Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

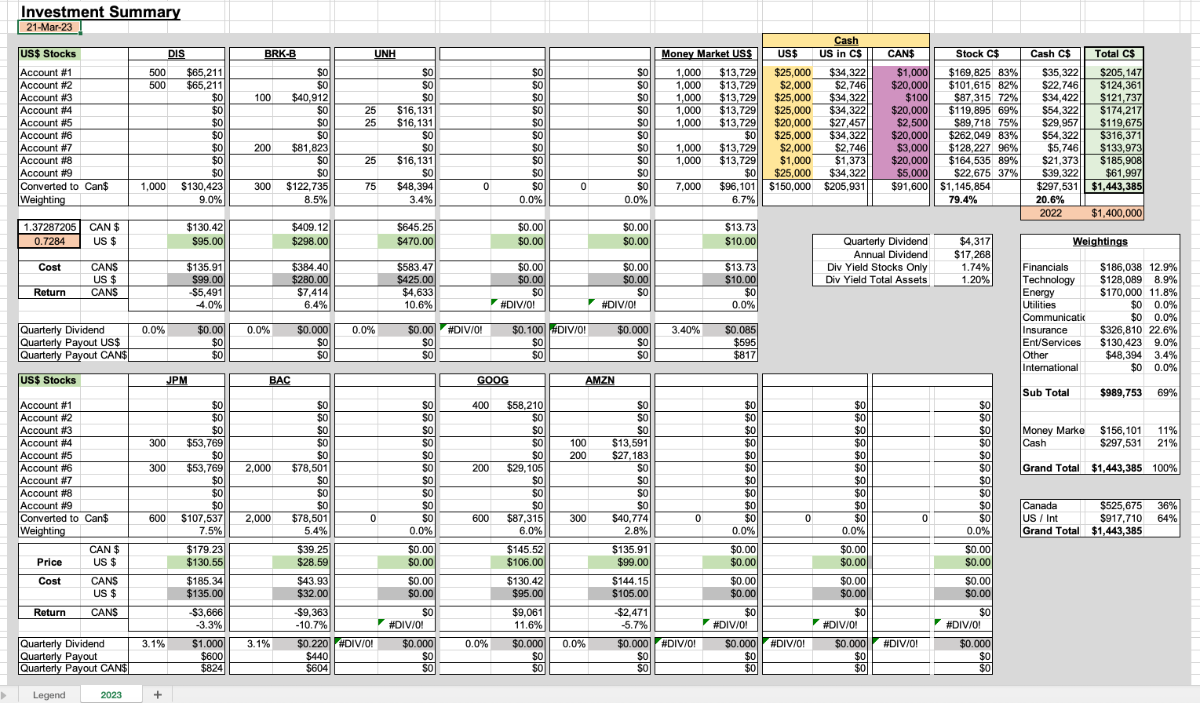

How Do You Track Your Investments Across Multiple Accounts and Firms?

Viking replied to Viking's topic in General Discussion

Here are a couple of screen shots (I made it a little prettier from the first version)...

-

Below is a reply in I made to @maplevalue in the 'Is Concentration a better strategy than Buy and Hold?" thread. I thought some people might find it useful to see exactly how I track my investments. Below I have attached a generic Excel file (tab 1 is a legend and tab 2 is the actual portfolio tracker). Please feel free to use/modify. It really is designed for a Canadian investor. But US investors might find it interesting to see the logic. I see the total value of all my accounts (top right). As I add new positions (or add to existing positions) in different accounts I immediately see the weighting of that position to my total portfolio. If I hold a basket of stocks (like US banks) I capture the total weighting in my weighting summary (top right of spreadsheet). I find this spreadsheet is useful because it captures everything I want to see in one quick view: my accounts, my wife's accounts (CAN$, US$). I track 9 accounts on this spreadsheet right now (my kids 3 TFSA's are not on the spreadsheet as they are smaller). ========== @maplevalue My family has investments in 12 different accounts. It can get confusing to keep track of everything. Confusion rarely leads to higher returns. I manage all 12 accounts as one investment (one bucket of money). I have an excel spreadsheet where i track all holdings by account and by stock. As i make trades i update my spreadsheet (takes only a few minutes). So i know in real time all the stock/sector weightings for my total portfolio. I also have average cost (as i usually hold positions in multiple accounts) and dividend information in my one page summary. Portfolio weighting is what i really care about. I find this big picture view is exceptionally important and useful. What i think about the most is: 1.) do i want to own a stock? 2.) if yes, what position size do i want? - a starter position for me is usually a minimum 0.5% to 0.75% of my total portfolio - as an example, i re-established a position in WRB again late today when the stock fell back below $60. I made it a 1.5% position. Larger than a usual starter position. But i understand the company and industry pretty well so i am ok going a little bigger. - when i make my first purchase of a stock i also think about how big i want to make it should the stock keep selling off. I would be comfortable taking WRB to a 5% position (of my total portfolio) - assuming no change in the story. 3.) what account do i want to hold the stock in? - tax free or taxable account? Etc etc… —————- Every Dec 31 of each year i ‘freeze’ my Excel spreadsheet. I create a copy and make updates in the new year to the new spreadsheet. I also have a summary page that pulls the total values (for each account) from each spreadsheet. I also capture deposits/withdrawals made that year (RESP, RRSP, TFSA, taxable accounts). My records now go back 25 years. So i know exactly what my long term results have been. For every account. And in total. Factoring in deposits and withdrawals. Yes, a little work along the way. But extremely helpful/useful. Most of the work is getting it set up. Investment Tracker.xlsx

