Castanza

-

Posts

5,064 -

Joined

-

Last visited

-

Days Won

8

Content Type

Profiles

Forums

Events

Everything posted by Castanza

-

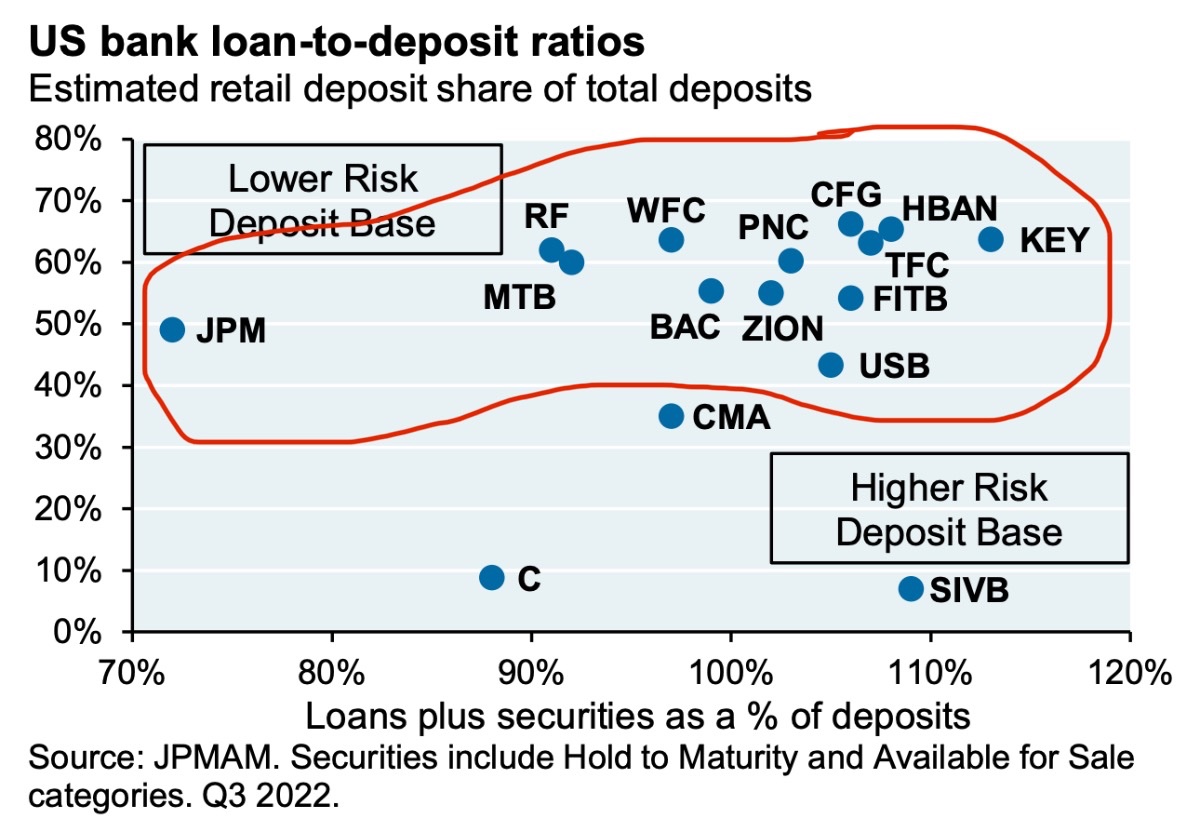

Personally I don't know enough about the regionals to jump in. I think buying KRE and then some of the big boys is the less risky way to play this.

-

Truist CEO retired....today....

-

TFC, USB, BAC Call KRE 6/20/25 $50 at 5.50 Call TFC 1/17/25 $40 at 3.70

-

Hmm the more I think about this situation, the less I like it. As @changegonnacome said the metrics and guidance for all these banks is going to be jacked if there is any serious movement of capital. Index play on regionals might be the safest bet should it get low enough. Maybe a basket of the big boys….something tells me that opportunity might not be as sweet as we think. Either way, it will be interesting to see what happens! The Bank of Castanza does not need any runs of its own.

