changegonnacome

-

Posts

2,694 -

Joined

-

Last visited

-

Days Won

7

Content Type

Profiles

Forums

Events

Everything posted by changegonnacome

-

The 'only' thing.....its the most important thing......the loans are 'money' good...........the credit quality in FRC's historical asset book is outrageously good.......if they can get their funding costs down and shrink the negative NIMs.......then its a very unprofitable zombie bank......but a going concern.........which limps on and probably gets bought out for below book value once rates normalize & the crystallization of MTM losses in a change of control gets smaller. Reducing funding costs is exactly how the muted FRC 'bail-in' by other banks would work.......overpay for some underwater loans they have and hand FRC cash and reduce their funding costs.......it would be an act of self-interested charity from an industry not known for any. There is a PR value to it.......08 the banks wrecked the country.....2023 the banks helped stop GFC 2.0 (I know it isnt but thats how you could play it). I'm not saying its likely to happen but it might be doable - or they wouldnt be talking about it so much. There's a longer term question about whether the franchise can be repaired.....it certainly cant for a long time to come re-implement its old business model.......and the question I've always had with FRC or any bank with such a high NPS rating in a commodity industry.......is as soon as you stop offering kind of sweetheart deals to your customers.....how loyal do they stay, how much did they love the 'deals' and not the bank.......the answer from SVIB & FRC is there is of course ZERO loyalty in a bank run scenario......when the 'new' SVIB is less likely to give the CFO/treasurer of HotStartUpCo a 3% 90% home mortgage collateralized with stock option that don't vest till 2030.......how 'interesting' does keeping all your corporate deposits with SVIB become......how strong really is the SVIB's/FRC's offering absent outrageously sweet deals. In terms of aggressive rate cuts in 2024......this would also bring the MTM loan book back closer to par.....such that they could sell the book and take a much smaller MTM loss that tangible equity could absorb.....and again lower their funding costs. Rates & bank run broke the bank........rate cuts would certainly help & why if your in First Republic the recession cant come soon enough.....your effectively your praying for it....certainly in First Republic where credit book is gonna do fine from a default perspective.....the market value of loan book would go up.....and your funding costs would drop like a stone. FRC is a bank that would love the US economy to go of a cliff and preferably as soon as possible.

-

Cant say across the board - the only small actually micro-cap i hold is Hostelworld......and on IBKR it indicates the margin requirement for HSW is 100%.......HSW is ~$150 mkt cap.......its also listed on LSE so maybe that factors in too to margin allowable

