TwoCitiesCapital

-

Posts

4,967 -

Joined

-

Last visited

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by TwoCitiesCapital

-

https://finbold.com/investors-ditch-the-euro-and-pound-for-bitcoin-in-record-numbers-as-their-value-plummets/ Record amounts of EUR and GBP buys, not mirrored by USD volumes, suggest people are fleeing those currencies and not just speculating in BTC. It's also telling that by buying BTC, they're casting a vote of confidence in it being the best store of value/currency alternative b/c they could've bought the USD, gold, or any other currency.

-

As mentioned, via funds and ETFs. Most of my fixed income positions are held in 401ks, HSAs, and etc where options are limited and I can't do individual securities. TLT/ZROZ/RGVGX are the primary Treasury funds I use to increase/decrease duration from money market/bank deposit type investments. I have a few intermediate corporate/core funds as well, but they're small relative to the Treasury position since spreads have not yet widened as has been pointed out by others. I also switch some of my mixed exposures from things like Pimco's StocksPLUS funds to their StcoksPLUS Long Duration fund which gives me an incremental duration/yield pick-up without changing the equity exposure and leverages dollars put in the market nearly 2:1. As far as agency bonds, there are funds/ETFs that track those as well. Or you can take a levered bet by buying agency mortgage REITs like AGNC which is what I've started adding.

-

I've been slowly increasing duration for this is exact reason. 10-30 year treasuries are all yielding around 4%. If the Fed cuts back to zero, it's highly probable these bonds go up 15-30% in an environment where equities are down an additional 20-30%. And all of that assumes the 10-year stops @ 2% for the bottom which may not be the case. Not a bad hedge IMO. I've been moving a number of my short-term bonds funds to intermediate exposures and adding small positions in ZROZ/ TLT now that 10-year treasuries are back above 3.5%. And if you don't want as much duration/credit exposure, agency mortgages at 6-7% is crazy. Especially if you think that the refinancing wave from lower rates doesn't hit due to negative equity in all of the newly issued mortgages...

-

Where Does the Global Economy Go From Here?

TwoCitiesCapital replied to Viking's topic in General Discussion

Crazy thing is that's it's pretty well known that rents lag prices by somewhere between 4-6 quarters. So it was pretty easy to forecast they would rise after home prices had risen 20+%. And now that they appear to be plateauing, probably pretty easy to say that rents might be a little softer in 12-18 months as well - even if the Fed stops hiking rates during that time. -

Where Does the Global Economy Go From Here?

TwoCitiesCapital replied to Viking's topic in General Discussion

You can only say they were underestimated in hindsight. I'd say right now everyone has underestimated the Fed so far which is why this sell off occurred in the first place. Whether that underestimation continues remains to be seen, but to say this is different because the severity has been correctly estimated can only be said in hindsight - seems crazy to say markets are getting it exactly right now when they got it wrong over the preceding 10 months. And I'm also gonna guess that the severity of the earnings contraction has yet to be priced in because analysts aren't yet reflecting a contraction in their estimates - just slower earnings growth -

Where Does the Global Economy Go From Here?

TwoCitiesCapital replied to Viking's topic in General Discussion

Was 2008 priced in when we were down only 20%? Was 2020 priced in when we were only down 20%? Was the Fed hiking rates priced in in March 2022? If you look at earnings estimates, they don't yet reflect a contraction that is near certain to come IMO regardless of how "well known" or "priced in" it's supposed to be. -

Where Does the Global Economy Go From Here?

TwoCitiesCapital replied to Viking's topic in General Discussion

There's a 30% chance that it will if you're in a vacuum and considering no additional information. But if you are a fan of Bayes, than we must update the marginal probability with new information. The new information being way above average inflation, commodity input prices significantly higher than a year ago, interest rates at 12-year highs, the USD at 20-year highs, the starting near record valuations, and the Fed being aggressive with interest rates while the economy is already in a technical contraction. All of those would typically point to the risk of it being well in excess of the 30% that prices may be lower. Just like the probability is probably quite a bit less than 30% in the year following a recession. Until the Fed capitulates, the risk is falling profits in an environment where multiples are still elevated and a Fed that is still removing massive amounts of liquidity from the market. I'm still buying stocks - commodity companies and Fairfax are still cheap. Things like Porsches IPO and Stelco's tender above the current price provide opportunity. But ultimately will be quick to take gains and have a higher allocation to fixed income/cash than I'd otherwise like. -

Where Does the Global Economy Go From Here?

