Thrifty3000

-

Posts

683 -

Joined

-

Last visited

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by Thrifty3000

-

Well, any veteran investor worth his salt would say if you have to ask then it's not okay. But, I'm pretty sure I'm not worth my salt, so I'm going to say you SHOULD invest - however, that recommendation comes with a caveat... I recommend taking a "starter position" of, say, 1% of your portfolio, or whatever amount gives you enough skin in the game to incentivize you to do the requisite research to ascertain not only a conviction buy price, but also a conviction exit price. At the very least I recommend reading Viking's thesis and maybe the last decade or so of Prem's annual letters. After you do that, then if you still CAN’T succinctly defend your conviction buy and sell prices I recommend exiting your starter position. However, if you CAN defend them then I say set your trade triggers accordingly and welcome to the FFH party. Hope this helps.

-

I wouldn’t be surprised if FFH breaks into the top 25 within 6 months, and the top 20 within 18 months.

-

In simplest “best practice” terms: 1) estimate intrinsic value 2) create a trade trigger to buy at a 40% discount to your estimate 3) create a trade trigger to sell at a 40% premium to your estimate 4) regularly update your intrinsic value estimate and your trade triggers (quarterly) 5) sit on your hands ^ this takes emotion and impulse transactions out of the equation

-

Great brands at a fair price. Whether mattresses, hockey sticks, banks, airports or container ships, I say the more the merrier.

-

Here are the corporate related elements of her plan…

-

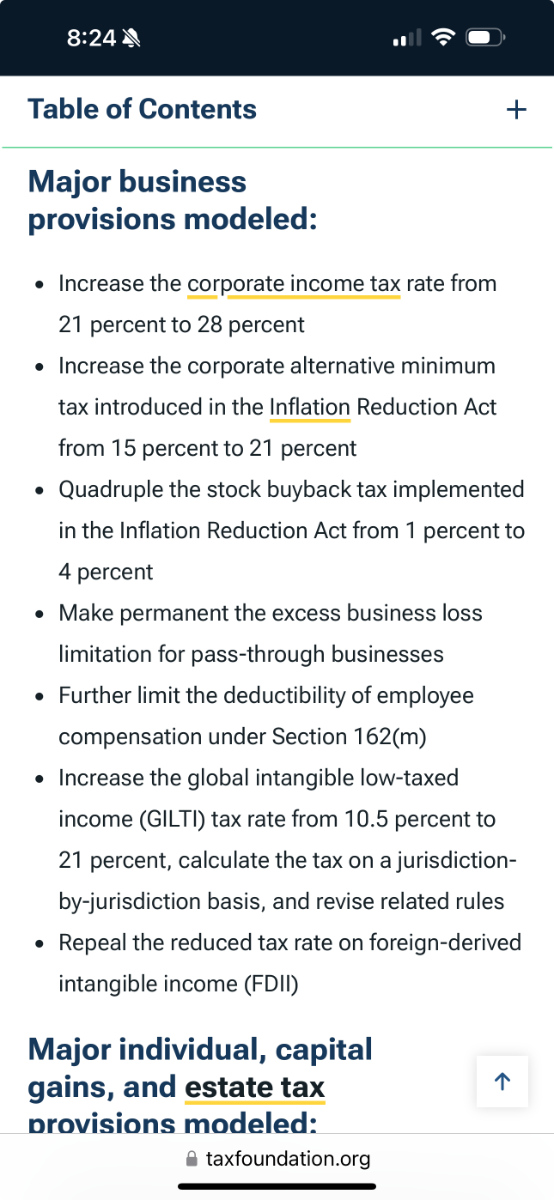

Ok, but Kamala is calling for 28% corporate tax in her budget plan. So I’m curious what the risk adjustment to fair value should be.

-

What would be the impact to FFH earnings if US corporate taxes increase to 28% from 21% (when the Trump tax cuts expire)? Do we just reduce the US-based earnings, or is there some kind of tax treaty with Canada that changes the math?

-

I think Sokol would be way more valuable/effective as a board member (holding operating managers accountable for high performance). As an operator he might be too much of a culture shock. However, I also think Sokol is probably too expensive of a board member. He would probably demand millions in board compensation, which would cause all kinds of headaches with future board comp and retention.

-

Just wait until the world recognizes how much better Prem has done with succession planning than Buffett.

