Thrifty3000

-

Posts

646 -

Joined

-

Last visited

-

Days Won

5

Content Type

Profiles

Forums

Events

Everything posted by Thrifty3000

-

YES. I was just about to say the same thing about return of capital. With so much cash flooding in the door it will be very interesting to watch where they park it. If the stock price continues hovering around book value then if they aren't using excess cash to buy back shares it means they must have REALLY juicy alternatives. I assume the only reason they would park excess cash into ultra-low yielding bonds rather than return capital would be if those bonds allowed them to underwrite additional insurance at extremely favorable rates.

-

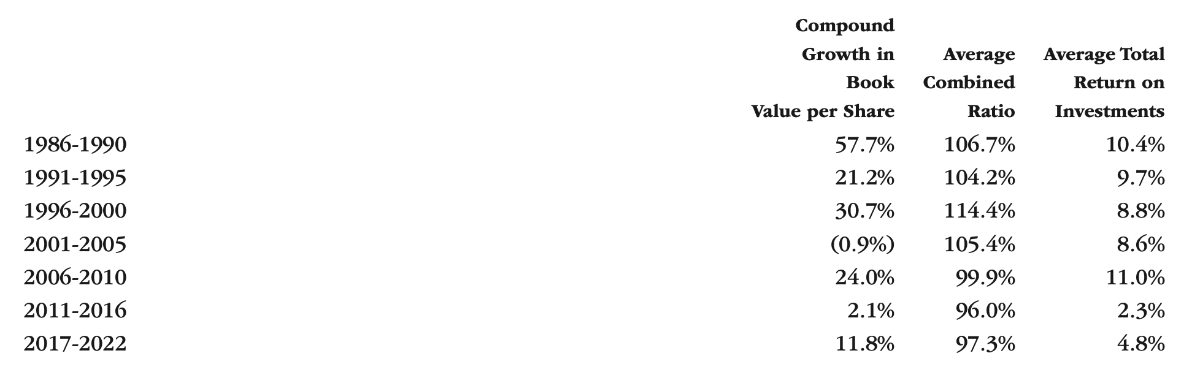

From 2011-2016 5-year treasuries yielded around 1.5%, and the portfolio only yielded 2.3% because of the equity hedges. From 2017-2022 5-year treasuries were extremely volatile, but appear to have averaged around a 1.75% yield. However, the portfolio returned 4.8% thanks to the equities, etc. I think the last decade shows us that a 4.5%+ portfolio return is reasonably achievable even in an environment with sub 2% treasury yields. Therefore, $100+ per share portfolio earnings (after taxes/expenses) seems plenty reasonable 4 years from now and beyond.

-

Here is a historical chart showing average portfolio returns:

-

If you want a doomsday scenario where cash and bonds collectively earn less than 1%, and the rest of the portfolio earns less than 8%, you're looking at EPS in the neighborhood of $90 pre-tax. After taxes and overhead/expenses would put it around $40 EPS. Add or subtract what you want for insurance earnings. I'd expect at least $25 to $50 EPS in that type of rate environment.

-

The investment portfolio will probably be closing in on $70 bil in 3 years. Bonds and cash will probably make up 60% of the portfolio. A blended 4.5% return, or $3.2 bil, should net around $100 per share. If the bonds are only earning 2% then the rest of the portfolio has to earn 8% to maintain the $100 per share bogey. I don’t think that’s too big of a hurdle for the investment team. I also think if interest rates are 2% that it’s not far-fetched to assume sub-100 combined ratios, which should help FFH stay in the neighborhood of $150 EPS through the cycle.

