Saluki

-

Posts

1,870 -

Joined

-

Last visited

-

Days Won

3

Content Type

Profiles

Forums

Events

Everything posted by Saluki

-

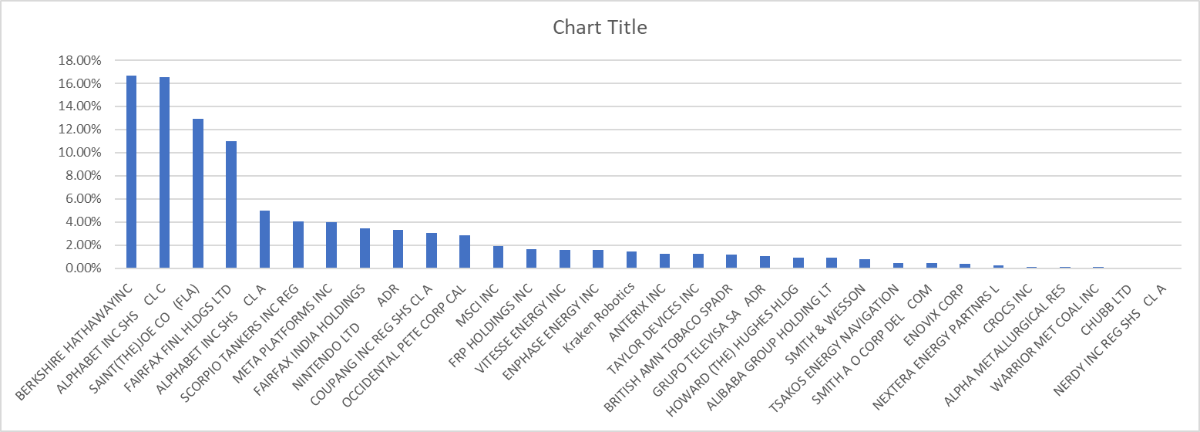

No, I exported this data from my Merrill account, which won't let me buy Kraken, so I looked at the position size in my other brokerage account and typed it in the excel sheet by hand. In that other account JOE is probably another 1.5% also, but otherwise it's accurate.

-

Not much change in the larger positions, but new small/mid position in MSCI, FRPH, KRKNF, and ENPH. The right tail is usually things I buy a few shares in while I study them and then add to them or replace them with something else that looks interesting and needs more research.

-

I was looking at this a few days ago, unfortunately Merrill won't let me trade it The CEO doesn't seem interested in listening to the activist who wants them to sell off the stakes in other companies and do a buyback or increase the dividend to close the gap between book value and market value. Unlocking that value will depend on how serious the Japanese government is about undoing these interlocking ownership structures (You own shares in my company, I own shares in your company and we sit on each other's boards, drink saki and vote against any minority shareholders that try to tell us we should run a company for the owners, not the management).

-

Someone who knows about my interest in sea drones sent me this: He created Oculus headsets as a teenager. Now he makes AI weapons for Ukraine : NPR I assumed the guy on the Silicon Valley TV show was completely made up, but Palmer Luckey is Keenan Feldspar! He seems like an interesting guy and politics aside I appreciate that he doesn't take himself too seriously. Besides the Hawaiian shirts, I've seen a few interviews when someone is asking a question and they say that he left Facebook, and he is quick to correct them. "I didn't leave Facebook, they fired me. Then they lied about why they fired me, so I sued them and won $100 million." So nice to hear the truth unsugarcoated rather than "I wanted to pursue other opportunities" or "I felt I did all I could there and it was time to move on" or "I wanted to spend time with my family."

-

Trimmed some VTS. No particularly reason. I bought it cheap and it's been over a year, and it's paying a nice dividend, but there are cheaper things out there with growth attached, not just harvesting existing opportunities. I continue to trim STNG and buy Tsakos to keep my product tanker position but at a better relative valuation.

-

I don't think we hit the top until we see stories like this again: Stories like this are why CNBC and other financial media are a joke. No fact checking whatsoever. I would bet money that his "investors" are his parents. I was curious when I saw this in my YouTube so I wondered "where are they now." Speaking of worthless journalism, check out this recent follow up from Money. First Generation Investors: Changemakers 2023 | Money Mattox, named “Most Likely to Revolutionize Wall Street” by Goldman Sachs as a teen himself, launched the hedge fund North Tabor Capital from his bedroom in suburban New Jersey when he was still in braces. Did no one call Goldman Sachs to confirm this? I doubt they bestowed that title on anyone, but if you're a journalist and someone makes a ridiculous claim, maybe you should fact check it. Especially since, according to Value Walk, he was operating his fund with convicted criminal Jacob Wohl, who also was on the news for starting a hedge fund in high school until he was shut down by authorities. Is Teen Hedge Fund Manager Cole Mattox On Jacob Wohl's Path? (valuewalk.com) I remember stories about people in their 20s making millions running crypto funds for others. It was right before BTC got cut in half. So keep an eye out for stories like this.

