Sweet

-

Posts

3,133 -

Joined

-

Last visited

-

Days Won

2

Content Type

Profiles

Forums

Events

Everything posted by Sweet

-

-

Depends. Yes those are winners but they are a huge portion of the index. Apple is sitting at 30 PE on flat revenue. Nvidia is 64 PE with huge growth expectations. There is too much of the index hinging on those 7 companies which in my opinion are quite richly valued already - it’s a double whammy. I’d prefer to hold the SP-500 less those companies.

-

Yeh 20% is too big still. Always a problem when they cut the winners, that’s the inherent advantage of indexing with the SP-500, it lets the winners run. A quality filter for profitability is important too - very important.

-

How do they manage / weight VIOO? My concerns with the ‘small cap’ ETFs is they cut the winners. For example, let’s say the next NVIDIA is hidden in there, does it get cut above a certain market cap? That would seem like a dumb thing to do. I agree that I like looking here than the SP-500 because of the Mag 7 dominance, but concerned about how the portfolio is managed. Cutting companies because they are no longer ‘small cap’ would be counter productive.

-

Came across this the other day, a paper from Oxford Uni called ‘Dissolving the Fermi Paradox’. Forgot to post it. Of course I’ve no idea how likely this is as the next person but seems well thought out: https://arxiv.org/abs/1806.02404#:~:text=The Fermi paradox is the,universe we in fact observe. Would be disappointing if it turned out to be the correct solution.

-

You can’t possibly look at the performance of the FTSE 100 since 08 and say it was fine until Brexit. It was terrible before and it’s terrible after. European indexes have been terrible too from that time. Overlay just about any European index on the SPY and it’s pretty much the same story.

-

Some truth to that though, they are perma low multiples. Economy has been stuck since 08 really, as has much of Europe.

-

That was my thought too because he had a large new holding in it: https://whalewisdom.com/filer/saber-capital-managment-llc Thermal coal doesn’t much interest me, and as I’ve learned from investing in energy, expectations that management will pay out nearly always disappoint.

-

I like John Huber’s writing, he makes the complex simple. I don’t have a subscription though. Anyone know what company he is referring to? https://basehitinvesting.substack.com/p/a-royalty-on-the-growth-of-others

-

Thanks GFP. It’s too hard for me so decided to just move on.

-

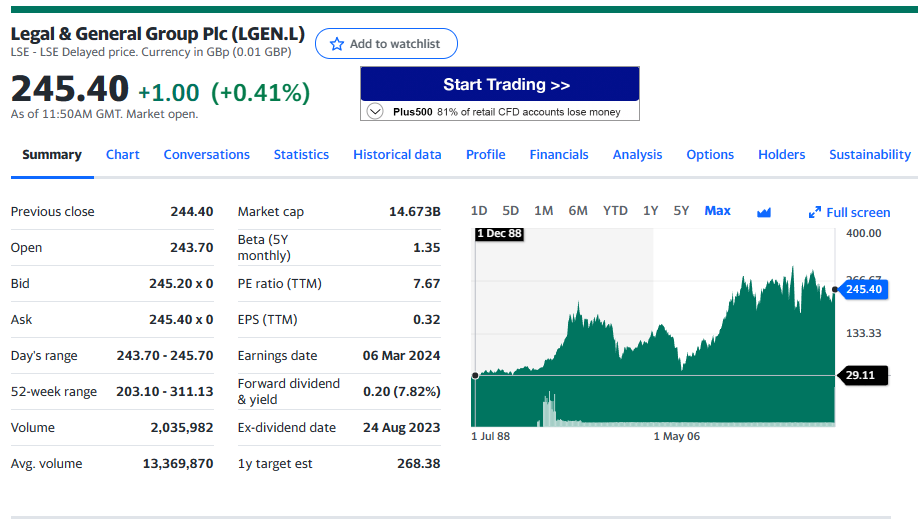

Has anyone looked at the UK company Legal and General? It is an insurance company (among other things) and has a fat dividend and a relatively low PE. It has negative revenue in the past few years, something I cannot get my head around. The details of this company are over my head unfortunately.

-

Extremely volatile initially and extremely good for speculators initially, but it would probably moderate and find a range like anything else.

-

Exactly. You pick your spots. There were large banks trading as low as a PE of 6 just a few months ago.

-

He may be calculating it differently, I checked other sources and the difference appears to be consistent

-

Yes you are saying that multiple expansion is to be expected given the tailwind and also saying that changes in interest rates, taxes etc can move the needle both up and down in terms of multiples. We are in a different era from the 20s-50s etc. Just so many different moving parts these days and much more money chasing the stocks through passive indexing and the like. My post is only to point out that things aren’t that out of whack to historical standards.

-

In terms of PE we aren’t too far away from the from the ~35 year average of 19. Notable that the lowest PE since 1989 has been 13.

-

What Is the Best Investment That You've Ever Made?

Sweet replied to Blake Hampton's topic in General Discussion

The cost of membership of this board. I wonder how many baggers of my membership I’ve made in the short period of time I’ve been on the board. -

Happy new year and all the best for the new year.

-

Aswath Damodaran's investment picks and returns?

Sweet replied to schin's topic in General Discussion

Lol, yes. He is excellent though, and his classes are much more than valuations, you learn about finance, modelling, capital and all sorts of other things. I regularly check his blog - especially if he covers companies I own or thinking about owning. -

Aswath Damodaran's investment picks and returns?

Sweet replied to schin's topic in General Discussion

This. If you have to get out you calculator and run all sorts of models then it’s probably a pass. -

Public Company Share Repurchase-Cannibals

Sweet replied to nickenumbers's topic in General Discussion

What’s the ticker? Are you talking about PKW? -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Sweet replied to twacowfca's topic in General Discussion

What or who is causing this pump? -

Much sequencing, outside of places like hospitals, is performed by sequencing providers. Most of these providers offer multiple types of sequencing approaches to their customers. Typically Illumina and a long-read approach which has usually been Pacbio but some have all three. The Pacbio instrument are hugely expensive but if you are a large dedicated sequencing provider you tend to just swallow the costs if that’s what your clients want. The Oxford Nanopore basic sequencer can be bought for $1k making it by far the cheapest sequencer around. The technology is very different too. Short-reads aren’t bad they just aren’t as good as long-reads all else being equal. It’s simply more information. Illumina still have a cost advantage over both Pacbio and Oxford Nanopore but it’s narrowing fast. The long-read offering from Illumina makes sense they had to develop that. How good it is nobody knows because it’s really only just on the market. I’m not saying Illumina or Pacbio are bad bets. I suppose I’m saying why own Illumina and Pacbio but not Oxford Nanopore which has by far the most interesting technology. I am somewhat skeptical about the economics of Pacbio, uncertain about Illumina’s future and unsure that Oxford Nanopore are able to execute. There is also the possibility that another company comes out with a new technology and just cleans up. I guess the more I know the more I tend to think let’s just buy a biotech etf

-

Yes but what if the tech just moves on, and Illumina goes the way of Sanger?

-

A few years ago maybe. The latest chemistry improvement from Oxford Nanopore has brought the accuracy from 95% to 99%. It’s not as accurate as Illumina or Pacbio yet but it is getting there and will likely match them in the next few years. All else being equal the longer the read the better, there is no benefit to short reads and that’s a problem for Illumina - they are trying to bring out long reads.