-

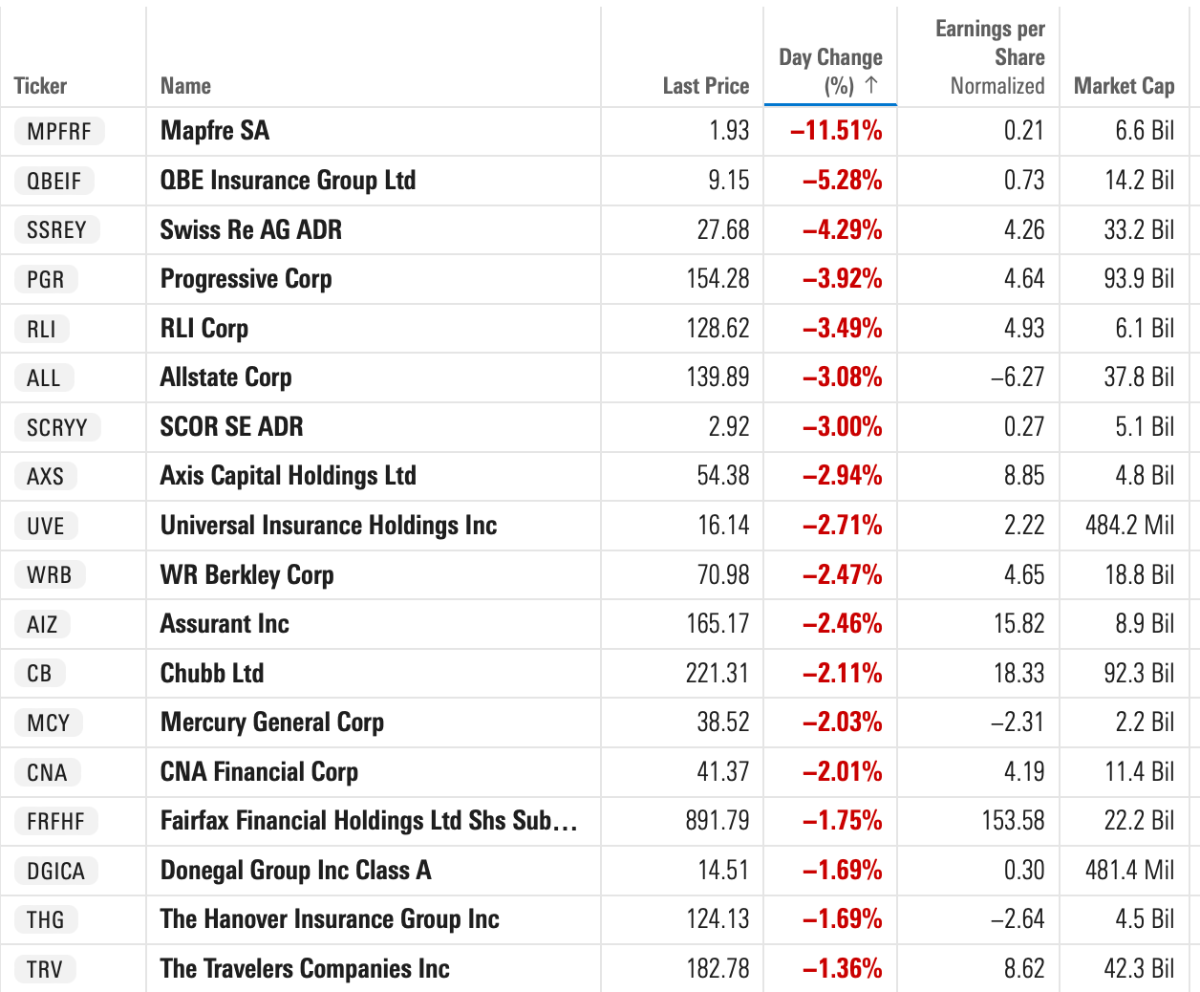

Industrywide beatdown:

-

If we assume BV grows by $150 per share annually for the next 3 years then depending on which year P/BV hits 1.2x your compound annual return from today's price would be as follows: If P/BV is 1.2x on Dec 31 2024: approx 40% CAGR! If P/BV is 1.2x on Dec 31 2025: approx 26% CAGR If P/BV is 1.2x on Dec 31 2026: approx 21% CAGR Of course, if P/BV is still a sad and lowly 1x BV by Dec 31 2026: approx 14% CAGR And, if P/BV reverts to the 2020 level you're looking at a Dec 31 2026 CAGR of approx 2% (buying opportunity!)

-

Good news. FFH's Price to Book Value ratio has solidly expanded this year. Here are the numbers (using GAAP for 2020 and 2021). Dec 31, 2020= .71 Dec 31, 2021= .78 Dec 31, 2022= .78 Dec 13, 2023 (Estimate)= 1.0 I have a hunch the strong upward trend isn't going to stop at 1. I'll be surprised if we don't hit 1.2 in the next 2 years. A new baseline of $150+ EPS is especially exciting when you apply a 1.2x multiple and compare the result to today's stock price. #stillCheapAF

-

What Is the Best Investment That You've Ever Made?

Thrifty3000 replied to Blake Hampton's topic in General Discussion

Yeah, last I checked Dogecoin still hasn't paid a dividend. And, neither have Beanie Babies or tulips for that matter. Not my kind of asset. -

What Is the Best Investment That You've Ever Made?