-

When asked for a method for finding good companies to invest in as a small investor, he mentioned thumbing through all the companies in the Moody's manuals when he was starting out. When the reporter said that there were thousands of companies there, he said "start with the As." I keep coming across interesting companies haphazardly and most of them don't make the cut. But in an effort to systematize the search, I'm going to focus for a while on the Russell 2000. I don't want to do a deep dive, but if I spend just 5 minutes on each one learning the basics of who they are and what they do, I will get through all of them in less than a year even if I only do 6 a day. If I'm looking for 1 in a hundred companies, this method should produce at least 20 companies that might be great for further research. I'm going to start at the smallest companies and work my way up, starting today. A few each day. Just looking for the obvious: low PE, low P/B, lots of cash, a holding of a respectable value investor, buybacks, insider ownership etc, should not take more than a few minutes each. Anyone else want to join me?

-

Setting a multiplier when value investing (Graham/Dodd)

Saluki replied to adventurer's topic in General Discussion

All those ratios and measurements are just tools, and you have to decide what is the best tool for the job. If you have enough of those measures, P/E, P/B, EV/Sales, etc, you will eventually find one that makes it look cheap. But you probably need to do a deep dive on the industry for a stock that you are interested in to know what is the measure that is most important. In Banking it's usually price to book, in Insurance it's usually that and the combined ratio. If it's a retail company, same store sales growth is probably the most important metric etc. Graham's theories came out of the great depression, so he put more emphasis on assets (book value) than earnings because he saw how the depression (or now COVID) can make income unreliable, but the assets don't fluctuate so much. But every sword is double edged and the asset thing is hard today because most tech companies have very little assets compared to older industries. So price to book is meaningless. Also, book value reflects what you paid for it, and if you screen for it you will pick up a lot of stuff that is selling for a lot less than replacement costs, but which nobody wants. When oil was cheap, offshore drillers were selling dirt cheap. But those things are expensive to build and don't have a lot of scrap value as the cost is in the technology which is worth less the longer it's not being used and maintained. -

In founder run companies like FFH and BRK, where the insiders have most of their net worth, there is a definitely a comforting approach to risk management instead of trying to scoop up every last nickel from the poker table.

-

Odd Lots: How a Professional Sports Bettor Really Makes Money on Apple Podcasts I don't know anything about sports betting, and I didn't think serious people can do it profitably, but this podcast on how it works and how to use your edges was very informative.

-

Yesterday, I saw this company jumped 80%, and I wasn't familiar with it, so I checked it out. I don't care enough about it to start a post, but I guess here is a good place to put it. Ocean Power Technologies, Inc. (OPTT) Stock Price, News, Quote & History - Yahoo Finance OPTT is Ocean Power Technologies, and they are a nano cap that reminds me of Kraken Robotics, but their tech isn't as good and they aren't profitable. They make stuff for the oil and gas industry, and some of it has applicability to defense, which is why Teledyne Marine signed a deal with them. They also announced some deals with an unnamed US government agency. It was curious that they announced several deals but didn't mention any dollar amount. After some more digging, it looks like they are in a fight with an activist investor who says that OPTT is in financial trouble and they are refusing to let the investor, Paragon, do a non dilutive preferred investment, and are instead trying to pump up the stock price and issue shares to dilute everyone. Besides the drone stuff which they sold to the UAE, and looks amateurish, they also have some buoy that generates electricity from the sea movement, and it's all over their website. The problem with that wave electricity generation is that it's usually not feasible. It tends to be expensive and usually gets damaged in storms. It looks like they tried to partner with a big company to develop/license it but they walked away because it wasn't feasible either. This stuff would be an interesting green tech (and more reliable than wind generation) if someone could actually make it work and produce electricity at a price that makes it competitive with wind/solar. Maybe someone will figure it out, but I don't think it will these guys. I think with AI the easy money has already been made in places like NVDA, and in drones the same is true about defense contractors. But I'm still convinced that if you keep turning over stones you will find things in related industries that will benefit and are off the beaten path so they aren't noticed by the crowd. I don't think OPTT is one of those, but I'll keep turning over stones and eventually something will come up. (I have about a 1.5% each in Taylor Devices and Kraken Robotics, which are adjacent to companies that make drones, and I plan to hold them for a few years and let them compound quietly in the shadows, adding on the dips when I can.)

-

Slowly building up positions in FRPH and ENPH at these prices. Sold a little STNG and bought the same amount in Tsakos.

