LearningMachine

-

Posts

1,829 -

Joined

-

Last visited

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by LearningMachine

-

Fast Growers - What Are Your Top 5 Picks Today?

LearningMachine replied to Viking's topic in General Discussion

With MarineMax, I was surprised to see they are somehow getting higher gross margin than other players in the boating industry value chain. However, their cash is getting sucked into working capital ($813M for Inventories in 2023 10K, up from $454M in 2022 10K) and PP&E ($528M in 2023, up from $246M in 2022), leaving no cash available for shareholders. -

At a 51B GBP Market cap yesterday, if you took out $16B ITC stake, you're paying 35B GBP for the company. Management has publicly committed to 40B FCF over next 5 years. So, you get your money back in 4.375 years, that is 22.8% FCF yield. Even if you assume US menthol ban happens, you get your money back in 5 years for a 20% FCF yield, instead of 4.375 years. Few companies like this where management also has some direct control over pricing and margins. I might still change weighting, and get out and in at different times. Also, took a small stake in WBA last week, where management currently doesn't have much control over re-imbursement rates, but revenues keep going up over years, and owner-led management is now building a business that will have some control over loss rates with primary care, adherence & specialty pharmacy that insurers would be willing to pay for.

-

Bought BTI yesterday. My biggest position in any stock. Ever.

-

VSCO: took a big position today. My biggest position in any stock, ever!

-

You can listen to the presentation here:

-

Another talk with Arjun Murti: https://www.youtube.com/watch?v=oqCsZuJfCm0&list=PLtt4Fntz3tuvRPlel5NlFuiPq5A6U2igu&index=109 . Found him to be a more rational thinker than Jeff Currie. Arjun Murti doesn't seem to get carried away by some dogma or agenda to sell a narrative, and instead looks at issues from multiple perspectives, and doesn't take extreme positions.

-

Buyology: Truth and Lies About Why We Buy - Martin Lindstrom

LearningMachine posted a topic in Books

I stumbled into this book when looking deeper into Buffet's quote that "It’s share of mind. It’s not share of market. It’s share of mind that counts." Buffett and Munger would love reading this book. Reminds me of Munger's Psychology of Human Misjudgment. Really loved the concept of "Somatic Markers", that is, bookmarks in brains that brands try to put. -

Timely lessons from Buffett's 1999 Fortune article

LearningMachine replied to LearningMachine's topic in Berkshire Hathaway

Looking backwards, it is easy to say in hindsight which companies compounded equity at 20% a year for decades. Looking forward, much harder to do. Even where the general consensus is that the company will compound equity at 20% a year for decades and is reflected in price, I think neural nets are getting persuaded by the story telling around the company by others more than actually figuring out that certainty is high, and a lot of times, they are going to be disappointed. Any companies that you think will compound equity at 20% a year for decades? -

Timely lessons from Buffett's 1999 Fortune article

LearningMachine replied to LearningMachine's topic in Berkshire Hathaway

@Viking, right on, psychology is the biggest one. Buffett is such a genius and so generous at sharing his learnings. Loved how he explained that after no increase from 1964 to 1981, 10X increase from 1981 to 1998 was not just due to interest rates going down and corporate profits' share of GDP going up, but also due to "market psychology": "Once a bull market gets under way, and once you reach the point where everybody has made money no matter what system he or she followed, a crowd is attracted into the game that is responding not to interest rates and profits but simply to the fact that it seems a mistake to be out of stocks. In effect, these people superimpose an I-can't-miss-the-party factor on top of the fundamental factors that drive the market. Like Pavlov's dog, these "investors" learn that when the bell rings--in this case, the one that opens the New York Stock Exchange at 9:30 a.m.--they get fed. Through this daily reinforcement, they become convinced that there is a God and that He wants them to get rich." Indeed some other things have changed since 1999. "Helpers" have invented new ways of taking a cut of transactions, e.g. SPACs, traffic-routing, options trading, hedge funds, IPOs, acquisition fees, spin-off fees, etc. Wall street has to stay fed. Buffett was not able to imagine corporate profits going above 6% of GDP to 10% of GDP without causing political issues. He was still right on S&P 500 not doing too well from annual growth rate perspective in subsequent 17 years, and political issues cropping up, for example, some folks getting so fed up at not getting their economic share without understanding what's going on that they are getting drawn to conspiracists & demagogues, and ok with putting democracy at risk, and pushing for continued money printing. -

