Xerxes

-

Posts

4,724 -

Joined

-

Last visited

-

Days Won

7

Content Type

Profiles

Forums

Events

Everything posted by Xerxes

-

pretty impressive that in Q1 and Q2, he added mightily to Starbucks on the dip. In contrast I added mightily to Starbucks before the 30% drop in early 2024. opps

-

Movies and TV shows (general recommendation thread)

Xerxes replied to Liberty's topic in General Discussion

Gladiator 2 is one of the worse movie ever made. Bad script. Bad acting. Useless nods to the first movie. Everyone know everyone 12 years later. my god. What happens to Ridley Scott. How the almighty has fallen. Just all around bad. Hollywood at its worse. And in the middle of it all, Denzel Washington with his Chicago accent. -

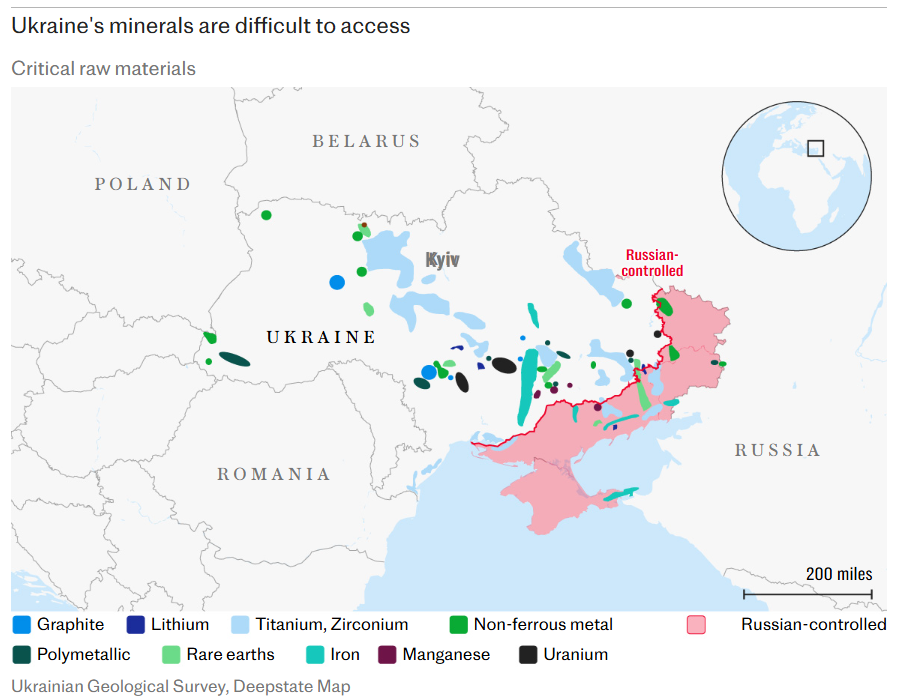

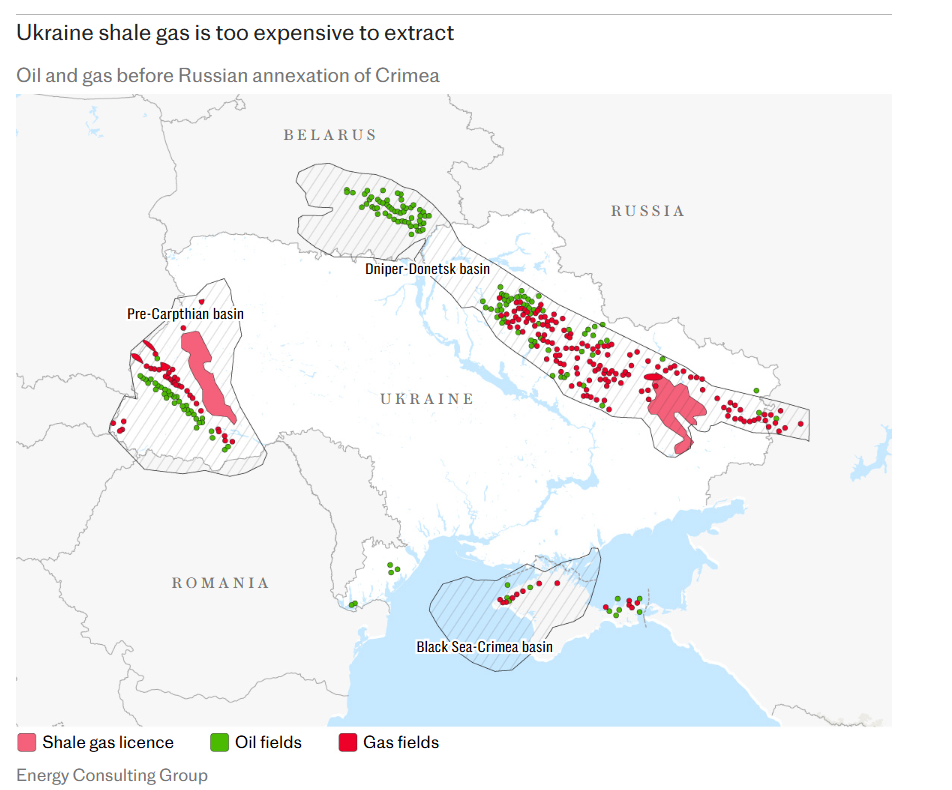

Revealed: Trump's confidential plan to put Ukraine in a stranglehold Donald Trump’s demand for a $500bn (£400bn) “payback” from Ukraine goes far beyond US control over the country’s critical minerals. It covers everything from ports and infrastructure to oil and gas, and the larger resource base of the country. The terms of the contract that landed at Volodymyr Zelensky’s office a week ago amount to the US economic colonisation of Ukraine, in legal perpetuity. It implies a burden of reparations that cannot possibly be achieved. The document has caused consternation and panic in Kyiv. The Telegraph has obtained a draft of the pre-decisional contract, marked “Privileged & Confidential’ and dated Feb 7 2025. It states that the US and Ukraine should form a joint investment fund to ensure that “hostile parties to the conflict do not benefit from the reconstruction of Ukraine”. The agreement covers the “economic value associated with resources of Ukraine”, including “mineral resources, oil and gas resources, ports, other infrastructure (as agreed)”, leaving it unclear what else might be encompassed. “This agreement shall be governed by New York law, without regard to conflict of laws principles,” it states. The US will take 50pc of recurring revenues received by Ukraine from extraction of resources, and 50pc of the financial value of “all new licences issued to third parties” for the future monetisation of resources. There will be “a lien on such revenues” in favour of the US. “That clause means ‘pay us first, and then feed your children’,” said one source close to the negotiations. It states that “for all future licences, the US will have a right of first refusal for the purchase of exportable minerals”. Washington will have sovereign immunity and acquire near total control over most of Ukraine’s commodity and resource economy. The fund “shall have the exclusive right to establish the method, selection criteria, terms, and conditions” of all future licences and projects. And so forth, in this vein. It seems to have been written by private lawyers, not the US departments of state