-

Ahem…

-

^ Boooo. Too conservative!!

-

Also, given the average P&C company trades at 12 times earnings, and Prem’s latest baseline medium-term earnings expectation of $125 per share, then I’m thinking we still have room to run.

-

Up 35% YTD. While the S&P 500 trails solidly behind at 18%.

-

In addition to a cash buffer I like to keep an untapped HELOC handy. If I need cash at a time when every security in my portfolio is substantially undervalued (like 2020) then I’ll just draw on the HELOC - for a few years if necessary.

-

Starter position in Sky Harbour common below $10, and warrants below $1.40. Bought a little more FFH in Feb and again a couple weeks ago during the yen turmoil. Also, during the VIX spike I sold McKesson calls for around $25 and bought them back a week later for about $.60. (Sell high, buy low)

-

-

I go back and forth on whether to use an average of the common and diluted count since not all dilution will actually occur. But, we know that more than 0% dilution will definitely happen, so I don't let myself use the common.

-

I think the main difference between your near term estimates and mine is that I use the fully diluted share count (since it hasn't been declining as quickly as the common share count). If I used the common share count I think our EPS estimates would be within a couple dollars of each other's for at least this year and next year.

-

IIFL getting caught up in another scandal. This time it involves the chairperson of SEBI. Too much corruption… https://hindenburgresearch.com/sebi-chairperson/

-

When Charlie Munger and I buy stocks — which we think of as small portions of businesses — our analysis is very similar to that which we use in buying entire businesses. We first have to decide whether we can sensibly estimate an earnings range for five years out or more. If the answer is yes, we will buy the stock (or business) if it sells at a reasonable price in relation to the bottom boundary of our estimate. What will the next 10 years of FFH earnings look like? Will it be the dreaded earnings cliff, where interest rates round trip to the zero bound, FFH hedges equities, combined ratios edge back towards 100, and maybe the Canadian Government raises corporate taxes or a string of mega-cats catch FFH completely by surprise. That nightmare scenario may look something like this... Or, if you're the perpetual optimist, then maybe you assume that after a decade of carefully and deliberately structuring its management team, insurance business and investment team for a future sans Prem, that the "new Fairfax" is finally geared to achieve its dual mandate of a 7% portfolio return and a 95 combined ratio. Maybe your crystal ball foretells this happy future... Or, if we can assume with 80% confidence that real life will land somewhere between our best and worse cases, that some results will turn out better than feared, and others will turn out worse than hoped, then maybe we can assume a result that falls somewhere reasonably between the two - and invest with conviction when Fairfax - as it is today - is fairly priced for even our worst case scenario. The base case... ^ I think a job well done for a value investor is to follow that approach diligently and consistently. Much easier said than done! PS. My forecasts above are necessarily rough and change constantly as new insights arise.

-

If you want to get rich, concentrate. If you want to stay rich, diversify. If your goal is to own an asset that will pay dividends to your great great grandchildren, while also paying dividends to future generations of Watsas then your interests are probably well aligned with FFH. If you want maximum near term financial engineering to boost share prices so you can flip your shares to the next impatient “investor” then there’s probably more disappointment to come. IMHO, FFH is best viewed as the Watsa and friends family office. A family office wants the best long term - multi-generational - risk adjusted returns.

-

IDBI Bank IDBI Market Cap: $12 billion USD (FFH Market Cap: $25 billion USD) IDBI Net Earnings: $670 million USD Market Cap at time the sale was announced in 2022: Approx $8 billion Amount being sold: 61% (Currently worth $7.3 billion) Fairfax India Total Assets: $3.6 billion IDBI 3 Year Net Earnings Trend: ^ feels like this is way bigger than Fairfax India and I have a hunch Prem is going to want all he can eat of this one. This is an example of a deal with a high probability of being a better use of funds than share buybacks. If bank performance is largely a reflection of the region's economic performance, then I'd love to own a good bank in the world's fastest growing economy.

-

What was the gut instinct on the pet insurance business back when FFH entered that one? Personally, as far as business concepts go, I assumed pet insurance ranked right up there with tanning beds for babies. Turns out the FFH investment team saw something I didn’t.

-

^ feels like an important thing to nail down

-

+1 Where might that $1b+ come from if they're using free cash to buy back stock.