-

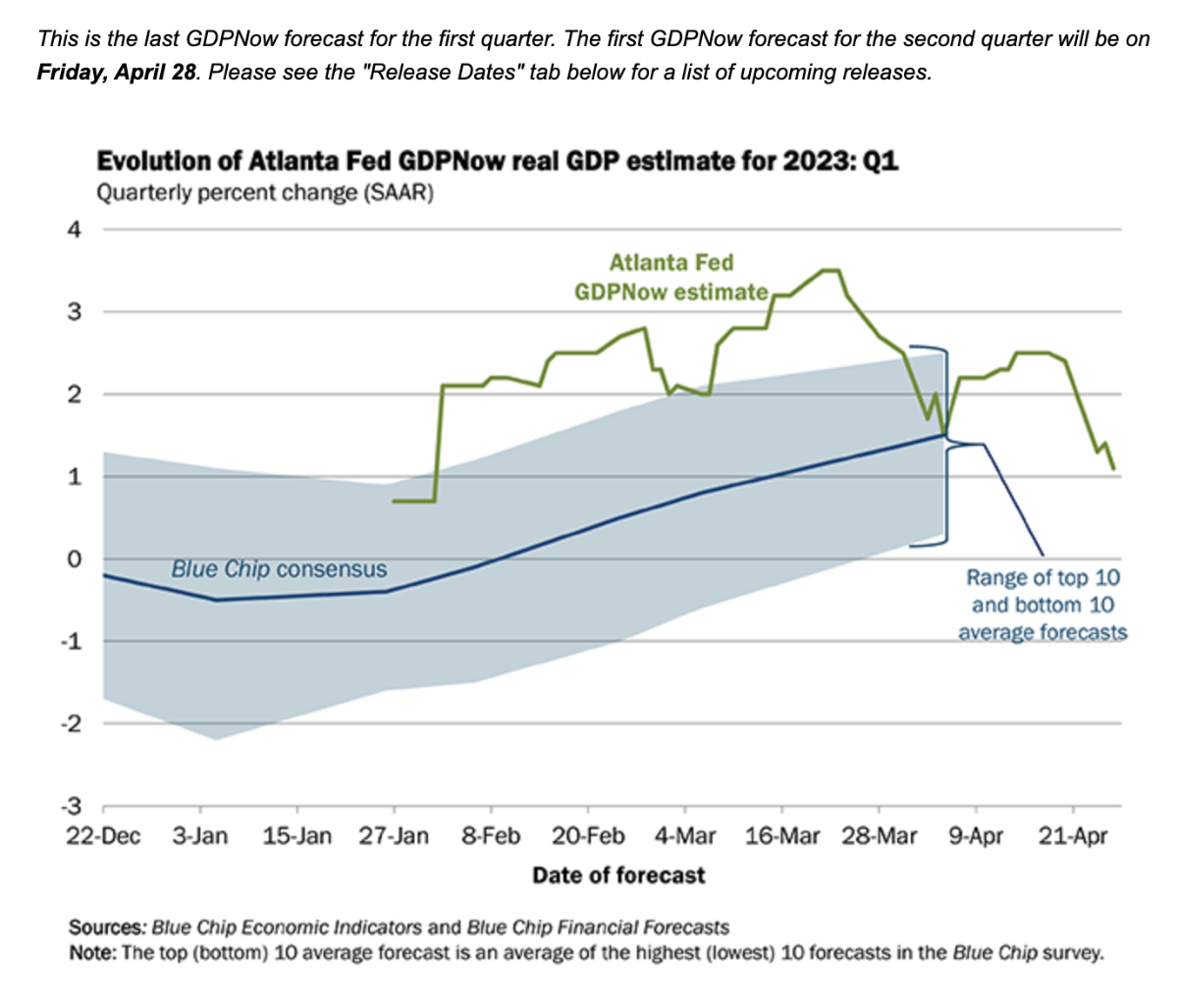

This is Q1............lets see what Atlanta Fed GDPNow predicts for Q2 on Friday and how those predictions evolve over the Qtr.......extrapolating some of the momentum......Q2 could go negative......but Q3 seems, to me at least, to be highly probable to go negative.......the severity and length of that negative dip.....is tough to predict......I have a view that Powell will surprise with his resoluteness in the face of a weakening economy......as Druckenmiller points though, to date, Powell has not been a profile in courage.......the right thing to do is to hold the line on rates into a weakening economy & put this inflation nonsense to bed.....to do so requires courage......courage in public officials is usually in short supply.

-

https://www.atlantafed.org/cqer/research/gdpnow Atlanta Fed 'GDPnow' estimates for Q1 GDP took a major downgrade today........you can see the evolution over time...with SVB collapse & tightening credit conditions playing a role as the estimates began to ratchet down in March. Not perfect - GDPnow's average model error rate is 0.83%...when you take their final Q estimate and compare it against the reality Q2 GDPNow estimates out this Friday....which will be very interesting (if your into this stuff!)

-

Final destination is the grave......unless some dramatic rate cuts come.........this is that rarest of a birds a US bank that really wishes the US economy would go off a cliff ASAP to save its bacon! Quite a turnout for the bank investing handbook. Doesn't necessarily think they are going out of biz immediately though........NIM's are negative but some equity capital can be extracted by selling the wealth unit......that will buy them a few more quarters before they breach regulatory ratios and need to raise external dilutive capital (if they can, not sure there's biz model there anymore when they sell wealth unit)...........of course all contingent on the large bank depositors sticking around.....in some respects whatever equity thats left in FRC (ignoring big picture MTM negative equity) is slowly getting transferred out the door to JPM et al in deposit interest payments.