TwoCitiesCapital replied to Viking's topic in General Discussion

70% of the time you didn't have CAPEs at 30+ heading into an inflation above 9%. 70% od the time you didn't have dollar at 20+ year highs. What matters is the relevant comparables - not all data ever. There's NEVER been a time where CAPEs were this high with inflation this high. All relevant comparables has CAPEs @ like 15 or less. We started at 30. Historically, higher rates and higher USD and higher oil led to contractions in corporate profits. USD is @ 20-year highs, US rates @ 12 year highs, and oil is still up like 10-20% YTD despite the massive pullback recently. Contracting profits is a MUCH higher probability in that environment. SO historically, multiples have NEVER been this high with inflation this high and historically earnings have contracted when you had those 3 things in tandem. That doesn't sound like a "1/3 of the time stocks go down" environment. things are oversold. I expect we could get another bounce - but the ultimate trajectory is lower and will be until the Fed capitulates. We can re-evaluate forward looking projections at that time. -

Where Does the Global Economy Go From Here?

TwoCitiesCapital replied to Viking's topic in General Discussion

Yes. And what's breaks is corporate profits/margins. Not saying we can't see a bounce in equities - particularly of the Fed capitulates. But ultimately I think it's likely that risk assets are lower in a 6-12 months than they are today. -

Wall St. and how to get in.

TwoCitiesCapital replied to whatstheofficerproblem's topic in General Discussion

I never managed to get internships. But I was placed @ Bridgewater Associates via a recruiting firm (I think it was Greenstreet) after I moved to NYC without a job. Only thing I had going for me at the time was the first level of the CFA under my belt. My small school in Mississippi was definitely not target and had no other connections with the firm. So - work with recruiting firms who will be working with hedge funds open to non target candidates and make sure you can best the ivy league guys that will be there too -

Blasphemy-"Trading" a Core Position

TwoCitiesCapital replied to E. Nashton's topic in General Discussion

Pretty much the only trading I do. Some of my longer term hold positions have been dogs (Fairfax, Altius, Fairfax India, etc), but have reasonably average/decent returns on them selling portions when they've popped and repurchasing shares they drop. I typically am comfortable doing this with ~40-50% of the position and will often times ignore my self-imposed position limits for a short-term add to core positions since the intention is to sell on any improvement of oversold conditions. -

I dunno. I quite like it as a public vehicle. Take out shares at a discount. Crush the market with NAV compounding. And issue new shares at NAV when institutional partners want to get in for that performance in size OR when sentiment shifts back to being positive as it was when this IPOd.

-

That was absolutely true of them from 2008 - 2016. But in 2016 they dumped all of the intermediate treasuries and have been in short-term treasuries since. They're actions over the last 6 years seem to demonstrate that they no longer believe deflation was the risk or they'd have been adding 10-year treasuries @ 3.5% in 2018 and again at 3.5% earlier this year. They didn't in either instance.

-

I think the discount to NAV is like getting the fees for free for the next decade plus at this point.

-

+1

-

Where Does the Global Economy Go From Here?

TwoCitiesCapital replied to Viking's topic in General Discussion

Agreed it's better than smaller towns which would have even less opportunity (but also lower cost of living). I live like royalty here. I own a 2,500 sq ft penthouse condo for what I paid in rent for a 700 SQ ft mediocre apartment in NY. But that opportunity wouldn't have been available if not for starting out in NY and getting pedigree at Bridgewater and Pimco prior to moving to StL IMO. Plenty of people working for my same company making a lot less. I was just able to successfully arbitrage the wage/CoL discrepancy. If I had just started here I probably wouldn't have done that and would have started at significantly lower wages. There's cost to be considered outside of the cost of living is the only point in making. -

Where Does the Global Economy Go From Here?

TwoCitiesCapital replied to Viking's topic in General Discussion

That's right. -

Where Does the Global Economy Go From Here?