Timely lessons from Buffett's 1999 Fortune article

LearningMachine replied to LearningMachine's topic in Berkshire Hathaway

Buffett said that in May 2019, when S&P 500 was 2932, and S&P 500 P/E was 21.15 (earnings yield of 4.7%), and 10 year treasury yield was 2.39%. In other words, S&P 500 earnings yield was almost double of 10 year treasury yield. Today S&P 500 is 55% higher at 4536, and S&P 500 P/E is 24% higher at 26.26 (earnings yield of 3.8%), and 10 year treasury yield is 3.84%. In other words, S&P 500 yield is lower than 10 year treasury yield. -

Stumbled into re-reading Buffett's 1999 Fortune article. So, full of insights. Interest Rates(https://fred.stlouisfed.org/series/DGS10) #1. From Dec 31, 1964 to Dec 31, 1981, Dow Jones went from 874.12 to 875 because "there was a tremendous increase in the rates on long-term government bonds, which moved from just over 4% at year-end 1964 to more than 15% by late 1981." #2. "If government interest rates, now at a level of about 6%, were to fall to 3%, that factor alone would come close to doubling the value of common stocks." Corollary of #2 is that if government interest rates were to double from 3% to 6%, it would come close to halving the value of common stocks. Any thoughts on when Mr. Market will realize this for S&P 500? Corporate Profits as a percent of GDP(https://fred.stlouisfed.org/graph/?g=1Pik) Maybe Mr. Market will notice when higher interest rates start lowering some debt-laden companies' profits such that overall corporate profits as a percent of GDP go down from current high of around 10%, a percentage that was unthinkable to Buffett in 1999? #3. "[F]rom 1951 on, the percentage settled down pretty much to a 4% to 6.5% range. By 1981, though, the trend was headed toward the bottom of that band, and in 1982 profits tumbled to 3.5%. So at that point investors were looking at two strong negatives: Profits were sub-par and interest rates were sky-high." #4. "[Y]ou have to be wildly optimistic to believe that corporate profits as a percent of GDP can, for any sustained period, hold much above 6%. One thing keeping the percentage down will be competition, which is alive and well. In addition, there's a public-policy point: If corporate investors, in aggregate, are going to eat an ever-growing portion of the American economic pie, some other group will have to settle for a smaller portion. That would justifiably raise political problems--and in my view a major reslicing of the pie just isn't going to happen." Is Mr. Market waiting to notice both strong negatives at the same time, and can't just notice the headline interest rate that has already arrived? Thoughts?

-

Buffett/Berkshire - general news

LearningMachine replied to fareastwarriors's topic in Berkshire Hathaway

Yes, that was part of my take-away as well. You can see the snippet at https://www.cnbc.com/video/2023/05/06/warren-buffett-on-oil-we-like-occidentals-position-in-the-permian-basin.html . Beyond that, Buffett and Munger also said other positive things about oil: Shale is a not a long term source of oil. "If you like quick death in your oil wells, we have them for you." "Just imagine taking 5 mb/d out of production in the world and then we are also taking down our strategic petroleum reserve" He was making this point to highlight possibility of oil price shooting through the roof after 5 mb/d production from shale runs out. Changing the official target for inflation rate from 0% to 2% is sending a message that you're going to depreciate the currency over time. There is lot more oil under Permian if you can figure out how to take it out. Buffett also accepted the risks he is taking with oil price going up or down, but is saying those are acceptable risks. He didn't go into on this talk but Munger has shared recently about the cartel's pricing power being part of their decision making. Also, even if the oil price doesn't shoot through the roof, if the price of the rights to receive cash from oil at today's price is so low that he is going to get his cash back in some years, he is happy with that and doesn't find the need to explain it to everyone. When Buffett is giving a muddled message, i.e. talking about both pros and cons, it usually means he has been thinking about it a lot to decide to buy more if he could. For example, at the 2020 Annual Meeting, when asked about why he was not buying BRK stock when it was trading at about $160 for B-Shares, he gave a similar muddled message that BRK was worth less compared to when he had bought before the pandemic, and ended with something like "we'll see." Right after saying that, he bought a lot of BRK. That said, I still find it surprising BRK is not buying oil sands with much higher reserve lives, no exploration costs, and lower cash operating costs than shale. ' -

