All Activity

- Past hour

-

One of the most pro-Trump leaders in Europe: https://www.bbc.co.uk/news/articles/cgqj77909jpo A perfect example, if one was ever needed, about why it’s pointless to try and be Trump’s friend. Because if you aren’t kissing his ring constantly he’ll turn on you.

-

Ya come into my kitchen buddy, ya gotta take the heat The art of the haggle was well practiced, well before the art of the deal. Global Inventory will continue to drain, along with high US gas prices, all the way through the midterms. Orange Boy ain't got the cards. The haggle is just being friendly; recognise the entertainment value, and play the game. Play well ... and we can make you a deal between friends . SD

-

Counter drone technology is way behind and needs to catch up.

-

Netjets doesn't fly to small towns in BC. Also I would feel ridiculous flying on a Citation jet or slightly smaller all by myself every month or other month...even with a couple of other people it seems like such a waste of resources...money and jet fuel! That's a lot of other luxury trips I could take around the world flying in business class! Plus I'm not at Eff You Money yet...I'm at I Don't Need Your Dumb Ass, So Don't Waste My Time Money! Cheers!

- Today

-

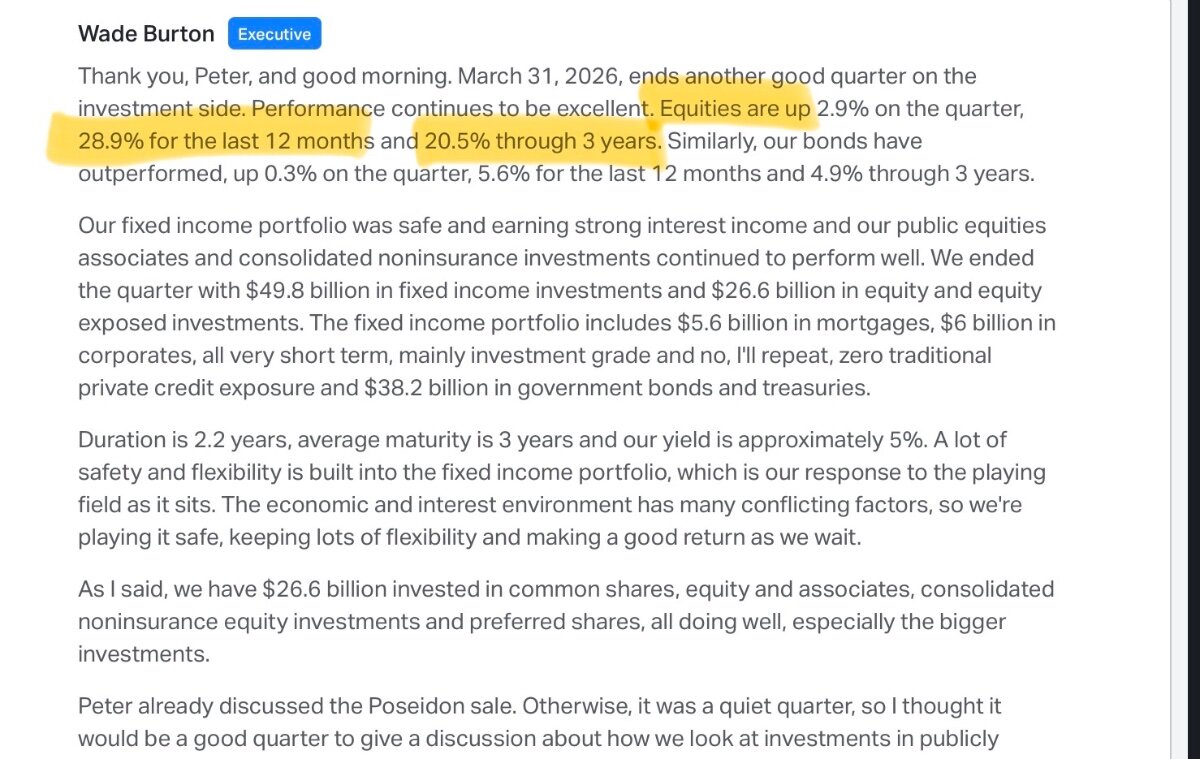

I think it was 19% over 39 years but I can’t find the reference. Last three years have been good as we know but most of it hasn’t shown up in accounting returns yet.

