies quickly adopting. I think it is probably a counter intuitive take since if we are truly late cycle with rising interest rates then small cap's probably don't outperform, but we have seen a lot of weird stuff happening like Gold rallying during a bull market, bonds and stocks dropped during 2022, etc.. I am curious what other ideas are out there?

-

Probabilistic investing often looks like luck.

-

Over the last couple weeks sold a bunch of Dec. 2028 BRK puts ATM and slightly out of the money. $35-$40 at strikes between $460-480

-

speculating on a take over?

-

Dealraker, I think you missed the Art of the Deal here...Trump is luring Iran into negotiations with honey...everyone knows Iranian's love honey, especially in their baklava-like desserts! You beat them over the head with missiles, then give them everything they want plus some honey (especially Mamuka), and then WHAMO...you get them to sign over all of their nuclear material! Works every time. Cheers!

-

That’s what makes a market. I don’t expect them sell at these prices. I think they will ultimately sell the whole bank to a much larger European bank at a premium which will facilitate the exit.

-

Nice.

-

Yes. It is a bank. In Greece. That doesn't mean it can't compound nicely from here. But should it trade at much higher multiples? No.