-

Is Concentration a better strategy than Buy and Hold?

Viking replied to Viking's topic in General Discussion

@maplevalue My family has investments in 12 different accounts. It can get confusing to keep track of everything. Confusion rarely leads to higher returns. I manage all 12 accounts as one investment (one bucket of money). I have an excel spreadsheet where i track all holdings by account and by stock. As i make trades i update my spreadsheet (takes only a few minutes). So i know in real time all the stock/sector weightings for my total portfolio. I also have average cost (as i usually hold positions in multiple accounts) and dividend information in my one page summary. Portfolio weighting is what i really care about. I find this big picture view is exceptionally important and useful. What i think about the most is: 1.) do i want to own a stock? 2.) if yes, what position size do i want? - a starter position for me is usually a minimum 0.5% to 0.75% of my total portfolio - as an example, i re-established a position in WRB again late today when the stock fell back below $60. I made it a 1.5% position. Larger than a usual starter position. But i understand the company and industry pretty well so i am ok going a little bigger. - when i make my first purchase of a stock i also think about how big i want to make it should the stock keep selling off. I would be comfortable taking WRB to a 5% position (of my total portfolio) - assuming no change in the story. 3.) what account do i want to hold the stock in? - tax free or taxable account? Etc etc… —————- Every Dec 31 of each year i ‘freeze’ my Excel spreadsheet. I create a copy and make updates in the new year to the new spreadsheet. I also have a summary page that pulls the total values (for each account) from each spreadsheet. I also capture deposits/withdrawals made that year (RESP, RRSP, TFSA, taxable accounts). My records now go back 25 years. So i know exactly what my long term results have been. For every account. And in total. Factoring in deposits and withdrawals. Yes, a little work along the way. But extremely helpful/useful. Most of the work is getting it set up. -

Is Concentration a better strategy than Buy and Hold?

Viking replied to Viking's topic in General Discussion

@dealraker As per usual, your comment did not disappoint! As i get older, I am starting to think a little about the future… a future when i am no longer around (hopefully many years away). Or if i am hit by a bus tomorrow. What happens to what i have built? I really like your strategy: 1.) establish a culture with the next generation: buy stocks and hold them for the long term 2.) time tested strategy: “wealth is built from holding the stocks of productive businesses” I understand that my strategy is not repeatable by anyone in my family. I will leave them (hopefully) a bucket of $. But nothing more (as it sits today). I leave them fish. But i have not taught them how to fish. Thanks… lots to think about. ————— i some ways, i may be setting my kids up for failure… because i am role modelling the wrong behaviour (regardless of how well it is working for me). -

Is Concentration a better strategy than Buy and Hold?

Viking replied to Viking's topic in General Discussion

@ICUMD Fairfax India’s stock - for me - has felt a little like a mermaid’s siren call drawing ships to wreck. That is a really unfair thing to say as i do think Fairfax India is managed very well. But the stock really is challenging: - confusing (trades in US$ on Canadian exchange) - illiquid (i can move the price when i try and flex a position higher or lower) - ever shrinking float of shares available to public (both Fairfax India and Fairfax have been buying back stock) - perpetually undervalued (at least the past 4.5 years) - unpredictable catalyst (timing of company buying back stock) - parent (Fairfax) who is profiting greatly from undervaluation (methodically, materially growing ownership percentage each year). I have held a large position a couple of times over the years. But i am lucky not to have been burned (just singed). Having said all that, i do think the stock is very cheap. I do own a little Fairfax India. And i do flex my position up and down a little. But i now keep it small. Good luck!

-

Is Concentration a better strategy than Buy and Hold?

