scorpioncapital

-

Posts

3,003 -

Joined

-

Last visited

-

Days Won

2

Content Type

Profiles

Forums

Events

Everything posted by scorpioncapital

-

I would think both servicing and private MI are both low margin businesses. In one, you generate a fraction of a percent on servicing the loan and in the other, you receive a fraction of a percent of the total mortgage as a premium. I believe companies like Ocwen are outsourcing their collections to India to reduce costs, how much can they make of the total mortgage for this function? MI appears like a business of writing deep out of the money options. You collect a pittance of a premium but you don't expect to be exercised (or rather you don't expect - in the aggregate - to pay out a large part of your premium as many events have to happen for a default to occur). So the constraints are a) how much business you can write and b) how much money you make in relation to your equity base. Just to see how razor thin it is , you are making like 0.5% in premium on the amount of the mortgage. Right now return on statutory capital are very fat - something like 38% if you include the unearned premium. But it would seem that reserves for losses and a buffer require an equity margin above and beyond minimums. Thus I see returns in the mid teens to 20%. The unearned premium appears to be some sort of float while the earned premium is pure profit if the reserves for losses are accurate and things go well.

-

buying stocks with margin vs buying stocks with float

scorpioncapital replied to muscleman's topic in Fairfax Financial

I also wouldn't say that "term loans" imply no discomfort. Have you noticed during the financial crisis as the price of equity fell, it was almost like a margin call? Some companies went bankrupt, others had to restructure their balance sheet. This was also seen when naked short sellers pushed the price of the equities lower, even if it wasn't justified. -

Yes, I believe today you can write high FICO insurance and generate 20% return on statutory capital. What I've noticed is that the insurers trading at 2-3x book. So let's say leverage ratio is 16:1 (which appears to be the line in the sand for regulators on leverage limits to be compliant with Fannie and Freddie certification) and you have 500 million in statutory capital. You can write 8 billion and earn 20% = 1.6 billion. Add your paid in capital and let's say 2 billion = 4x book. Obviously this is "fair value" and there should be some discount and profit potential for the investor coming in. I would imagine if you paid 2x book in the above scenario, you'd have a potential to double your money. This is why it seems puzzling the multiples are so high, where is the profit potential for the incoming investor if he is "pre-buying" the future profits unless you assume higher leverage than 16:1 and/or higher than 20% returns. Also, you may assume some return on the premiums. For simplicity, I usually just assume that the discount rate for the earnings = the return on the investments. If this holds, you can cancel out and assume the above numbers directly.

-

Makes sense, thank you. Another puzzle for me is the valuation of the mortgage insurers. Most of them trade at 2 or 3x book value. This is a little "alien" to me for insurance operations. I am used to the idea of 1x book value as a starting point. Is it simply due to anticipation of a high growth rate or is there something about the value of the underwriting that makes it more valuable? With servicing, I can wrap my mind around the value of servicing rights and free cash flow yields while the servicing runs off.

-

buying stocks with margin vs buying stocks with float

scorpioncapital replied to muscleman's topic in Fairfax Financial

Every company in the world leverages through margin. Look on the line on the balance sheet that is labelled liabilities or corporate debt or bond issues. And every company pays a price for it. Insurance you have the chance, but not the guarantee that the rate may be negative (e.g. Berkshire which is an exceptionally run operation). Some insurance operations can even turn the liability into equity by releasing acquired reserves - this is almost like having part of your principle forgiven. Over time and large scales, the cost of funding of insurance may provide a distinct advantage - or it may not. There are also regulations on how float can be invested for most operations depending on type of premiums written, statutory capital , etc..If you look at most insurance companies 50% plus, if not 90% plus of float is fixed income. These companies will never be allowed to own anything else. Here it becomes a closer race between borrowing at say 8% and investing 100% in a business for 20% returns and an insurer borrowing at 0% or even -2% and investing 100% in bonds at 8%. 8% * 3x float = 24% roe - (cost of float) 8% debt * 1.5 leverage * return of investment purchased (e.g. 20%) = 30% - 8% = 22%. As you can see, it's a very close race. -

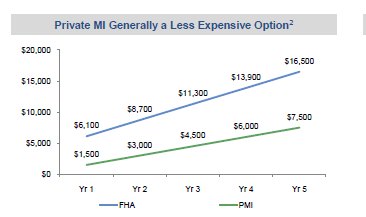

I see servicing as sort of a low margin collection business. I'm starting to conclude insurance is a "cleaner" way to play the space too and returns are good at the moment, generally seeing 20% returns on writing what in effect is a deep out of the money option (e.g. 20% payout on a 750+ FICO score customer where they put in 5%-15% down, if a default occurs and the bank can't sell the property except for a big loss). There's a lot of things that must go wrong for such a payout to occur. In the meantime, you collect these premiums and with rates going up the investment portfolio could generate respectable leveraged returns. PS... do you know why FHFA mortgage insurance rates are double to triple the price of private MI rates? I think this fact is the key to a real arbitrage and why this sector is poised for growth. The chart below is from an Ocwen presentation and based on a $200,000 typical mortgage. Clearly, private MI can't be underpricing so severely so I'm trying to understand what's happening.

