Xerxes

-

Posts

5,689 -

Joined

-

Last visited

-

Days Won

9

Content Type

Profiles

Forums

Events

Everything posted by Xerxes

-

Movies and TV shows (general recommendation thread)

Xerxes replied to Liberty's topic in General Discussion

Only if JRR Tolkien knew that some day +$400 million would be spend on some obscure appendix attached to Lord of the Rings. It is not easy what Prime is doing. With Game of Thrones, HBO has access to the source talent, and the show has more of an adult theme to it. And that is what the market wants. I think Peter Jackson Hobbit’ 3rd movie left a bad taste and turned the whole thing into a joke. The third movie had no substance, beyond being an amalgamation of jokes. unclear how this will unfold in this day and age. The first episode was ok. -

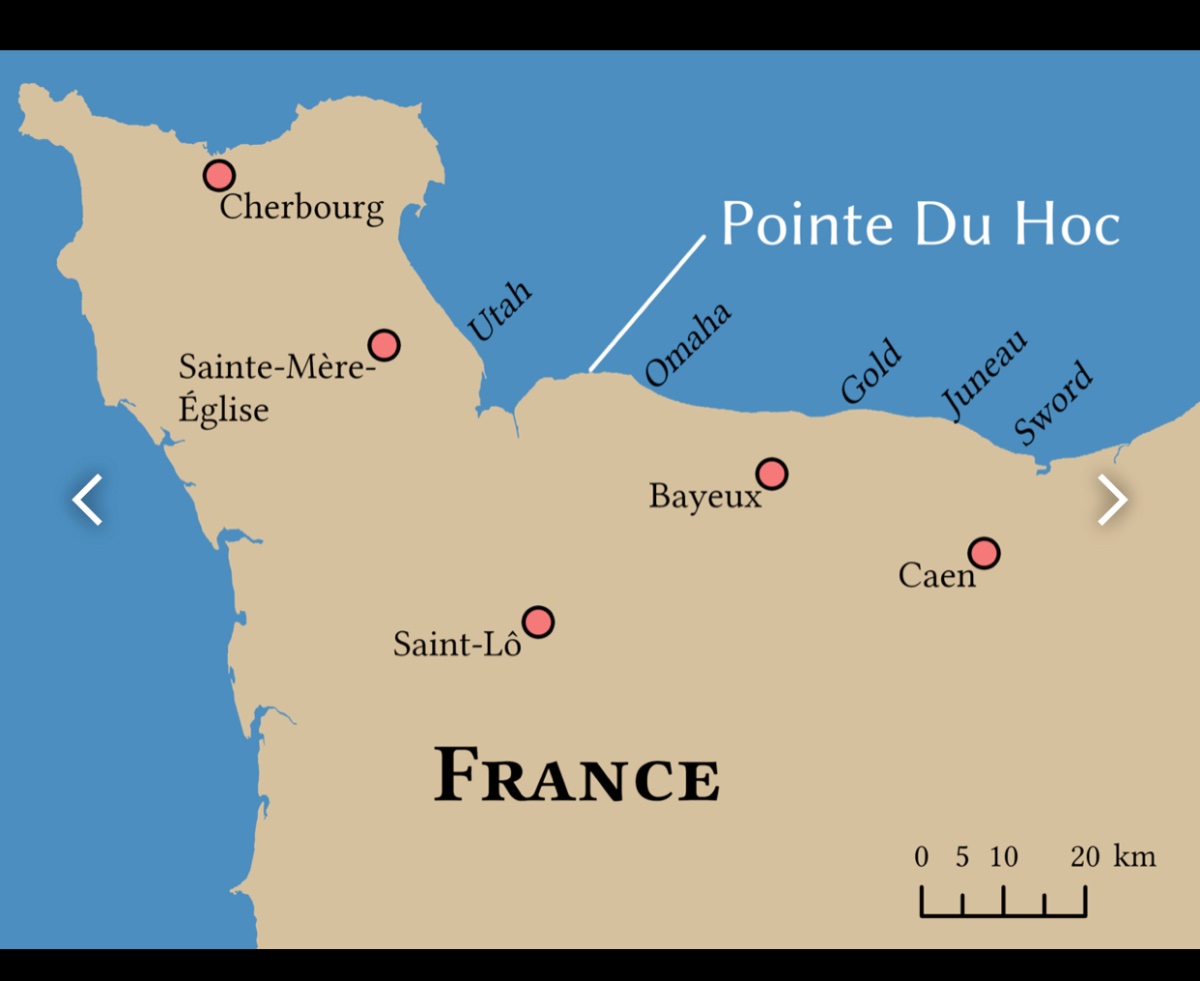

@maxthetrade i enjoyed also the “D-Day” beaches but like more than 15 years ago. There this one place I ll never forget, it was cliff overlooking some of the “beaches” on one side and “Utah beach” I think on the other side. It was packed with German battery installations. when I went to see it there were no howitzers, but their placement were there and massive cavities caused by the Allied bombardment. The massive bunkers are still there. For some reason, I remember the name Pointe du Chut but looks like it is called Pointe du Hoc. Even Call of Duty back in the day had a level where you had to climb those cliffs and disable those howitzers, only to discover that the Germans moved them more inland. https://en.m.wikipedia.org/wiki/Pointe_du_Hoc

-

I found this to be an illuminating and hilarious read

-

@Viking i think I have done my fifth day trip down to the Adirondacks (for hiking) this summer since border re-opened. will probably go to Vietnam, Cambodia and Thailand for Christmas but not for hiking or biking. Just normal tourist stuff.

-

The Economist on Occidental. Blomstran also alluded to the potential carbon capture business with OXY

-

was there last august. I personally enjoyed Garibaldi hike couple of hours drive from the city. If you are into hiking, highly recommend.