Viking replied to Viking's topic in General Discussion

@Paarslaars i agree that concentration is a terrible strategy for the ‘average’ investor. My view is the ‘average’ investor should buy the Index via ETF’s and be done with it. Most average investors won’t get the return an Index gets. My point is if you want outsized returns (much better than the Index), concentration is one viable path. IF YOU ARE ABLE to figure it out/find the right fit. i think 8% is a reasonable long term return for most equity investors moving forward. If your goal is 10% why bother with active management? It is so close to 8% just go with Index/ETF’s. Save time. Cost. And stress. But if you want to really outperform the index… something like 15% or higher every year? Buy and hold? Maybe. But i think it is unlikely. Concentration? Possible. But you have to be good. And that is the rub. Perhaps the lesson for ‘average’ investors is to be open to the idea. When the stars align (when something you understand exceptionally well gets wicked cheap). ‘Buy and hold’ is a solid idea. So is diversification (especially if you don’t know what you are doing). Concentration? For some investors it can play an important role (those that fully understand the risks). -

Is Concentration a better strategy than Buy and Hold?

Viking replied to Viking's topic in General Discussion

Here is what Druckenmiller had to say about concentration as a strategy: ---------- Stanley Druckenmiller: When I’ve looked at all the investors (that) have very large reputations — Warren Buffett, Carl Icahn, George Soros — they all only have one thing in common. And it’s the exact opposite of what they teach in a business school. It is to make large concentrated bets where they have a lot of conviction. They’re not buying 35 or 40 names and diversifying. I don’t know whether you remember that Icahn a few years ago put $5B into Apple. I don’t think he was worth more than $10B when he did that. [In 1992] when I went in to tell Soros that I was going to short a 100% of the fund in the British pound against the Deutschmark, he looked at me with great disdain. He thought the story was good enough that I should be doing 200%, because it was sort of a once-in-a-generation opportunity. So, [these investors] concentrate their holdings. This is very counterintuitive. In my thinking, [concentrating your bets] decreases your overall risk because where you tend to be in trouble is if you have 35 or 40 names. If you start paying attention to one. If you have a big massive position, it has your attention. My favorite quote of all time is maybe Mark Twain: “Put all your eggs in one basket and watch the basket carefully.” I tend to think that’s what great investors do. - https://thehustle.co/stanley-druckenmiller-q-and-a-trung-phanin/ -