-

The market structure changed a lot during the period you are focused on. I think if you are uncomfortable with leverage you shouldn’t own Fairfax. I see the leverage as a feature not a bug. They did change their investment style by taking more control and significant influence positions (which hurts reported returns up front) but not their process of looking for margin of safety. Again beating the index is an outcome of the process not the goal. Most institutions since the GFC are focused on short term relative returns b/c they want to keep the AUM. Thankfully we don’t have to play that game.

-

I doubt there was much of an uptick in oil getting out of the strait, with the mines still in place. It found it interesting to see oil drop below $80 without much changing in the flow of oil shipments. I think we will see another 2 months of little oil movement, with oil reserves continuing to drop.

-

Yes and no. Yes, you cannot eat relative returns, but if the S&P returns 15% per annum for 15 years while your equity portfolio returns 10% per year for 15 years, then clearly the people running the equity book are incompetent. As markets change, your investment style has to change. With all due respect, you could have bought plenty of incredible business at low multiple of earnings - ASR in 2004 is a good example (airport concessions in Mexico at 5x free cash flow.). If you need leverage to make your equity portfolio match the S&P then why not just be long S&P and avoid the issues that come with leverage?

-

The SOH is now closed but good deal for you my friend. We are in the bargaining stage where every barrel of oil comes with unlimited middle eastern haggling. The rug merchants are now in charge.

-

Sure, that is even better. What is the company's 40 year track record when it comes to its equity book?

-

How about 40 years?

-

I agree with you that 5 years is enough, but the longer the time period, the more accurate is the evaluation. An organization that beats the S&P over five years but trails over 20 is not very good. This is why I chose 15, you are free to choose 20 or 25.

-

Don't confuse them with history. Nor with sensible questions.

-

My cognitive dissonance, LOL? The thread that just keeps on giving.

-

Are any of my fellow CofB&F members considering ordering [by now : preordering, [until 23th June 2026]] this book : Regime Change - Maggie Haberman & Jonathan Swan ?

-

The goal isn’t to outperform the S&P, it’s to generate absolute returns. Over time the process should outperform the S&P especially when the leverage is included. This most recent 15 year period the backdrop was particularly difficult for this investment style because of the change in market structure. Further, the decision by Fairfax to accumulate more significant influence and control positions ensures that the accounting returns lagged economic returns since 2012. While the lag continues, the gains are coming pretty regularly now as the strategy has matured.