-

Opportunity might be gone pre-market

-

Guidance to New Members of the FORUM!!

Castanza replied to [email protected]'s topic in General Discussion

1.) Actionable is a personal choice. Do your own DD. Nobody’s suggestions should be considered financial advice. 2.) “Investment ideas” is for stock specific discussion. You can search for companies there. General Discussion is for anything else. Usually market or finance related but not alway. 3.) Historical info is best found in individual equity discussions. No great way to search, but you can page back to the timeframe you want to see. Welcome -

You’d have to dig into the holdings to see what they are and if they hedged. But I believe that is the general consensus. For the situation on hand it seems like deposits stickiness, size and diversity are more important.

-

A basket of long dated call options in some of these could be interesting

-

How is this even responsible to say? There is no guarantee companies will do that. Fear stoking at its finest.

-

From my nosebleed seats, what I never understand about interest rate hikes is how everyone says it will take 12-18 months before we see the effects. Yet they continue to raise rates every quarter. Everything is just modeled out with textbook equations and they just hope that matches up with reality on the outcome side? Seems like a fools errand. Blunt tools indeed. It’s like baking a cake for 40 min and doing the toothpick test at 10 min, seeing the results and then upping the temp because it’s not done yet….Should you be surprised when the cake ends up burnt?

-

Not sure on the breakdown of the VC pool but SIVB was in both sectors; and I’m sure GOOGL and META would run ads for anyone willing to pay. To your payroll cuts….I guess that’s possible? Don’t really know . Either way VC funding was expected to decline and I’m sure both companies were acutely aware of the cash flow provided by them. Could be some short term pullbacks as they adjust and the numbers trickle through the next few quarters. More definitive numbers on ad spend would be great. I think someone posted a breakdown/estimation on one of the GOOGL or META threads a while ago.

-

Anyone else wondering how this will shake out for GOOGL and META in the ad department? Startups have been spending about half their cash on advertising between the two for some time. Many as high as 50% of cash. You had what 445B VC funding in 2022? Say 30% of that goes to ad spend so 133b and 50/50 split GOOGL and META....just napkin math without the nuance, but not immaterial when you consider GOOGL had 283b in ad rev 2022.

-

Liquor

-

On the Go, but here are a few topics highlighted. - Russia has largely failed and will never hold Ukraine - Russia is short on munitions and using most of what they make within a month. - Russia looks weak but can still make calculated pushes and capture territory. - Both armies are very different animals than when the war started. Both have greatly benefited from conscription/mobilization of additional forces. - Ukraine unlikely to re-capture major cities or hot spot locations (likely to lose Bakhmut) - War in general is at a relative stalemate - Ukraine wants more funding but US has 11B left in the tank. F16 don't make sense as 12 would eat that budget up. US production is bottlenecked and everything we give Ukraine is being taken away from current US missions. The "extra supply" is a myth. US debating future funding of resources based on our own risks as we deplete OUR supply. The benefit of a dozen F-16 to Ukraine would be negligible. - Some of the munitions very useful to Ukraine are not necessarily something we will continue to produce because they are not strategic to the US (speaker listed some shells and other munitions). US is Air dependent not Artillery. - Russia's nuclear declaration of use for Nuclear weapons is a much lower threshold than NATO nations. Putin is still irrational and the same people who said Russia wouldn't invade are the same ones saying Putin will never push that button. - Should the US supply cluster like munitions (cant remember specific name)? Maybe because they are already being used. - Ukraine will have to spend billions post war to de-mine the nation. It's going to be a massive problem that will hinder rebuilding. - Germany re-thinking the shipment of Leopard tanks as Ukraine may not be able to maintain them.

-

https://podcasts.apple.com/us/podcast/backing-ukraine-against-russia-with-colin-kahl-and/id682478916?i=1000601391447 Latest episode is worth a listen if you haven't. Covers the majority of the stuff you guys have been squabbling about the past few days.