or commerce. President Zelensky himself proposed the idea of giving the US a direct stake in Ukraine’s rare earth elements and critical minerals on a visit to Trump Tower in September, hoping to smooth the way for continued arms deliveries. Volodymyr Zelensky proposed a US stake in Ukraine’s minerals production when he met Donald Trump in September He calculated that it would lead to US companies setting operations on the ground, creating a political tripwire that would deter Vladimir Putin from attacking again. Some mineral basins are near the front line in eastern Ukraine, or in Russian-occupied areas. He has played up the dangers of letting strategic reserves of titanium, tungsten, uranium, graphite and rare earths fall into Russian hands. “If we are talking about a deal, then let’s do a deal, we are only for it,” he said. He probably did not expect to be confronted with terms normally imposed on aggressor states defeated in war. They are worse than the financial penalties imposed on Germany and Japan after their defeat in 1945. Both countries were ultimately net recipients of funds from the victorious allies. A new Versailles If this draft were accepted, Trump’s demands would amount to a higher share of Ukrainian GDP than reparations imposed on Germany at the Versailles Treaty, later whittled down at the London Conference in 1921, and by the Dawes Plan in 1924. At the same time, he seems willing to let Russia off the hook entirely. Donald Trump told Fox News that Ukraine had “essentially agreed” to hand over $500bn. “They have tremendously valuable land in terms of rare earths, in terms of oil and gas, in terms of other things,” he said. He warned that Ukraine would be handed to Putin on a plate if it rejected the terms. “They may make a deal. They may not make a deal. They may be Russian someday, or they may not be Russian someday. But I want this money back,” he said. Trump said the US had spent $300bn on the war so far, adding that it would be “stupid” to hand over any more. In fact the five packages agreed by Congress total $175bn, of which $70bn was spent in the US on weapons production. Some of it is in the form of humanitarian grants, but much of it is lend-lease money that must be repaid. Republican Senator Lindsey Graham suggested at the Munich Security Conference over the weekend that Trump’s demand was a clever ploy to bolster declining popular support for the Ukrainian cause. “He can go to the American people and say, ‘Ukraine is not a burden, it is a benefit,’” he said. Sen Graham told the Europeans to root hard for the idea because it locks Washington into defending a future settlement. “If we sign this minerals agreement, Putin is screwed, because Trump will defend the deal,” he said. Ukrainian officials had to tiptoe though this minefield at the Munich forum, trying to smile gamely and talking up hopes of a resource deal while at the same pleading that the current