TwoCitiesCapital replied to Viking's topic in General Discussion

As someone who moved from NYC to StL, I can confirm the cost of living in StL is VERY affordable relative to NYC. I can also confirm that my ex-girlfriend who moved from Maryland to St Louis took a 40% paycut because most jobs in St Louis pay quite a bit less than the jobs in the more costlier districts. Unless if you're able to arbitrage and keep the higher wages (like I did from NYC), the lower cost doesn't really help you. This should be more manageable NOW in a post-covid/remote work environment, but that was NOT the case when I moved in 2017. But, I'll add you're definitely giving stuff up by living in these cheaper cities. The selection of bars/restaurants/nighlife/entertainment matters a little less to me now that I'm 33 vs 23. But as someone who has been single here for a year now, the dating market in StL is a lot more limited than in NYC. As is the job market. So you're definitely giving stuff up to obtain those lower prices. -

This. And they've followed periods of exceptional returns which is what 2011-2021 represented. It wouldn't shock me, given the weight of the indices, of you had another lost decade at the index level even while certain sectors (like energy and materials) go bang busters. After a decade of sucking air, there are parts of the index that would need to 2-3x to have a meaningful impact on the index level returns - particularly if other constituents are actively working the opposite direction. Energy had fallen to like 2-3% of the S&P 500 but is currently having a very outsized contribution to index earnings for instance. That's why it can be up double digits for the year even while S&P is down double digits. I'd expect this might be the case for a few more years to come before the index right sizes itself.

-

Where Does the Global Economy Go From Here?

TwoCitiesCapital replied to Viking's topic in General Discussion

While I don't disagree with your outcome, I can absolutely guarantee the average millennial isn't doing this math so it can't be what's driving their discontent. I think it's less asset prices directly and more simply the quality of life they can afford. After rent, student loans, car payments, and food there isn't much left over for most living in large cities nowadays. Sure, some of this is their own fault. They had cheaper schools to attend, cheaper cars to buy, cheaper neighborhoods to live in, etc. But on the flip side, if every decision in your life is involving sacrifice and you're driving a shitty car in a shitty neighborhood in a shitty town with a shitty degree so you can go to a job that pays shit wages, what quality of life is that? They're not going to feel any wealthier/better by cutting those expenses. Either way they feel poor or are living poorly because those are the options available to most outside of the upper 5-10% of millennial earners. And they're smart enough to see it's happened in an environment of corporate prosperity/tax cuts/bailouts where little of the benefit has trickled down to those who labored to make it possible. That's what's driving most millennials/Gen Zs discontent IMO. -

Yea, this wasn't even margin as it's a retirement account. Had just structured the trade as selling short one ATM put and using proceeds to buy 2 OTM puts. Meant I could short it without upfront cash, wouldn't be on the hook if it kept rising (as it did for the first year I had the trade on), and would still be present for any drop over 10-15%. Trade is off that I was on the hook for falls smaller than 10-15% which were covered by cash held on the account. But in exercising the short and NOT selling the longs, there wasn't enough cash in the account to buy the 100 shares for all the contracts so they sold all of my Alibaba in HK and some of my Exor in Europe to convert to USD to cover the trade. Wouldn't have happened during daytime hours when the long puts could've been sold OR the underlying AAPL shares I was forced into buying could just be sold. All just a f*ck up in the timing of the exercise which I didn't realize could happen when exchanges were closed overnight. Now I'm a little more cautious about the strategy and vol has exploded since I initially bought the position so would be more expensive to put on now (i.e. the loss I'm potentially on the hook for larger before my gains would offset it).

-

I don't disagree. I'm not "selling everything" Own fair chunks of Fairfax and Exor and a bunch of commodity plays. Some cheap European stuff like Porsche and Eurobank and plenty of EM exposure. But am still about 40% short/intermediate bonds (which is crazy for my age) and haven't been adding to 401ks/IRAs etc this year but have been building cash, prioritizing debt reduction, and buying iBonds (ready for another 10k slug in January). Investing through 2008 and 2020 taught me cheap gets cheaper. Just in case that's wrong, I still have appreciable exposure, but nothing works quite as well as cash and shorts. I was previously short AAL and AAPL via options. AAL I did well with and have since closed. Apple wouldve done well, but a few weeks back IB exercised my short puts in the middle of the night. Since the long puts I held against it couldn't be sold, they liquidated a bunch of my overseas holdings AND then owned long puts at the open when it was 2% higher. Didn't realize options could be exercised in the middle of the night, but now I do. Am hesitant to risk reopening the short again since prices are higher for options and I ultimately lost about 2-3k on what was a winning trade due to the inopportune exercise time.