Thrifty3000 replied to Blake Hampton's topic in General Discussion

I invested a bit over $200,000 in my side hustle starting in 2012 (which was nearly a third of my net worth at the time). I was able to unload it for a cool 8 figures in 2018. (Thank you everything bubble!) Like Viking mentioned above, I would have NEVER been able to invest that much had my wife and I not been so dang frugal in our 20’s (always trying to put one of our salaries in savings). Also like Viking, my most impactful public equity W was loading up on Fairfax post-2020. It became my first ever seven figure gain on a public equity, which has been fun. And, despite having followed Fairfax since 2010, if not for this board I’m sure I wouldn’t have had the conviction to bet so big. -

Yes. I was at my son's basketball game and while he was on the bench I did a super-back-of-the-envelope estimate just to see how much of a per share impact we were actually talking about. Basically just started out with the highest level round numbers: - I gave FFH the benefit of the doubt and assumed a nice round $200 mil earnings potential - Subtracted opportunity cost of, say, $80 mil for what the $2 bil could alternatively earn in treasuries - Took the resulting $120 mil and divided by 23 million shares - Which came out to a little north of $5 per share. So, that's usually enough info for me after a first pass impact assessment, where I just want to quickly understand if we're talking about pennies per share, dollars per share, or tens of dollars per share. You can then go in and add whatever other variables to the mix you want, which would likely pull the estimate down a buck or two, but it's not a level of detail I'm going to worry about.

-

Back of the envelope, I estimate this will increase the earning power of the bond portfolio by around $5 per share. (I’m assuming less than 2% loss provision, but pulled that out of the air.)

-

Let me know when they make a billion dollar decision. Anything under $100 mil is noise.

-

Yes, 15% is possible long term. The magic is in the $2,700 of portfolio investments per share vs $900 per share of book value. You only need to earn 5% to 7% on that investment portfolio to have the kind of ROE you're talking about. Could Warren Buffett earn 5% to 7% on a $60 billion portfolio. 100% guaranteed he could. Can Hamblin Watsa earn 5% to 7% on a $60 billion portfolio? I have a hunch they can going forward.

-

If FFH earns around $3.5 billion in 2024 as expected, and if the market cap remains around BV, which is approx. $22 billion now, it seems buying back shares is an excellent way to allocate capital. Given FFH knows full well that buying back shares at 1x BV practically guarantees better than 10% EPS growth going forward, if we see FFH deploying cash in ways other than buybacks we should get pretty excited by the relative prospects. 2 favorable scenarios: 1) FFH gets to buy back shares at or below BV, which practically guarantees double digit EPS growth. 2) Mr. Market bids FFH shares up above 1.2x BV and we all get to perceive the joyous wealth-effect of multiple expansion. Though we’ll have to face the anxiety of speculating whether FFH’s investment prospects will still be as good when they no longer have the no-brainer buyback option in their toolkit.