Buffett/Berkshire - general news

LearningMachine replied to fareastwarriors's topic in Berkshire Hathaway

I know I myself started the speculation that Footnote 2 in Table 11 might be related to interest rate hedges on HTM, but we don't know for certain. All the footnote says is "Includes amounts in accumulated other comprehensive income related to the hedging of items that are not recognized at fair value on the Consolidated Balance Sheet." What we do know with certainty is what we have them on the record saying on Jan 13, 2023: Because they are talking about treasuries above and HTM doesn't impact capital, I understand they are likely referring to only AFS. BAC provides more details on cash flow hedges on pages 107 and 108, but they don't distinguish between AFS and HTM. https://www.sec.gov/ix?doc=/Archives/edgar/data/70858/000007085823000092/bac-20221231.htm . Overall, though, we can't claim that they bet on interest rates staying low especially given that at least for AFS, they are saying that treasures are "swapped to floating" and that "we don't have any capital impact from rising rates.". If that had the foresight or received guidance to do that for AFS, you could argue they might have at least given thought to doing something like that for HTM. -

Buffett/Berkshire - general news

LearningMachine replied to fareastwarriors's topic in Berkshire Hathaway

I posted the below earlier why he didn't get out of BAC that a lot of folks have been missing and that he didn't want to get into at the meeting, but he alluded to it with his love for Moynihan and by his comments about wanting to own a bank 100%. He owns 12.9% of BAC and that continues to go up, while staying under the limits. ***** If you can get out of other banks, you can then help your own bank (BAC) and Moynihan plan for this at the expense of other banks potentially being counterparty to these hedges: Hedges on held-to-maturity: "hedging of items that are not recognized at fair value on the Consolidated Balance Sheet". See footnote 2 to table 11 on page 52: https://www.sec.gov/ix?doc=/Archives/edgar/data/0000070858/000007085823000092/bac-20221231.htm . Thanks to someone on the group for sharing privately. Hedges on Available for Sale: "we don't have any capital impact from rising rates." See https://app.tikr.com/stock/transcript?cid=19049&tid=2592914&e=1784038192&ts=2718283&ref=u8yosp . So far resulting in about ~$800M quarterly floating interest income. If you have the patience for securites/loans to mature and get lent out at much higher rates, interest income will be much much higher than what it is today. ***** -

Buffett/Berkshire - general news

LearningMachine replied to fareastwarriors's topic in Berkshire Hathaway

The 10k replacement test is interesting. What other companies would you not be willing to switch away from for life even if someone offered you $10K? AMZN comes to mind, but capex there is a different matter. Also, for AAPL, getting out and then getting back in after probability of China taking over Taiwan materializes would cost a lot in taxes, and given the probability is not 100% anyway, he is saying he doesn't want to get out. However, for someone not in AAPL currently, it might be worth to wait to see if that entry point comes especially at current prices. -

Where else do you get such gifts in life. Rights to boundaries marked on earth are actually generating FCF, and you can buy them indirectly for over 10% unleveraged FCF yield, and the price of the product generating FCF is guaranteed (with some lag) by a cartel of governments. People get unnecessarily worried about volatility during that "lag", and end up thinking it is safer to buy boundaries marked on earth that either don't generate any FCF, or buy rights to boundaries that generate much lower FCF yield where the rights are funded with short-term debt exposed to interest rate risks and where the price of the product is not guaranteed by a cartel of governments.

