Xerxes

-

Posts

5,689 -

Joined

-

Last visited

-

Days Won

9

Content Type

Profiles

Forums

Events

Everything posted by Xerxes

-

I always enjoy listening to the good Admiral whether on Bloomberg or elsewhere (though less interested to buy his fiction book). This is an incredible episode on his time in service as a sailor and a Navy admiral, the war in Ukraine, him being in the pentagon when 9-11 happened. Worth listening. There is a book he very highly recommended called “Chip wars” written by an SME. I also saw a review on it in The Economist. I think I would be buying.

-

I am listening to Biden speech live, it was very short one, and even I, more or less a liberal, consider this speech an absurdity and idiotic. The first & only question that was asked was about Lula and president election, no one bothered with question on oil

-

Movies and TV shows (general recommendation thread)

Xerxes replied to Liberty's topic in General Discussion

just saw this new trailer. I like the bit with Marchel Foch in his carriage (decades later destroyed by Hitler). I presume the overexcited German general is that of Ludendorff. Gone are the days where depicted German or French soldiers in war movies speak accented English. -

Indeed,

-

Nope, you have suspected incorrectly. Actually only the Caesar comment earlier upthread was to frame West, as it is the people flushed with excitement to "take on the Barbarians" that in turn embolden the fictional Caesar. The Kaiser comment was not to frame West but actually East. The ruler of the House Hohenzollroen at that point in time was not exactly looking for advice from mere mortals gazing upon the autocrat. Indeed, he had already toppled the mighty Otto von Bismark, so the opinion of the mortals was not exactly needed. Inertia had already put his path (and by extension that of the Reich) on a collision course with that of Great Britian. It is said that at the time, Germany was too big for Europe but too small for the world. I can say the samething about today's Russia. And as you have outlined, Putin would have given similiar speech. But the real hero in the story was the "balcony", whom by sheer coincidence became both a symbol of communism as much as symbol of the Prussian past history, thereby surviving throughout the decades (to this day) different regimes and ideaologies, until humans stopped being crazy. It took more than hundred years from 1914 till today --------------------------------------------------- On the comment about "but yet people flock to the U.S." and "we can't make people accept the US way of life ", you are definitly confusing two different things. - First and foremost, if people immigrate to the U.S. (or anywhere for that matter), they should accept that country's way of like. No excuses. I live in French-speaking province. You immigrate here be prepared to learn French. - But what you are mixing up, is the fact that a lot of people coming in are from the countries, where U.S. either choke the living hell out of them economically and/or has endlessly interfered with them. Guess what, stop being such an asshole on an international stage and perhaps some of those people would actually like to stay where they are. Maybe there would be less Algerians in France, if it was not a former colony of France. Maybe there would less Indian and Pakistani in U.K. if the sub-continent was not colony. I get that a Polish person moving to the U.S. speaks volume of the opportunities in the U.S. but i find it incredibley arrogant for Westerners (of which I am one) to think that they can go around do-whatever-the-f&ck they want to do around the world, and then complain why those people are moving to the West.

-

It is Sunday, i figured a light hearted historical post about a "balcony". This is Kaiser William, the last of his Wilhelmian line (unbeknownst to him at the time), declaring war in 1914 from Stadtschloss in Berlin. 4 years later, from the same balcony in Stadtschloss, the revolutionary led by Liebknecht give their speech in 1918, ushering the end of the Monarchy. By close of World War 2, the Stadtschloss has been largely destroyed by the Allies. With the Communist now in power in East Germany, they made plans for the demolition of the palace. Now interestingly the same balcony from which the Socalist German Republic was declared in 1918 was preserved while the rest of palace was demolished. The balcony was kept as a facade around which a new building was raised.I had a hard time finding a picture of Palast der Republik with the balcony facade. So not sure where exactly the "balcony" was preserved. From Wiki: "So solid was its construction that the dome and its entire mount remained intact even after the rest of the building fell to the ground.[14] Only one section was preserved, a portal from the balcony from which Karl Liebknecht had declared the German Socialist Republic. It was later added to the Council of State building (Staatsratsgebäude), with an altered cartouche, where it forms the main entrance. The empty space where the Stadtschloss had stood was named Marx-Engels-Platz and used as a parade ground." In turn this Communist building was demolished with the Unification of Germany. It was in 2003 that the decision was made to re-build the Stadtschloss along with its famed balcony. In Berlin, Rebuilding the Hohenzollern Stadtschloss May Have Become a Grand Blunder - The New York Times (nytimes.com)

-

War ! War ! Caesar, the People demand War. Glory to the Republic.