-

+1

-

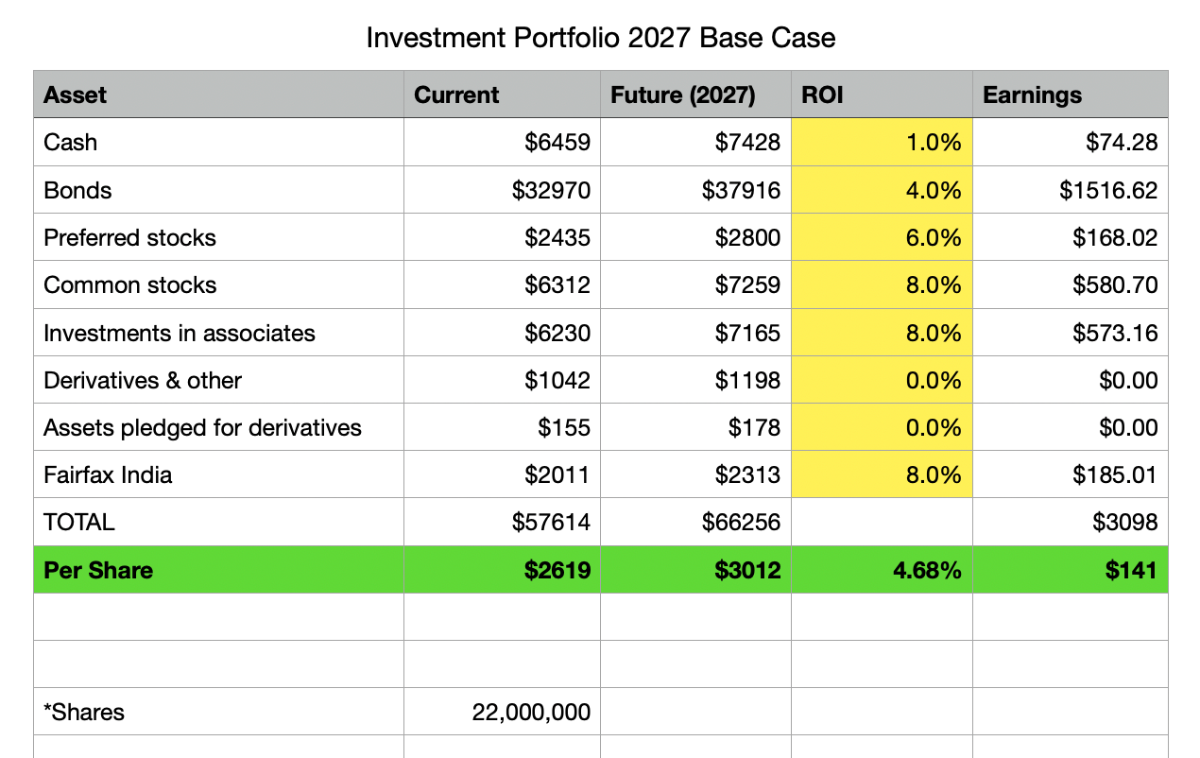

^ here is a post from August where I provided a table with about as conservative of a forecast possible of the earning power of each category in the investment portfolio in 2027. You can see it’s by no means a stretch for the investment portfolio alone to earn $140+ per share. You can then add to that whatever number you want for underwriting earnings (say $0 to $50 per share) and for any opportunistic surprises (like pet insurance subsidiary sales), etc. The most important number is the earning power of the bonds. My table shows a 4% interest rate. I follow the same logic as Leon Cooperman on this front. In a world with at least 2% inflation and 1.5% GDP growth it’s hard to envision a long term scenario where bonds don’t yield at least 4%. Long story short, people worrying about FFH earnings falling off a cliff in 4 years are likely overweighting the significance of underwriting earnings and underweighting the power of a huge investment portfolio that can produce solid earnings per share without any heroics from the FFH investment team.

-

Maybe they expect 3 or 4 good peak-cycle years to be offset by 3 or 4 trough years. Not an unheard of scenario for FFH historically. (However, I’m in the camp that believes this unusually strong peak-cycle experience for FFH will set it up to take advantage of the trough from a position of strength. But, I have a hunch analysts have little incentive to join our camp.)

-

Maybe a 1x BV valuation is just another way of saying they don’t have enough reason to expect FFH’s long term ROE to exceed whatever discount rate they’re modeling.

-

I bought a pretty good chunk of McKesson for $125 per share towards the end of 2018. It was way out of favor because of opioid liability fears. The price declined from my initial purchase before Mr. Market started waking up to how much cash that company generates and how quickly it could overcome even a worst case scenario. Took about 3 years for the price to double, and only another 2 years after that to double again - once the earnings track record was clearly reestablished post-opioid settlements. Mr. Market has fallen in love with MCK again, so it's selling for an aggressive multiple now, despite not really having the most exciting growth prospects. So, after enjoying my ownership of MCK for a looong 5 years, I've lately been selling in favor of cash. I think we're only around mid-way through the FFH turnaround story. I think we're about where McKesson was a couple years ago. I think FFH will have a few more strong legs up as either Mr. Market sees 3 strong years of earnings in a row, or more likely, as Mr. Market begins to more confidently forecast the 3 strong years of earnings while also waking up to FFH's longer term earning power. Each large upward leg in share price will only catch more attention. I don't think we'll have to wait 3 years for Mr. Market to fully value, and very possibly, start to overvalue FFH - especially if earnings forecasts for years 4 and beyond solidly exceed $150 per share. A $2,000 per share price tag for FFH a couple years from now is certainly not out of the question.

-

^ what he said

-

Just hit $9 hundo intraday. Mr Market is waking up.

-

Only 2 questions on the call?!

-

$25 per share of carrying value over fair value is also a nice bonus. No excuse for FFH to trade for less than $900 USD per share. And even that is absurdly cheap - as evidenced by FFH ramping up the buybacks again in Q3. PS. I love FFH and I'm not afraid to say it.

-

Yeah, was surprised to see a pullback on premium growth. Maybe they're just being conservative in the third quarter and waiting to back up the truck on higher volume in Q4 and Jan1. Did you notice this footnote? (2) Excluding Ki Insurance, gross premiums written decreased by 4.0% and 4.6% in the third quarter and first nine months of 2023 and net premiums written decreased by 9.5% and 1.2% in the third quarter and first nine months of 2023. Excluding Ki Insurance, the combined ratios were 92.4% and 93.1% in the third quarter and first nine months of 2023 and 114.8% and 101.2% in the third quarter and first nine months of 2022.