text breaches Ukrainian law and needs redrafting. Well, indeed. Talk of Ukraine’s resource wealth has become surreal. A figure of $26 trillion is being cast around for combined mineral reserves and hydrocarbons reserves. The sums are make-believe. Ukraine probably has the largest lithium basin in Europe. But lithium prices have crashed by 88pc since the bubble burst in 2022. Large reserves are being discovered all over the world. The McDermitt Caldera in Nevada is thought to be the biggest lithium deposit on the planet with 40m metric tonnes, alone enough to catapult the US ahead of China. The Thacker Pass project will be operational by next year. The value of lithium is in the processing and the downstream industries. Unprocessed rock deposits sitting in Ukraine are all but useless to the US. It is a similar story for rare earths. They are not rare. Mining companies in the US abandoned the business in the 1990s because profit margins were then too low. The US government was asleep at the wheel and let this happen, waking up to discover that China has acquired a strategic stranglehold over supplies of critical elements needed for hi-tech and advanced weapons. That problem is being resolved. Ukraine has cobalt but most EV batteries now use lithium ferrous phosphate and no longer need cobalt. Furthermore, sodium-ion and sulphur-based batteries will limit the future demand growth for lithium. So will recycling. One could go on. The mineral scarcity story is wildly exaggerated. As for Ukraine’s shale gas, a) some of the Yuzivska field lies under Putin control, and b) the western Carpathian reserves are in complex geology with high drilling costs, causing Chevron to pull out, just as it did in Poland. Ukraine has more potential as an exporter of electricity to Europe from renewables and nuclear expansion, but that is not what is on Donald Trump’s mind. The second violation of Ukraine Ukraine cannot possibly meet his $500bn demand in any meaningful timeframe, leaving aside the larger matter of whether it is honourable to treat a victim nation in this fashion after it has held the battle line for the liberal democracies at enormous sacrifice for three years. Who really has a debt to whom, may one ask? “My style of dealmaking is quite simple and straightforward,” says Trump in his book The Art of the Deal. “I aim very high, and then I just keep pushing and pushing and pushing to get what I’m after.” In genuine commerce the other side can usually walk away. Trump’s demand is iron-fist coercion by a neo-imperial power against a weaker nation with its back to the wall, and all for a commodity bonanza that exists chiefly in Trump’s head. “Often-times the best deal you make is the deal you don’t make,” said Trump, offering another of his pearls. Zelensky does not have that luxury. He has to pick between the military violation of Ukraine by Putin, and the economic violation of Ukraine by his own ally.