-

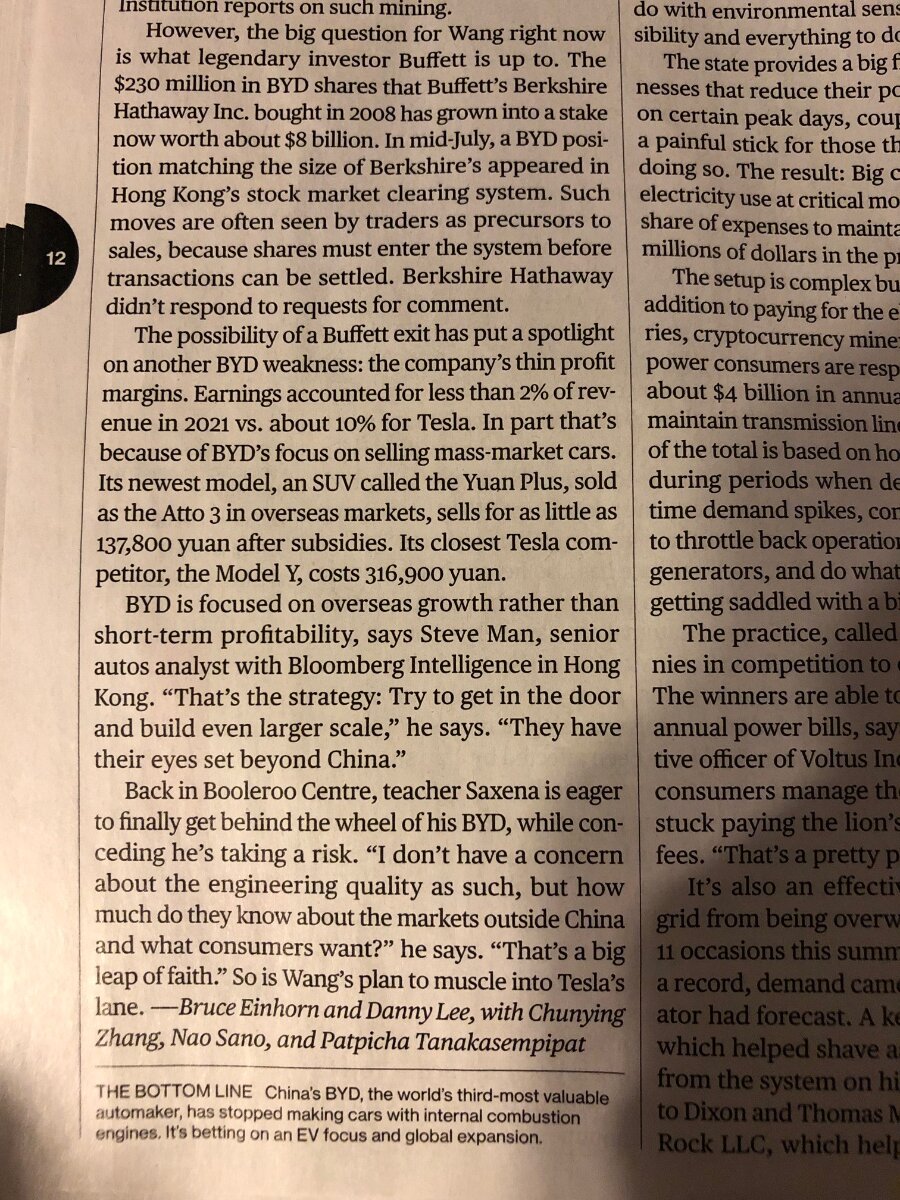

Apologies if already posted. About BYD

-

-

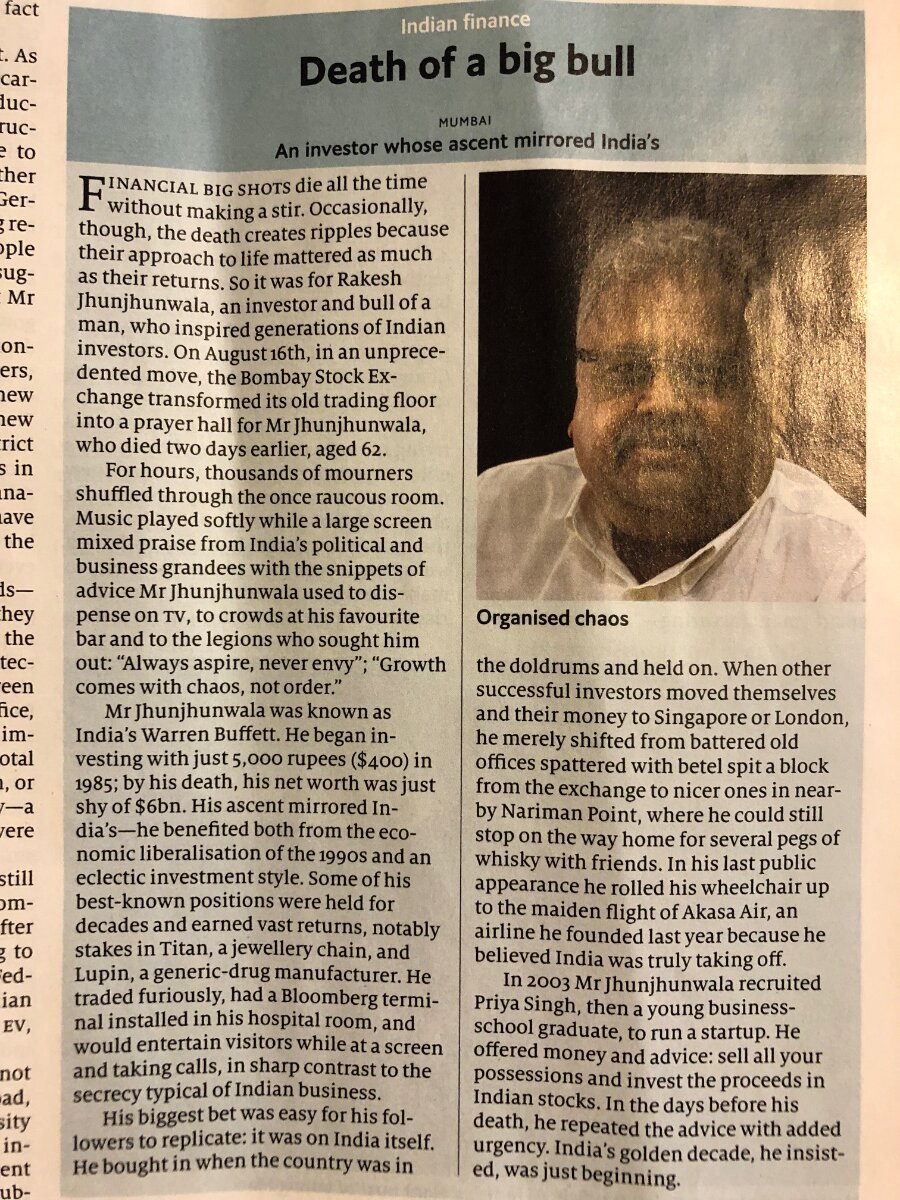

See attached piece about the passing of a titan in India. See the last paragraph. Conviction is inversely correlated to your geographical distance from the promise land. We are in North America so we see FIH as boring, boring, boring

-

I have done the volcano in Sicily, walking on ashes is not fun. Patagonia is however interesting.