-

I stumbled on this podcast interview of Mitch Rales from Danaher. https://podcasts.apple.com/us/podcast/mitch-rales-the-art-of-compounding/id1154105909?i=1000654291328 The Rales brothers don't give interviews and this is the only podcast interview that Mitch has ever done.

-

The other coal stocks are up double digits today, I'm assuming that this is why. In addition to OXY, I also own some VTS which I got in the spinoff from Jeffries, and have been trimming a little lately. Both mid size positions. I also have some ENPH, which I believe will benefit both from clean energy and the need for more residential housing. They are hurting a bit now, but moving their production to the US entitles them to a lot of subsidies from the Inflation reduction act and they appear to have best-in-class tech for residential solar. I don't know if shipping counts as energy, but I have a 5% position in STNG, which is a product tanker company, and have been trimming it a bit and adding to TNP. I own a tiny bit of NEP, which I cloned from @lnofeisone . I'm not crazy about the debt but I don't mind buying some at these prices while I continue to study it.

-

This was a really great book to read on vacation, but I wish I read it at home so I could take more notes. The author talks about many disasters and how people react in ways that help or hurt their chances to survive. Common reactions to an earthquake, fire, or terrorist attacks, are doing what others are doing, freezing or panicking. Why? It includes a lot of research, including brain imaging studies (what type of brain will predict whether the person will panic and pull out their respirator under water?) . Are there things that you can do to have the right actions ready when something happens. A few fascinating takeaways were that although most disaster preparedness consists of telling people to remain calm and wait for the professionals, the "first responders" are almost never fire or police, but regular folks. In fact, of the 3800 employees at Morgan, 99% of whom survived the WTC attack on 9/11, they survived because the head of security told them to ignore the intercom message that told them to stay where they are until help arrives, and led them out right away. The warnings set up by the government are practically useless. If the terrorist alert color code goes from yellow to orange, what does that tell you to do besides worry? Shortly before the largest earthquake ever recorded happened in Valdivia, 9.5 Richter scale, a worldwide Tsumani warning system was established. The people in Hawaii heard the sirens and had over 10 hours to get ready before the Tsunami hit, yet dozens died because they heard the sirens and didn't know what it meant. There are numerous videos of firefighters responding to fires in nightclubs and the people are just standing there while the wall behind them is engulfed in flames. Why? A little bit of thinking of the worst possible event and how to respond could save your life. It's got some relevance to investing too. Like "thesis drift" and "anchoring" are applicable to both. Recognizing that something is not normal and accepting reality rather than talking yourself into complacency is a big lesson. Things like periodic exposure to stress, overcoming tunnel vision, and "tactical breathing" that are commonly used by special forces to maintain clear thinking in emergency situations are applicable to other situations that you might find yourself in. Highly recommend!

-

I was going to post something on the Citi post, but this is relevant to most banks, not just Citi, so maybe it deserves its own post since I don't see the particular topic being discussed. It's difficult to believe that all the big banks are spending so much on lobbying, including ads on streaming platforms targeted to consumers, to try to block enactment of Basel endgame, yet they are doing better than before on their stress tests. They are trying to prevent Basel endgame because holding more capital will lower your returns on invested capital. So how are they more secure, without holding more of their own capital in the firm? I don't think they are. It looks like smoke and mirrors, also know as portfolio compression. They claim that they are using AI to find ways to comply with new regulations at the lowest cost. My guess is that its one of the companies that goes through your order book and then comes up with a massive swap for hundreds of exposures to different counterparties and then does one large trade which seems to net out a lot of positions, and reduce the number of counterparties so that your positions look less risky. It's like portfolio margining on steroids. The problem is that with hundreds of smaller trades, if you or your counterparty runs into trouble, it's easy to peel off some that risk and sell it off. Asian equities? African currency? Oil? No problem. But if you have cleaned up the dregs in your book with a massive bespoke trade with a counterparty who runs into trouble, who will be willing to buy that Swiss army knife trade with so many legs that it would be hard to value, let alone hedge? The vanilla exposures are already cleared through a clearing house somewhere, and the stuff that's leftover is stuff that isn't easily cleared. (Cross-currency swaps to hedge loans in African currencies that you can't spell?). Not naming any bank in particular, but if Lehman was still around and they got in trouble. Who would buy these one off weird trades that exist to clean up your net capital, not to perform some useful function that some other bank would want? Would that have made it harder in 2008? Now replace Lehman with another bank or insurance company who is still around. I don't like companies with lots of debt in general, and I have work conflicts that keep my away from investing in many banks, but if I didn't, it's something that I would give serious thought to.

-

Bought some FRPH and ENPH.