-

The Enemy [I mean, Zelenskyy] gets a Vote too.

-

Is this a political thread in disguise we do already have a DOGE thread, a Tesla thread etc even a SpaceX thread

-

imagine if Putin comes back with a counter offer: I will give 60% control to the U.S. of rare earth in the Donbas (occupied by Russia or not) if U.S. formally recognize Russia’ annexation and halt all aides what a world

-

Fantastic book and long. So it is my long-read book in the background on slow burn. Read that chapter that I posted just this past week. Timely I think with what will be happening (or not happening) in the Pentagon.

-

so that there is no confusion, comment was about capital return (dividend + buyback), and not valuation gain as a result of more volume of business and margins

-

cheers.

-

@SafetyinNumbers Please ignore my question; i realized there is a thread on it

-

Why say Strathcona Resources vs. Athabasca. They both have similar market cap and have a strong capital return policy. I know neither very well, just wondering your take

-

Barrick Gold talked about the need to redomicile to U.S. probably accelerated under Trump. There was no mention of this on conference call, and we know it is “been there done that” for FFH, but do folks here see a risk that the operation business environment would become such that FFH would need to redomcile out of necessity, for tax or other reasons.

-

The year : 1902 Reformer: Lord Fisher, First Sea Lord Target: a bloated Royal Navy By 1907, the Navy was costing £31 million pound. About £5 million pound less when the reform commenced in 1902. All that even as the fighting capacity of the Navy increased, both through introduction of new hardware, re-allocation of resources, elimination of fiefdoms and removing old ships which till then was used to “show the flag”. I think Lord Fisher would have been a good portfolio manager.

-

for what is worth from the conference call: Gautam Khanna Great. And then my last one, just on the new administration and how is TransDigm kind of working constructively with them and your thoughts on DOGE, and I'll just leave it open ended, but... Kevin Stein That's a great question. I anticipated this earlier, I think, in the Q&A. DOGE is -- it's a great opportunity for the U.S. to improve and streamline what they're doing, specifically with government DoD, DLA procurement. We think this is a really good thing. We've been engaging with the DoD over the past several years and have suggested a number of improved forecasting, inventory management and improved buying practices that would save the government money and save us time and energy in production. So we invite all inquiry and assistance. I've met with some of the DOGE folks in D.C. It's important to remember that TransDigm is a very small supplier. I think we're 0.3% of the DLA budgets and this amounts to less than 1% or somewhere around 1% of our revenue, are these types of products that would fall under a concern of DOGE. We see this only as an opportunity for TransDigm, the government, the DoD to improve what we're doing together. So we warrant any and all inquiries and work together to come up with a stronger solution in the future. So that's really where we're at. It's a small part of our business is supplying spare parts to the government. The bulk of what we do is either falls under TINA today, which is fully cost disclosed? Or is commercial of the type or competitive that's the bulk of our business falls under those 3 categories. So we invite the work that we need to do together to improve how we work together with the government. So that's, I guess, our answer.

-

In 2018 AGM, Prem has said and I quote (based on memory) "we want FIH to be as far as possible from FFH" A comparison was made (again from memory) to self-sustaining ships going on a voyage of discovery, while not putting mainland to risk.