-

Is there a major economical distinction between say (1) Allied World itself directly doing a buyback using its own equity to buy the minority (thereby making FFH full owner) and (2) FFH using its balance sheet to buyout the minority thereby making FFH full owner directly. One is a buyback at a subsidiary level while another is buyout at the group level.

-

Didnt Buffett already blew off CVX when he invested in the preferred in Occidental, (i.e. thereby giving Oxy firepower to take over Anadarko

-

Movies and TV shows (general recommendation thread)

Xerxes replied to Liberty's topic in General Discussion

House of Dragon was pretty good ! They really did a good job of showing who is who in the Taygaran familly & give full context in the span of one hour. Not an easy feat. -

Thanks @Viking @glider3834 Cheers

-

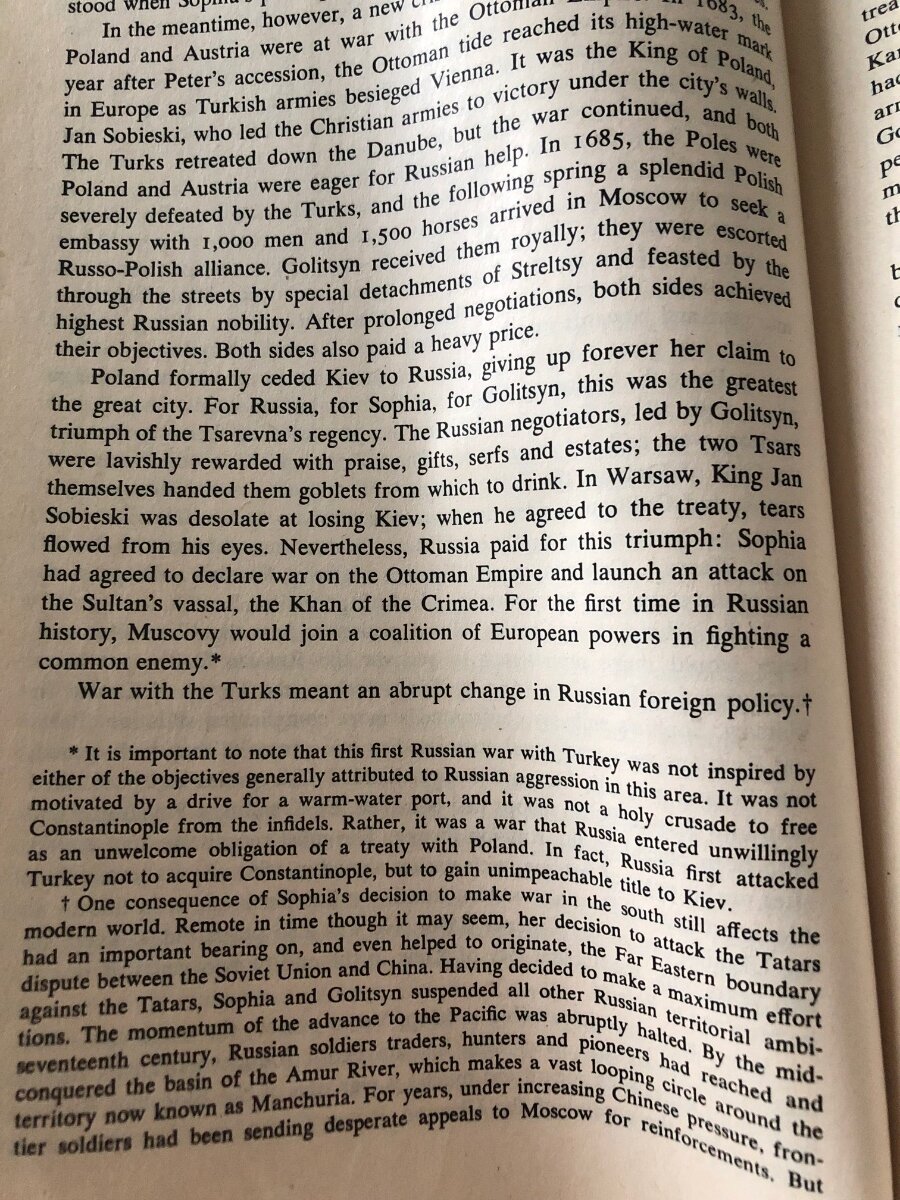

Game of Thrones : Warsaw, Moscow, Constantinople, Kiev and Crimea. Same locations as today but several hundred years ago.