-

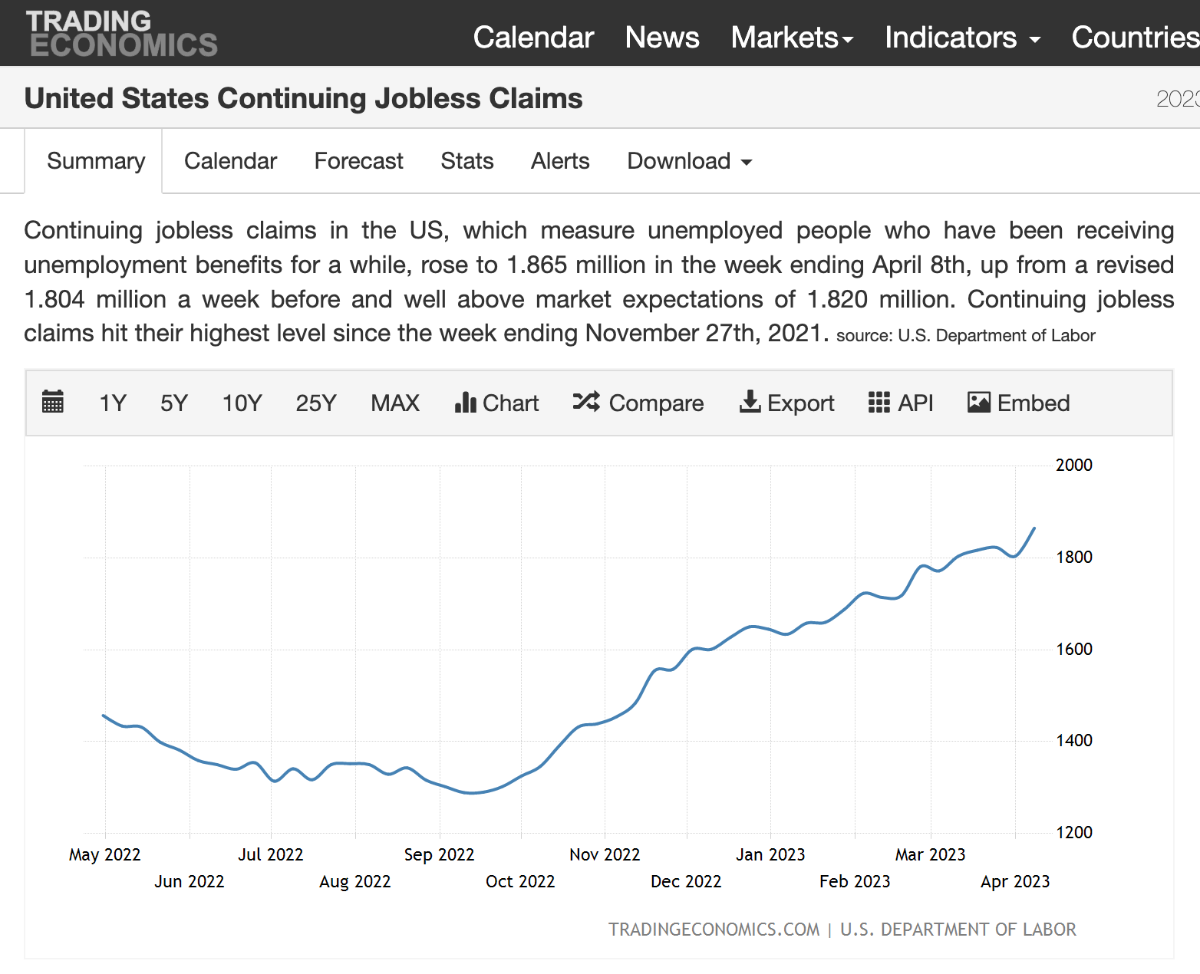

I would be SHOCKED if it doesn't happen before year end. Shocked, stunned & floored. Just based on the credit contraction data being indicated in loan officer surveys & continuing jobless claims relentlessly climbing as I shared in previous post......and a Fed I think that will continue to invert the yield curve via additional raises until they know for sure employment has cracked.....we are IMO hitting crunch time on this.......and even then they will hold the line (no cuts in 2023) and let the economy deteriorate a little further into the back end of the year to ensure a round of wage setting across the economy is being done with a poor macro backdrop. Tactically the next couple of FOMC meetings are super important to secure that outcome in the back half of this year. The severity of said recession I have absolutely no clue about........because 2008 was the last recession everybody anchors to that and they are i think wrong on that front.......2008 was a once in a generation, once in a century systemic crisis......I just don't see that risk out there........I expect a kind of garden variety one in line with hiking cycle driven recessions of the past......if you, as the Fed, create the recession it stands to reason the solution to bring back full employment is a loosening of financial conditions......basically steepen the yield curve, make it attractive to folks to provide credit.....but we aren't going back to zero interest rates......and when done we wont be going to 3.4% unemployment either....the Fed will attempt to float unemployment around the 4.5% area to ensure its not a contributor to inflation on a go-forward basis.....post this inflationary bout they will be very trigger happy to raise rates I think......so a higher floor for Fed fund above zero + an inclination to nudge rates up once they perceive slack to dissipating in the employment market.

-

Druckenmiller takes aim at dollar in sole conviction trade https://on.ft.com/44fqmDJ The Druck joins me in hard landing camp……