I was crafting a response to @RedLion in the 'what are you selling' thread. I thought my response (which just kept getting longer) probably warranted its own thread as it might resonate with others who want to discuss it. Concentration, not buy and hold, has been my secret sauce for the past 25 years. This strategy has delivered for me an average total portfolio return of 19% per year over 25 years (each of my first 3 years had negative returns). So, from my perspective, 'concentration' is a better strategy than a simple 'buy and hold' strategy. My comment to @RedLion is it is easy to do well when you are concentrated in a stock that outperforms the market over multiple years. Lots of volatility along the way also helps (allowing for a position to be 'flexed' up and down). And that has been Fairfax for the past 30 months. Important: my goal is NOT to concentrate my portfolio. I take what Mr. Market gives me (I try and be flexible and opportunistic). My preference is to be diversified. But when Mr. Market gets stupid with one or more positions (which happens lots) then I am happy to concentrate. To fund this increase in position size i use cash or I sell the stuff in my portfolio that i have less conviction in. Key: it is the concentration that drives the outsized returns over the years. Of course there are many factors that drive an investors performance over decades. While I think concentration has been the most important factor impacting my performance (in terms of return) there are others. I pay attention to macro. I also am ok carrying large cash balances. I follow a pretty narrow range of companies and industries (although this has expanded over time). ----------- In terms of 'flexing' a position: - Canada has a number of tax free accounts for investors (RRSP, LIRA, TFSA, RESP). (Before my wife and i sold our house in 2021 all of our investments were in tax free accounts.) I do most of my ‘flexing’ of positions in my RRSP and LIRA accounts (Revenue Canada doesn't care what you do - in terms of trading in and out of positions - in those accounts). - low fee (self-directed) accounts also makes executing this strategy easier. (Of interest, i used a full service broker up until around 2012. In 2012, i got a new financial advisor at RBC Dominion Securities and she told me my portfolio was too concentrated and i HAD to diversify it. My previous adviser was a buddy from high school - he got pushed into a new role at RBC. After the third phone call with the new advisor i decided it was time to flip all of my families investments to self directed accounts where RBC would leave me alone.) Not having to think about taxes is a big benefit. Paying a minimal amount to execute trades is another big benefit. I understand these two things help greatly when concentrating/flexing a position. --------- Real life example #1: when I left Kraft Foods in 2004, I was given two options with my pension: 1.) leave it with Kraft; they manage it and i get some unknown amount when I retire, or 2.) take a lump sum amount with with me and deposit it into a LIRA and manage it myself. I went with option 2. So my lump sum payout was $30,208 back in 2004. Today that LIRA is over $1.1 million = 19% annual return. (When I left Kraft taking my pension with me was an after-thought. It has since become a financial home run. It really is crazy how things turn out sometimes. I call that phenomenon ‘positive unintended consequences’ when taking calculated risks in life… Well thought out actions usually turn out exceptionally well because the downside risks are usually well understood. But my experience is there are always a few meaningful ‘unintended positive consequences’ - unknowable at the time you make the decision - that make a good decision even better than initially thought.) Real life example #2: after our third child was born (2003) my wife and I set up a group RESP. We deposited $2,000 for each child ($6,000 total). The government kicked in 20% so we started with $7,200 in 2003. My kids are all in university right now. Total 'value' of the account is $202,500. (So far we have pulled out $117,500 to fund their educations and the current account balance is $85,000). Annual return has been a little under 17%. Our $2,000 initial investment back in 2003 will pay about 70% of each of our kids post-secondary education. (I use this as a real life example with my kids to teach them the power of compound interest. Hopefully it will motivate them to take personal finance seriously when they start earning big girl/boy money after they graduate.) Bottom line, concentrating/flexing has delivered solid returns over a 25 year period. It works. (I don't think it was luck.) ---------- I have had this 'flex' strategy with Fairfax going back to 2003. Yes, it all started 20 years ago. My portfolio was up 87% in 2003 and it was mostly due to Fairfax. In hindsight, Fairfax had issues in 2003 that I did not fully appreciate. Some dumb luck involved there, for sure. But I'll take it. (Lots of people on this board at the time held my hand and helped me through the dark days of the short attack on Fairfax. Sanjeev. Bsilly and others.) Fairfax fell out of favour again in 2006 (can't remember why). At the same time it was sitting on a massive credit default swap position (aka 'The Big Short'). As the housing/financial system in the US blew up, Fairfax made billions over the next couple of years. Mostly due to Fairfax, my portfolio had 4 straight years of stellar returns: 2006 (+29%), 2007 (+47%), 2008 (+17%) and 2009 (+31%). Bear market, strong upward trend that lasted years and lots of volatility - does this sound familiar? When I concentrate in a position I try not and leave it super concentrated for long periods of time. Sometimes there is a catalyst involved that should spike earnings and that always spikes a stock price (eventually). More lately, Fairfax got wicked cheap again in late 2020. I remember Sanjeev pounding the table on this board in 2H 2020 about how ridiculously cheap Fairfax was at the time. I got aggressive buying Fairfax in Oct and when the vaccine news came out in Nov, 2020 i backed up the truck on Fairfax. 2021 and 2022 have been my two best years ever in terms of total return. And 2023 has started out great. For the past 30 months we have had a strong upward trend and lots of volatility. Today Fairfax is a 29% position for me. ---------- There are times when the stars align for Fairfax (in terms of what is going on under the hood) and it is poised to make a bunch of money. Often, at the exact same time, the stock is deeply out of favour (2006)/hated (2020). The really interesting thing is 'the story' is out there for all to see and the stock still sells off. Conviction is important. And to have this you have to have a good understanding of the opportunity. Back in Sept/Oct 2022 we all knew Fairfax was sitting on a $1 billion after tax gain from selling its pet insurance (that no one know they even owned, it was such a small business). When this deal was announced the stock... sold off! At the same time, spiking interest rates was driving future interest income through the roof. And we were in an insurance hard market, which was driving 20% top line growth and record underwriting profit. What did the stock do? It sold off to US$450 in October. NUTS. What is a rational investor to do? Back up the truck. When the stock pops higher I lighten up (I sell back down to my core position size over time). I am happy to book profits (that whole 'pigs get slaughtered' thing). I have never owned Fairfax as a buy and hold stock (or any stock in my portfolio). I own it when it is cheap. I back up the truck if/when it gets crazy cheap. When the stock gets fully valued I likely will be completely out of it (and will stop following it so closely). Over the years, I have used this strategy with other stocks. Fairfax is just the best example because of its frequency. Back from 2013-2015, I was banging the table on Apple (you can go back and read my posts on the Apple thread... similar to Fairfax today). My returns: 2013 (+32%), 2014 (+29%), 2015 (+19%). Mostly driven by Apple. I wasn't even following Fairfax during these years. (Before i invested in Apple i owned Blackberry for a brief time. By the third conference call i realized Blackberry management was a mess so i sold my position at a high single digit loss. Bad decision… right? Wrong. Buying Blackberry was a great decision because it taught me about the cell phone industry. When Apple got cheap a short time later i was ready. Without investing in Blackberry i never would have bought Apple. And that is one of the really cool things about investing… it is constantly giving you opportunities to turn adversity/failure into triumph.) Of interest, when i was exiting my oversized position in Apple in 2015/2016 some dummy named Warren Buffett was JUST STARTING to buy shares. Another really cool thing about investing: you can do lots of really stupid things and you can still do really well. Another example of concentration was when I went 100% cash in Feb 2020. A global freight train - the virus - was coming. Here in North America we watched it hit Asia first and then a week later it hit Europe. We knew what was coming and we knew it was going to be devastating. About a week later we saw the virus wipe out the two care homes in Washington State and completely paralyze the health care system/society. NOT going to 100% cash at the time seemed irrational to me. ---------- There was only one time where I got messed up with this strategy and was in 2018. I was concentrated in BAC and the market decided they needed to throw a tantrum to get Powell to pivot from his tightening strategy. Stocks dropped 20% in December 2018 and financials got killed (down even more in a couple of weeks). Fortunately, I got lucky. Powell caved and stocks rocked in January 2019, led by financials. My analysis on BAC was solid. Sometimes that doesn't matter. ---------- 'Buy and hold' is a great strategy. I love reading @dealraker 's posts. Part of me wishes I could invest like he does. Holding ETF's is another solid strategy. However, I also think Druckenmiller is on to something with the whole concentration thing. The key is knowing when to concentrate. And how much to concentrate. And when to take profits (and sometimes losses when the market moves against you/you are wrong). I laid this out above in detail because I wanted investors on this board to understand that there is no 'right way' to invest for everyone. There are many different right ways. And you see this in spades from all the exceptionally smart people who post on this board. The key is to find a strategy that fits for you (intellectually, emotionally, age, level of interest, commitment level, life situation etc). This will happen by keeping an open mind, constantly learning, trying different things and being rational. My strategy works for me. And I understand it will not work for most investors. I definitely do not recommend it to my friends/family... I tell them to buy ETF's. I hope that by sharing this it will stimulate lots of good discussion. And thinking. That ultimately delivers better returns to everyone on this board. Best of luck!