-

Personally i always thought Fairfax was a tad out of its league with this large % investment in the airport. For me, Fairfax is a financial investor, fist and foremost. And does not have the ready-deep pocket to be a strategic investor of a major infrastrucutre asset and to be able to inject new capital if needs be. That said, this could be a Westinghouse like situation, where FIH sells while either FFH or FIH ends up keeping a sliver in that JV entity that bought it from, which may even be a name like Brookfield.

-

Greg H on Q3 numbers for Raytheon and the war in Ukraine. I appreciate his steady hand and responses, not to mention the work that he does. Cramer on the other hand … like an overgrown child who just found where Ukraine is on the map and suddenly expert on the matter. He is a nice guy for sure, but I never cares too much for theatrics.

-

Molotov-Ribbentrop pact was between two extreme ideologies and not two kins. It was always going to blow up. Sino-Soviet relation (and now that of Russia) had some sour moment in the 1970s, but their current ideology is clearly a anti-Western one (and that front needs a long game and not a short-game which was the basis of the Ribbentrop-Molotov pact). That central anti-Western front unites them far more than their differences separates them. I think you guys are reading too much with WW2 analogies IMHO. If anything, perhaps there is some resemblance between the clandestine French-British alliance with Israel in the 1956 Suez war. Even that is a stretch.

-

@Spekulatius I would let the technocrats at US State Department run their cost-benefit model to gauge the NPV of attacking Russia proper. That aside, by all means, flood Ukraine with defensive weapons. If Kremlin has done the attack on the infrastructure much earlier in the war (as soon as they realized the fantasy of coup was not to be), West wouldn’t be crying foul play. LoL. ironically if Putin looses power, it won’t be because of taking Russia on an imperial adventure, but rather because he didn’t hit them hard enough on the right targets (conventionally).

-

Get over it people. Folks were blowing up each other infrastructure since the dawn of whatever. I get the emotional baggage specially with this conflict given who is the “enemy”, but there is no need to act like it is first time you see this (I.e. infrastructure getting destroyed affecting real people). That is what happens in war, last I checked. And I do check very often. Maybe this is first war that actually interests you (one does wonder why). If that is so, welcome to the real world. Reminds me of murder of George Floyd. No one cared how many black men died before or since. But Floyd’ murder was the one we chose to hang our hat on. Perhaps something to do with being in lockdown in Covid and needing to get it out. Who knows Analyze this conflict for related news, what it could become and share resources if you want help the victims. Keep the OMG reactions, “I cannot believe it” …. for some other forum. PS: sorry for my usual rambling. Not trying to offend anyone.

-

Prem speaking at Toronto Economic Forum. Something to do with Greece economic relations with Canada.

-

Not off topic and all info is great info. I will be listening to the last link. Thanks again

-

Which activities in life brings you the most fun?

Xerxes replied to Charlie's topic in General Discussion

Was doing crossfit before Covid. Stopped. That said, I do run/trail run minimum 40-50 km per week. Minimum 10 km going up/down on a local mountain per week. Small mountain but still, every week. bicycle a lot in summer. Did 450 km in Sicily over 7 days with +800 m elevation every day. Had 35-38 degree temperature first 3 days. I am seriously looking at Cotopaxi, the king of the volcanoes, and stuff like that. The highest I have been in 5,100 meters and need to push further. -

Thanks @Castanza. Though to the clip looks long. is the misconception that you are speaking of is about them not being a commercial venture ? i know as much about Blackwater as I know about Wagner Group, which is not much, other than they are “guns for hire” type of organization. In Wagner case, going further and actually acting as unofficial army of the State and its proxy. SS Waffen was not “guns for hire” nor a proxy to be used in distant hybrid wars. It was the very embodiment of the NSDAP party, it’s leader and its ideological spearhead.

-

I get a feeling even if at some point Ukraine formally recognize Crimea as de jure Russian territory as a concession to end the war, you still have Western countries that by spite will oppose that and not recognize that. Israel annexed the Golan Heights in early 1980s, after few decades of occupation after having getting hold of it in the 1967 war. The only country to formally recognize that was U.S. and only under Trump so some +30 years later, after Israel’s annexation and some 50 years after Israel conquered it.

-

I have not done any research but I would say (as an uninformed person) that Wagner Group reminds me more of Blackwater than SS Waffen. SS Waffen wasn’t created as a commercial entity to privatize war. Both Blackwater and Wagner Group were. SS Waffen was an instrument of the Party, and while may have started as Hitler’ bodyguards, it’s combat division worked side by side with Wehrmacht. There was a video interview, I saw years back where one of the heads of Blackwater was stupid enough to compare his company to the East India Company taking on the savages. The sheer cluelessness and arrogance of these people was too much for me.