-

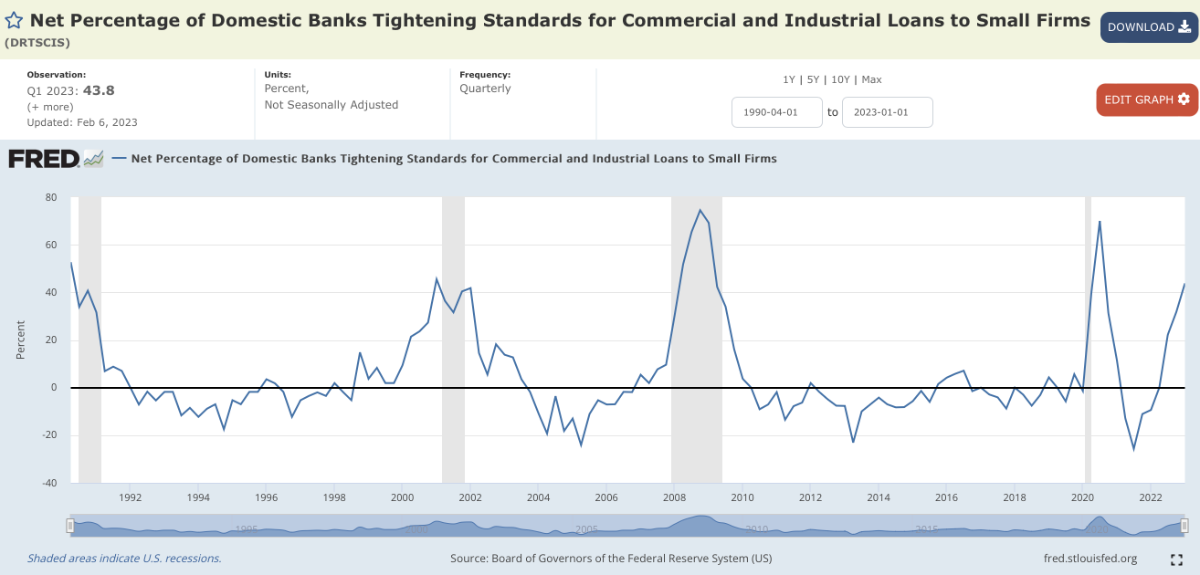

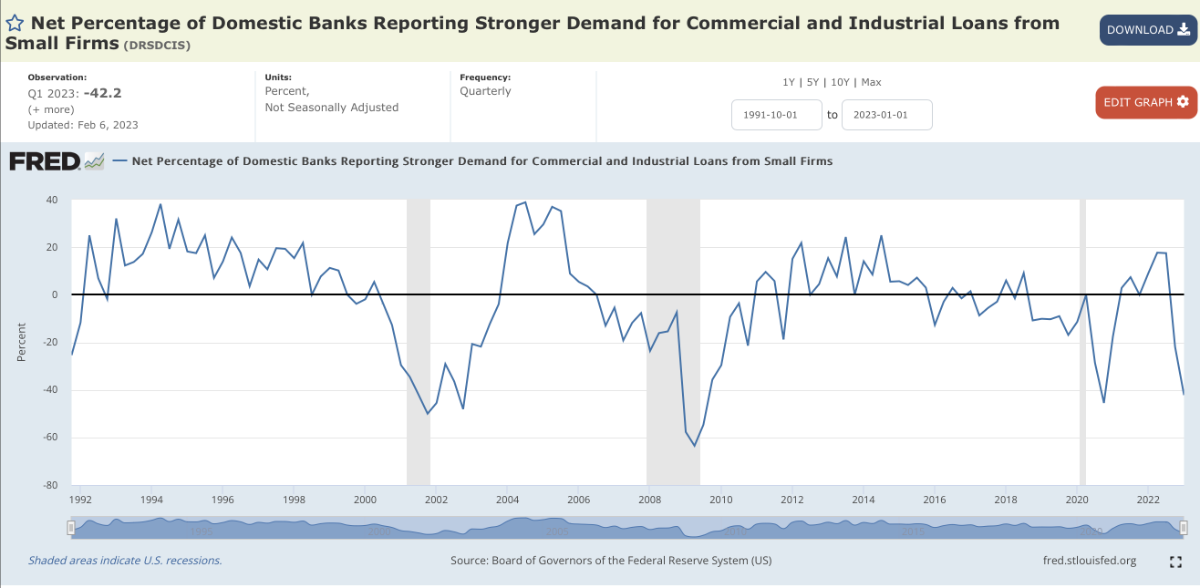

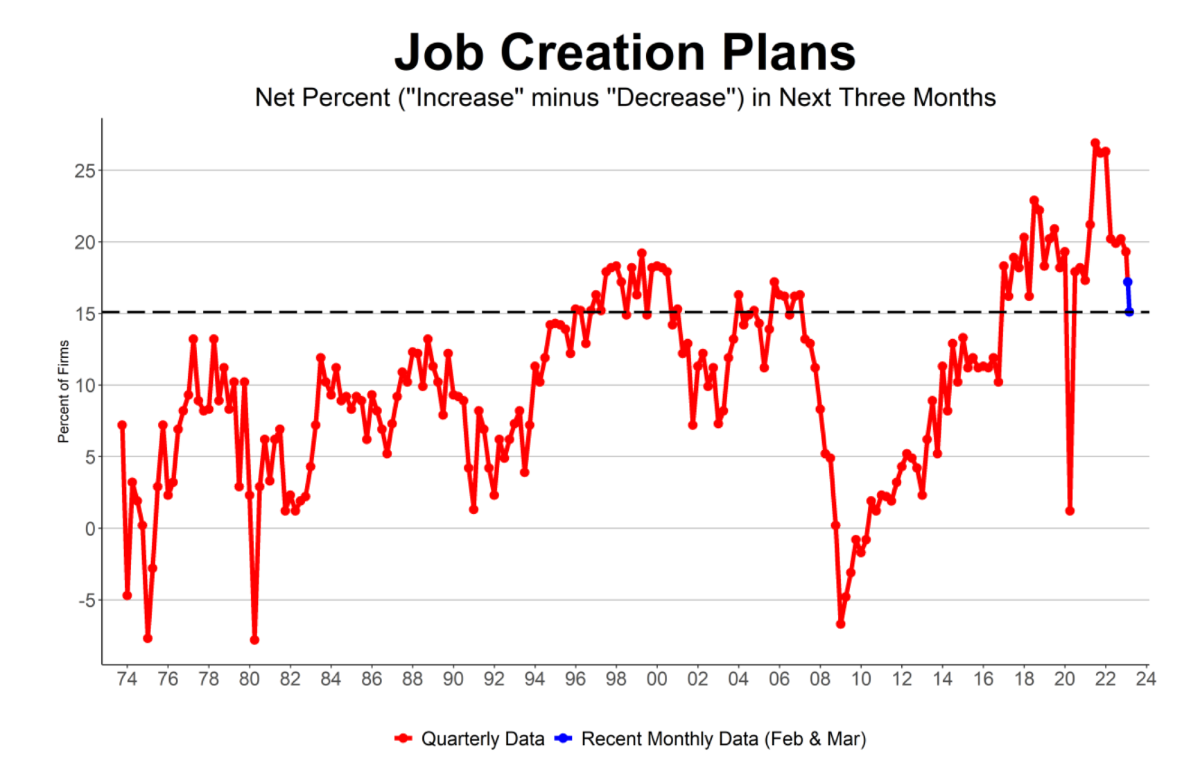

Its impressive - the power of brand........and a triumph for the food scientists at Pepsi to create such brand/flavor addicted customers......the vast majority of companies outside of Tobacco, unfortunately, don't have such a direct line into peoples dopamine receptors and so you have vastly inferior pricing power relative to a Pepsi/Coke/Altria.......and so you get the mighty 3M today....revenue/volume declines....and the inevitable layoffs to try to get ahead of margin declines. Its very clear at this point that the economy is deteriorating.....everywhere you look the sources of funds, (1) Credit (2) Employment Income - for spending in the economy are drying up........ Credit contracting significantly (I focus on small firms...but medium large firm data is just as bad)....inverted yield curve + SVB crisis has created exactly what the Fed wanted - Credit availability, as discussed previously is the mechanism by which the Central Bank gets to influence spend in the real economy first..........a credit contraction precedes & then creates a relatively modest spending contraction (modest relative to the total quantum of spend in the economy where income is actually the largest source of funds).....the modest credit contraction begins to effect at the margins employment, leading to increasing unemployment claims.....which has a much larger effect on aggregate spend ......given one persons spending is another person income.......the first 0.5% rise in unemployment above trough low, given the circularity of employment & spending & the momentum inherent in it, pretty much always goes on to complete a full 2% rise above trough....Sahm's rule......so 3.4% is 'our' low.......jump to 3.9%.....pretty much ensures a trip to 5.4% unemployment levels is in the offing. Employment levels go up on on an escalator & down on an elevator....try hiring a 1000 people and then try firing a 1000......the latter is a much speedier process. Credit contraction is beginning to feed into the outlook for small firms job creation plans but happens with a lag against the credit contraction backdrop (NFIB chart below) So we are getting elevated layoffs (3M etc.) but up until recently laid off folks were getting re-absorbed quickly by other firms hungry for workers.....we all know the JOLTS stuff and all that........but more interestingly given the supply of laid of workers vs. the demand for workers and the ability for other firms to absorb them..... that has started to show a negative mis-match....the so called continuing unemployment claims below.....steadily rising MoM In some respects an economies health is either improving or dis-improving....improvement being driven by credit creation & growing incomes and MTM wealth ....this unfortunately everywhere you look is a 'dis- improving' economy...............there are no new incremental sources of funds coming..........credit is contracting against a deeply inverted yield curve......continuing claims are rising and so incomes look like they are next to go.......if you work in 3M or Disney or similar firm......your pay rise next year is you get to keep your job....so no extra funds coming from pay rises soon.......everybody already refinanced their houses & house prices at best have stopped appreciating in real terms on a nationwide basis....no extra funds for 'fun' to be found in bricks & mortar........and SPY is stuck around 4100 at best....stubbornly ~15% below its highs of 4800....so no extra wealth effect or wealth wealth leaking out of 401k/IRA's gains right now into the real economy. With all that said.......this is EXACTLY what the inflation problem requires & what the Fed wants to happen.......the soft landing scenario is one where a small uptick in unemployment to ~4 or 4.5% in the next few months is enough to scare the hell out of those with a job to seek exceptionally modest or no pay rises into the back half of this year.....while also incentivizing them to dial back spending & increase their savings by enough that spending growth & by extension inflation moderates. Its possible it happens......but unlikely.......the chain reaction nature and speed by which employment deteriorates always catches Central bankers off guard & flat footed.......4.5% unemployment might be all thats needed to get us 'back to 2'....but the impreciseness of monetary tools relative to the complexity of hitting & holding a defined unemployment number........is like asking a cardiac surgeon to operate with a machete instead of a scalpel.....your gonna end up with blood and guts......and unfortunately we will, for a time, cause Powell is a mere mortal with a limited toolkit & deep seated fear of becoming Arthur Burns.... we will end up with 'unacceptable' levels of unemployment....and a recession that justifies a lightly shaded grey bar on future FRED charts.