-

Lucky. My view is in a bear market one goal for investors should be to not lose money (at least that is one of mine). That capital preservation thing Buffett talks about: ‘Keep what you got.’ My gut told me this weekend (after doing a bunch of reading/thinking/processing) i was getting out over skis with the equity weighting in my portfolio (it was up to 70%). Stocks popping higher the past 2 days gave me my opportunity to do some rebalancing in my portfolio (sell on strength). I bought my dividend portfolio last week primarily to get a dividend yield of 5.7% over the next year (that is what the yield on the basket of stocks i purchased worked out to). Well Mr Market offered up a 3% gain in less than a week. And the proceeds are now in cash earning 4% so i lock in a higher 7% return risk free (with zero volatility). Plus by sitting in cash i can reload should stocks sell off again (my guess is they will). I continually trade in and out of Fairfax. I have a very big core position that i am happy to hold. But i also buy chunks of shares on big dips (like we saw last week when it dropped under US$635). Today it is trading at $665. Of course, i do not hit the absolute low (on the buy) and high (on the sell). But if i can make a quick 2 or 3% on a trade on a stock that is undervalued (on 100 or 200 shares at a time) i am happy to do it. And if the stock keeps going lower i am happy to simply hold a larger position. I sold down my oil position simply because it was getting too large (that gut thing). At the end of the day, no one knows where the price of oil is going over the next year (with a high degree of certainty). I love the set up for oil. But i also understand what i do not know. That sleep well at night thing.

-

Sold a bunch of the stuff i bought last week. Happy to lock in some nice small gains. Up about 3% on average (FFH, RJF, SF, BCE, T.TO, SLF, CWB, BNS, CM etc). Everything was held in tax free accounts. I also lightened up on my oil holdings (CNQ and SU) - no gain here… just decided is was getting too overweight. Moving proceeds back in to money market type funds that pay 4% (risk free). Back to 50% cash. Fairfax continues to be my largest weighting (by far). Oil is #2 and big US banks is #3. What did we learn over the past 2 weeks? Higher interest rates are starting to break things in the economy. Banking crisis with regional banks is likely to tighten credit moving forward. Commercial real estate (and highly levered parts of the economy) is now getting onto investors radar. I think we continue to be in a bear market. My focus right now is capital preservation. My total portfolio is back up a little over 10% YTD. No need to try and be a hero given the current risk/reward set up.

-

At the 24 minute mark the hosts provide a good summary of the differences in accounting for banks between the US and Europe. Bottom line, Europe stress tests the bank for interest rate risk (across their entire business) and the US does not. They say JPM is one of the few US banks that runs/published its total interest rate risk. They also feel the real issue at many regional banks in US is credit risk. They account for 80% of all commercial loans; these loans tend to be concentrated (so when issues arise, these banks tend to blow up). i appreciate getting a European perspective on the current financial crisis.