-

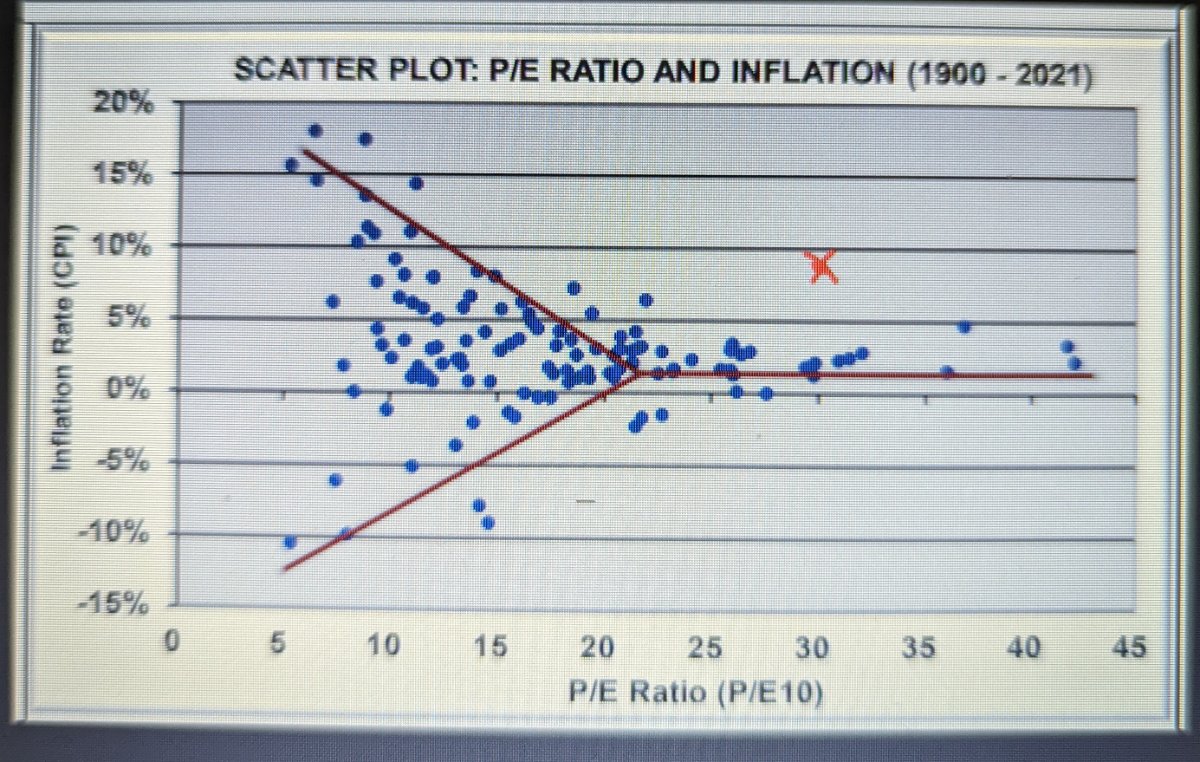

I was a little late to the inflation will persist party. Definitely was on the 'transient' and the deflation is the risk side. Still largely there in the near term, but agree that ita likely to be higher over the next decade than the last. That being said, I've regularly made the argument equities are not an inflation hedge. They do terribly in periods of elevated inflation. The attached shows the evolution of CAPE ratios in the US in varying environments of inflation. 1-3% is the sweet spot. Anything above or below that crushes multiples. The red X is where we're at today with inflation ~8-9% and trailing CAPE @ 29. There needs to be some combination of massive profit growth (to bring multiples down), multiple contraction (to bring multiples down), or a decline in inflation to sub-3% fairly quickly. With corporate profits already juiced from 2020/2021 stimulus, margins near record highs and contracting, and tax rates already lowered in 2017, seems a bit much for me to think it'll be corporate profits growth playing a huge role here. So multiple collapse and/or disinflation are the plays to get is back to more normalized environments.

-

I'll be doing this for the winter. Have two bedrooms of my three bedroom condo rented. Will have a rooftop tent on the car and take it out west for 3-months while the renters clear most of my mortgage.

-

Glen Bradford has a SeekingAlpha piece recently expecting some resolution on the legal cases in the next 3 months. Sounds like a pipe dream after the decade I've been holding the securities, but we shall see.