rogermunibond

-

Posts

2,054 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by rogermunibond

-

Are you guys operating from the same talking points? Or are your Russian bots?

-

If you're an oil and gas EP CEO, how are you feeling about the price of oil now? OPEC+ lifting production, possible lifting of Russian oil sanctions, with the breakeven at $50/barrel, they aren't adding rigs anytime soon.

-

Chancellor Merz seems to disagree with @luke He plans to push it through ASAP https://on.ft.com/43mdLAi

-

German is shifting bigly to spending. $528B to infrastructure spending $232B to defense Lifting debt brake and running larger >2% fiscal deficits

-

Strangely enough I've never seen such in the county code. Occupancy is reflected in the Fire Code but that doesn't seem really specific to residential SFHs.

-

I'm in a state where Section 8 income cannot be rejected when searching for tenants. It's an onerous slog. There are limits on the number of unrelated persons who can live in a home but not on the number of directly related individuals iirc.

-

Macro thread - Why is the market up/down?

rogermunibond replied to Luke's topic in General Discussion

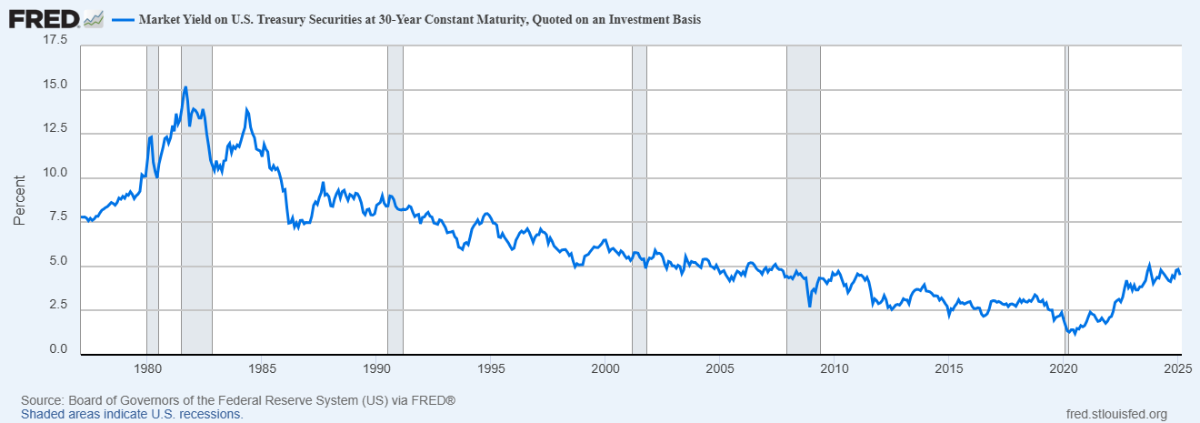

the 30 year yield is not going sub 3% without a huge economic shock

-

Reviving this thread because in some respects MMT has proven itself over the last 3 years. Inflation was largely not monetary in the current episode and has come down as real resource scarcity was allayed through production/supply chain disruptions. Coordinate monetary policy with the Fed has brought down inflation, despite large fiscal deficits. Proponents of the view that US federal debt crisis is afoot like Ray Dalio haven't explained why MMT doesn't currently continue to apply. The current administration is concerned about reversing tradeable vs nontradeable economic sector growth and reversing public sector versus private sector economic growth but have they put their money where it matters most? The House budget framework is still proposing Federal deficits of $2T per year (about 6% of GDP) going out the next ten years, which is $1T more per year than advisable. And most of the Federal spending is coming from tax cuts. We've yet to see what the administration is going to do to 1) build more infrastructure; 2) build substantially more housing of all types in all regions; 3) keep inflation and prices in check other than oil.

-

Still waiting for someone to quote Burke

-

Macro thread - Why is the market up/down?

rogermunibond replied to Luke's topic in General Discussion

https://www.reuters.com/business/energy/opec-proceed-with-planned-april-oil-output-hike-sources-say-2025-03-03/ OPEC+ approved an April production hike - gradual reversal of the 2.2 Mbd production curtailment. There's really no need for US domestic production to increase. -

Pretty interesting China macro observations from Li Daokui. The tariff stuff is at the end and not nearly as interesting as the local bond debt burden issues that Beijing is tackling. Going to have to pay attention to what comes from the NPC. https://www.bloomberg.com/news/videos/2025-03-03/china-fully-prepared-for-us-tariffs-ex-pboc-adviser-video

-

Alcohol and Coffee are fine and which one is better?

rogermunibond replied to Haryana's topic in General Discussion

Almost every metaanalysis of coffee has shown little to no risk for overall human health iirc. All the outlier studies that linked to cardiac events or some other issue were not replicated. Can't same the same for alcohol which does have real downsides - addiction/substance use disorder and cancer. BTW, THC use is going to be more like alcohol - there's just a small percentage of people who have risk for bad effects on THC use. Similar to the percentage at risk for SUD. -

Macro thread - Why is the market up/down?

rogermunibond replied to Luke's topic in General Discussion

Sizeable shifts in Consumer spend and net exports There are only six subcomponents. Maybe the size of net exports decline is overestimated. -

Macro thread - Why is the market up/down?

rogermunibond replied to Luke's topic in General Discussion

Atlanta GDPNow has Q1 growth at -1.5% -

Macro thread - Why is the market up/down?

rogermunibond replied to Luke's topic in General Discussion

Interview with Neil Dutta on macro. Sees Fed cutting in June. Housing slowing, payroll slowing, state/local govt spending down. -

Anyone have thoughts on why HII is down? IIRC they are mostly a naval shipbuilder and with the lack of active USN surface vessels shouldn't HII be getting a bid?

-

MGP's FY25 guide of $520-540M sales implies some big drops in Distilling and Branded segments. If Beam Suntory, BF, Sazerac, and HH drop prices to fight for share, could be hard on the so-so Lux Row brands.

-

MGPI bought back shares in q4 and the FY2025 guide isn't bad. Interesting buy.

-

Any benefits for railroad from automation at railyards or other depots? It would seem to be too farfetched for autonomous operation on long haul stretches of rail.

-

Weaken USD Overall I like the idea as laid out by Jim Bianco to reduce US defense spend as a % of GDP and have European nations raise their share as % of GDP to 5% ish.

-

Careful on the 10 year yields. The debt ceiling is limiting total Treasury issuance. Meanwhile inflation is perking up. https://www.apolloacademy.com/wp-content/uploads/2025/02/InflationOutlook-022525.pdf If there is comprehensive budget bill passed, and the debt ceiling is raised, issuance in the latter half is going to perk right up. Wall Street was rightly worried about Stagflation under Biden in 2022-23. I think those Stagflation worries are going to rise up again for late 2025 and into 2026.

-

Could be a plus plus for CP and CNI https://www.freightwaves.com/news/new-u-s-fees-on-chinese-ships-may-drive-demand-for-canadian-intermodal-rail

-

Could be a plus plus for CP and CNI https://www.freightwaves.com/news/new-u-s-fees-on-chinese-ships-may-drive-demand-for-canadian-intermodal-rail

-

https://www.nber.org/papers/w33465 Net savings of $205B according to this study

-

Not sure what the big deal is. PetroChina, a state owned enterprise, has been making dividend payments to shareholders since the 2000s. Sure the VIE is cumbersome and has never had its regulatory status "blessed" but there are SOEs that have listed using the VIE. And China VIE controlled companies have made dividend payments to ADR/ADS over the last 4-5 years. No issues. SAFE review and approval, but if you read the rules it's mostly related to payment of dividends or share buybacks funded from retained earnings.