-

i agree that insurance is different from banking. Here is the piece i do not understand… when interest rates were falling the past 5 years to essentially zero in 2020/2021 did all these P&C insurers not book massive ($billions) in gains on their fixed income holdings? It looks to me that when interest rates were falling the gains from most of the fixed income portfolio flowed through the income statement and book value. I would have expected that in Dec 31, 2001 there should have been billions of gains sitting in the ‘held-to-maturity’ portfolio at all these insurers. But now that interest rates have spiked higher massive losses are suddenly showing up… and have conveniently been tucked into the ‘held-to-maturity’ bucket so losses do not flow through the income statement. Is my understanding correct? Essentially, the gain (from cratering interest rates) is allowed to flow though the income statement but the loss (from spiking interest rates) is not allowed to flow through the income statement? There is a logic here i do not understand. If anyone has an answer i am all ears.

-

Happy to add to my already oversized position in FFH today. Price traded at $635 for much of the day. Stock is down 9% off its recent highs. BV is $658. My guess is they will earn $130/share in 2023. My guess is Q1 earnings will come in around $35/share. They paid a $10 dividend in January. So my guess is March 31, 2023 BV will be about $685 ($658 + $35 - $10 = $685). But what about its $38 billion fixed income portfolio. Rising interest rates over the past year must have resulted in billions in held-to-maturity losses… right? Wrong. As crazy as it sounds, Fairfax fixed income portfolio was positioned perfectly on Dec 31, 2022. It is a big, big WINNER from rising interest rates. It is better positioned than any large financial institution i know (bank, insurance etc). Most insurance companies are sitting on billions of held-to-maturity losses right now. These losses did not flow through the income statement. These losses did hit book value (so most now prefer to report ‘adjusted book value’). Yes, the held to maturity losses don’t matter. Silicon Valley Bank thought the exact same thing 10 days ago… and it didn’t matter. Until something happened THAT NO ONE THOUGHT WOULD HAPPEN. Well, now all those held-to-maturity losses do matter. so much so that Silicon Valley Bank is out of business and its shareholders have been wiped out. An accounting gimmick resulted in poor decision making at financial institutions (they did not manage their interest rate risk properly). That is now resulting in a loss in confidence in the financial viability of many financial institutions. An interest rate risk has quickly and unexpectedly morphed into a solvency issue. It will be interesting to see how investors discount held-to-maturity losses on insurance companies books moving forward. Insurance is different? Really? That is what banks thought 10 days ago too. And it was right. Until is wasn’t. I would imagine insurance regulators are probably better understanding which insurance companies a have large held-to-maturity losses sitting on their books. Does this force more conservatism at insurance companies moving forward (i.e. slower growth)? Does this extend the hard market? Bottom line, financial system panics are never a good thing. So at a share price of $635, Fairfax shares are trading at a P/BV of 0.93. Cheap. For a company that is poised to grow earnings by $130 in 2023. This is an effective earnings yield of 20%; or a P/E = 4.9. That is very cheap. And a company that is a big winner of rising interest rates… I hope the stock keeps going lower in the current financial panic. Fairfax stock has become the gift that keeps on giving (rising stock price with big swings happening 2 or 3 times a year).

-

Added to FFH. Added RJF and SF to my US bank/financials basket. Added TD to my Canadian dividend basket. Cash is down to 30% position.

-

Is First Republic dead man walking? Credit downgrade to junk can’t be a good thing. Followed by ‘rumour’ it is up for sale? Not something a consumer/business customer wants to hear. It will be interesting to see if any banks actually get sold and to whom. ————— First Republic Bank, which was downgraded to junk by S&P and Fitch, is looking at a possible sale: Bloomberg https://ca.finance.yahoo.com/news/first-republic-bank-downgraded-junk-020341444.html Ratings agencies S&P Global and Fitch cut First Republic's credit rating to junk status. The bank is now considering various options, including a sale and boosting liquidity Bloomberg reported. It could attract interest from larger lenders if it goes on sale. First Republic Bank is considering various options, including a sale, Bloomberg reported Wednesday, citing people with knowledge of the matter. The bank is expected to attract interest from larger lenders if it goes on sale, per Bloomberg. The San Francisco-based lender is also looking at options to boost liquidity, per the news outlet. Ratings agencies S&P Global and Fitch had cut First Republic's credit rating to junk status earlier on Wednesday due to concerns that depositors could pull funds from the lender. First Republic has been assuring customers of its liquidity since the implosion of Silicon Valley Bank — which in turn triggered concerns about the financial health of regional banks. On Sunday, First Republic said it was getting $70 billion of additional funding from the Federal Reserve and JPMorgan Chase after its share price slumped sharply amid Silicon Valley Bank's implosion. "We believe the risk of deposit outflows is elevated at First Republic Bank despite the actions of federal banking regulators and the bank actively increasing its borrowing availability to mitigate risk associated with the bank failures over the last week," wrote S&P Global Ratings analysts Nicholas Wetzel and Rian Pressman. First Republic's share price closed 21.4% lower at $ 31.16 apiece on Wednesday. They are down 74% so far this year.

