backtothebeach

-

Posts

1,045 -

Joined

-

Last visited

-

Days Won

3

Content Type

Profiles

Forums

Events

Everything posted by backtothebeach

-

In the last few days I have heard perplexity.ai being mentioned in various podcasts, and now here on the board in the Google thread. The name sucks IMO, but this could catch on. Maybe they find a catchy name for their engine that could become a verb... Private company for now. From Wikipedia: "Perplexity was founded in August 2022 by Aravind Srinivas, Denis Yarats, Johnny Ho, and Andy Konwinski.[7] Aravind Srinivas previously worked at OpenAI and now serves as Perplexity's CEO.[8] "Perplexity has raised $73.6 million in a Series B funding round, led by notable investors including Nvidia and Jeff Bezos. This investment, part of the total $100 million raised so far, has contributed to the company's current valuation of $520 million.[15][16][2][17][18] The investors so far include New Enterprise Associates, Nvidia, Databricks, Bessemer Venture Partners, Jeff Bezos, Susan Wojcicki, Jeff Dean, Yann LeCun, Andrej Karpathy and others.[19][20][8][21][18] Despite this high valuation, Perplexity has fewer than 40 employees.[19] It has garnered about 10 million monthly users.[22]

-

My guess is around $1B = 4-5%.

-

Audio quality is much better here, starting at 52:50 https://seekingalpha.com/article/4671013-fairfax-financial-holdings-frfhf-q4-2023-earnings-call-transcript

-

Post mortem on this trade: Selling the $40 three more times I ended losing $0.25. It wasn't as much fun as I thought, in fact a nuisance having to watch this p.o.s. stock every Friday in order to roll the short options. Waste of energy - lesson learned.

-

+1 Pretty much what I figured out about 5 years ago. Only two steps, with an optional third: 1. Buy Berkshire and/or other reliable compounders when they are relatively cheap. 2. (optional) when they are really really cheap add a little leverage, take off leverage when they seem slightly expensive 3. Do nothing Questions to figure out: Which companies are compounders? Which are reliable? What yardstick to use for "cheap". Not too hard for Berkshire. Or even the S+P500 if you happen to catch it in a bear market. Sadly that is boring AF, so I have not been able to stick to only these. Getting better at it though.

-

Buffett/Berkshire - general news

backtothebeach replied to fareastwarriors's topic in Berkshire Hathaway

Year-end BV should be around $260 per B-share. -

Ultimately the feeling that I was possibly cutting a long term compounder short without a really valid reason. Risking a huge opportunity cost long term versus risking a little more downside. A couple of posts on the Fairfax 2024 thread helped.

-

Bought it back 1% higher. Fuck. i suppose it was a good test to know if I would still buy my position today.

-

Very rational and makes a lot of sense. Especially the ”avoiding cash burning a hole in your pocket“ aspect.

-

What was your main takeaway? Are you indexing (part of) your portfolio?

-

There are many ways to employ leverage, each with its own nuances and execution quirks. They all involve interest as either a direct cost, indirect cost, or opportunity cost. Let’s say you have exactly the cash needed to buy 1000 shares of BRKB in your account: 1. You buy 1200 shares of BRKB, and end up with a negative cash balance on which you pay interest. 2. You buy 1000 shares and go short 2 ITM puts, for example strike price 5-10% above the current share price and expiring in three months. You end up with a positive cash balance on which you earn interest, but have limited your upside. If things were perfect, with a smooth uptrend, you could possibly roll this short ITM put up and out when it expires (higher strike and longer expiration), and basically have the leverage for free or even take in a little extra time value. Unfortunately, it rarely works out like that over longer periods, even BRKB is too volatile. This worked great when interest rates where close to zero, one could sell rather deep ITM puts. Nowadays these puts are assigned quicker once the time value has evaporated. If the puts get assigned, you end up with scenario (1.) 3. Similar to (2.), you buy 1000 shares and sell 2 ATM or OTM puts for some extra income and possibly getting your 20% leverage at a cheaper price if the stock drops below the strike price, in which case you end up with scenario (2.) or (1.) if assigned. 4. You buy 800 shares and go long 4 deep ITM calls (for example LEAPS) that use up the rest of your cash. The time value in the options is basically the interest paid on not having to pony up the entire stock price for 400 shares. Positive: there’s no risk of getting margin-called. 5. You borrow money somewhere else (mortgage etc.), put it into your account and buy 200 extra shares. This way you cannot get margin-called by your broker. 6. There used to be single stock futures, and now it appears there are CFDs (contracts for difference) available at IB with a financing rate similar to the margin interest. However I have no experience with the mechanics of CFDs. For example buying 1000 shares and buying exposure to 200 additional shares via CFDs may or may not have advantages over scenario (1.) above. Feel free to add to the list or correct any inaccuracies.

-

If your broker is going to margin call you at 150%, I think being 120-130% invested is too much. Portfolio margin at IB, allows you to go up to 500-600% in theory (depending on what you are holding) so your 120% would be much saver.

