Spooky

-

Posts

677 -

Joined

-

Last visited

-

Days Won

1

Content Type

Profiles

Forums

Events

Everything posted by Spooky

-

Agree. The US government has been running a deficit of about 6.7% of GDP which is helping the US economy keep growing. Agree. Coming off of the run-up we had in the markets this last year and a half I am expecting more volatility. The Fed has been making noises that the US remains vulnerable to an inflation shock. Trump's / Republicans' policy goals seem contradictory with most voters wishes to lower inflation. Higher tariffs will increase prices and potentially damage global economic output. Mass deportation will increase labour costs. Also, if the Republicans extend the tax cuts without addressing spending then the deficit will get blown out even further. Layer on top of this heightened geopolitical risk and there is a lot of uncertainty. All that being said, I'm not selling down my equity positions based on macro factors, just going to make sure I have some extra dry powder / resilience for the year ahead.

-

Hope you are not serious.

-

If everyone thinks like this won't it corrode US society / capitalism in the long run?

-

How does the board feel about some of these Trump cabinet picks? Matt Gaetz as AG doesn't fill me with confidence for the prospects of the rule of law or a politically independent DOJ.

-

Devil Take the Hindmost Extraordinary Popular Delusions and the Madness of Crowds Irrational Exuberance There are also a few chapters in Howard Marks' book The Most Important Thing which are great on bubbles and directly relevant to your question.

-

Ordered the book, looking forward to reading it.

-

Advice for keeping online investing account secure

Spooky replied to Sweet's topic in General Discussion

This is built in to interactive brokers for transfers of funds / deposits. -

Advice for keeping online investing account secure

Spooky replied to Sweet's topic in General Discussion

Two factor authentication Unique strong password for each account (I use Bitwarden to manage my passwords and can monitor if a password is hacked / released on the dark web) Have several different brokerage accounts -

Agree wholeheartedly. They key to happiness is lowering your expectations.