-

Basket of Large Cap US Financials - No Brainer Buy Today?

Viking replied to Viking's topic in General Discussion

@Dinar those are all good questions and i am not an accountant or an expert on banking. So the short answer is i am not really sure how exactly it all plays out. That is why i am suggesting a basket approach. And as we learn more, tweaks can be made. Today i sold some BAC and initiated a position in JPM (even though i think JPM is more expensive). So i will manage my weighting based on who i like the best. But i also understand there is much i don’t know. So i also don’t want to go all in on one or two names. My plan is to also go wide with exposure; so include all 4 big banks, MS and GS and probably also AMEX. I just think these are exceptionally strong, well run franchises. This is not a super high conviction trade for me. I like the current risk/reward set up. But it is a very fluid situation. I will be flexible as more information becomes available. In terms of deposits at the big banks, i think they will continue to be quite sticky. Especially if the big banks are perceived to be safe havens (which appears to be happening). In a banking crisis people are not thinking about the interest rate on their checking account. They are thinking about if the safety of the money in their checking account. In terms of interest rates, we may well have seen peak rates for this cycle. Interest rates across the curve are much lower today. So led-to-maturity losses are already much lower for all banks. We will learn much more on this front when banks report Q1 results in another month or so. In terms of commercial loans i think BAC is pretty well positioned compared to peers (i might be wrong). -

Is buying a basket of the too big to fail US financials not a no-brainer trade today? I am thinking equal weight positions in JPM, BAC, WFC, C, MS and GS. They look like they will be big winners from the current panic. We know deposits are fleeing from the regional banks to these institutions. Credit Suisse is close to being put out of its misery. The winners? Yup, the big boys. Will it be a rocky couple of months (maybe even a year)? Yup. But as we emerge on the other side of this bank panic they will be even more dominant. There are more shoes to fall. Commercial real estate looks like the next shoe to drop. The panic hitting regional banks will just get worse as more ‘surprises’ on their books get revealed. Interest rate risk (rising rates) + market risk (current bank run) + credit risk (shit like commercial real estate) = category 5 hurricane for regional banks The big banks were at the epicentre of the banking crisis in 2008. They were the cause of it. It took the big banks 7 years to emerge from the last crisis. This time around, the banking crisis is different. The big banks are in much, much better shape this time. So they will emerge from this crisis faster, stronger and larger. Just depends on how bad things get. There likely will be some short term pain… perhaps a year or so of lower earnings. But looking out a couple of years, there is a lot to like. What are the risks? 1.) new regulations reducing profits (or forced capital raises diluting existing shareholders) 2.) government deciding big banks are the new oil: evil incarnate How to play the opportunity as an investor? 1.) start with a core position (basket - equal $ weights for each company you like) - big enough total position you are happy if stocks run away from you higher - small enough you can add to your position on weakness 2.) perhaps add 20%- 30% to position on declines (perhaps for every 5% decline - on average - of the stocks in your basket). Another way would be to buy a large cap ETF but you would not have any control over the weightings.

-

Michael Kofman has been one of my go-to’s when wanting to get an update. He just returned from a trip to Ukraine to get first hand information. He expects a Ukraine offensive in the coming months (after Ukraine is re-armed by the West). He expects something decisive to happen. He is normally pretty guarded so that surprised me.