-

There is also BAE that straddles both sides of Atlantic. I agree w/ you that the return from the European names will be poor. Referring strictly to their willingness to return cash in a politically charged defense environement. If you are looking for additional material, I think good source of material for A&D is the Aviation Week; i have been getting a print copy for almost +10 years now. A good weekly podast is the following: Defense & Aerospace Report Podcast [Feb 09, ’25 Business Report] - Defense & Aerospace Report Comes out every weekend and is the first thing I listen to Monday morning. More : (these are all recurring weekly podcasts) DEFAERO Strategy Series [Feb 11, 25] Bendett & Eugene Rumer on Russia, Ukraine On-going Conflict - Defense & Aerospace Report DEFAERO Daily Pod [Feb 10, 25] Trump Week Three & Byron Callan’s Week Ahead - Defense & Aerospace Report

-

yeah. IT ain’t sexy enough for me. And the prevailing view on land system is not looking bright, even with the largest land war in Europe. Gulfstream though is a gem. what is striking for me about GD is that since it’s corporate transformation in the 90s and very early 2000s, (I.e exiting aerospace and coming back to it via Gulfstream purchase) has not reshaped its portfolio, except for the bolt-on w/ IT in the 2010s, in contrast to the rest of cohort.

-

@Spekulatius @Hektor you gents do know about Electric Boat, don’t you ? no I don’t mean a boat that is electric. But rather the name of shipyard business owned by General Dynamics for decades now.

-

Nice. A blend of fact and fiction when it comes to Israel. Israel DID have nuclear weapons in 1973 and used it as BLACKMAIL to get critical weapon delivery from Nixon and Kissinger. Now I would have done the same thing if I were them. Nothing wrong with that. But let us not assume that Israel is too noble to blackmail. And to this day, we don’t know if Israel attacks USS Liberty on purpose or not in 1967. What was that for ? It is thick with controversies. Hell, an Iraqi mistake with USS Stark in the mid-1980s came out cleaner than that. Back on Ukraine, it needs to take the loss so that it can grow to be the fortress that needs to be. After this round 2, Ukraine will have the most advanced, combat-ready military force on the continent. That is an asset. Yes no one can trust Putin with any settlement. But you can trust that Trump doesn’t want another 2021 Kabul situation. And you can trust that once there is a ceasefire there would a reckoning in Moscow to take stock of what was accomplished. That will keep them busy. The question is Zelenskyy the man to lead Ukraine toward that settlement.

-

because banks are “financial services” companies and they are providing financial services to a corporate client, who has decided to take a position on itself and needs a product that fits the needs. Ideally banks makes their dough via fees And not taking a directional position for or against the corporate client. I.e so they would have been long the FFH shares to balance the TRS, if the risk officer was clear minded

-

We don’t know. He may be wanting something somewhere else. Not everything is and revolves about Ukraine. Russia clearly cares about Ukraine far more than America cares. ex: no trouble from Kremlin when (not if) Greenland is annexed etc. That is the whole idea as to why great power want to talk to each other directly. Quid pro quo. But like John Bolton said on CNN, in Russia they are probably drinking vodka directly from the bottle after yesterday announcement.

-

Easy answer: Rhienemetall, SAAB, and Thales etc US defense contractors are primarily long-cycle defense business. Driven by long term security needs. And not directly influenced by ebbs and flow of War in Ukraine. If anything the war Ukraine has shown the reliability of Western product portfolio and offering in a real setting. Just as 1991 Gulf War demonstrated Western weaponry in a real setting and opened up the market for Gulf nations to place POs for Abrams, Hummers, Patriots etc. even though Saddam was defanged.

-

Hard cold truth (mostly anyways)

-

Not exactly. Your knowledge related to FFH and investment in general have been compounding since 1998 by holding FFH since. Surely that unique knowledge and viewpoint cannot be squeezed into four years for those that ticked high CAGR by buying four years ago for the same overall financial return.

-

in the 90s when I was a teenager, my dad took me there and helped me open an account. i stayed ever since. on a more practical matter, they always reverse charges when i asked them. that said i never used RY for my mortgage. The rates are always too high .., and we always the underdog banks like National Bank and/or BMO coming with good mortgage product undercutting RY and/or TD.