-

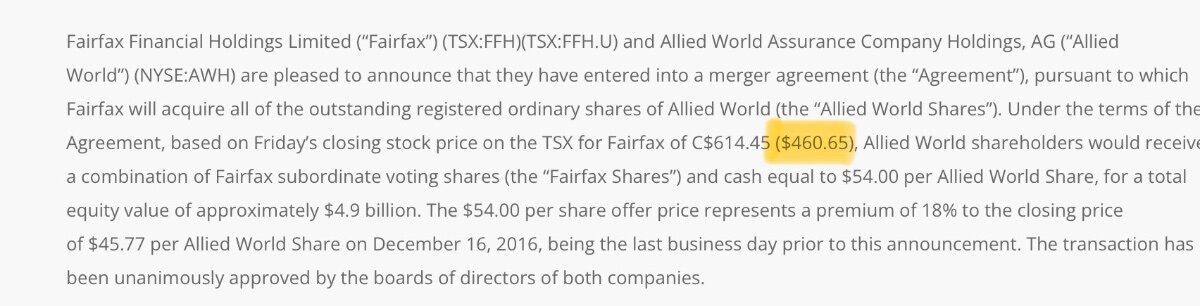

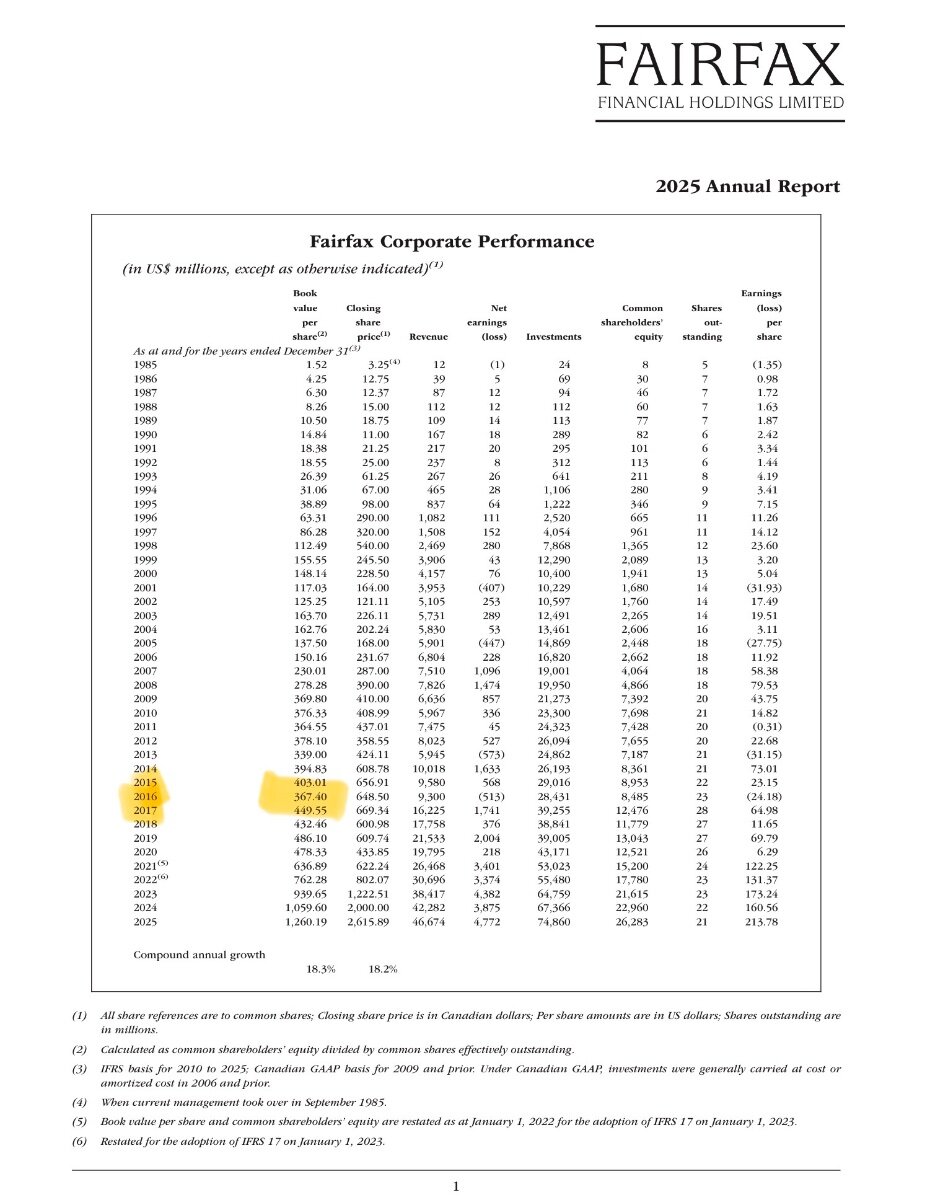

When they announced the deal in December 2016, the stock was trading closer to 1.3x BV. That’s when the Allied World BOD signed the definitive agreement. In March 2016, they also issued equity for closer to 1.4x BV. This was in a backdrop of low interest rates so ROE was structurally lower.

-

And Trump does what Trump does, there's 55 plus years of it laid open for view. He creates total chaos, his tag along's elope into some bizarre claims of success while others gape at what is complete failure, failure, and more failure. Trump sneaks in his paychecks, one after another, always plain out in the open corruption. 2nd grade special needs kids can make that determination but the tag along's choose not to. Why? You got it! Trump looks the part. He's got the John Wayne thing. It takes 1 and 1/2 hours of makeup, hair preparation, and massive body enhancements within the black suit, but we get there. Different voices, unique childlike facial expressions, it all sells and sells to the tag along crowd. All these years for Trump and there's no legitimate business for his "wealth" only scam bezel fake shit. Yet it works, and works, and works, the more stretch his followers do to legitimize - the more committed they are to believe. Bookmark this if you are young because this is the craziest garbage you will ever see in your lifetime. The next person who tries this shit won't have success such as this. Trump owns the world...for now. My extended family of businessmen, some fabulously wealthy remind me that I'm not coming up with the main theme that allows all this to happen. They tell me it is fear, that no matter how much wealth or power anyone has today they all fall in line with this fruitcake goofball because of fear.

-

In the past few days i am thinking about how the digital euro (not wero) will change payments in europe and i can't see how MA&V +european banks aren't the losers of this. Why is this not priced into these companies today? Every merchant will try to get customers with bonus systems to switch over like it worked in Brazil and India and every merchant+bank will be forced to use/offer it. The merchant payment processors doesn't seem to be impacted because they can still earn their fees. Just Ayden will lose its interchange fee because it is also the bank, so overall i think that Ayden will probably lose the most of all the merchant payment processors in europe because for a merchant than the fees aren't material different to other payment processors?