-

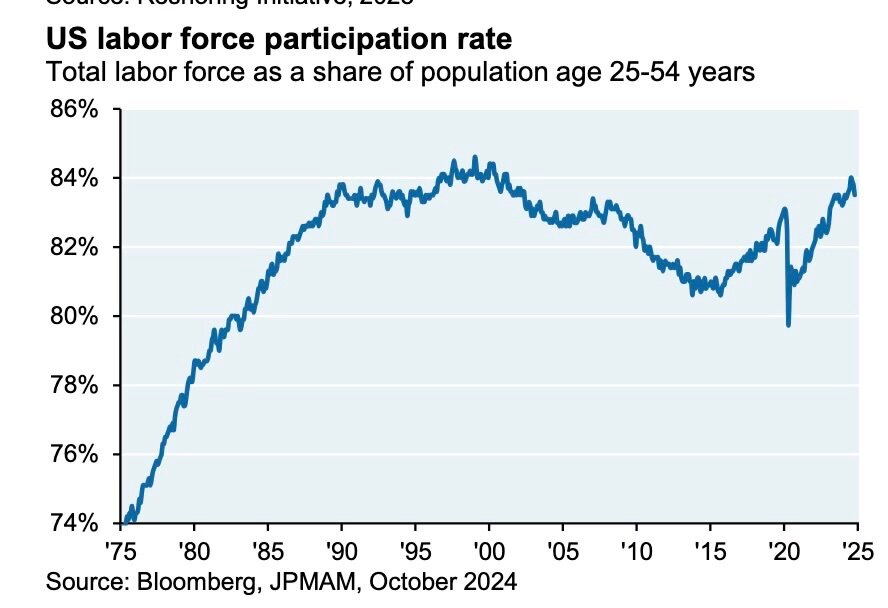

Source is from JPM

-

Have to agree with the thrust of @Spekulatius comments here. Looking at the raw data and the US economy seems to be in excellent shape and is much better than its global peers. Most countries would kill to have the economic strength and dynamism that the US is exhibiting. The problem, as usual, is that the benefits of this economic strength accrue to the top 1-10% of the population and the effects of inflation are felt more acutely by poorer segments of the population. Under the first Trump administration, ordinary people benefited since stimulus checks were sent directly to individuals. This is part of the reason why people remember his administration so fondly. The downside of this is that the distribution of stimulus directly into the economy is what led to the initial spike of inflation - too much money in the real economy chasing too few good with supply constraints. The stimulus in 2008/2009 didn't make it's way out of the banks that needed to repair balance sheets so it didn't have the same inflationary effect. Now the really interesting part is whether or not Trump / the republican's policies will be better for 90% of the population. I'm not really sure. Tariffs would be inflationary. Also, if they want to extend the tax cuts they will need to cut spending elsewhere or blow out the deficit. Government spending is one of the key drivers of economic growth currently. Biden's policies were going back to the period prior to neoliberalism - more industrial policy, stronger unions, infrastructure spending etc. There has been a surge in reshoring activity of US manufacturing jobs after reshoring progress declined under Trump. The largest surge in manufacturing-related construction spending on record, which appears directly tied to passage and implementation of the Chips bill; key locations include Arizona, Ohio and New Mexico. An industrial policy that overwhelmingly benefits GOP districts: ~75% of energy bill spending is going to GOP districts. Close to an all-time high in the labor force participation rate. Highest YTD equity gains in an election year since 1936. Will be interesting to see what happens but Trump and his team are inheriting something quite good.

-

-

Interesting. Wonder how fast until Trump tries to fire him! I've been reading Trillion Dollar Triage and there were some run-ins between Trump and the Fed in his prior term.

-

We're all probably better off not letting partisanship affect our portfolio investment decisions. The latest JPM Eye on the Market was interesting, there is a section discussing this issue and a Trump victory: https://am.jpmorgan.com/content/dam/jpm-am-aem/global/en/insights/eye-on-the-market/kamilton-amv.pdf

-

a black swan super compounder for the next decades!

-

Do we have a definitive list of which investments are Todd's vs Ted's vs Buffett's?

-

How do we square the discussion above with the jump in UK gilt yields after a) the budge proposed by Liz Truss' causing a collapse of her government; and b) the recent jump in gilt yields after the recent Starmer budget? I guess under a) the Bank of England needed to get involved.

-

Is the monetary system in the UK significantly different than in the US? Seems like the bond Vigilantes have been out in force there.

-

He wrote an article in fortune about this back in Nov. 2003: America’s Growing Trade Deficit Is Selling the Nation Out From Under Us.

-

Thanks @wabuffo. I always learn something from your posts. The plumbing of the US financial system is so interesting (and complicated haha).

-

Can you please elaborate on this further? What would happen if there is not enough private sector demand to buy the US Treasuries offered at auction?

-

You're onto something here Parsad. Either taxes need to rise or spending needs to be cut - otherwise the US could be headed for a similar story to what is happening in the UK with yields on government bonds rising sharply. The Fed is not really in control of interest rates on government debt, rather it is market participants' willingness to lend to the government. There is a scenario where US interests could end up being higher than the market is currently forecasting and we know what would happen to stocks in this scenario.

-

He sure does love T-Bills right now. Up to $288 B from $129 B at year end! I wonder how much of the equity sales are tied to: a) the risk of higher potential taxes after the election; b) overvaluation of Apple; or c) probability of some kind of financial crash. Buffett always said he doesn't do market timing / macro but he has been pretty good at it in the past. For point c) one thing I have been thinking about are Elon's comments if Trump wins where he will slash government spending by $2 Trillion. Given how much government spending / deficits are contributing to GDP currently this could create a serious recession.

-

The hurdle rate at CSU was only lowered for larger acquisitions over $100M.

-

Do you plan to continue holding Berkshire once Buffett is gone?

Spooky replied to Milu's topic in Berkshire Hathaway

These issues are not really business issues. Dividend policy can change but it does not fundamentally alter anything about the underlying businesses.