-

Thanks Viking, I must have misunderstood your earlier comment, few pages back. I thought you were making an argument that over time FFH will start to be valued on an earning multiple (P/E) as the earning grows and not be based on book value (P/B). So my last comment was really an answer to that

-

The Last Kings of Shanghai: The Rival Jewish Dynasties That Helped Create Modern China: Kaufman, Jonathan: 9780735224438: Books - Amazon.ca First heard about this book, in the book recommendation section of The Economist. In fact there were two books but the second one i don t really remember, but will look for it. Just bought this paperbook and am a good one third through. I was always fascinated by Hong Kong, trade, opuim wars, China etc and more or less that region of the world and this is superb book that covers a lot of it. I highly recommend this book, it follows the story of two merchant famillies from Baghdad, who end up establishing themselves in east Asia and built their commercial enterprises. Their commercial dynaties end with the Communist take over in 1949. The one dark cloud in this otherwise successfull establishment (Sassons) was their wholesale participation in the opuim trade and the immense profits they made of it.

-

Great read: Vladimir Putin is in thrall to a distinctive brand of Russian fascism | The Economist

-

First time i see an article from the Western media that is so appropritly titled. The lingering collapse of the Soviet Union with its half a dozen frozen and not to frozen conflict. Well done Bloomberg. "Yet empires don’t die quickly: Their collapse, historian Serhii Plokhy wrote, is a “process rather than an event.” When a vast entity once held together by the iron discipline of the metropole gives way, don’t expect a new, stable status quo overnight." Russia's War in Ukraine Is How the Soviet Union Finally Ends - Bloomberg

-

@Viking Wouldn't an earning multiple be more appropriate for a business that does not have "lumpy" returns. And Fairfax's lumpy returns at that, happen to have a wide variety of "quality". Perhaps in a distant future it will be like that, but for now its valuation will remain anchored based on sum of the parts (i.e. BV). What do you think ?

-

The reality is Prem is not sharing the canvas he has in mind. It all makes sense to him and his team, I am sure, but no narrative is being communicated to the shareholder base. At a certain price you get the deep value guys in, that is all fine and well. But at a certain point to bring the long term buy-and-hold you need to build and clearly communicate a narrative. even in the shareholder letters you are being dragged into the rabbit hole of some back story, which while fine and educational does not tell the would be buy-and-hold crowd where that canvas is going. Contrast that to Markel simplicity when it comes to communication to shareholders. For clarity we are not talking the merit of one capital allocator to another. But the effectiveness of their communication. That being said, looks like Greg is jumping in with both feet !!! (Or soon)

-

Movies and TV shows (general recommendation thread)

Xerxes replied to Liberty's topic in General Discussion

One of my all time interesting spy story is the tale of Reilly. The TV shows was filmed in the early 1980s and covers the era around Russian revolution (before and after) and great power rivalry. really story and a fascinating character. https://en.m.wikipedia.org/wiki/Reilly,_Ace_of_Spies -

@Parsad hahha I don’t own ETFs or mutual funds. Haven’t bought any mutual fund in the 5+ years. Never owned any ETF if I remember correctly. I own only common stocks. And some insignificant crypto through WealthSimple

-

Does the fact that he is adding to Apple, an already large position, is an indication that he is implicitly thinking that the 10-year T-bonds have peaked.

-

I think secretly Prem Watsa likes the fact that FFH is an orphan stock. It keeps it undervalued while letting him complete his canvas. If he was all gung-ho about closing the gap, he would be cleaving off the parts he didnt like faster while communicating a clear narrative to the shareholder base and would be . His narrative has been in the past 5 years: "we made mistakes, we will re-earn your trust, stock is cheap" so pleading patience, while continuing empire building. I am ok with that, as the name is only one component of my portfolio and offers a very powerfull source of diversification of thoughts. He is my Anti-ARK and I like that,