-

New Bank Added to Insured Bank Deposit Program Dear Client, We would like to provide a brief update on our Insured Bank Deposit Program. What: Simmons Bank, Tristate Capital Bank will be added to the Insured Bank Deposit Sweep Program. Maybe past is prologue distinctly remember First Republic getting added to IBKR's sweep program in the weeks before their troubles!

-

I definitely put this in my too hard pile - its like trying to predict the weather....way too many variables and the chaos associated with investor behavior two or three derivatives out. It was kind of musings on what I'd do as a boomer presented with the current environment. I'm on shakey enough prediction ground with my musings on what inflation does next (& the Fed & the economy).....so I wont go any further........it just struck me as an interesting thought......and one the likes of KKR & Blackstone have likely already had!......given volatility laundering inside PE/RE funds offered to retail/wealth management clients seem to be the next growth wave for the folks in alternative asset managers.....very clever and good timing by them!

-

The relative piece is important here....we are at an interesting juncture. Depending on your return requirements on a go forward basis there is indeed an alternative to equites....TINA is gone (for now).....and we've got a hell of lot of boomers that enjoyed a basically uninterrupted fall in interest rates from 1981 to 2022 twinned as it was with a wonderful period for asset/equity holders........who might blame those boomers for pulling their pile of chips from the volatile equity table for the final stretch of their life journey....buying some peace of mind, comfort & predictability found in owning treasury's & such........this boomer demographic is a very large cohort of wealth everywhere........how they choose to allocate capital will be interesting to watch. I wonder if another 2022 like drawdown with even higher yielding treasury alternatives around vs 22....might see a bunch more boomers throw in the towel in the next large downdraft & jump ship in greater numbers to T-bills/CD's/savings accounts/MM funds & not return......in a way aren't secular bear markets defined by relief rally's where each subsequent rally has less and less people return to bid back up assets to anywhere close to their previous highs....resulting in those charts we know from 1999 & 2008....of lower lows & reversals that fail to take out the the highs of the last rally........the next correction in the equity market will happen with the backdrop of alternatives like this - https://www.bankrate.com/banking/cds/cd-rates/ - 5.1% yielding certificate of deposits. I've been privy to one or two boomer chats that played with this idea of 'going to treasury's'......that perhaps it was time to cash in the chips at the equity casino "its been a good run" & head for the fixed income exits.....and these folks aren't dummies either they understand full well the limitations we've discussed of fixed income instruments vs. equites in growing wealth against the backdrop of inflation....but they also understand what a fabulous run they've had & when to leave a party.

-

The global flashpoint, as everyone knows, is/will be in Asia.......as America did in its rise to regional hegemon & subsequently global hegemon..........China, as an emergent rising power, will seek first to dominant its own region of the world...if it can't dominate/control an island a number of miles of its coast it has a problem.......the 'containment' of China from becoming a regional hegemon in Asia is this century's great battleground......and the likely frontline of WW3 if it happens.......as we know China is surrounded by difficult & problematic neighbours....... it has a tough tough road ahead to create anything close to the North American-esque sphere of dominance & safety that the USA first established and then enjoyed in the formative period of its rise to global superpower.......Russia has been pushed into China's arms as allie & now defacto dependents......the cost of the Ukraine war in a strategic sense for the West is that, with Russia in its back pocket, we've helped China put one piece of the complicated jigsaw its attempting to put together in its region.........it's clear to me the Western power should be trying to make China's life ever more problematic instead of simpler............Japan, Vietnam, S Korea & Australia are absolutely key to that and whomever else we can get in our column.

-

Massively levered maybe not. But selling PUTS when the Fed wanted the market and economy to go up worked out very well.......they never got exercised and if they did (on the right companies) I was cash/margin covered & you got put the stock & they invariably rallied upwards anyway & you exited at profit + your premium.....in this situation IMO you sell OTM Calls......safe in the knowledge that the Fed needs the economy to go down/slow to fix inflation and the market going down is a consequence of that and a help too to their aims......don't fight the Fed!.....sell OTM calls on economically sensitive companies/index....& if you ever get called....and your now short the shares....you sit safe in the knowledge that the beta sucks, the economy is slowing and you'll get to exit........selling vol essentially.....rinse, repeat. This morning especially I opened up an ultra bearish option spread.....selling 6 month 15% OTM calls on SPY/QQQ......recycling the net premium and buying equally priced 6 month OTM puts on same ......its a direction bet clearly.....and pretty levered on the assumption that I'm using what I consider 'free' call premiums (other people's money) to buy bear puts.....high high probability IMO the bet costs me nothing at worst....at best it pays handsomely with high returns on equity. It feels asymmetric...but for peeps reading this the notional bets your taking can be large...you need these options covered by cash IMO or modest shock absorbing margin if you do indeed get called or put....it just so happens that I get paid 4%+ holding cash or 5% for 3M treasurys to cover such little exercises....and again for those that have me confused with a perma-bear I'm up to my tits in a bunch of longs with maybe 80% gross market exposure.....so this short stuff as a % of NAV is small-ish for me....I'm not betting the house on SPY 3000 and dont suggest you do either.....I do way better with SPY at 5000 than 3000 thats for sure (for full full disclosure I do way better with the FTSE rallying if I'm honest)

-

Yep......why wouldnt it....unemployment at 50yr lows, nominal wage increases running at 5-6%......feeding into nominal spending increases YoY of about the same...against.....a labor force participation rate that is flat/depressed, productivity growth horribly low, demographics deteriorating & a dysfunctional immigration system......the 'spend' side of the economy is outpacing the 'output' side of the economy by a level which just makes 2% inflation impossible.