-

Phenomenal businesses that don't require any capital

LearningMachine replied to LearningMachine's topic in General Discussion

I know it is true in case of HP. Maybe also true for some parts of Dell. With Amazon retail, if it doesn't include their delivery infrastructure, warehouses, etc., i.e. basically everything they are spending capital on, could have been true, but that's not the reality today. -

Phenomenal businesses that don't require any capital

LearningMachine replied to LearningMachine's topic in General Discussion

Apple Pay could go one step further. Once it has enough market share, say above 30%, it will have the power to tell merchants that they need to accept Apple Pay directly e.g. through https://www.apple.com/newsroom/2022/02/apple-unveils-contactless-payments-via-tap-to-pay-on-iphone/, and merchants need to pay Apple higher transaction fees than they pay Visa/MC/Amex if they want access to higher-income Apple customers. If merchants don't want it, they can say good bye to some of their 30% of sales. Similar to how AmEx is able to get merchants to pay higher transaction fees with much smaller market share. Apple wouldn't need to exercise the power in such a blunt way, but it can exercise it in more subtle ways, inch towards it slowly, and achieve the same result in the end. -

Is Concentration a better strategy than Buy and Hold?

LearningMachine replied to Viking's topic in General Discussion

Because if you can get out of other banks, and you talk to the CEO of your own bank regularly (Moynihan and Buffett have shared earlier they call each other), you can then help your own bank (BAC) plan for this at the expense of other banks potentially being counterparty to these hedges: Hedges on held-to-maturity: "hedging of items that are not recognized at fair value on the Consolidated Balance Sheet". See footnote 2 to table 11 on page 52: https://www.sec.gov/ix?doc=/Archives/edgar/data/0000070858/000007085823000092/bac-20221231.htm . Thanks to someone on the group for sharing privately. Hedges on Available for Sale: "we don't have any capital impact from rising rates." See https://app.tikr.com/stock/transcript?cid=19049&tid=2592914&e=1784038192&ts=2718283&ref=u8yosp . So far resulting in about ~$800M quarterly floating interest income. If you have the patience for securites/loans to mature and get lent out at much higher rates, interest income will be much much higher than what it is today. -

High Quality Multi-family REITs - EQR, CPT, ESS, AVB

LearningMachine replied to thepupil's topic in General Discussion

@thepupil, thanks for contributing to joint learning culture through your insightful posts. Is development pipeline your main reasoning for picking CPT over EQR, ESS & AVB, even though CPT seems to have been diluting the most out of the big MF REITs? Is there more to your reasoning? When interest rates were low, it made sense to be a developer that develops for $250K/unit, get $13,200 (half of $2000*12) net-operating-income and sell at 3.3% cap rate (given low interest rates) for $400K/unit. When interest rates/inflation/cap rate are high, say 7%, $13,200 of net-operating income translates to $188K/unit. So, it doesn't make sense to be a developer. It would be better to be able to buy apartments at below replacement cost of say $150K/unit after there is some more fear on the streets when articles start popping up of smaller operators with higher leverage and lower maturities not being able to refinance as they can't meet debt service ratios. -

High Quality Multi-family REITs - EQR, CPT, ESS, AVB

LearningMachine replied to thepupil's topic in General Discussion

Thanks @thepupil, for net cash from operating activities, I was going by what they have in the 10K on page F-8 at https://www.sec.gov/ix?doc=/Archives/edgar/data/906345/000090634523000008/cpt-20221231.htm#ic3d0808623a844d5be74a512380237cd_121 . Indeed, what's helping CPT survive here is low leverage and well staggered maturities to be able to withstand 10% interest rate scenario.