-

I'm not lol added a bit more this morning

-

SNC (SNCAF) - new position

-

You’ll find this culture in all of the logistics related businesses. Getting the product moved at all costs takes precedent. This makes me think back to when I was working my way through college at UPS. Two stories: Was finishing up the day with some residential delivery and my brakes went out while in a development. Was driving this old piece of junk p800. Called in to the center and the manager said to just try and finish the day but use the e-brake (hand brake) to finish the day. They were more worried about getting the pickup pieces back to the center before the Louisville freight left. Was driving back to the center doing 55 on an Ohio country highway. Had a rear re-tread peel off the tire. Picture 2 feet of rubber slapping around attached to the tire with internal cable. Called in and they said limp it back lol…so I was a little more seasoned and disgruntled at this point. Said “ok boss”. Made sure no cars were around, pulled out and got it up to 25. The rubber flap slapped up under the wheel well, snapped off the gas tank fill tube and absolutely shredded the side of the package car. Pulled over with a smirk on my face, called it and again and said “you’re gonna need a tow truck”. They learned to send out a mechanic to change the tire next time. Moral of the story…I’d be willing to bet there are ticking time bombs like this all throughout the industry. Shit rolls downhill and as employees and management catch heat from up the chain you eventually end up with the straw that broke the camels back. Hence the Ohio train issue.

-

Thanks for sharing, any good books out there on the family?

-

Always though Kluber Lubrication would be a good addition to Lubrizols portfolio.

-

Atlas Copco (Stockholm Exchange) Stumbled upon this company from a podcast. Sounds like something right up WB alley. Large industrial conglomerate that manufactures compressors and vacuum pumps, 50B mktcap, b2b focused, family run for 150 years, shown resilience and has navigated many tough markets.

-

Who Do You Follow and What Are their Circle of Competence?

Castanza replied to BG2008's topic in General Discussion

If you find yourself in BFE PA this Nov the Saturday following Thanksgiving I'll make sure you go home with a cooler full of venison. RE @BG2008 @Gregmal @thepupil @Dinar Macro @wabuffo @changegonnacome @Viking @SharperDingaan General Ideas @longterminvestor @gfp @kab60 @KJP @Spekulatius @LearningMachine @Ross812 @Lance (haven't seen post in a while) @Saluki just to name a few. All for generally different reasons. I don't know if Lance ever posted anything other than "What Are You Buying" positions. But every time I looked at them I was like "Damn, that is cheap." Learning Machine is a 10k animal. Spek a no bullshit common sense approach. -

Who Do You Follow and What Are their Circle of Competence?

Castanza replied to BG2008's topic in General Discussion

@Castanzafor shit takes and money losing propositions Far too many to name. This site is hands down the best collection of investors I have been able to find on the web. Learned a lot from others on here. -

$LW tracker position Anyone else look at this? Potato company that specializes in frozen French fries. Operations in the US, Argentina (plant being built) and China. They supply big shops like MCD (~10% of Rev), as well as other chains and restaurants. Contracts negotiated every 3 years. Covid disruption has yet to normalize but they have been able to pass on the majority of this increase in COGS without issue. Global Margins is the key category and those margins have not yet come back to pre-covid levels. This could be close fully priced here at $100. But there could be upside if margins come back to normal levels and the contracts are re-negotiated at higher prices. Andrew Walker had a podcast on it and in the Global segment there seems to be room to do this. Not sure management has the appetite to do so. Being that fries are one of the highest margin food products for restaurants I can see this happening. Recession proof too. Management does have incentives at $140 and $212 share price so it's possible <--- but not necessarily a bet I'd make just on that alone. They do seem to have a new focus on dividend payout and share repurchase. They are also open to more aggressive M&A which would help reduce COGS pending locations they can secure. The Play TLDR: - Margins normalize around 25% (pre covid) - Global Margins come back as supply chain issues ease, crop production comes back to normal and sales volume comes back. Management has said they are trending up. - Management is incentivized to grow share price with targets at 140 and 212 - Contracts renegotiated and pricing power is flexed. (MCD pays like .11-.13 per pound of fries) Could be fairly valued here but worth a spot on the watchlist regardless imo. Low leverage smooth operating business with a very healthy market share, M&A hungry management in specific markets (EU & Africa) with a new focus on div and buybacks.

-

PCYO, BRKb