-

CPI print for March is consistent with my long held view…..domestic services inflation is not magically going away….it is not some exogenous phenom that is disappearing or rolling off soon…this ain’t supply chains and it ain’t Putin….it’s occurring contemporaneously MoM at a ~5%+ clip….it is Made in America inflation created at the intersection of nominal pay increases/spending growth & anemic productivity growth underpinned by ultra low unemployment …..headline inflation will continue to fall for a little while more…..but it can’t fall forever cause headline & core are about to converge & flat line in the mid-4’s. The only thing that changes the math is weakening spending, rising unemployment & maybe some minor uptick in labor force participation precipitated by weakening economic backdrop. I stand ready at each inflation print & economic print to pivot from my view and go 112.5% long…..the inflation prints are changing until demonstrable economic weakness starts showing up in the data….retails sales, unemployment etc etc

-

Spot on - the people showing up in the office will have a demonstrably higher ‘survival rate’ in downsizings. WFH policy ‘maximizers’ will be the first on the chopping block…..an interesting measure of this would be the office occupancy data that gets released by control/access system operators….keep an eye on the Monday & Friday office occupancy levels rise as the economy deteriorates….this would be an excellent real time employee ‘fear’ index.

-

Your sending me research papers....and factor quant models...and the Dean of Valuation.....and I'm simply telling you & saying that if say Uncle Sam offered me a 10yr treasury bill today with a 10% coupon....and Apple was being offered to me at the same time with TTM FCF earnings yield of 3% & IMO poor prospective earnings growth....that somehow those two instruments can't be compared somehow...cause they are apple & oranges ...nonsense....if thats my investment choices.....in my humble opinion you take the 10yr T-bill @ 10% and run, run fast....if you offer me Hostelworld equity then I tell Uncle Sam to go to hell with his t-bill. Now if your also saying that the ERP hasn't been a great predictor of prospective stock returns..that the ERP as a factor is useless..thats its use is limited.....I just agreed with that in my post above.....I never said it was gospel or live your life by the ERP....the ERP in 2021 flashed a very generous 2-3% over bonds...signalling stocks were cheap and one should buy them up.....it was wrong, very wrong....stocks were actually expensive.....bonds were in a 3000yr bubble...making stocks look relatively cheap under the ERP or 'fed model'...Cliff Asness is right.....but if you are trying to tell me that an investor can't think in opportunity cost across both bonds and equities in a holistic way, forecasting & estimating prospective returns relative to risk in both and coming to a conclusion on where best to put their incremental marginal dollar cause somehow it's impossible to compare the two . Then we have fundamental disagreement. As @thepupil says above.....equities arent always the 'right' answer....and to not consider them while thinking about where your next incremental dollar gets invested....is to be a one trick pony.........and thats before we get in to your or anyones relative or historical ability @vinod1 to accurately forecast the equity coupon or future prospects for a company.....lots of investors I know..... lack a demonstrable ability as fundamental business analysts.....and their returns would greatly benefit from loading up on bonds for all their nominal limitations....simply because they provide a lower probability of impairment of capital.....whereas poorly chosen equities offer limitless opportunities to do so.

-

For sure.......but at the same time you've got to ask yourself investing in anything where both the equity 'coupon' is TBC and the liquidation price of the investment is subject to timing (when you need to sell it) and valuation risk (how much the market is paying that day on an earnings multiples basis at that time)......that you are being adequately compensated for that risk relative to perhaps more certain alternatives...bonds, investment properties etc.....ERP, with all its shortcomings that I am not ignorant too, is a measure at a point in time of the reward to the risk your being paid to hold an instrument where the "coupon" is variable....& indeed the future price redemption level is variable.........it is not a panacea.....but your investing acumen, decision making over time and so your ability to 'pick winners' is not a certainty either.......while holding an index does not excuse you from risk also.....price matters.........lost decades happen in indexes too if the 'buy-in' price is too high and the alternatives available to you contemporaneously were better........ask our Japanese friends.....or maybe ask a Nov 2021 vintage QQQ purchaser now or indeed in 3/5 years time....right now that QQQ purchaser would be immeasurably better off, if he/she had a time machine, 'investing' in a ZERO coupon FDIC insured checking account....christ even cash stuffed in a mattress would have outperformed QQQ in that period. ERP in Nov 2021 was 'wrong' of course.....bonds were in a bubble, a 3000yr hum-dinger of a bubble....so the ERP looked reasonable because your comparing one variable (bonds) that were in a unsustainable bubble against another thing....it was a useless measure back then.....the mistake of course was not recognizing that. The ERP failed then.......it is not perfect. Don't ever remember saying it is...but if you told me that the 10yr/30yr treasury for the next 10yrs was going, to on average, be around the current zipcode of where we are now.....I would argue you are making an error buying SPY at 4100......the earnings outlook is IMO average to poor....& your paying too high a multiple for those earnings relative to alternatives. Thats my opinion For example on our bond versus stocks argument....I'd be willing to wager.....with anybody....that purchased today and sold in exactly one years time........that a 30yr treasury bond with its paltry 3.6% coupon....sold in a years time at mark to market will very very likely outperform SPY/QQQ incl. dividends on a total returns basis......I'm assuming here of course that our 30yr bond gets some capital appreciation at our point of sale because the Fed has started cutting rates in 2024 & we redeem above par while picking up 3.6% in the intervening period.....I'm also assuming SPY earnings continue to shrink....and multiples on those contracted earnings shrink too as optimism turns to pessimism.