-

I'll be in Munich, Berlin, Copenhagen and Stockholm over the next week and a half. If anyone is in those cities, feel free to message me. Cheers.

-

Well, in Bill Gates' book on climate, he mentions investing in companies where the technology isn't currently feasible in order to move the ball forward. So some of his bets may not be economic, but more like a charitable investment. Maybe the nuclear stuff is in that basket? The obvious names that will benefit from upgrading the grid have run up a lot, so that ship probably sailed. I think you might have luck in some of the smaller names or adjacent tech. Tantalus systems is a very small cap so my broker won't let me trade it, but they make smart meters and sell them, plus recurring revenue, to utilities. If using your Tesla as a battery for the grid becomes a thing, companies like this will probably benefit. I own some ATEX, which has FCC licenses that are used for 4G/ internet of things, for grid reliability (like being able to deactivate a broken wire before it hits the ground). NextNav is a company that I don't own, but they have some frequencies that are used for emergency services and GPS. They are not profitable, but one of the selling points for their bandwidth is that it's less susceptible to hacking than current GPS. Maybe that has some applicability to prevent North Korean cyberattacks on our grid? I'm sure there are some companies besides Tesla that will be making whole house battery backups.

-

I picked up a few shares of CPNG too, but it's less than 5% for me. The article I posted hasn't been on Yahoo yet, so I suspect more selling when it does, and if it hits the teens again, I may start buying in bigger size. I trimmed some VTS and STNG, and added to some smaller positions that I'm still building. (Tsakos, Kraken, FRPH).

-

Movies and TV shows (general recommendation thread)

Saluki replied to Liberty's topic in General Discussion

We just finished watching Bodkin TV series. It's like Only Murders In The Building but darker. Podcasters investigating 3 people who went missing on Halloween 20 years ago. Lots of secrets uncovered in a small Irish town and lots of plot twists to keep you guessing. -

I think the EU is a bad idea, but that doesn't make Europe uninvestable. It's like saying "Is Asia uninvestable?". China is much different than Japan or the Philippines. The underperformance of European equities has more to do with the fact that they don't have a silicon valley. Without MSFT, GOOG, META, AAPL, and NVDA, the S&P500 wouldn't be running circles around Europe. In a study I saw of countries with the most 100 baggers, it had the usual suspects: US, India and China, but Sweden was also up there. Most European countries are higher taxed than developing countries, but they also have a lack of corruption, good infrastructure, a highly educated workforce, and respect for property rights. You can argue that the industrial revolution kicked off in England because wages were so high, so it made labor saving machines worthwhile. In China many farmers still plant crops by hand. Labor is so cheap that the outlay for industrial equipment to produce food that isn't expensive is not worth the money. So, just as there is a reshoring in the US for some manufacturing to prevent another global disruption like what happened in 2020, there may be some bright spots in Europe for manufacturing that requires a lot of capital per worker (the company that makes the machines that TSMC uses to make chips is manufactured in Holland). Iceland produces way more geothermal electricity than it needs, so it became a world leader in Aluminum production, which requires large amounts of electricity. Maybe that will be attractive for crypto? Since there are no trees in Iceland, maybe it's a great place for wind power? I hate shipping, but who dominates in operating shipping companies? Greeks and Norwegians. The only American I can name who did well in shipping besides Vanderbilt is George Steinbrenner. If you look at individual companies, not countries, and focus on bottom up, not top down, I'm sure there are some gems there. It's like that old joke about the kid who's an optimist and the dad takes him to a barn piled with sh1t to the ceiling. The kid is ecstatic, and the dad asks what's the bright side of this? He says "with all this sh1t, there's gotta be a pony in here somewhere!"

-

The post (I think it was deleted) bemoaning the value of this board reminded me of this clip of an interview with Steve Cohen's performance coach. There are lots of things that are too hard for you individually, but collectively you can do a lot by putting your heads together and problem solving. Even Buffett had Munger to bounce ideas off of, and people like Bill Ackman are the public face of their funds, but they don't run one man shops.

-

Charlie Munger's Bookshelf - Help Me With Identification Please

Saluki replied to Voodooking's topic in General Discussion

I see Pinker's "the Better Angels of our Nature" and "Pre-Suasion" another Cialdini book. -

Public Company Share Repurchase-Cannibals

Saluki replied to nickenumbers's topic in General Discussion

It's a small cap, so I'm hesitant to mention it because it's not very liquid, but check out Taylor Devices. Currently P/E is 17, they bought back 15% of shares in a block trade from an insider this year. It's growing earnings and backlog for orders, and although it's structural business is tied to construction, it's aerospace/defense business is stable and they have been doing business with defense department/NASA since before I was born.