In the past few days i am thinking about how the digital euro (not wero) will change payments in europe and i can't see how MA&V +european banks aren't the losers of this. Why is this not priced into these companies today? Every merchant will try to get customers with bonus systems to switch over like it worked in Brazil and India and every merchant+bank will be forced to use/offer it. The merchant payment processors doesn't seem to be impacted because they can still earn their fees. Just Ayden will lose its interchange fee because it is also the bank, so overall i think that Ayden will probably lose the most of all the merchant payment processors in europe because for a merchant than the fees aren't material different to other payment processors? -

CNN - Politics [June 19th 2026] : Italian foreign minister cancels trip to US over Trump’s comments about Meloni - - - o 0 o - - - -And the temperamental Italian blonde - most of the time dressed in white - gets all worked up of the eigthy years old pro, experienced womanizers comments about her! - So much for that good personal relationship! International Politics anno 2026! - You can't make this up! - - - o 0 o - - - In politics, there are things you just don't engage in, especially towards women!

-

About what you would expect from a Trump friend and donor...literally looks like the profile pick for any Trump "organization"/mafia associate! No bid friend/donor who destroyed the reflecting pool! Cheers! https://www.yahoo.com/news/politics/articles/company-owned-by-trump-donor-won-17-million-no-bid-reflecting-pool-contract-000248757.html

-

KW is an interesting company. I totally agree with you - retail shareholders in KW got taken out behind the woodshed owning the stock. But my read is Fairfax did ok. The stock they owned was table-stakes (as Jamie Dimon would say). It got Fairfax access to Kennedy Wilson’s deal flow. Real estate partnerships. Mortgage loans. ThePacWest deal was an absolute home run for Fairfax (still is). And in the end, it also allowed Fairfax to take KW out on the cheap (at least that is my initial uneducated read). Real estate is deeply out of favour - this is likely an ideal time to buy something like KW. Now having said all that… KW is a bit of a complex beast… so I could be completely off base in terms of how it works out for Fairfax. We will see. It reminds me a little of when Fairfax took Recipe private when Covid was still a thing here in Canada - Fairfax got it cheap (in terms of buying when there was a lot of pessimism).

-

Can you explain to me what the financials look like for each investment? What was the money Fairfax put in? (That is not the reported deal price.) What is the (likely) return they are going to generate off it in the coming years? Bottom line, I am being open minded with their new purchases. One reason is I haven’t spent a lot of time trying to understand them. I will get around to it. Another reason is Fairfax has been hitting the ball out of the park - as a result, I am giving them the benefit of the doubt. i don’t expect them to be perfect. Some investments will look like clunkers. Lynch said if you are right 6 times out of 10 you will do well in this business. I am not worried when it comes to Fairfax’s equity portfolio these days.

-

Well, it's also important to consider where they are currently allocating capital. -KW, is questionable for me based on said company's own shareholder returns last 5, 10 or 15yrs. But we will remain curious. -UA a classic dumpster diving investment down 90% from its peak. -Sleep county remains to be seen. -Andrew Peller which also don't seem particularly cheap or particularly high moat businesses. Whilst I acknowledge they have had a good 5yr run, that was after a long drought and it's by no means certain to me that they have had some sort of eureka moment and this will continue. For that reason, I'm generally a bigger fan of share repurchases than most of the above acquisitions. However only time will tell. Despite all that, I remain invested because of what I said previously, the better mouse trap that they have. And that helps enormously over the long term. I definitely do believe the insurance companies have turned a corner. They are much larger, more diversified across both lines of insurance, and geographically, and have better underwriting standards. Their float is now in excess of $40B and I think interest rates are going to be persistently higher for longer than people are currently expecting just as a function of global sovereign debt levels and inflation risks. Thats powerful with their total investment portfolio 3:1 leveraged. I do generally trust their prudent overall risk management as they have a lot of skin in the game.

-

Ah yes how conveniently you forget how the Shah got into power. It was the US and UK that orchestrated a coup that destroyed democracy in Iran to bring a dictator to power and so he could give 40% of Irans oil to western companies. The Shah was a US/UK puppet who was terrorizing Iranians. Also read up on the atrocities that followed the coup and understand the reason why the revolution took place.