-

"So comparing a static earnings yield to a bond (or inflation) isn't valid." Its the most valid thing in the world....investing is the practise of comparing things..... prospective returns relative to risk and opportunity costs........if you aren't thinking about the pricing of your next equity investment relative to other things you could also invest in (investment property's, bonds, private credit, yourself etc.) you are doing it wrong. Do these investments have different characteristics....YES.......does that mean you can't compare them......NO.......End of.

-

Vinod your throwing around terms like 'real' and 'nominal' in a very strange manner......perhaps we need to clarify terminology because I feel like fundamentally we are having a poorly defined conversation with ambiguous interpretations of terms ......we live in a nominal world......it is the stated figures we see all around us....that your understanding? ...you talk to your boss about a pay increase....its a conversation about increasing your nominal pay by X%...............once you have that nominal pay increase 'in-hand' you can make assessment based on historical or future inflation what you believe that pay increase translate too in REAL terms...so 'nominal' is the number you see.....and 'real' is a number you adjust too in the context of inflation. That's the way i use. How do you use it.....or use in the context of what your comments above. Now let's define "earnings yield'from Investopedia: https://www.investopedia.com/terms/e/earningsyield.asp#:~:text=What Is Earnings Yield%3F,a company's earnings per share. "Earnings yield is the 12-month earnings divided by the share price" OK now take the nominal and real terminology we (hopefully) have agreed on above.....and apply it what you are calling the 'earnings yield' of a stock(s) 'approximate return'....not much approximate about the earnings yield it can be precisely calculated?....it uses the current share prices & TTM earnings....both are knowable......nothing approximate there?..not much place to use real & nominal terminology either...the prospective earnings are, as we all know, uncertain and we spend inordinate pages on this board trying to figure them out..........then also can you please explain to me like I'm labrador what you are saying here - "When someone says "earnings yield" of stocks as an approximate return, they mean real return not nominal return.".......because earnings yield to me & Investopida and everyone I speak to.......refers to a nominal number....the share price divided by 12-month earnings....basically an inverse P/E.......your use of the terminology of real & nominal in this context is confusingly put so my guess is your shoe-horning some other investing concept into these concepts that I'm not getting. The way I might use it would be to calculate XYZ Company's 'earnings yield' of let's call it 3% (share price of $100 divided by TTM earnings of $3 per share). XYZ company has an 'earnings yield' of 3%........you agree?.......this interpretation of an earnings yield is widely accepted by almost everyone in the investing biz...now if we want to start throwing around terminology like real and nominal and attaching it to 'earnings yield'.......we can do that too and this is the only way I know how....... let's say inflation was 5% in the same TTM period that XYZ had its earnings.......the real or inflation adjusted earnings yield is -2% (3% earnings yield minus the TTM inflation rate -5%). Great if we could get to the bottom of this @vinod1........we can have separate discussion on the usefulness of ERP as concept.....the fact its a point in time calculation.....how its performed as a future indicator of stock returns......or indeed a predictor of whether stocks are expensive or cheap on an absolute or relative basis, its failure in emerging markets as per Damadaron etc.

-

You’ll need to be a bit clearer on that one cause it makes no sense - are you saying stock ‘yields’ live in a universe where they aren’t subject to inflation pressures/adjustment…..or somehow they are guaranteed by dictate to adjust upwards always to provide a guaranteed real return for the purchaser like TIPS are over inflation……that’s big leap & it assumes perfect pricing power…..and ignores why its called equity RISK premium (ERP)…..I mean SPY usually grows its earnings….……but not always….thats the risk..….we are about to enter a period IMO where we will be/are printing nominal falls in earnings…..and very large REAL falls in earnings……ask SPY owners who bought at 4800 with say bottom up earnings now for SPY sitting at around 210 about it….they have a 4.375% earnings yield on that purchase price….in a ~5% inflation economy…not good…...& where 3 month treasury’s have a 4.9% yield with NO risk….and where the direction of travel for earnings is likely not good….yes time will make the math work…but no guarantees…..what are corporate tax rates & earnings going to be in five years with AOC as President? I’ve seen people talk about how historical ERP figures…….are dumb, cause they’re a point in time and static and compare apples (fixed coupon) to oranges (equity ‘coupon’)….as companies grow their earnings / ‘yield’..….and bonds don’t……my rebuttal to that thesis…..is exactly what market participants don’t know that?……..the historical ERP is very valid measure of valuation as EVERYBODY understands one is a fixed coupon and the other is not….the variable-ness of the equity coupon above the bond coupon….is the RISK…most of the time the E goes up…but not always….how much investors historically wanted in compensation to take that risk is a very valid benchmark across time……it is in some respect a measure of optimism and pessimism…..exuberance & fear….its the only thing that matters but it does matter.

-

Stocks Haven’t Looked This Unattractive Since 2007 - https://www.wsj.com/articles/stocks-havent-looked-this-unattractive-since-2007-78fc374c?mod=hp_lead_pos3&mc_cid=22aaaa4263&mc_eid=34200f3bc4 It's tough out there for stocks.....with bonds giving so much competition.......the bearish amongst you will even notice how the above is using trailing earnings......there's a kind of optimism built in to the thought that SPY earnings can be maintained at even these nominal levels (never mind keeping up with inflation in real terms).....my thoughts are that earnings come down in nominal terms quite a bit but in real terms quite a lot (already have).....but I think the 10yr rallies too such that its yield drops.....the Fed will get what it wants (a slowdown/reccession). Anecdotally I'm in the process of buying a house and about 50% of the loan origination officers I spoke to about a month ago in the Tri-state area have lost their jobs

-

Earnings have already taken a hit.......but even more so if you do the correct thing intellectually & you inflation adjust them downwards...as I've said before as an example Apple's fiscal Q1 (Christmas Qtr)...showed a YoY fall in nominal earnings of about 13%......not great but in real terms its much worse.....it's more like a ~20% fall in earnings if you inflation adjust it to real terms. Inflation is the silent thief of portfolio returns......and so you've got to be careful not become a boiling frog as an investor in an inflationary environment. Finally the reality of historical inflation/Fed driven bear markets to be mindful of.......is that lots of the fall in equity prices happen usually only AFTER the Fed begins to cut rates...its both a function of the reality that the underlying economy is in trouble AND kind of peak pessimism.......I think there is feeling out there that once the Fed starts cutting we are just magically off to the races again in terms of equity prices.....the historical record would suggest equity markets have more to fall once the Fed begins to cut.