-

High Quality Multi-family REITs - EQR, CPT, ESS, AVB

LearningMachine replied to thepupil's topic in General Discussion

I wasn't saying $100B + $88B = $188B in net income. I was saying that as interest income. Sure, they might have to pay a little more for some portion of their deposits if they really want to keep them. If the inflation keeps going, deposits will start going up again too at some point. Regarding losses, really depends on how fast the interest rates go up. Basically, the question is do the banks take so much money from people and companies that they have nothing left and have to go under, or can they just keep on increasing how much they are charging just upto the point that there aren't widespread losses. -

High Quality Multi-family REITs - EQR, CPT, ESS, AVB

LearningMachine replied to thepupil's topic in General Discussion

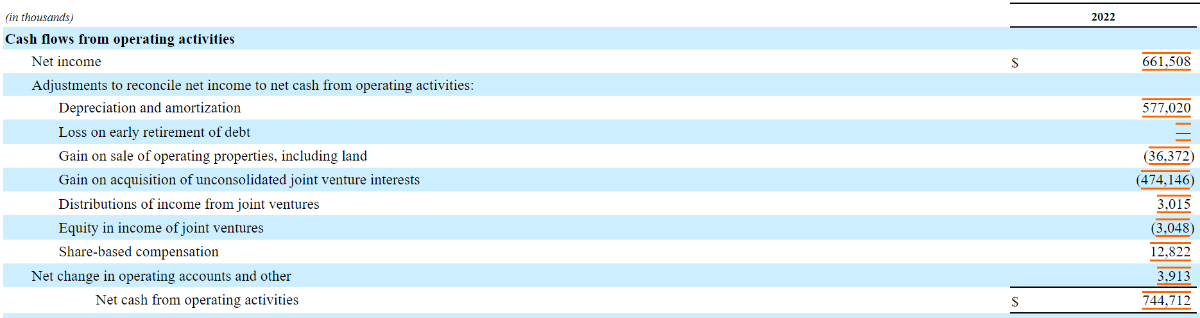

Thanks @thepupil, I agree it depends on how fast interest rate is going up for CPT, and for that, the most important figure is CPT's weighted average maturity. I'm curious how you built your WA Rate column? Is it based on their maturity schedule on page F-20 in the 10K at https://www.sec.gov/ix?doc=/Archives/edgar/data/906345/000090634523000008/cpt-20221231.htm ? CPT's 10K says weighted average maturity is 6.4 years. Is CPT the REIT with the highest weighted average maturity, or you have found another with a higher weighted average maturity? Also, not sure how your starting point is 852M for NOI - Interest for 2023. Regarding net cash from operating activities, I see it was $744.7M in 2022. For 2023, assuming we believe their midpoint FFO per share, at 106,700,488 shares, FFO would be $747M for all shares in 2023. -

High Quality Multi-family REITs - EQR, CPT, ESS, AVB

LearningMachine replied to thepupil's topic in General Discussion

I'm not saying rents won't rise at 10% per year, taking more than 7 years to double. If interest rates go to 10% in a few years, all the additional rent increase is eaten up by additional interest and some more, and that additional interest is going into BAC's pocket. As long as no-one forces them to liquidate that $880B, they can lend the other $1+ Trillion at 10% interest rate, which is $100B in interest income on $1T alone, and wait to rent that $880B at 10% as it matures. -

High Quality Multi-family REITs - EQR, CPT, ESS, AVB

LearningMachine replied to thepupil's topic in General Discussion

Indeed, you can't look at what other people are saying. You've to do your own thinking and have confidence that anytime in history, if a bank had a bank run, they wouldn't have been able to give 100% of depositors their money. It is analogous to when Buffett was asked what would happen to the country if oil prices went down, and he answered it beautifully that short-term people will try to mark-to-market the reduced FCF on oil companies, resulting in a lot of short-term thinking that low oil prices are bad for the country, even though longer-term we all know low oil prices will be better, but the effect will be positive slowly. Similarly with banks with sticky deposits, you know long term, if they can rent out those deposits at 7-10% instead of the current rents of 2-3%, they will be better off. Now, if you start walking into other kinds of thought patterns that what if they have to liquidate now, you can talk yourselves out of it. While the thought pattern of liquidating your assets might apply to some specific banks, it doesn't apply to other specific banks. You've to be really good at assigning probability ranges to thought pathways, and decide which pathways to thought patterns to cut off for specific bank situations.