-

Which businesess related to mortgages do you think has better economics? Both servicing and insurance seem to be high volume, low margin businesses and both seem to be in some form of long-term run-off.

-

"SMA refers to the Special Memorandum Account which represents neither equity nor cash but rather a line of credit created when the market value of securities in a Reg. T margin account increase in value. For example, assume the market value of securities purchased at a cost of $10,000 on margin (at 50%) increase in value to $12,000. This $2,000 increase in market value would create SMA of $1,000, which provides the account holder the ability to either: 1) buy additional securities valued at $2,000 (assuming a 50% margin rate) without depositing up additional funds; or 2) withdraw $2,000 in cash, which may be financed by increasing the debit balance if the account holds no cash. It should be noted that while an increase in market value over original cost creates SMA, a subsequent decline in market value has no effect on SMA. SMA will only decline if used to purchase securities or withdraw cash and the only restriction with respect to its use is that the additional purchases or withdrawals do not bring the account below the maintenance margin requirement. SMA will also increase on a dollar for dollar basis in the event of cash deposits or dividends." So from what I understand SMA is a tracking account created by market gains, cash transactions, or dividends. I usually just look at excess liquidity, that's the important value for all practical purposes - including option writing.

-

In Canada it's pretty simple. You pay taxes to Canada as long as you have ties to that country when you're travelling. For all intents and purposes I consider this definition to consist of two things: 1. You are travelling on a tourist visa even if you travel for years on end (although you can never stay put very long.) 2. You are financing the travel from money in your "home" country and continue to pay your bills at home. This last point is a bit murky. What if you have no house to rent or own or car, just bank accounts and medical care and a phone? Well, I think that would be fine given that your money centre is still your home country.

-

How can taking a random % be right? What you do is walk around your home office and measure the square feet. Then you divide by the total # of sq feet in your house and that's the %.

-

Your highest conviction idea for 2014 + why

scorpioncapital replied to steph's topic in General Discussion

KCG holdings. Largest market maker, growing brokerage. Selling close to book value. costs are going down, earning power is going up, debt is being paid down. 2014 should be good. -

fbrc, cheap, just bought back 650,000 shares.

-

IB as a partner is a good investment. They have helped me to make more money then otherwise would have been possible in stocks, options, and futures. Am just an individual. I am surprised they don't take ALL the business away from everybody else, call it lack of knowledge. I'm sure there are a huge amount of 10k+ accounts out there. I hope they succeed big time, but that has never been in doubt.

-

My observation for several years holding the same stock is that you almost always tend to get some proportion as a payment in lieu. I'd say around 30% of the total.

-

He said an interesting thing - I usually go long the things others go short. I liked that :)

-

And now, Jefferies & Rich`s first `semi-letter`! http://jefferies.com/CMSFiles/Jefferies.com/files/Insights/JefferiesInsights_July2013.pdf

-

Tax treatment of options in Canada - Non trader

scorpioncapital replied to beerbaron's topic in General Discussion

given that you have to file an ammended T1-ADJ if a written put is assigned instead of expires worthless in a new year, I usually add these two provisions to reduce headaches - either write options that are deep out of a money with slim chance of assignment OR ensure assignment is in the same year as it was written. -

i sell deep out of the money put options while waiting. If I think a stock is overvalued now, many premiums are yielding 15-20% on collateral at half the price. Presumably half the price is a better entry point for a stock you like than twice the price.

-

The easiest strategy is to buy a good investment and forget about it. You don't have to worry about when to sell or buyback. And you don't miss out when it shoots up. Conversely you also have to watch it go down, but so what if you're holding for a long time?

-

calculating returns for selling puts

scorpioncapital replied to scorpioncapital's topic in General Discussion

thanks! seems options reduce buy/sell flexibility to some degree in exchange for carrying out a plan at fixed benchmarks. -

calculating returns for selling puts

scorpioncapital replied to scorpioncapital's topic in General Discussion

Does anyone with experience know how assignments of option contracts occurs in real life? E.g. You sell covered calls 6 months away at a certain strike. Let's say the premium is close to zero. It's one month later and the stock reaches the strike price. Question: - Is assignment immediate or do you have a couple of minutes or hours notice? - Is assignment guaranteed? I.e. could the other party wait for the stock to rise even higher thus ensuring a lower exercise price but giving the seller uncertainty about what will happen? - Can you induce the assignment at the strike if you want to? -

cypress is a tax haven right? So a 6.7% one time tax in a tax haven appears to be peanuts to foreign account holders who are paying no income tax.

-

calculating returns for selling puts

scorpioncapital replied to scorpioncapital's topic in General Discussion

I see, so people are saying something like: put premium / (Capital outlay if exercised * probability of exercise (est.)) * (time to expiry*annualized adj.) = return. (and minus interest on collateral if you have to pay it) -

For deep out of the money puts, I take the return to be roughly equal to the premium divided by the collateral requirement. Some people take it as the risk of exercise * the cost divided by the premium (but how do you quantify the risk for an of the money option?). as an aside, do people think getting 10.5% annualized on a 4month put that is 33% out of the money is a good deal in this environment?

-

What's to stop interest rates from staying at zero until stocks double from current levels, only then to be raised for them to crash back down? Who wouldn't want to participate in the extraordinary profits from now until that time?