-

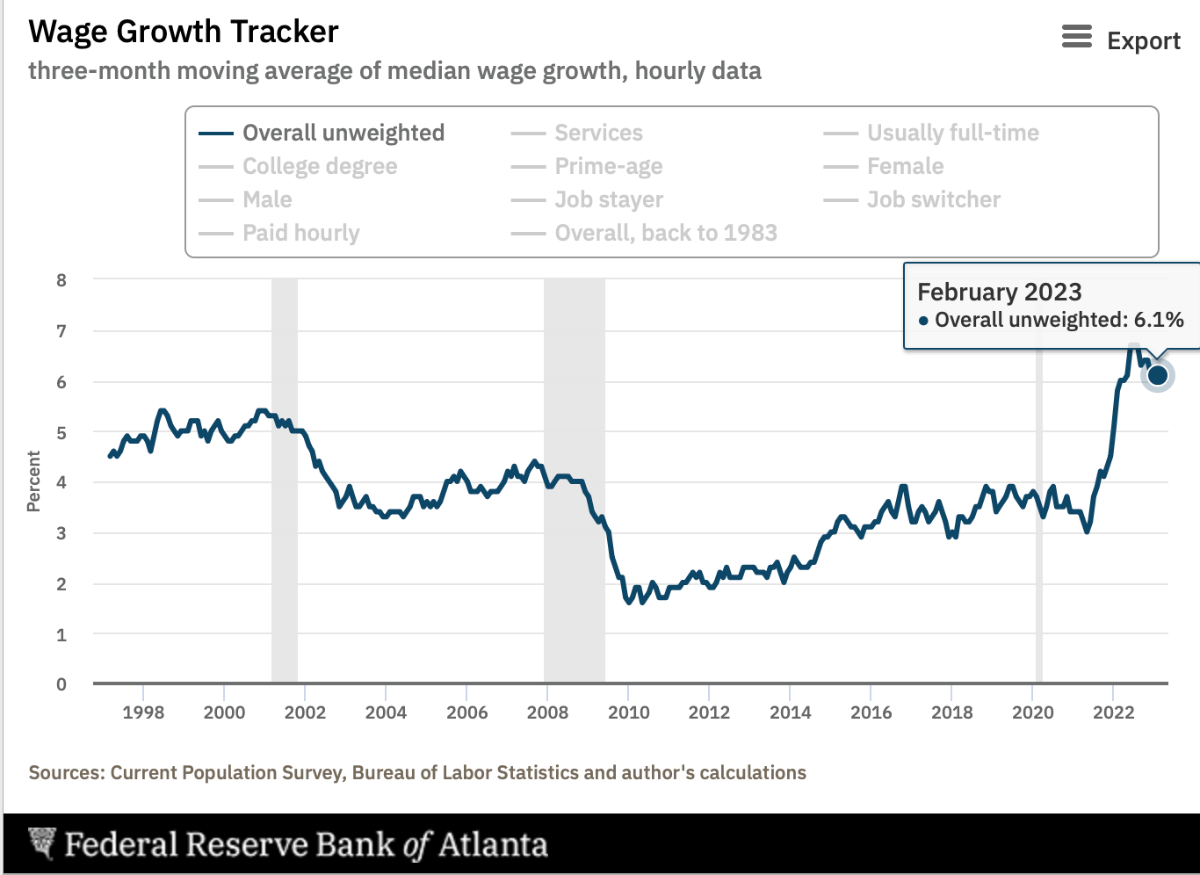

The problem is that there is inflation and it ain't going away any time soon as much as people wish it just would. It does goes away with deep underlying weakening of credit conditions, spending & unemployment (or a magical productivity boom).....the weakness let's be clear, is what the Fed is shooting for. My math - which I've covered ad nauseum, in an economy which looks like what we have now, is pointing towards ongoing & persistent/entrenched whatever way you want to put it ~mid-4's inflation (driven almost wholly by domestic services inflation). Please look at the below from the Atlanta Fed in terms of wage growth...which is a proxy for nominal spending growth...now think about this wage/spending growth in the context of poor productivity growth & ultra low unemployment. You CANNOT print 6% annualized wage increases in a sub-2% productivity economy and expect inflation to be anything other than above 4%. https://www.atlantafed.org/chcs/wage-growth-tracker As bad as mid-4's inflation is......think about how vulnerable that mid-4's inflation is to external forces out of the US's control.....like another energy shock. There is very little 'wiggle room' with an inflation number like that.....its unacceptably high. End of. Finally and as I've said before.......one should think of money (but more precisely 'money' which turns into spending on goods/services) as like shares outstanding issued against the quantum of goods and services being produced in your economy......issuing more 'shares/money' say via nominal wage increases or government 'handouts'....does nothing to change the REAL quantity of good & services.....it serves to change only the quoted price....in this case the quoted price of goods and services goes up.....we call that inflation! When its new shares in a company....and when the business fundamentals in that company haven't changed an iota.....we call that "dilution"....and the knowledgeable among us know that the price of our shares should go down.........a dilution event in company shares is akin to inflationary dilution in an economy that starts giving itself 6% nominal pay increases......and is only growing REAL output at an anemic level. Its like those AMC APE fools thinking more AMC shares being issued is gonna make them rich.....when in fact it's more REAL people going to the movies & buying popcorn that will do it.

-

100% agree (as a 41yr old! ) - when everybody and its mother has gone to one side of the boat in terms of predicting something in financial markets........generally speaking, the intelligent investor, should get on the other side. What is so widely predicted, through a process of Soros-esque reflexivity, rarely comes to pass as predicted.