-

Undecided. Probably just leave it in cash for a while earning interest, as collateral for short puts that may be assigned. For example a while ago when I needed cash (to buy more FFH!) I switched STLC.TO stock to short ITM puts, which may be assigned at some point.

-

You're probably right, but planning to lighten up at a certain multiple and then not doing it is what? Anyway, I don't think it was a bad moment to reduce concentration risk, and I still have loads.

-

Selling 1/6 of my irresponsibly overweight FFH.TO, sniff. Months ago I planned to lighten up once it hit 1.1 * BV. I think it is pretty close to that on soon to be reported BV. Trying to be prudent, but feels like leaving money on the table.

-

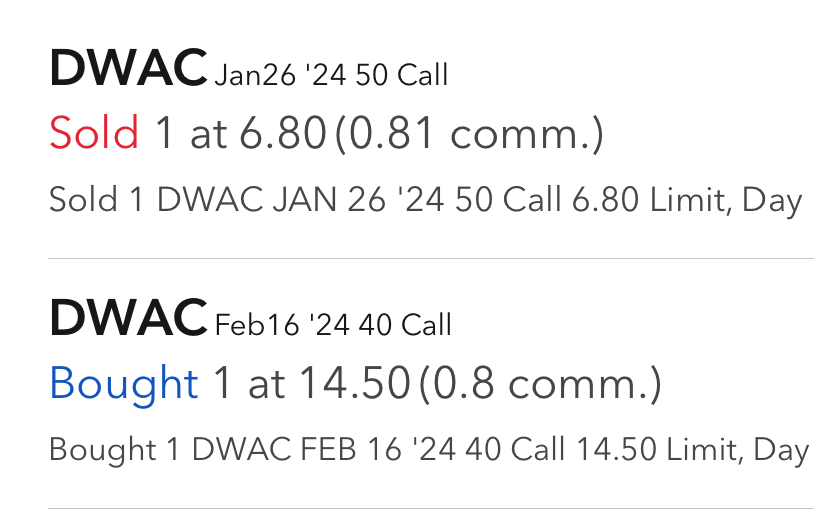

Lol, only 1 contract for fun. Just rolled down the short $50 call to the $40 strike for extra credit. Now only $5.50 net cost. Can I get $5.50 out of 3 more weeks of the $40 strike? Maybe. I probably should not clutter up the board with this stuff.

-

I think DWAC is going to be volatile for a while, and is unlikely to drop straight back down. Put on a little gamble today. Implied volatilities are through the roof.

-

Doesn't sound like Charlie at all IMO. Short sentences, borderline rude to the questioner, lacking wit. "I think old-fashioned intelligence works pretty well."

-

Buffett/Berkshire - general news

backtothebeach replied to fareastwarriors's topic in Berkshire Hathaway

Excellent. Berkshire now fully owns the largest truck stop/highway travel center chain in the U.S. How can that not be good. Price paid is water down the bridge. -

POLL- S&P 500 2024 Return Estimates by the board

backtothebeach replied to Luke's topic in General Discussion

Yep. We've all heard Buffett and Munger say it countless times. Yet the prediction game (short term market direction, interest rates, macro economy) is oh so tempting, even on the "Corner of Berkshire..." Years ago on a different board, one of the more undiplomatic posters wrote "predictions are garbage". For some reason that stuck in my mind and I frequently remember it. -

POLL- S&P 500 2024 Return Estimates by the board

backtothebeach replied to Luke's topic in General Discussion

This poll is missing an option. The one that Buffett would choose. -

I Need a Laugh. Tell me a Joke. Keep em PC.

backtothebeach replied to doughishere's topic in General Discussion

-

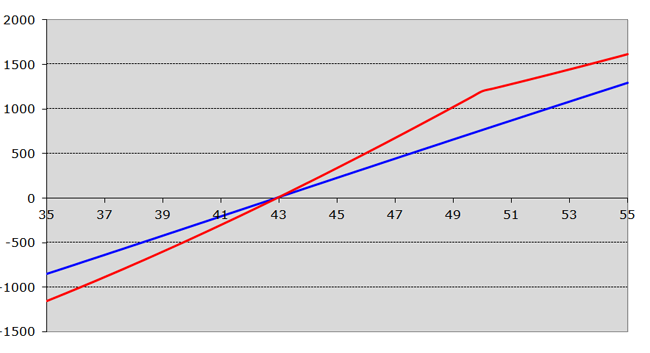

@lnofeisone your assessment was spot on, comparing risk graphs for January 17, 2025, with no changes in implied volatility. blue risk graph: -short Jan'26 45 put +long Jan'26 42.50 call red risk graph: -short Jan'25 50 put +long Jan'26 42.50 call

-

I think I was just looking for a synthetic long close to zero cost and with a low breakeven. I like your alternatives, especially the second one that introduces a calendar element and possibly a lot more flexibility in year two.

-

EBAY synthetic long: -short Jan'26 45 put +long Jan'26 42.50 call for a credit of $0.20 per share. A cash efficient way to go long. You miss out on the 2.5% dividend though.