-

@UK Khuruschev and Putin have a completely different verticals of power. The former might have schemed his way to the position of leadership like a worm, after the hardliners like Beria were made disappear but he largely worked to de-construct the myth of Stalin and with it his own vertical of power. Putin is the complete reverse as he has consolidated power. Now that being said I find western media full of references of “unhinged Putin” and “hoping for a palace coup”. Clearly, sabre rattling aside he has not gone up the escalation ladder by moving nuclear warheads out of storage for everyone to see. In fact, the danger is far less than 7 months ago IMO, notwithstanding their losses. To me that is a sign of rational actor who can do the math. A clearly misinformed and somewhat out of touch … but a rational actor. now of all folks wishing of a palace coup etc, who has actually done the deep dive to understand the consequences of another soul taking power who is even worse than him. In Stalin case, his death meant the end of the Korean War, but the Cold War raged on and the fact his successors had a softer touch was a blessing. I would not expect this in today’ Russia. in Putin case, right now he gets the media attention as he is the ultimate authority, but who are the hardcore nationalists behind him that are actually saying that Russia is taking it too easy on Ukraine and should go much harder at it. (Infrastructure etc)

-

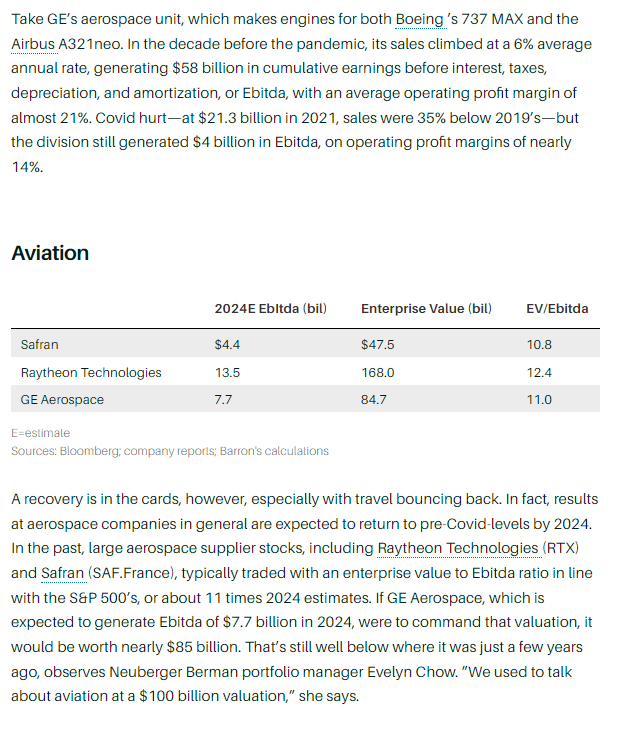

I dont follow Siemens Healthineers. As for SAFRAN, they and General Electric both have a mega business centered around the CFM/Leap engines. But i think we get a lot more optionality with Larry Culp and what he can do with new verticals within the GE Aerospace business than SAFRAN. Even with the CFM/Leap business, GE has more important IP with its design of the engine core (hot section) vs. SAFRAN ownership of the cold section (the outer section). I just think there is more to have with GE as a long term owner. Below is from Barron's. SAFRAN is not hugely cheap.

-

@dealraker Barrons had a recent breakdown of the three business that are going to be spun off. I posted it on the General Electric thread. Re-posted below. Personally, while i am interested in GE Aerospace (re-named GE Aviation) with Larry Culp at the helm, i dont want to deal with spin-offs in 2023 and 2024. I dont even believe they have shared yet even the proforma capital structure of three companies, since i last looked. I do know however that the remenants of the Baker Hughes stake and AerCap will be remain part of GE Aerospace until fully unwinded, which would probably mean matching liabilities to it. I am not expecting a UTC like spin off of Otis and Carrier.

-

"Never saw someone getting killed by a train that they saw coming" (paraphrase) That is how Jeffrey Currie from Goldman Sachs characterize his very bearish view on European natural gas prices, led by a planned collapse of industrial demand.

-

Thanks @dealraker I very much enjoyed reading your last few posts.

-

Very truth. Investment point of view: But I like to think like interest-rate cycle there is such thing as superhero-cycle. As that cycle eventually went from drought in the 90s and turned into a raging bull, someone would have made some dough on that portfolio of call options. Consumer point of view: But agreed that from a consumer point of view, it was better to have a major media company that was going to put its whole weight behind it and believed in it. If SONY bought everything, it is likely that they would have never made a large bet as Walt Disney made. It took guts to do what Walt Disney did. Who would have thought there could be so much value behind all of these secondary characters that could be mined and mined and mined. That value behind the secondary characters came into the money only because of major investment they had done in the first-tier characters.

-

"Nobody gives a sh*t about any of the other Marvel characters. Go back and do a deal for only Spider-Man." Sony Almost Bought All Marvel Character Rights in the 1990s (screenrant.com)