-

When looking at fundamentals i think the key is your timeframe. If your timeframe is the next couple of months then, yes, the fundamentals for oil are weak. That is because for the first 5 or so months of the year, supply usually outstrips demand. Oil inventories build. And then as we hit June/July then demand starts to outstrip supply (driving/flying spikes). And oil inventories shrink. This dynamic was known a week ago. When i look out 12-24 months i continue to like the fundamentals for oil. Why? - demand from China will increase in 2023 from 2022. How much? My guess is 1 million barrels per day - global demand (ex China) will continue to increase; likely 500,000 or so barrels per day (primarily India and the rest of the developing world). - SPR drawdown has almost ended; 800,000 barrels per day of supply is being removed from the market (and i think the plan is to replenish supplies when oil trades below $70 which would add to demand). - we will see some new supply from US shale of about 500,000 barrels per day. Interestingly it appears growth from shale is slowing and might plateau in the next couple of years. - Russia, is of course, a big wild card. It makes sense to me Russia production will not remain at 2022 levels (given sanctions and exit of oil services companies) and will likely be lower. reduction in supply of 500,000 barrels per day makes sense. OPEC? US shale is no longer in control of the oil market. OPEC is back in control of the oil market. This is perhaps the most important factor in todays oil market. People are anchored to the ‘shale is in control’ narrative. They are playing checkers (as usual). That is because investors expect the recent past to play out again in the future. Instead, investors need to read up on their 1970’s history… the last time OPEC was firmly in control. How did that go for oil prices and US consumers? Not pretty. But i know, the 1970’s price spike was all about geopolitics. So what is going on today on the geopolitical front? it is just as bad as back in the 1970’s. The West is at war with the ‘authoritarian block’ led by China and Russia and it is getting worse. Where do the gulf countries sit? Increasingly, it appears they are siding with the ‘authoritarian block’. Why? The middle eastern countries are sick and tired of being lectured to by the West. Trudeau/Canada called out Saudi Arabia for (pick a reason) and Saudi Arabia severed all ties (including pulling all international students out of the country). Biden gets elected and personally attacks the Saudi leader over the Kashoggi murder. Seriously? Do people think Saudi Arabia wants anything to do with the US or Canada right now? What Saudi Arabia does know is the ‘authoritarian block’ will STAY OUT OF ITS DOMESTIC POLITICS. Qatar is likely still seething over the extremely negative coverage it got in the West before and during the recently held world cup. Biden’s trip to Saudi Arabia right before the US election with cap in hand was instructive. The fact the Saudi’s/OPEC cut production weeks later (the ultimate f-you) is even more instructive. Its not a fluke that China just brokered a deal between Iran and Saudi Arabia. Having a common enemy (increasingly the West) can create strange bed fellows. And that is how geopolitics works (not naive notions like ‘right’ and ‘wrong’). So what does this have to do with the price of oil? OPEC+ (including Russia) is firmly in control of the oil price. Oil will be priced where they want it to be. My guess is they want oil priced between $80-100. High enough they can provide a good life for their citizens. But not so high it will spur the West to action. The wild card is Ukraine (that geopolitical thing). Sounds like we will likely see a Ukraine offensive in the coming months. It it is successful then Russia will respond. How? No idea. But they are a very important oil producer…

-

If history is any example, the stock market might try and help convince the Fed to end rate hikes. And then try and convince the Fed to actually start easing. So my base case is to expect some pretty wicked volatility. So the market averages continue to swing in big directions both down and then up… but with a flat to downward bias in the coming months. What is an investor to do? Active management will likely outperform simply buy and hold in the coming months. As we get to the bear market bottom, likely later this year, then buy and hold will likely outperform from that point forward. Obviously, just a guess. But it is useful to have a plan.

-

Investing for the past 10 years has been all about following the Fed. When they are easing it is risk on for assets (stocks, bonds and real estate). When they tighten it is risk off for assets. Now it's pretty useless to debate whether this is good or not - that does not put food on the table. The simple question is what do they do moving forward. And how can investors profit? Do they continue with their tight monetary policy? Is inflation still public enemy #1? Or do financial stability concerns cause a pivot to a more accommodative policy? Super interesting times! And probably a good idea to fasten the seatbelt... the ride from here could get even more rocky.

-

The sell off in oil is a gift for investors that can handle the volatility. The fundamentals have not changed much. In fact the fundamentals are getting better as companies will be reigning in spending on increasing production. The sell off in oil is being driven primarily by sentiment. The sell off is great for oil companies. Yes, even at $68 oil they are still making buckets of money. Over the last 2 years they have completely deleveraged their balance sheets. Most oil companies are now returning 50-75% of free cash flow to investors. The problem with buybacks is they are usually done at high prices. Significant buybacks in the coming months (at very low prices) will be very accretive for shareholders. Today both SU and CNQ have dividend yields of 5.5%. Very good in a low interest rate world. Oil stocks (and the oil market) continue to be very mis-understood by investors.

-

Built out a portfolio of Canadian high dividend payers. 5% of my portfolio. Average dividend yield is 5.8%. With interest rates cratering, my guess is dividend paying stocks are positioned very well. Will build this out on stock market declines. - Communication: T.TO, BCE - Banks: RY, BNS, CM, CWB - Utilities: ENB, TRP - Life insurer: SLF

-

Added to SU. Starter positions CNQ, JPM, MS, WRB. - not much has changed with oil from a fundamental perspective. Sentiment stinks. Love one day 10% declines in stocks when it is being driven by sentiment.

-

BAC, WFC, C, SU All down more than 5%. It looks to me like the big banks will be the big winners. The business at all the small banks that are going under will need to squish somewhere.